%201.svg)

Discover Chargeback Guide: Rules, Process, and Tips for Merchants in 2026

¿Devoluciones?

Ya no es un problema para ti.

Recupera cuatro veces más devoluciones y evita hasta el 90 % de las que se producen, gracias a la inteligencia artificial y a una red global de 20 000 comerciantes.

Discover gives you one shot to make your case, no second stages, no recovery windows. Authorization doesn't protect you on card-not-present transactions. Digital goods get minimal structural coverage. Your rebuttal needs to anticipate objections Discover hasn't raised yet, not just respond to the ones the cardholder did. The merchants who stay ahead of this don't manage chargebacks better. They've built operations where fewer chargebacks make sense to file in the first place.

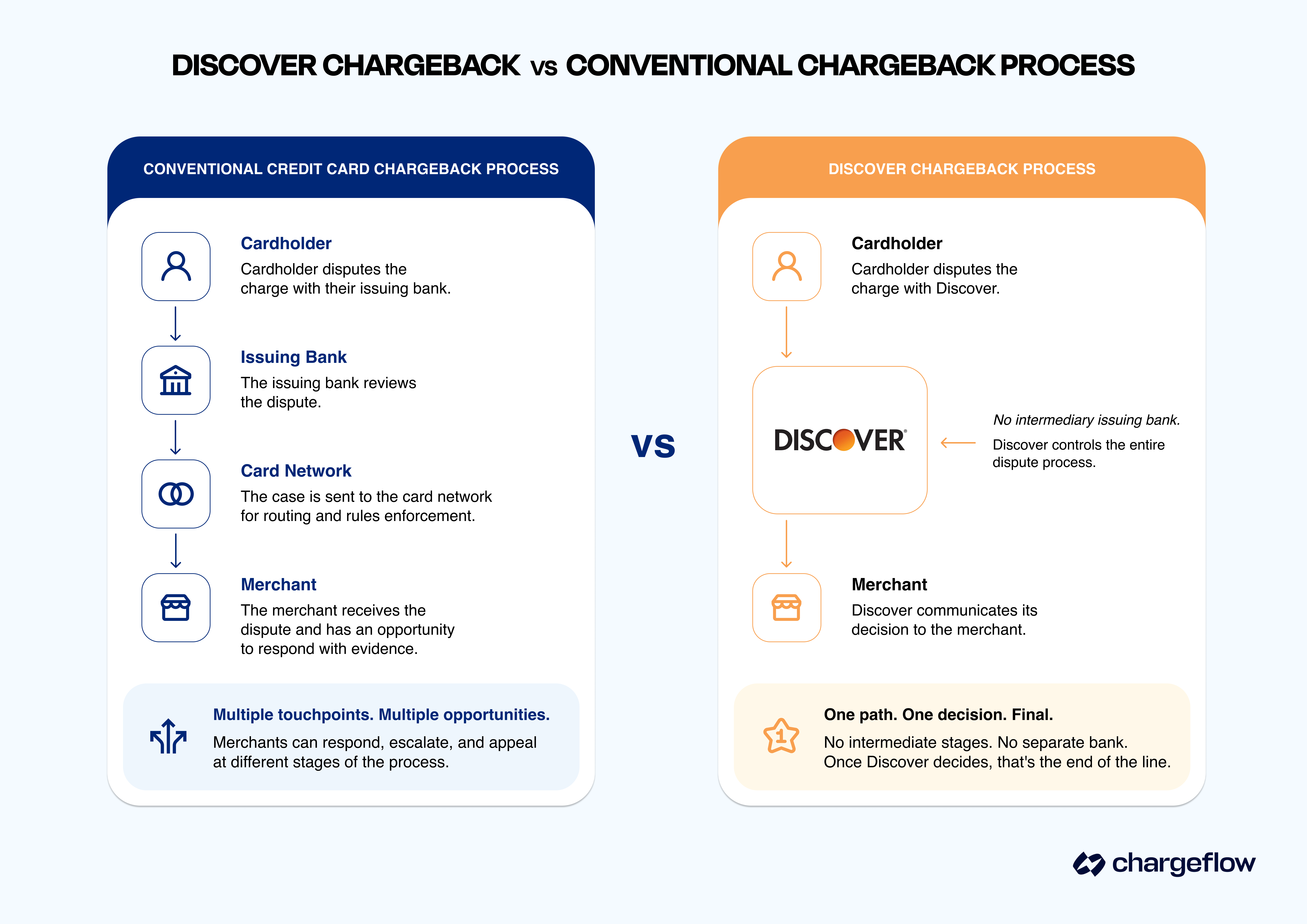

Discover chargebacks operate by a fundamentally different set of rules, and most merchants only find out the hard way. Unlike Visa and Mastercard, Discover issues its own cards, meaning it controls both the rules and the final verdict on every dispute. There’s no separate issuing bank to negotiate with. When Discover rules against your rebuttal, there’s no further stage to appeal; the only other option is arbitration.

Discover’s compressed process means there’s no opportunity to counter new information the cardholder introduces. Your rebuttal has to anticipate everything upfront.

What’s equally consequential is that valid authorization offers far less chargeback protection than merchants assume. For card-not-present (CNP) transactions, Discover believes that authorization only proves a card exists, but does not verify the cardholder’s identity. Digital-first businesses face an even steeper structural disadvantage. Discover’s framework heavily favors cardholders for intangible goods. And underneath all of it, Discover quietly tracks how well merchants build their cases over time, rewarding strong rebuttals and penalizing weak ones. Understanding these dynamics isn’t optional anymore.

What is a Discover Chargeback?

A Discover chargeback is a forced payment reversal initiated by a cardholder and adjudicated entirely by Discover itself. One cardinal distinction between Discover chargebacks and traditional credit card chargebacks is that there’s no intermediary issuing bank; the very entity that issued the card controls the entire dispute process and verdict.

The dispute process is streamlined. But that mostly works against merchants, not for them. There are no additional stages where you can course-correct, and no separate bank to appeal to. Once Discover renders its decision, that’s effectively the end of the line for that case.

Why does this matter, you ask? Discover holds roughly 5% of U.S. card transaction volume, a minority share that still translates into significant dispute exposure for high-volume or eCommerce merchants. Mistakes in timing, evidence packaging, or documentation strategy carry real financial and account-level consequences.

Common Discover Chargeback Reason Codes

Discover uses self-descriptive alphabetic abbreviations for its chargeback reason codes, unlike Visa and Mastercard, which use numerical systems. Discover specifies 26 reason codes across seven categories: Fraud, Not Classified, Authorization, Expired, Processing Errors, Services, and Dispute Compliance. Most codes are two-letter abbreviations of the dispute description.

The practical implication is that merchants who handle multiple networks can read Discover codes faster at intake. But that surface readability can also breed overconfidence. A code like AA or RG looks simple; the evidence requirements behind them are not.

Here’s what each category contains and what merchants need to know about each code:

Cardholder Disputes

AA -- Cardholder Does Not Recognize: The cardholder claims they don’t recognize the transaction on their statement. This commonly occurs when the buyer forgot about the purchase or didn’t recognize the billing descriptor.

AP -- Canceled Recurring Transaction: The cardholder claims they’re still being charged for a recurring transaction they previously canceled. This is frequently seen in subscription businesses.

AW -- Altered Amount: The transaction amount and authorization amount don’t match. This code also covers cash advance transactions.

CD -- Credit Posted as Card Sale: The card was debited instead of credited, which is typically a merchant error during a reversal where a refund becomes an additional charge.

DP -- Duplicate Processing: A single transaction was processed more than once, often from multiple batch submissions or POS system duplicates.

RG -- Non-Receipt of Goods or Services: The cardholder claims they didn’t receive what they paid for. Common with shipping delays.

RM -- Quality Discrepancy: The cardholder claims the goods or services were damaged, defective, or didn’t match the product description.

RN2 -- Credit Not Received: The customer returned merchandise or refused delivery, but the merchant didn’t process the credit.

Authorization Codes

AT -- Authorization Non-Compliance: The merchant processed a transaction without a positive authorization response, including processing without electronic authorization.

DA -- Declined Authorization: A declined transaction was sent for processing, anyway. This occurs when a merchant continues attempting a card that has already been declined.

EX -- Expired Card: The card had expired at the time of the transaction or expired before processing was completed.

NA -- No Authorization Request: A transaction was processed without ever requesting authorization from Discover.

Errores de procesamiento

IN -- Invalid Card Number: The card number doesn’t match a valid account. Causes range from a mistyped number to an expired card being reprocessed.

LP -- Late Presentment: The transaction wasn’t submitted within Discover’s required timeframe.

NC -- Not Classified: A catch-all for invalid transactions that don’t fall under any other Discover category.

Fraud Codes

UA01 -- Fraud/Card Present: A fraudulent transaction occurred using the physical card.

UA02 -- Fraud/Card-Not-Present: A fraudulent transaction occurred in a CNP environment. This is a very common fraud code for eCommerce merchants.

UA05 -- Fraud/Counterfeit Chip Transaction: The cardholder denies participating in a transaction processed at an EMV chip terminal.

UA06 -- Fraud/Chip-and-PIN Transaction: The cardholder denies a transaction at a chip terminal without a PIN pad.

UA10 -- Request Transaction Receipt (Swiped Card): The issuing bank requests transaction documentation because the cardholder claims fraud. This is a pre-chargeback retrieval step rather than a full chargeback code.

UA11 -- Cardholder Claims Fraud (Swiped, No Signature): The cardholder identifies a charge as fraudulent. This most often surfaces when they’re reviewing their statement.

Dispute Compliance

DC -- Dispute Compliance: Discover invokes this code when it determines the merchant failed to comply with its Operating Regulations. The most common trigger is failing to respond to a Retrieval Request. Unlike other codes, DC chargebacks are typically initiated by Discover itself, not the cardholder, and are typically difficult to fight. The burden rests entirely with the merchant to prove that they complied with Discover's Operating Regulations; Discover need not demonstrate that a violation occurred.

Discover Chargeback Codes Merchants Need to Watch Most

Not all codes carry equal risk. Three chargeback codes are most frequently abused for friendly fraud:

UA02 is the most common fraud code for eCommerce merchants. Because the burden of proof lies entirely with you in a card-not-present environment, digital shoplifters exploit this code the most.

AP is the dominant code for subscription businesses. Cardholders who forgot to cancel, find cancellation too difficult, or simply want out will frequently bypass you entirely and file directly with Discover. Without airtight cancellation records, you can hardly pre-empt this category of Discover chargebacks.

RG is similarly prone to abuse. In many cases, delivery occurred. The dispute hinges entirely on the strength of your delivery evidence, making documentation quality, not the facts of the transaction, the deciding factor.

These three Discover chargeback reason codes share a common trait. Disputes under the consumer and fraud categories are generally the most susceptible to chargeback fraud, precisely because it’s easy for the cardholder to claim a service wasn’t rendered, or a transaction was unauthorised. Merchants who fight these codes without understanding that dynamic will constantly under-prepare their rebuttals.

Understanding the Discover Chargeback Process

Understanding the Discover chargeback process as a sequence of steps is technically accurate. But it’s more useful to understand it as a power structure, one in which the timeline, the rules, and the final verdict are all governed by the same entity. That context changes how you engage with every stage.

1. The Pre-Dispute Inquiry

Before a formal chargeback is filed, Discover typically initiates a pre-dispute inquiry. This internal flag gives merchants a narrow window, usually 20 days, to resolve the issue directly. Resolving a dispute at this stage costs you nothing beyond the refund. Ignoring it may cost you more if you lose the chargeback that ensues.

The inquiry stage is where a significant portion of merchant losses happen. Not because of bad evidence, but due to inattention.

2. Representment

If the inquiry escalates, your rebuttal is called a chargeback representment, and it’s your one substantive opportunity to make your case. You’re not just responding to what the cardholder said. You’re anticipating what they might say next since there is no next stage where new information can be introduced. Whatever you don’t address stays unaddressed.

3. Arbitration

Assuming you win and the cardholder disputes the outcome, the case moves directly to arbitration. Losing arbitration cases carries a $475 fee in addition to the chargeback amount. If you’re an excessive chargeback merchant, you pay an extra fine of $25 per chargeback. That makes the decision to pursue arbitration as much financial as it is evidentiary.

What You Can Control

Within Discover’s compressed process, your agency remains in three places: how quickly you respond at each stage, how comprehensively you build your rebuttal the first time, and how well your documentation was constructed long before any dispute was filed. This is where automated chargeback management comes into play.

Important Note: Unlike other card networks that may encourage direct merchant-to-customer communication, Discover’s chargeback rules strictly prohibit merchants from contacting the cardholder directly once a dispute or chargeback is initiated. All communication and evidence submission must run through Discover's dispute process

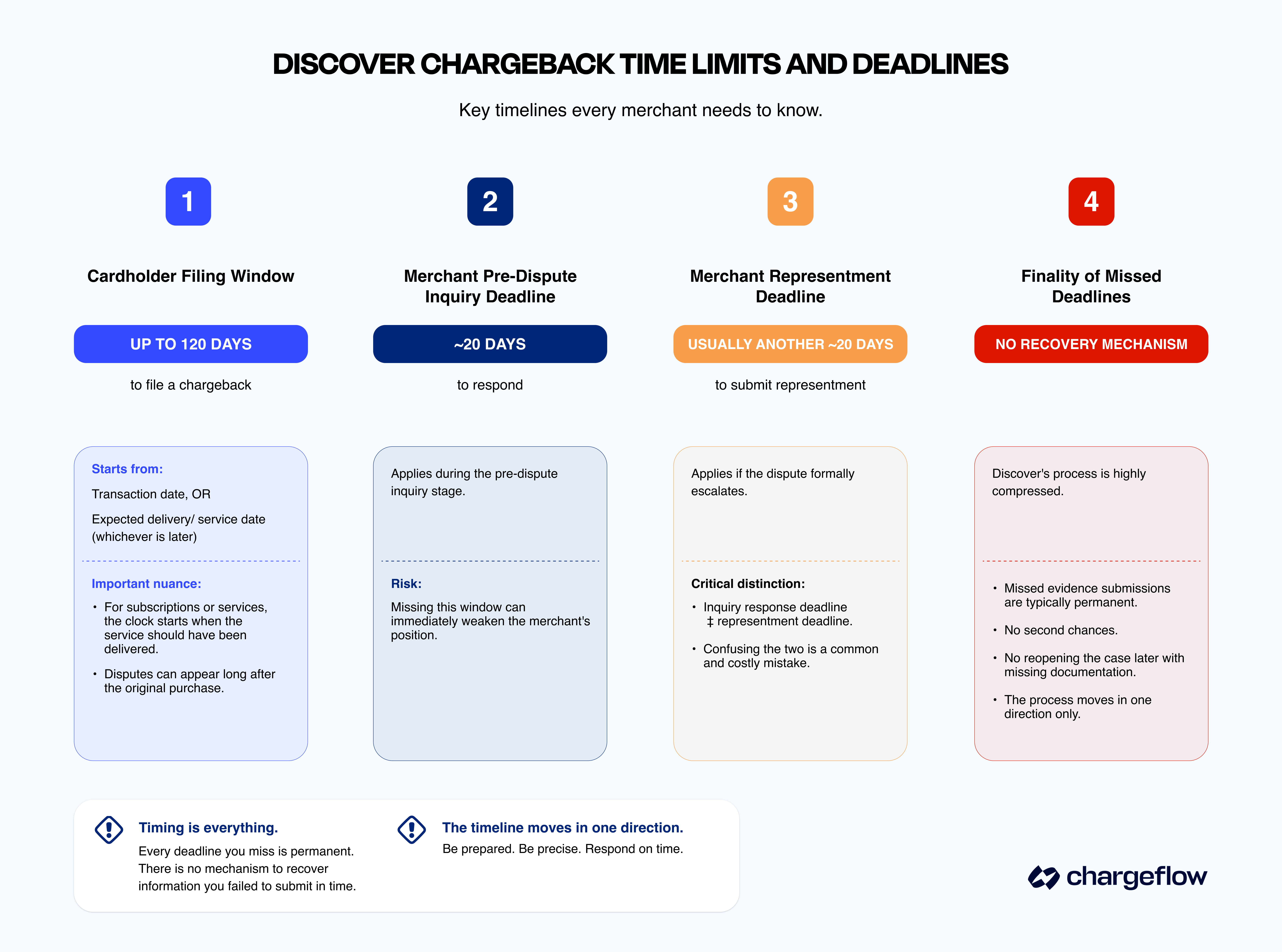

Discover Chargeback Time Limits and Deadlines

Discover gives cardholders up to 120 days to file a chargeback. The 120 days aren't measured from the statement date. Rather, it begins from the transaction date or the expected delivery date, whichever is later. For services or subscriptions, it starts from when the service should have been delivered. That distinction matters because a dispute can arrive well after a merchant assumes the window has closed.

On the merchant side of the aisle, once a chargeback is filed, you typically have 20 days to respond at the pre-dispute inquiry stage, and a separate window, usually 20 days, to submit a representment if the dispute formally escalates. These are not the same deadline, and conflating them is a common and costly mistake.

What makes Discover's merchant timeline uniquely punishing is the compression we've already established. Every deadline you miss is permanent. There is no mechanism to recover information you failed to submit in time. The timeline moves in one direction.

Merchant Guide to Handling Discover Chargebacks

Once a Discover chargeback lands in your queue, you’re operating inside a fixed structure. Your job is to apply a consistent playbook: decode, decide, assemble, and learn.

To do this well, you don’t rely on gut feeling. You run a decision system on every dispute, and then automate as much of it as possible.

Here’s a breakdown of the playbook:

Score Before You Respond

Not every dispute deserves the same energy. Evidence shows that some chargebacks originate from merchant mistakes. The moment a dispute arrives, score it on three dimensions: the amount at stake, the strength of evidence you actually have, and how clearly your policies support your position. A high-ticket order with delivery confirmation, device fingerprints, and a signed terms agreement is a different fight than a low-value dispute with no tracking and an ambiguous cancellation policy.

If the math doesn’t support fighting, absorbing the loss at inquiry might make sense.

Let the Reason Code Build Your Evidence Package

The reason code tells you what Discover is adjudicating, and therefore exactly what your rebuttal needs to dismantle. UA disputes require identity and behavioral evidence: AVS results, device data, IP history, and prior purchase patterns. Recurring billing disputes live or die on cancellation timestamps. Non-receipt disputes need the fulfillment chain, not just a tracking number.

Stop reinventing this for every dispute. Build code-specific evidence checklists once, map them to your systems, and treat each rebuttal as an execution of that checklist, not a fresh exercise in judgment under deadline pressure.

Write the Rebuttal for the Objection Discover Hasn’t Raised Yet

Most merchants respond to what the cardholder says. The ones who understand the psychology of chargebacks respond to what the cardholder might say next. Lead with your policy, attach code-matched evidence, then explicitly address the most likely counterargument; the one Discover might weigh if the cardholder pushes back. Whatever you leave unaddressed at representment stays unaddressed permanently.

Treat Every Loss as a System Input

A lost UA dispute with weak identity evidence is a signal to tighten your fraud controls. A lost recurring billing dispute is a signal to redesign your cancellation flow. A pattern of non-receipt disputes in a specific product line is a fulfillment problem, not a chargeback problem.

Merchants like Beard Club, who compound their win rate in a short period, aren’t necessarily better at responding to disputes. They use every dispute data point to make the next one less likely.

Doing all of these manually across dispute volume, multiple reason codes, and multiple networks is where the playbook breaks down for most businesses. That’s the gap Chargeflow was built for. Here's Beard Club in their own words:

Best Practices for Avoiding Discover Chargebacks

Discover dispute patterns seem to skew risk toward specific fault lines: card-not-present fraud, cancellation disputes on recurring billing, and non-receipt claims on digital goods. Here’s how to address those pressure points directly.

Build Against Discover’s Known Biases

For CNP transactions, authorization offers almost no protection when a cardholder later claims they never approved the charge. What does? Behavioral evidence collected at the point of sale (example: device fingerprints, IP addresses, 3DS data, and prior purchase patterns on the same account). Collected systematically, this makes unauthorized claims significantly harder to sustain.

For subscription businesses, the cancellation flow is your highest-risk touchpoint. Discover defaults to the cardholder’s story unless you can show a timestamped cancellation request in your own logs, not a confirmation email, but the request itself. Your cancellation UX should generate that record automatically, every time.

For digital goods, accept that Discover’s framework offers limited intrinsic protection and adjust accordingly. Apply tighter fraud controls, capped first-time order values, and flows that make legitimate customers feel heard before they reach for the dispute button.

Make Chargebacks Hard to File

The common thread among merchants with consistently low Discover chargeback rates is that they make customers feel a dispute is rarely their only option. That means billing descriptors that match what the customer remembers buying, proactive communication on delays before the customer notices them, and refund paths that are easier to find than a bank’s dispute form. The difference between folks who do this and those who don’t isn’t knowledge? It’s whether you treat it as operational infrastructure owned by product and ops, or as a customer service afterthought.

Stop Chargeback Fraud Before It Starts

Chargeback fraud is generally the leading cause of chargebacks. And disputes originating from intentional abuse of the system are hard to reverse once they’re in the pipeline. The better strategy is intercepting them before they count against your ratio.

Chargeback alerts notify you the moment cardholders initiate disputes, giving you a window to resolve them directly before formal chargebacks are created. That single intervention removes the case from your metrics entirely. Chargeflow’s Alerts system detects those early signals across Discover and other networks, triggering workflows before the dispute settles against you.

For repeat digital shoplifters, cardholders who habitually buy, consume, and dispute, Chargeflow Prevent flags or blocks high-risk cardholders before they complete checkout. The dispute that never gets filed never costs you anything.

Stay Below the Threshold

Discover’s monitoring program triggers at approximately 1% chargeback ratio and 100 chargebacks per month. Once flagged, remediation windows are short, and consequences escalate faster than on other networks.

At that point, dispute-by-dispute management isn’t enough. To stay comfortably below Discover’s thresholds, you must build operations where chargebacks are a byproduct of genuine edge cases, not the default outlet for customer confusion, friction, or opportunism.

Conclusión

Most merchants treat Discover chargebacks as an operational inconvenience, something to handle out of necessity when it happens. The ones who understand consumer psychology treat it as a system to understand and build against before anything ever goes wrong.

The difference between those two postures is what this guide has been about. Not only the rules, but the structural logic behind them. Not just what to do, but why it matters that you do it before the clock starts.

You can compound your chargeback outcomes without necessarily doing more. Doing the right things earlier, more consistently, and with better infrastructure trumps all smarts and hustle that leaves you where you started. That’s what Chargeflow makes possible at scale.

If you're ready to stop managing Discover chargebacks dispute by dispute, Chargeflow can show you what systematic looks like for your business. Schedule a demo to see the numbers yourself.

¿Devoluciones?

Ya no es un problema para ti.

Recupera cuatro veces más devoluciones y evita hasta el 90 % de las que se producen, gracias a la inteligencia artificial y a una red global de 20 000 comerciantes.

.png)