%201.svg)

Billing Disputes: What They Are and How to Resolve Them (Insider Secrets for Merchants)

Rétrofacturations ?

Ce n'est plus votre problème.

Récupérez 4 fois plus de rétrofacturations et prévenez jusqu’à 90 % de celles à venir, grâce à l’IA et à un réseau mondial de 20 000 commerçants.

A billing dispute is a broad term for all billing-related controversies between you and your customers. A chargeback is the specific, card-network mechanism this guide has focused on, because that’s where the cost is highest, the deadlines are tightest, and the most is at stake.Most disputes trace back to a handful of recurring causes: unauthorized charges, billing errors, product or service issues, and subscription problems. Which ones you see most often depends heavily on the sector. Subscription businesses lose the most ground in the free-trial conversion and the cancellation flow. Travel and hospitality carry the highest cost per case and the most complex evidence requirements. Digital goods face disputes with no shipping label to point to. Retail e-commerce splits its exposure between item-not-received and not-as-described claims, each requiring different proof.

A billing dispute isn't fraud. But you should treat it like it is anyway. Why? Because Visa estimates that as much as 75% of all chargebacks are baseless. And that share has been climbing for the better part of a decade.

You can't tell, from the first customer complaint, whether a billing dispute is a five-minute fix or the start of a real fight. Assume it's the second one. Then do your due diligence to understand the objective reality.

The logic is simple. Prepare for the dispute that turns into a real fight, and you've lost nothing on the ones that don't. Skip that preparation because a dispute seems routine, and you won’t know until it's too late.

This guide explains everything you need to know about billing disputes: what they are, why they happen, and the practical steps to resolve and prevent them.

What Are Billing Disputes and Why Do They Occur?

A billing dispute is the umbrella term for the various kinds of disagreements raised by a customer (cardholder, client, or account holder) over a charge they've been billed for. The customer is essentially saying, "I don't think I should have to pay this, or pay this amount." That disagreement can show up anywhere money changes hands on a recurring or invoiced basis. And how it gets resolved depends entirely on where it's raised and who's being asked to step in.

But for the purpose of this guide, we'll define a billing dispute as a cardholder-initiated dispute that proceeds through the card network's formal chargeback process. That means the customer has gone beyond contacting you, the merchant, and has asked their bank to reverse the transaction.

Again, card chargebacks are just one resolution path among several. We're focusing onn it because that’s where merchants face the highest cost, tightest deadlines, and the stakes are biggest.

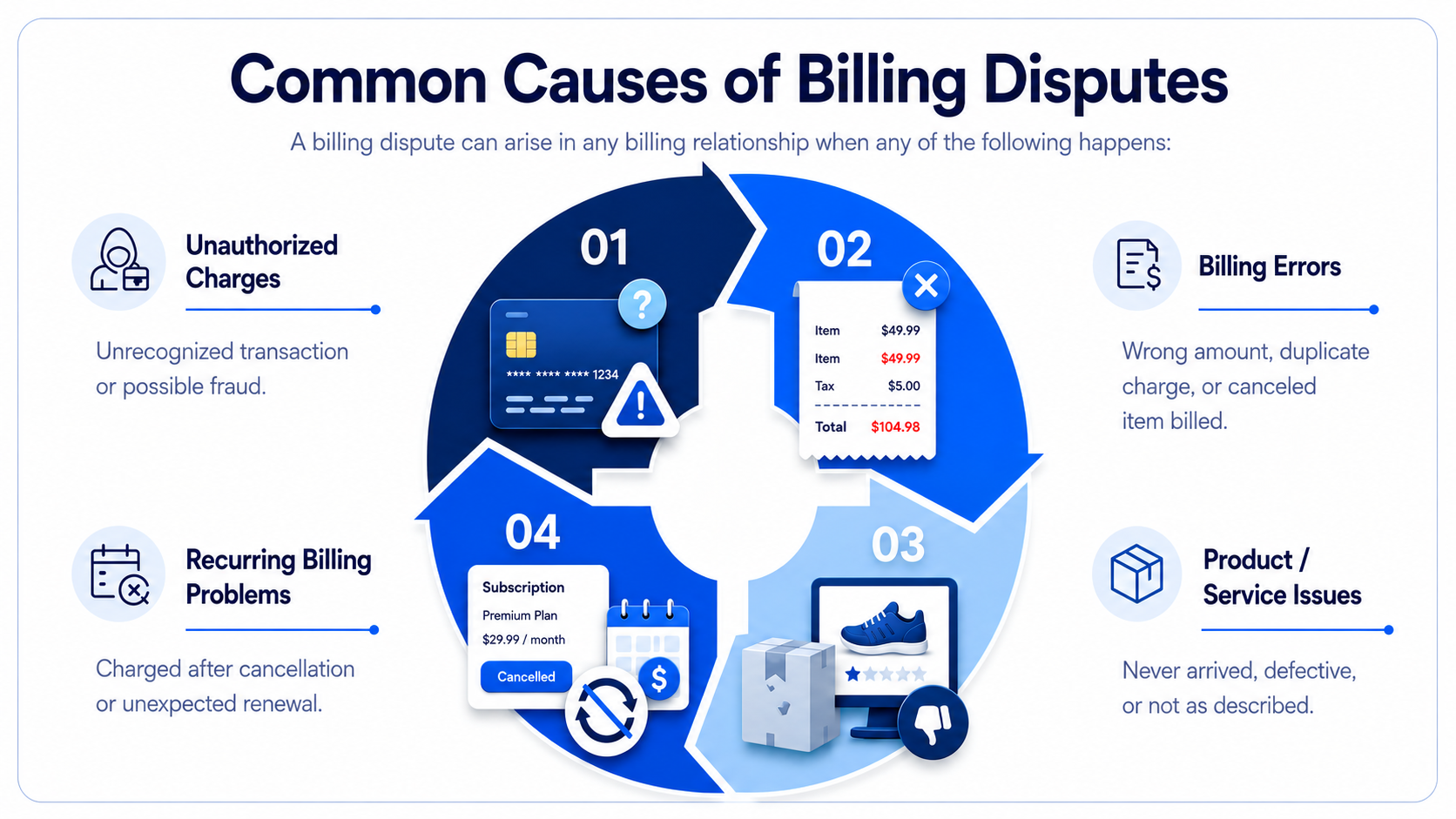

Common Causes of Billing Disputes

A billing dispute can arise in any billing relationship when any of the following happens:

- Unauthorized charges: The customer doesn't recognize the transaction at all. This can be a result of potential fraud or a family member/friend using a card without clear authorization.

- Billing errors: Wrong amount charged, duplicate charges, or being billed for something already cancelled.

- Product/service issues: Item never arrived, didn't match what you described, was defective, or the service wasn't delivered as promised.

- Subscription/recurring billing problems: You continue to charge after cancellation, or there’s a charge the customer didn't realize they'd signed up for.

This is not a comprehensive list of the causes of customer disputes, but these four are the categories you'll encounter most often.

How to Handle Billing Disputes Effectively

Most chargeback analysts treat every billing dispute as a foregone conclusion of revenue loss. That’s why the advice to “respond fast, gather evidence, submit a strong case” doesn’t cut it anymore.

The more prudent question is where in the lifecycle a dispute actually gets decided. Because by the time a formal chargeback lands in a merchant's queue, the cheapest opportunities to preempt it have usually already passed.

That said, here’s how to handle billing disputes without breaking a sweat:

Use The Networks’ Pre-chargeback Window

Every major network now offers some version of a pre-dispute or chargeback deflection program. And they’re worth naming individually because they don’t behave the same way:

Mastercard’s Ethoca Alerts notifies a merchant when an issuing bank receives a cardholder complaint, placing a short hold (usually about 24 hours) before the chargeback is filed. During this interval, a merchant enrolled in the program can refund and stop the billing dispute before it’s ever logged as a Mastercard chargeback.

Visa’s Order Insight and Rapid Dispute Resolution work earlier, still. Order Insight gives issuers detailed transaction information at the moment a cardholder inquires about a charge, often letting cardholders recognize a legitimate purchase before a dispute is even opened, while RDR automatically refunds eligible transactions based on predefined rules, removing them from the VAMP calculation entirely.

American Express’s Accelerated Dispute Resolution gives merchants up to eight calendar days to respond to a non-fraud dispute. During this window, liability for the disputed amount remains with Amex rather than you. There’s the option to refund the Amex chargeback, challenge the dispute with evidence, or settle directly with the card member.

Discover offers a dispute-resolution dashboard, the Discover Network Dispute System, typically used by processors on a merchant’s behalf. This allows authorized users to view your Discover chargeback documentation, upload evidence, and track the status of a claim.

Used well, these pre-chargeback alert tools genuinely limit billing disputes from becoming chargebacks at all, which is the cheapest possible outcome.

Where The Network Tools Stop, And Why That Gap Matters

The honest limitation is coverage and scope. Ethoca’s reach outside Mastercard is partial. It offers some coverage for Visa and limited coverage for American Express, Discover, and JCB (Discover’s long-standing partner).

And on those three networks, it applies to only a single chargeback reason code. That means a merchant who onboards all four major card types is, by design, working with four different tools, four different response windows, and four different rule sets just to cover the pre-dispute touchpoint alone.

And none of them follow a transaction through to representment if it does become a chargeback.

That's the gap most merchants are solving for today. Not four dashboards and four rule sets. It's one system that catches every alert, on every network, in time to act on it, and still builds a real evidence package for whatever slips through anyway.

Guess what? That's exactly what a cross-network automation chargeback platform does. It’s one inbox for every alert, one evidence process regardless of which card brand sent the dispute. And nothing depends on someone knowing the latest policy shift or checking the right dashboard before the window closes.

Sector-Specific Billing Dispute Prevention Best Practices

Some sectors are prone to billing disputes more than others. Below are actionable, sector-specific prevention strategies for billing disputes you can incorporate right away.

Tourisme et hôtellerie

According to Mastercard, merchants offering travel and hospitality services report the highest average chargeback value at $120. Travel and hospitality carry the highest per-dispute cost of any sector covered in this guide.

Where Travel and Hospitality Disputes Come From

- Bookings that are made weeks or months in advance. Cancellations, no-shows, pre-authorizations, incremental charges, and cross-border currency conversions all create legitimate confusion for cardholders by the time the stay or trip actually happens.

- Unclear cancellation policies. An estimated 30% of chargebacks in the travel industry trace back to unclear cancellation policies. A guest cancels late, doesn’t get the refund they expected, and disputes the charge rather than rereading the fine print they may never have seen clearly in the first place.

- Disputed service quality on something that can’t be returned. Guests dispute charges when a room isn’t clean, amenities don’t work, or the experience doesn’t match what was advertised. And unlike retail, a hotel can’t resolve this the way a retailer resolves a damaged-product complaint. The service itself can’t be returned.

- Third-party booking complexity. Many hotels don’t process payments directly. They run on a property management system or booking platform that handles the technical integration. When a chargeback arrives, the platform gets the notification. But the hotel carries the financial liability and has to track down its own evidence after the fact.

How to Reduce Travel and Hospitality Billing Disputes

- Proactive, well-timed guest communication. A guest who never receives a booking confirmation may worry the charge is fraudulent. And a traveler who forgets about a pre-authorized hold may dispute it weeks later. Automated messaging at key moments in the journey reduces that anxiety and gives guests a direct path to resolve concerns before they call their bank.

- Reason-code-specific evidence, not generic documentation. Sending the wrong evidence is the single most common reason hotels lose disputes they would otherwise have won. That’s why automated dispute management is gaining massive recognition across the industry today.

Subscription and Recurring Billing

Subscription businesses carried an average chargeback value of $69 in 2025, according to Mastercard. Subscription chargebacks occur at two predictable moments: the first charge after a free trial, and the point at which a customer tries to cancel.

Where Subscription and Recurring Billing Disputes Come From

- The free-trial-to-paid conversion. A customer enters a card for a "$0 trial," the trial ends, and the system charges them for the first full month. The customer sees what appears to be an unexpected charge and has two options: contact support or call the bank. Most choose the latter.

- Cancellation friction. When customers struggle to cancel easily due to hidden cancellation links, multi-step workflows, or a requirement to call support instead of clicking a button, a chargeback starts to feel justified. Several US states now legally require one-click cancellation if the signup happened online, and the card networks themselves push the same standard to keep dispute rates down.

- Forgotten renewals, especially annual ones. Because charges recur automatically, customers are more likely to forget they ever authorized the transaction or fail to recognize the merchant's name on their statement. Disputes can surface months after signup. This makes it harder for the merchant to produce evidence by the time it happens.

- Unclear billing descriptors. Many merchants bill under a legal entity name or payment-processor identifier that doesn't match the brand the customer actually recognizes. That mismatch alone generates a steady stream of disputes that wouldn't otherwise happen.

How to Reduce Subscription Billing Disputes

- Implement one-click cancellation, no detours. Cancellation friction correlates directly with dispute rates, so removing it is one of the highest-leverage fixes available.

- Send renewal reminders before the charge hits, not after. This is particularly essential for annual plans, where a year is long enough that most customers genuinely forget.

- A billing descriptor that matches the brand saves you money. Using the legal entity or a processor code might generate confusion.

- Prevent at-risk subscriptions with network data. The clearest illustration of why this matters is the math itself. At 5,000 subscribers and a 1% dispute rate, 50 monthly cases cost roughly $30,250 in chargeback costs. That’s about $297,000 a year, before VAMP exposure.

Here's how The Beard Club reduced subscription billing disputes:

Digital Goods, Gaming, and Streaming

Digital goods carry an average chargeback value of $77 to $99. Merchants in gaming, gambling, and cryptocurrency exchange are generally considered high-risk by the card network, and their chargeback value averages at $99.

Where Digital Goods, Gaming, and Streaming Disputes Come From

- Instant fulfillment removes the dispute-prevention window entirely. Digital purchases are fulfilled instantly, with no shipping delay. This removes the buffer that would otherwise give a merchant time to run a fraud check or give a customer time to reconsider before the purchase is final.

- Consumption makes “return” meaningless. Once a digital product is downloaded and used, returning it is effectively impossible. Additionally, there is no shipping address for better identity verification, unlike in physical retail, where such information can be leveraged to confirm the purchaser’s identity.

- Microtransaction regret and family fraud. Players are enticed into small in-game purchases that feel harmless in the moment, then regret them once the credit card bill arrives. Separately, a child playing on a parent’s device or card can make purchases that the parent never notices until the statement appears. At this point, it gets disputed as unrecognized rather than resolved as a family matter.

- Forgotten renewals concentrated around specific windows. Players forget they subscribed to a season pass or recurring plan. That’s why disputes concentrate heavily around monthly renewal windows. The same mechanic is driving subscription disputes generally, just compressed into a gaming-specific cadence.

- Account takeover. A fraudster can steal login credentials, make extensive in-game purchases, then sell the loaded account on a third-party marketplace. The real owner discovers the charges later and disputes them. The platform is left to absorb a loss that started as a security breach rather than a billing disagreement.

How to Reduce Digital Goods, Gaming, and Streaming Billing Disputes

- Descriptors that name the actual item, not the studio. Billing descriptors should show the specific game and item purchased. Cardholders then recognize the charge immediately.

- A faster in-app refund path than the bank’s dispute button. If a player can fix an accidental purchase in two taps, the incentive to call the bank disappears.

- Tiering disputes by value, not fighting everything equally. Auto-refund weak, low-value cases. Auto-fight high-value or repeat offenders. Send only genuine edge cases to manual review.

- Connecting payment data to actual usage data. Was the item used in an active session? Was the device familiar? Generic fraud tools were never built to answer that. Without it, every dispute is a coin flip; the merchant usually loses.

Here's how Fenatics reduced digital goods billing disputes:

Retail eCommerce

Retail eCommerce had an average chargeback value of $84 in 2025.

The reason codes that dominate this sector are materially different in kind from those fueling subscription, travel, or digital goods billing disputes. Retail is the one category where a physical item is actually supposed to move from a warehouse to a doorstep. The evidence a merchant needs looks completely different, too.

Where Retail eCommerce Disputes Come From

- Item not received. This is the billing dispute filed when a customer reports that they never received the goods they paid for. It splits into two cases needing different defenses. Tracking shows delivery, but the buyer claims it never arrived. Or the order genuinely never shipped or got lost in transit.

- Item not as described, or defective. This covers everything from shipping damage to a disputed quality claim. It’s the second most common non-fraud chargeback reason retailers face.

- Poor customer service. When merchants delay responding to refund requests, buyers often escalate the issue to a chargeback, frustrated by the lack of timely communication. The dispute was about the silence, not the product.

How to Reduce Retail Billing Disputes

- Signature confirmation above your average order value. Requiring signature confirmation on orders above your typical order value closes off the most common item-not-received claim. A delivered package with no signature is a much easier claim to win against.

- Listings that match the box, not the marketing. Most “not as described” disputes start from a real gap between expectation and reality, even on an accurate listing. Multiple clear photos close that gap before shipping.

- Contemporaneous documentation, not evidence built after the fact. What wins a 13.3 dispute is documentation captured at or near the time of sale: listing screenshots, delivery confirmation, shipped-item photos. Nothing assembled afterward holds the same weight, which is why you need an autopilot chargeback evidence capturing.

- Fast response to the complaint, before it becomes a dispute. Most “not as described” disputes start as a customer service complaint that never got resolved. Often, the cheapest fix is just answering faster.

Pour conclure

A billing dispute is a broad term for all billing-related controversies between you and your customers. A chargeback is the specific, card-network mechanism this guide has focused on, because that’s where the cost is highest, the deadlines are tightest, and the most is at stake.

Most disputes trace back to a handful of recurring causes: unauthorized charges, billing errors, product or service issues, and subscription problems. Which ones you see most often depends heavily on the sector. Subscription businesses lose the most ground in the free-trial conversion and the cancellation flow. Travel and hospitality carry the highest cost per case and the most complex evidence requirements. Digital goods face disputes with no shipping label to point to. Retail e-commerce splits its exposure between item-not-received and not-as-described claims, each requiring different proof.

Underneath all four sectors sits the same structural pattern. The card networks already offer a pre-chargeback, but each only covers its own network, and none follow a transaction through to representment. Savvy merchants close that gap with a tool like Chargeflow, which keeps your business ready for disputes across every network at once, not just the one with the best alert system.

That readiness shouldn't depend on one person checking the right dashboard at the right moment. It should just be how the system runs: preventing and recovering billing disputes without lifting a finger.

Rétrofacturations ?

Ce n'est plus votre problème.

Récupérez 4 fois plus de rétrofacturations et prévenez jusqu’à 90 % de celles à venir, grâce à l’IA et à un réseau mondial de 20 000 commerçants.

.png)