%201.svg)

¿Qué es una reclamación del titular de una tarjeta? Guía para comerciantes sobre las normas, los plazos y los códigos de motivo de las reclamaciones de pago

Contracargos?

Ya no es problema tuyo.

Recupera cuatro veces más Contracargos y prevención , hasta un 90 % de las entradas, gracias a IA y a una red global de 20 000 comerciantes.

El término «disputa del titular de la tarjeta» tiene diferentes significados para cada persona: puede ser una llamada de un cliente a su banco, un sinónimo de «contracargo» o una categoría específica de códigos de motivo de Mastercard. disputas entre fraudes reales, problemas causados por el comerciante —como descripciones de facturación poco claras— y fraudes «amistosos». Las cuatro redes no comparten un mismo conjunto de normas: los códigos de motivo, los plazos de escalado y los umbrales de supervisión difieren entre sí. Para cuando llega una notificación, el banco ya ha actuado; la fase de investigación es el momento más económico para resolver un caso. Los plazos de presentación de reclamaciones por parte de los titulares de tarjetas son, de media, de 120 días; los plazos de respuesta de los comerciantes son mucho más ajustados. La prevención consiste en gestionar los índices y detectar el fraude amistoso, no solo las tarjetas robadas.

- Cada reclamación de un titular de tarjeta lleva asociado un código de motivo específico que te indica exactamente qué pruebas debes recopilar.

- Los datos de autenticación (3DS, coincidencia de AVS/CVV) constituyen la mejor defensa frente a disputas por «transacciones no autorizadas».

- disputas por «no se ajusta a la descripción» como las de «no se ha recibido» se basan en la documentación elaborada antes de presentar la disputa, no después.

- disputas por cobros duplicados suelen disputas más rápidamente con un reembolso en el mismo día y un registro de confirmación.

- Asignar de antemano los casos de tu base de datos a los códigos de motivo reduce el tiempo de respuesta y mejora las tasas de éxito.

Una reclamación del titular de una tarjeta es una solicitudes cliente presenta al banco emisor de su tarjeta para que se anule un cargo, normalmente alegando fraude, falta de entrega o una discrepancia entre lo que se pidió y lo que se recibió. Cada reclamación lleva asociado un código de motivo específico que indica al comerciante exactamente qué debe demostrar. Conocer el código de motivo desde el principio es la forma más rápida de reunir las pruebas adecuadas y responder dentro del plazo establecido.

| Código de motivo de la reclamación | Descripción | Cómo responder |

|---|---|---|

| Visa 10.4 – Otros tipos de fraude, entornos sin tarjeta física | El titular de la tarjeta afirma que no autorizó una transacción por Internet o por teléfono | Envía la coincidencia de AVS/CVV, los datos del dispositivo y la dirección IP, así como el historial de compras anteriores, si está disponible. |

| Mastercard 4837 – Sin autorización del titular de la tarjeta | El titular de la tarjeta niega haber autorizado la transacción | Facilita los registros de autenticación (3DS), la dirección IP y el historial de inicio de sesión de la cuenta. |

| Visa 13.1 – Mercancías o servicios no recibidos | El titular de la tarjeta afirma que el pedido nunca llegó | Enviar el seguimiento con confirmación de entrega y marcas de tiempo de tramitación |

| Mastercard 4853 – No se ajusta a la descripción | El titular de la tarjeta afirma que el artículo no se correspondía con lo anunciado | Facilita el anuncio original, las fotos y las especificaciones del pedido que coincidan con lo enviado |

| Visado 12.6 – Tramitación de duplicados | Al titular de la tarjeta se le cobró dos veces por una misma compra | Mostrar los registros de transacciones que demuestren que solo hay una autorización y una liquidación válidas |

| Mastercard 4834 – Tramitación de duplicados | La misma transacción se ha facturado más de una vez | Reembolsa el importe del duplicado inmediatamente y envía la confirmación del reembolso como prueba. |

disputas de los titulares de tarjetas disputas convertido en una verdadera carga para todo el ecosistema de pagos. Una reclamación rara vez se queda en eso. Alrededor del 60 % acaba convirtiéndose en Contracargos completa. Y, una vez que eso ocurre, ya has perdido los fondos. Ahora tienes que esforzarte por recuperarlos, no solo por explicar un cargo.

Una parte significativa de estas disputas un fraude en el sentido tradicional. Según Mastercard, una cuarta parte de todos sus Contracargos se debe Contracargos a transacciones recurrentes, en las que los clientes intentan cancelar una suscripción o, simplemente, no reconocen un cargo. Los estudios de Visa lo corroboran. El 35 % de los titulares de tarjetas confunde una transacción legítima con una fraudulenta, y el 70 % de quienes han impugnado un cargo da por sentado que un cargo no reconocido es sinónimo de fraude. Esto significa que una buena parte de disputas de los titulares de tarjetas contra disputas luchando podrían haberse resuelto con un proceso de cancelación, una descripción de la factura más clara o una alerta previa a la devolución.

Esta guía explica por qué disputas de los titulares de tarjetas. También aborda las diferencias entre las normas de las distintas redes de tarjetas y cuáles son los plazos de resolución. Aprenderás a interpretar un código de motivo en cuanto lo recibas, para que dediques menos tiempo a lidiar con disputas evitables de los titulares de tarjetas.

Comprender disputas de los titulares de tarjetas

El término «reclamación del titular de la tarjeta» tiene tres significados diferentes según quién lo utilice. Para un cliente, una reclamación del titular de la tarjeta es el momento en el que detecta un cargo que le parece erróneo y llama a su banco. Esa es la interpretación más restrictiva de la expresión.

Pero para los comerciantes, las entidades de procesamiento e incluso los bancos, «reclamación del titular de la tarjeta» y «contracargo» son dos caras de la misma moneda. Se suelen tratar como términos intercambiables. Chase le dice abiertamente a sus comerciantes que una reclamación «también se conoce como contracargo». Bank of America lo plantea siguiendo el mismo principio: cuando un titular de tarjeta reclama una transacción, se inicia el proceso de contracargo.

Así que, si has visto que el término «reclamación del titular de la tarjeta» se utiliza de forma tan amplia, no se trata de un uso incorrecto. Es simplemente la forma abreviada más habitual de referirse a Contracargos en los contenidos sobre pagos comerciales.

Luego está el tercer sentido, el más restringido y técnico: la propia documentación de Mastercard.

disputas del titular de la tarjeta disputas código de motivo 4853) constituyen la categoría más amplia de la taxonomía de códigos de motivo de Mastercard. Abarca desde la no recepción de productos hasta una suscripción cancelada que sigue apareciendo en el extracto. En este caso, la «reclamación del titular de la tarjeta» no es el fenómeno en su totalidad, sino una de las varias categorías de devoluciones. Se sitúa junto al fraude, los errores de autorización y los errores de procesamiento.

¿Por qué es importante esto? Pues porque la mayoría Contracargos con una disputa, pero no todas las disputas se convierten en una devolución. Estos dos términos se utilizan como sinónimos con tanta frecuencia que esta diferencia desaparece en la mayoría de los contenidos dirigidos a los comerciantes. Pero es precisamente esa diferencia la que determina a qué te enfrentas en cada momento.

Un breve repaso al proceso de reclamación del titular de la tarjeta

Como ya hemos explicado en una guía anterior, el derecho del titular de una tarjeta a impugnar un cargo está recogido en la legislación federal. No se trata de una decisión arbitraria de la red, sino de una protección federal.

Una disputa comienza cuando el titular de una tarjeta se pone en contacto con su banco emisor para impugnar una transacción. Si el banco está de acuerdo en que podría haber un problema, abre un expediente formal y, a menudo, el titular recibe un abono provisional mientras la transacción permanece en disputa. Esta fase se desarrolla íntegramente por parte del banco, antes de que se te notifique nada. Para cuando te llega la notificación de la devolución, el banco suele haber decidido ya que merece la pena tramitar la reclamación, por lo que puede parecer que ha surgido de la nada, aunque ya se haya llevado a cabo una revisión exhaustiva en una fase anterior.

Por lo tanto, al responder no estás apelando a la buena voluntad de una empresa. Estás respondiendo a un procedimiento de reclamación protegido por la legislación federal, que cuenta con sus propios criterios probatorios. El resto de esta guía explica detalladamente cuáles son los requisitos de dicho procedimiento.

Motivos habituales de disputas de los titulares de tarjetas

disputas de los titulares de tarjetas no disputas todas el mismo origen. Por eso, agruparlas todas es precisamente la razón por la que los consejos genéricos no funcionan.

Algunas disputas culpa de los titulares de las tarjetas, ya sea de forma deliberada o no. Otras las provocan los propios comerciantes. Pero en la mayoría de los casos, ambas partes tienen parte de culpa. Saber a qué tipo de situación te enfrentas determina cómo debes actuar al respecto.

El fraude propiamente dicho se sitúa en un extremo de la balanza. Entre los casos de disputas de pago motivadas exclusivamente por el fraude disputas los siguientes:

- Los datos del titular de una tarjeta se utilizan sin su permiso,

- Un error de autorización puede deberse a un fallo técnico, a un error humano o a una actividad fraudulenta.

Estas son las disputas no disputas prevención un mejor servicio de atención al cliente. Para ello, es necesario contar con sistemas de detección de fraudes y datos de autorización fiables.

disputas provocadas por los comerciantes disputas en el extremo opuesto. Tal y como ha señalado Mastercard, el principal problema es la descripción del cargo. disputas por una descripción irreconocible pueden evitarse por completo por parte del minorista, y optimizar la reconocibilidad de las descripciones es una forma probada de reducir drásticamente el volumen de disputas. Muchos comerciantes subestiman el problema: la mitad de los clientes llaman a su banco cuando no reconocen un cargo. A menudo, una línea confusa en el extracto es lo que desencadena toda la disputa.

Luego está la zona gris que hay entre ambas, denominada «fraude amistoso». Es entonces cuando la intención se vuelve confusa y el volumen sigue aumentando.

Las suscripciones son el ejemplo más claro de esto en la actualidad, y las cifras que hemos compartido en nuestra introducción sobre Contracargos de transacciones recurrentes apuntan directamente a la razón. Cuando un consumidor tiene que elegir entre discutir con una empresa para cancelar una suscripción o simplemente impugnar el cargo ante su banco, la impugnación sale ganando siempre. En palabras de Scott Adams, director ejecutivo de Fraud Deflect, los consumidores no quieren ese tipo de complicaciones.

Cada uno de estos casos acaba archivándose con un código de motivo específico que utiliza tu procesador para clasificar la reclamación, y ese código es el punto de partida de tu estrategia de respuesta. Lee nuestra guía sobre los códigos de motivo de las devoluciones para obtener más información al respecto.

Normas de la red de tarjetas para disputas de los titulares de tarjetas

Las cuatro principales redes no siguen un único conjunto de normas. Para empezar, tienen normas distintas en cuanto a quién controla activamente el proceso de resolución de reclamaciones. Visa y Mastercard operan a través de bancos emisores independientes. American Express y Discover emiten las tarjetas y gestionan la red por sí mismas.

Muchos han argumentado que, dado que todo el sistema de resolución de disputas de los titulares de tarjetas se diseñó para proteger al cliente, la fusión de las funciones de red y de emisor —como hacen tanto Amex como Discover— no hace más que reforzar ese objetivo. Las garantías de exención de responsabilidad por fraude, que favorecen de manera abrumadora a los titulares de tarjetas, se encuentran entre las principales razones por las que está aumentando el fraude por devoluciones. Cuando la empresa que emite la tarjeta es también la que gestiona la red, tiene todos los incentivos para ponerse del lado de su propio cliente en lugar del tuyo en caso de disputa.

Los códigos de motivo también varían. Mastercard utiliza códigos numéricos agrupados en cuatro categorías, siendo la clasificación más amplia la de disputas del titular de la tarjeta». Amex utiliza 34 códigos alfanuméricos. Discover utiliza 26, en su mayoría abreviaturas de dos letras. El concepto es el mismo, pero los formatos difieren según la red.

Los plazos de escalado son aún más importantes, ya que marcan el tiempo contra el que realmente estás luchando. Mastercard te da 45 días para presentar pruebas convincentes, el emisor dispone de 45 días para presentar un caso previo al arbitraje y tú tienes 30 días para responder a ello. El proceso de Discover puede durar entre 60 y 90 días de principio a fin, con un laudo arbitral definitivo en un plazo de 15 días y una tasa de 475 dólares si pierdes. Merece la pena analizar con más detalle los procedimientos completos de Visa y Amex más allá de la respuesta inicial en un artículo específico. Y eso es precisamente lo que hemos hecho con nuestra guía práctica sobre devoluciones de Visa y nuestra guía sobre devoluciones de Amex.

Los umbrales de devolución de cargos se corresponden, en su mayoría, con la línea roja discontinua. Visa señala a los comerciantes que superan un índice de disputas del 1,5 % para que sean objeto de un escrutinio por parte del adquirente, independientemente de cómo se resuelvan los casos individuales. El umbral de «comerciante con devoluciones excesivas» de Mastercard sigue el mismo índice del 1,5 %. A esto se le suma un mínimo de 100 Contracargos un mes natural, lo que eleva la tasa al 3,00 % y Contracargos 300 Contracargos nivel más grave, el de «comerciantes con un número excesivamente alto de contracargos». Amex activa sus programas de contracargos inmediatos y parciales inmediatos cuando se mantiene una tasa del 1 % durante tres meses consecutivos.

Hay que tener en cuenta que el límite interno de tu entidad adquirente suele situarse muy por debajo de los umbrales de la red. La imagen siguiente muestra un resumen de los umbrales de la red de tarjetas (los límites de tiempo se destacan en una sección posterior):

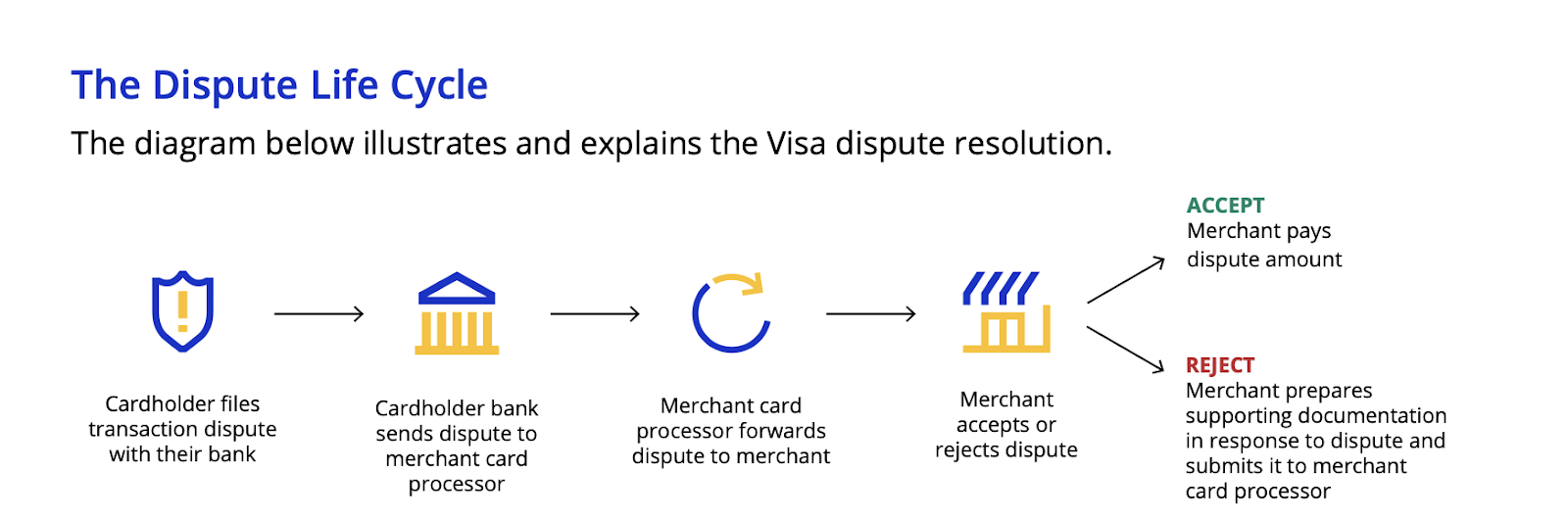

Proceso de resolución de reclamaciones de los titulares de tarjetas

Una disputa de pago se resuelve de una de estas tres formas: se revoca la devolución y se recupera el abono provisional del titular de la tarjeta, lo que significa que los fondos te son devueltos; se mantiene la devolución y los fondos se pierden definitivamente, y el abono provisional se convierte en uno permanente para el titular de la tarjeta; o bien, el titular de la tarjeta retira la disputa antes de que se alcance una decisión formal, sobre todo cuando el comerciante emite un reembolso al principio del plazo de investigación.

La tercera opción se utiliza poco. No todas las reclamaciones merecen una nueva tramitación. Algunas merecen un reembolso en la fase de investigación y nada más.

Actuar antes de que se produzca la devolución

Antes de que se presente formalmente una devolución, algunas redes te conceden un plazo para presentar alegaciones. Esa fase, cuando se produce, es tu mejor oportunidad para cerrar el caso antes de que siga adelante. Una respuesta contundente en la fase de alegaciones lo consigue: cierra el caso.

Amex utiliza esta fase de forma más explícita que las demás redes. Pero el principio se aplica a las cuatro redes. La cuestión no es si se emite formalmente una consulta. La cuestión es si se dispone de un proceso lo suficientemente rápido como para intervenir antes de que una disputa se convierta en una devolución. Las alertas de devolución existen precisamente para este margen de tiempo. Notifican a los comerciantes en el momento en que se inicia una disputa, con un plazo de entre 24 y 72 horas para realizar el reembolso y cerrarla por completo. La mayoría de los comerciantes se saltan esta fase, no porque no sepan que existe, sino porque sus procesos internos no están diseñados para actuar con tanta rapidez.

La notificación de devolución es el momento en que comienza a correr el plazo oficial

Cuando la fase de investigación no resuelve la disputa, o cuando la red se salta esta fase por completo, recibes una notificación formal de devolución. La entidad emisora abona provisionalmente el importe al cliente e inicia una reclamación formal a través de Visa Resolve Online, Mastercard Claims Manager o sistemas equivalentes para Amex y Discover. Este es el momento en el que la mayoría de los comerciantes consideran la reclamación como un gasto. Pero no lo es. Si sabes cómo adaptar tus pruebas al código de motivo, puedes revocar la reclamación.

¿Qué es lo que realmente marca la diferencia a la hora de responder a una reclamación sobre un pago?

Adaptar tus pruebas convincentes al código de motivo específico que figura en la notificación es la forma más segura de revocar la devolución. Tus pruebas convincentes constituyen una respuesta directa a la alegación concreta que plantea el código de motivo. Cuando una notificación de reclamación llega a tu bandeja de entrada, ya te encuentras en medio del proceso. Tu tarea a partir de ese momento es revocarla, no responder a una consulta pendiente.

Un código de motivo correspondiente a la no recepción de la mercancía requiere una prueba de entrega en la dirección del titular de la tarjeta, no una prueba de que el artículo se haya enviado. Un código de motivo correspondiente a la cancelación de una transacción periódica requiere una prueba de que el titular de la tarjeta aceptó las condiciones de facturación y de que no se solicitó la cancelación, no una copia de la página de condiciones del servicio. La prueba debe coincidir con el código.

Por qué la automatización de las devoluciones se ha vuelto cada vez más popular

Las pruebas incoherentes son la razón más habitual por la que los comerciantes pierden disputas deberían ganar. La mayoría de los bancos utilizan ahora sistemas automatizados para analizar las pruebas presentadas en respuesta a las disputas. Estos sistemas comprueban si tus pruebas contradicen directamente el código de motivo. Si no es así, la devolución se mantiene independientemente del resto de la documentación que hayas presentado.

Por eso, la gestión automatizada de las devoluciones se ha popularizado entre los comerciantes. Tal y como señalan Mastercard y Datos Insights en su informe global sobre devoluciones de 2025, las entidades emisoras y los comerciantes que revisen su enfoque, implanten tecnologías avanzadas de automatización y den prioridad a la experiencia del cliente obtendrán los beneficios de reducir Contracargos mejoran la satisfacción y la fidelidad de los clientes.

Comprender el funcionamiento de las fases previas al arbitraje y del arbitraje

Si el emisor impugna tus posiciones iniciales, el caso pasa a la fase de devolución previa al arbitraje. En esta fase, ya no se trata solo de recuperar los fondos, sino que también hay que gestionar el riesgo de que el caso llegue al arbitraje de devolución, lo que conlleva unos costes que, en muchos casos, superan con creces el importe original objeto de la disputa.

Amex queda fuera de este marco. A diferencia de Visa y Mastercard, que ofrecen vías de recurso más formalizadas, el proceso de devolución de cargos de Amex deja a los comerciantes con pocas opciones para solicitar una revisión adicional una vez que se ha emitido y confirmado una devolución de cargo. No existe ninguna vía de arbitraje a la que recurrir. La decisión es, en la práctica, definitiva, razón por la cual la fase de investigación reviste una importancia desproporcionada en el caso concreto de Amex.

¿Cuánto tiempo tiene el titular de una tarjeta para impugnar una transacción?

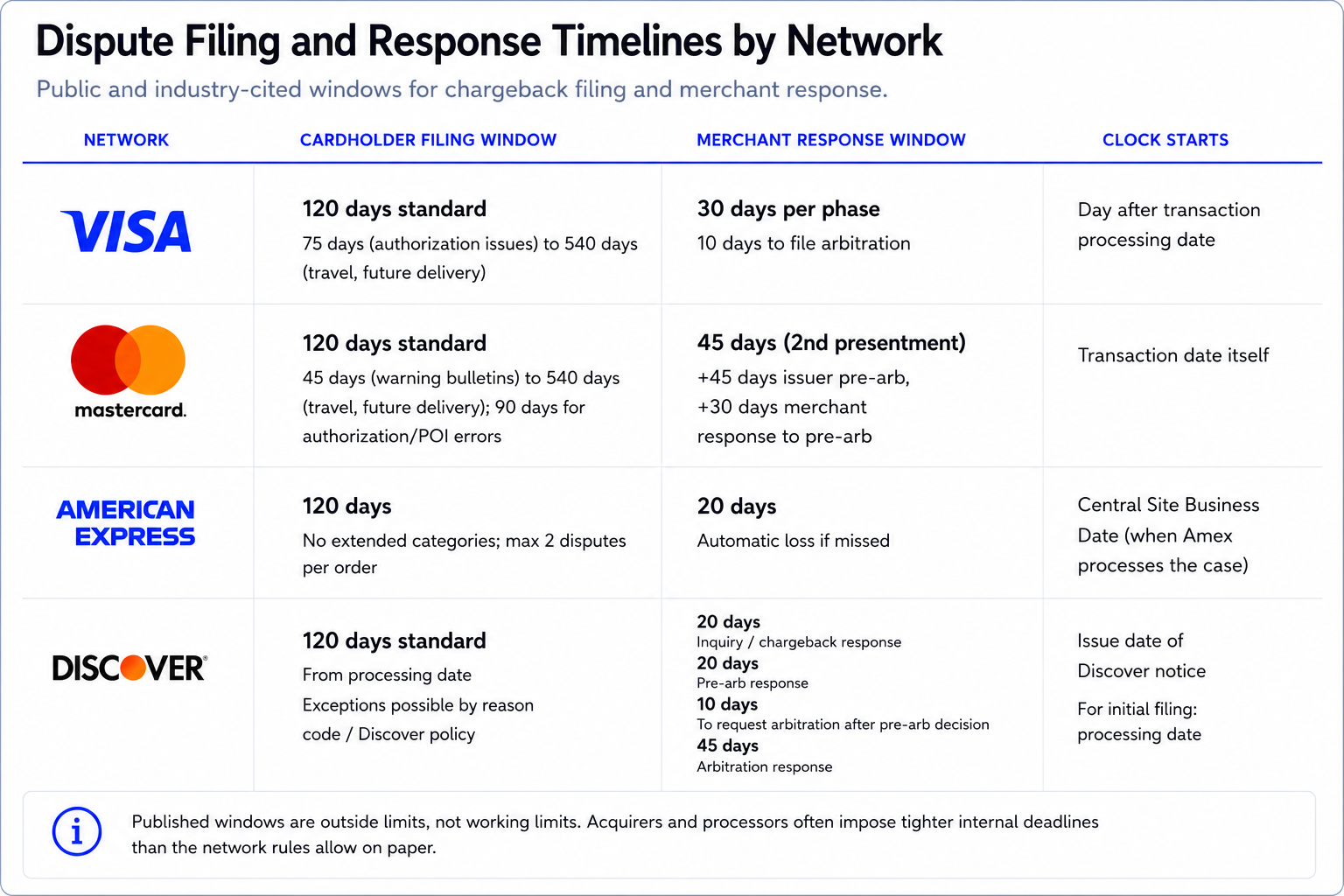

En las cuatro principales redes, el plazo estándar para que el titular de la tarjeta presente una reclamación es de 120 días a partir de la fecha de la transacción o de la fecha de entrega prevista. Sin embargo, el término «estándar» tiene un gran peso en esa frase. Cada red cuenta con categorías en las que el plazo comienza más tarde, es más corto o se prolonga mucho más allá de los 120 días, dependiendo del motivo de la reclamación. Analicemos con detenimiento los plazos de cada red:

Umbral para la presentación de reclamaciones y la respuesta de los titulares de tarjetas Visa

Los titulares de tarjetas Visa suelen disponer de 120 días a partir de la fecha de la transacción para presentar una reclamación, aunque el plazo puede reducirse a tan solo 75 días, dependiendo de la situación y del código de motivo. El plazo de 75 días se aplica específicamente a los boletines de recuperación de tarjetas y a los problemas relacionados con las autorizaciones. Por otro lado, determinados códigos de motivo de reclamación de Visa permiten un plazo de hasta 540 días naturales a partir de la fecha de procesamiento de la transacción, concretamente para transacciones con entrega futura y servicios de viaje.

En este contexto, un cliente que reserva un vuelo en enero y disputas en octubre está actuando conforme a las normas de Visa. Visa cuenta el plazo a partir del día siguiente a la fecha de tramitación de la transacción, no a partir de ese mismo día.

Los comerciantes disponen de un plazo considerablemente más corto. Visa concede a los comerciantes 30 días a partir del «día uno» de cada fase. Definen el «día uno» como el día siguiente al inicio de cada fase. Si desean recurrir al arbitraje, disponen de 10 días. El plazo publicado de 30 días es el límite máximo, no el plazo efectivo. Los procesadores como Adyen los plazos de respuesta de los comerciantes a 9 días para EE. UU. y Canadá, y a 18 días para otras regiones, con efecto a partir de julio de 2025. El plazo interno de tu adquirente es el que rige tu respuesta, y es casi seguro que sea más ajustado que lo que permiten las normas de Visa sobre el papel.

Umbral para la presentación y respuesta a reclamaciones de los titulares de tarjetas Mastercard

Al igual que los clientes de Visa, los titulares de tarjetas Mastercard suelen disponer de 120 días a partir de la fecha de la transacción o de la fecha de entrega prevista para presentar una reclamación. Este plazo se amplía a 540 días en el caso de los servicios de viaje y los artículos de entrega futura. Las categorías relacionadas con la autorización y los errores en el punto de interacción tienen un plazo más corto, de 90 días, mientras que disputas números de cuenta no registrados y los boletines de advertencia disputas aún más, a 45 días. Mastercard cuenta el plazo a partir de la propia fecha de la transacción, a diferencia de Visa, que lo hace a partir del día siguiente.

Los comerciantes disponen de 45 días a partir de la notificación de la devolución para presentar una segunda presentación. El emisor dispone de 45 días para presentar una solicitud de prearbitraje si rechaza el resultado. Y el comerciante tiene 30 días para responder a dicha solicitud de prearbitraje. El plazo de 45 días para el comerciante es el más generoso de las cuatro redes. Pero se aplica la misma salvedad interna de los adquirentes: los adquirentes y los procesadores también necesitan tiempo para tramitar las solicitudes, por lo que conviene prever al menos una semana antes de la fecha límite real de Mastercard.

Umbral para la presentación de reclamaciones por parte de los titulares de tarjetas American Express

Los titulares de tarjetas Amex también disponen de 120 días a partir de la fecha original de la transacción para impugnar un cargo, y no pueden presentar más de dos disputas un mismo pedido. En el caso de los productos defectuosos, el plazo comienza a contar a partir de la fecha de entrega, y no de la fecha de compra. No existen categorías con plazos ampliados de 540 días equivalentes a las disposiciones de Visa y Mastercard relativas a viajes y entregas futuras.

Los comerciantes disponen de 20 días para responder, ya sea aceptando la reclamación o demostrando que la devolución no tiene fundamento. Si no se respeta ese plazo, se produce una pérdida automática, independientemente del fondo del asunto. Veinte días es el plazo de respuesta más corto para los comerciantes de todas las principales redes. El plazo comienza a contar a partir de la «fecha comercial de la sede central de Amex», que se fija en el momento en que Amex tramita el caso, no cuando el comerciante lee la notificación.

Umbral para la presentación de reclamaciones por parte de los titulares de la tarjeta Discover

Los titulares de tarjetas Discover disponen igualmente de 120 días a partir de la fecha original de la transacción para presentar una reclamación, aunque pueden darse excepciones en función de circunstancias específicas y de las políticas de Discover. Los comerciantes tienen 20 días para responder a una consulta inicial y otros 20 días para responder una vez que se haya presentado una devolución formal, con un plazo de 10 días si alguna de las partes desea recurrir al arbitraje. La imagen siguiente muestra los plazos para la presentación de reclamaciones y las respuestas según la red:

Qué significa la asimetría

El patrón en las cuatro redes es idéntico en cuanto a su estructura, aunque las cifras difieran:

- Los titulares de las tarjetas tienen meses, los comerciantes tienen semanas y las entidades procesadoras se quedan discretamente con una parte de esas semanas antes de que el archivo te llegue a ti.

- Los plazos de reclamación de los comerciantes son, en teoría, de entre 20 y 45 días, pero el tiempo efectivo suele ser menor debido a los retrasos en la tramitación interna.

La implicación operativa no se limita a «responder más rápido». Se trata de que tu flujo de trabajo interno para la gestión de reclamaciones debe diseñarse en función del plazo más ajustado posible, no del máximo publicado. Si envías las notificaciones de reclamaciones por correo electrónico, esperas una aprobación manual o tratas cada caso como un problema de clasificación nuevo en lugar de como un proceso de respuesta automatizado y preconfigurado, el tiempo se te acabará antes incluso de haber empezado. Una transacción realizada hace catorce meses puede dar lugar hoy a una reclamación legítima de Visa o Mastercard. Tus registros deben estar disponibles cuando eso ocurra.

Prevención y evitación de disputas de los titulares de tarjetas

Los consejos para prevenir disputas —como fijar el descriptor, simplificar el proceso de cancelación y enviar una notificación previa a la facturación— no son incorrectos. Además, ya se han tratado anteriormente en esta guía. Sin embargo, no son necesariamente la estrategia de prevención definitiva. La estrategia de prevención comienza donde termina el análisis de las causas:

Gestiona los ratios, no solo disputas

Ganar disputas protege tu índice de devoluciones. Un comerciante con una alta tasa de éxito en las reclamaciones y un índice de disputas al alza sigue abocado a un programa de seguimiento que le priva de su derecho a responder y desencadena una intervención del adquirente que resulta difícil de revertir.

El volumen de reclamaciones y los resultados de las mismas son dos indicadores distintos que requieren dos enfoques de gestión diferenciados. La mayoría de los comerciantes realizan un seguimiento de los resultados. Es necesario realizar un seguimiento de ambos, y deben considerar la variación de la ratio como un problema empresarial que debe escalarse antes de que supere un umbral determinado.

Invierte en inteligencia de identidad IA

La mayoría de las herramientas de prevención del fraude se basan en una pregunta: «¿Es esta tarjeta robada?». Esa es la pregunta adecuada para el fraude propiamente dicho, pero no lo es para el fraude por devolución de cargo, la categoría de disputas que crece más rápidamente.

No se trata de casos de tarjetas robadas. Son compradores reales que han decidido que presentar una reclamación es más fácil que resolver el problema, y los sistemas tradicionales de detección de fraudes no los detectan porque utilizan sus propias credenciales. Las lagunas en la política de devoluciones, los procesos de cancelación y las descripciones de los cargos son aspectos básicos. La única laguna que queda es la detección: identificar a los clientes que ya han demostrado un comportamiento abusivo antes de tramitar su próximo pedido y tener que hacer frente a otra reclamación.

Esto es lo que el sector denomina ahora «hurto digital»: clientes que se aprovechan de las políticas Contracargos, devoluciones y reembolsos para quedarse con los productos sin pagar. Es el mecanismo que subyace a una parte significativa del volumen de reclamaciones que hemos descrito a lo largo de esta guía.

Chargeflow prevención se ha diseñado precisamente para esto. Analiza las señales posteriores a la compra comparándolas con una red global de comerciantes para señalar las transacciones que podrían dar lugar a disputas se produzcan. Identifica a los ladrones digitales conocidos en cuanto aparecen, bloqueando el fraude con tarjetas robadas y detectando en tiempo real a quienes realizan devoluciones repetidas y a quienes abusan de los reembolsos.

La prevención de devoluciones a este nivel no consiste en ser más precavido al finalizar la compra, sino en saber qué clientes ya han supuesto un gasto para otros comerciantes y actuar en función de esa información antes de que te supongan un gasto a ti.

Hay que tener en cuenta que la prevención tiene un límite

Incluso una empresa bien gestionada se enfrentará a Contracargos. Eso es un hecho. La prevención reduce el volumen, pero no elimina la exposición. Un estudio realizado por la propia Mastercard reveló que una cuarta parte de los comerciantes de distintos países registran un volumen anual de devoluciones superior a un millón de transacciones, y que, para el 13 % de los comerciantes, ese volumen representa el 2 % o más del total de transacciones. A esa escala, la prevención no es una infraestructura opcional. Es la diferencia entre un coste de negocio asumible y una ratio que te pone en el punto de mira de un adquirente.

Por eso los dos sistemas son más importantes que cualquiera de ellos por separado. Un marco de intervención previa a la tramitación bancaria —del tipo que detecta a un ladrón digital antes de que se procese su pedido o que identifica un patrón de fraude «amigable» antes de que llegue al emisor— es lo que evita, en primer lugar, que ese volumen aumente. Y un proceso de respuesta preciso permite resolver las disputas , a pesar de todo, llegan a producirse. Se trata de sistemas independientes, y se necesitan ambos.

¿Necesitas ayuda para desarrollar ambos sistemas? Habla hoy mismo con nuestros expertos.

¿Qué significa impugnar una transacción?

Impugnar una transacción significa que el titular de la tarjeta solicita formalmente a su banco que investigue y, en su caso, anule un cargo, alegando normalmente fraude, falta de entrega o un problema con el servicio.

¿Qué le ocurre al comerciante cuando se impugna un cargo?

Se notifica al comerciante la reclamación y el código de motivo correspondiente, y se le concede un plazo determinado (que suele oscilar entre 20 y 45 días, dependiendo de la red) para presentar pruebas que refuten la reclamación.

¿Qué es una reclamación comercial?

Una disputa comercial es el mismo proceso visto desde el punto de vista del vendedor: se trata de la devolución de cargo o consulta a la que una empresa debe responder después de que el titular de una tarjeta disputas de sus cargos.

¿Qué ocurre cuando se presenta una reclamación sobre una tarjeta?

La impugnación de un cargo en una tarjeta da lugar a una revisión formal por parte de la red de la tarjeta; a menudo, los fondos se revierten de forma provisional mientras el comerciante y la entidad emisora intercambian pruebas para determinar el resultado definitivo.

Gestionar automáticamente todas las reclamaciones de los titulares de tarjetas

Ya no tendrás que estar buscando manualmente los códigos de motivo y los plazos. Chargeflow la recopilación de pruebas y la presentación de reclamaciones para todo tipo de disputas, con la garantía de un retorno de la inversión cuatro veces mayor.

Empieza gratisContracargos?

Ya no es problema tuyo.

Recupera cuatro veces más Contracargos y prevención , hasta un 90 % de las entradas, gracias a IA y a una red global de 20 000 comerciantes.

.png)

.avif)