%201.svg)

Contestations de paiement Amex : le guide complet pour prévenir et résoudre les litiges en 2026

Des rétrofacturations ?

Ce n'est plus votre problème.

Récupérez 4 fois plus de rétrofacturations et prévenez jusqu’à 90 % de celles à venir, grâce à l’IA et à un réseau mondial de 20 000 commerçants.

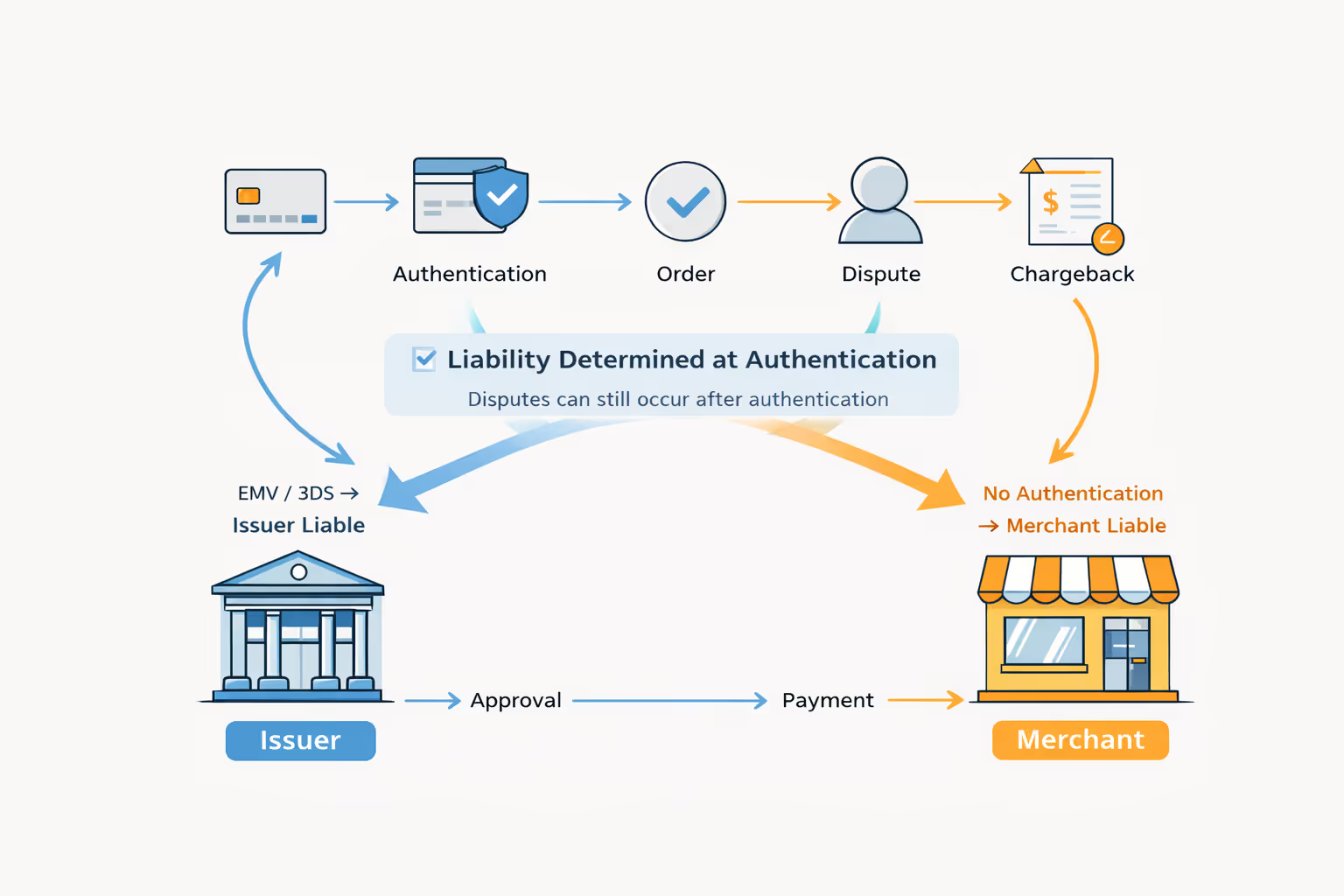

Les rétrofacturations Amex ne laissent guère de marge d'erreur aux commerçants : le processus est centralisé, les délais de réponse sont courts et les programmes de surveillance peuvent restreindre les droits de paiement. Les titulaires de carte disposent généralement de 120 jours pour contester un prélèvement, et les commerçants ont généralement 20 jours pour y répondre. En tant que commerçant, vous devez mettre en place des mesures de prévention, un système de collecte de preuves et un processus de réponse aux contestations conçu pour respecter les délais et les exigences documentaires d'Amex.

- Les litiges liés à American Express sont traités plus rapidement et font l'objet de moins d'allers-retours que les rétrofacturations Visa/Mastercard, car American Express est à la fois un réseau et un émetteur.

- En règle générale, les commerçants ne disposent que de 20 jours pour fournir des justificatifs après avoir reçu la notification, un délai plus court que celui imposé par de nombreux autres réseaux.

- Parmi les codes de motif couramment utilisés par American Express, on trouve la fraude (codes de rejet de débit 4526/F24), les biens/services non reçus (C08) et le crédit non traité (C05).

- La gestion proactive des litiges Amex grâce à la soumission automatisée des pièces justificatives permet de réduire les risques liés aux délais de réponse et les pertes de chiffre d'affaires.

Un rejet de paiement Amex (appelé « litige » par American Express) permet aux titulaires de carte d'annuler un prélèvement directement auprès d'Amex, puisque cette dernière fait office à la fois de réseau de cartes et de banque émettrice. Les commerçants disposent d'un délai limité (généralement de 20 jours) pour présenter des preuves convaincantes avant que le litige ne soit tranché par défaut en faveur du titulaire de la carte.

| Étape | Qui | Action | Calendrier type |

|---|---|---|---|

| 1. Recours introduit | Titulaire de la carte | Contactez Amex en ligne ou par téléphone pour contester un prélèvement | Dans un délai de 120 jours à compter de la transaction |

| 2. Le commerçant a été informé | Amex | Envoie un avis de contestation accompagné d'un code de motif au commerçant | 1 à 3 jours ouvrés |

| 3. Pièces à conviction produites | Commerçant | Télécharge les reçus, les accusés de réception et la correspondance | 20 jours à compter de la notification |

| 4. Avis sur Amex | Amex | Évalue les éléments de preuve au regard des critères du code de motif | 7 à 30 jours |

| 5. Résolution | Amex | Le montant est soit recrédité au commerçant, soit remboursé au titulaire de la carte | Variable |

American Express est le troisième réseau de cartes de crédit aux États-Unis. La carte Amex est acceptée dans plus de 160 millions de points de vente à travers le monde et a traité plus de 1 670 milliards de dollars de transactions en 2025. C'est également le réseau de cartes que les commerçants connaissent le moins, et cette méconnaissance leur coûte cher.

Contrairement à Visa ou Mastercard, Amex joue souvent à la fois le rôle de réseau et de banque émettrice, ce qui lui permet de contrôler la majeure partie du processus de contestation. Les titulaires de carte disposent généralement d'un délai de 120 jours pour contester un prélèvement, avec peu de possibilités de faire de nouvelles tentatives. Les commerçants ont généralement 20 jours pour répondre, soit moins que n'importe quel autre grand réseau, et n'ont qu'une seule chance de trouver la bonne réponse.

Si vous manquez cette échéance, ne répondez pas de manière satisfaisante ou dépassez les seuils liés aux taux de fraude et de rétrofacturation, vous risquez de vous retrouver soumis à l'un des trois programmes de surveillance punitifs dont de nombreux commerçants ne soupçonnent l'existence qu'une fois qu'ils y ont été inscrits. Pour gérer efficacement les rétrofacturations d'Amex, il faut d'abord bien cerner le contexte.

Comment fonctionnent les rétrofacturations American Express

Un rejet de débit Amex est une annulation forcée d'une transaction initiée par un titulaire de carte et traitée au sein du système en circuit fermé d'Amex, dans lequel Amex joue simultanément le rôle de réseau de cartes, d'émetteur et de décideur principal.

Comme Amex a une vue d'ensemble de la transaction, elle dispose d'une meilleure visibilité que les réseaux qui s'appuient sur des banques émettrices distinctes. Visa et Mastercard s'appuient sur des banques membres qui n'ont pas toujours la même visibilité sur les transactions.

Ce système présente à la fois des avantages et des inconvénients. American Express indique qu’en 2025, seule une infime partie des transactions par carte a donné lieu à des litiges transmis aux commerçants. Cela laisse supposer un examen interne approfondi de leur part. Pour les commerçants, cela signifie que les litiges qui leur sont transmis ne sont pas des plaintes aléatoires, mais des cas qu’Amex a déjà examinés et jugés dignes d’être portés à leur attention.

Amex est également mieux placée pour détecter des schémas tels que la fraude amicale, car elle peut mettre en corrélation le comportement des titulaires de carte chez différents commerçants. Cependant, sa procédure de règlement des litiges a toujours tendance à donner raison au titulaire de la carte. Et les commerçants ont peu de moyens de contester la classification interne d'Amex une fois qu'un dossier a été classé.

Comprendre la procédure de contestation de paiement d'American Express

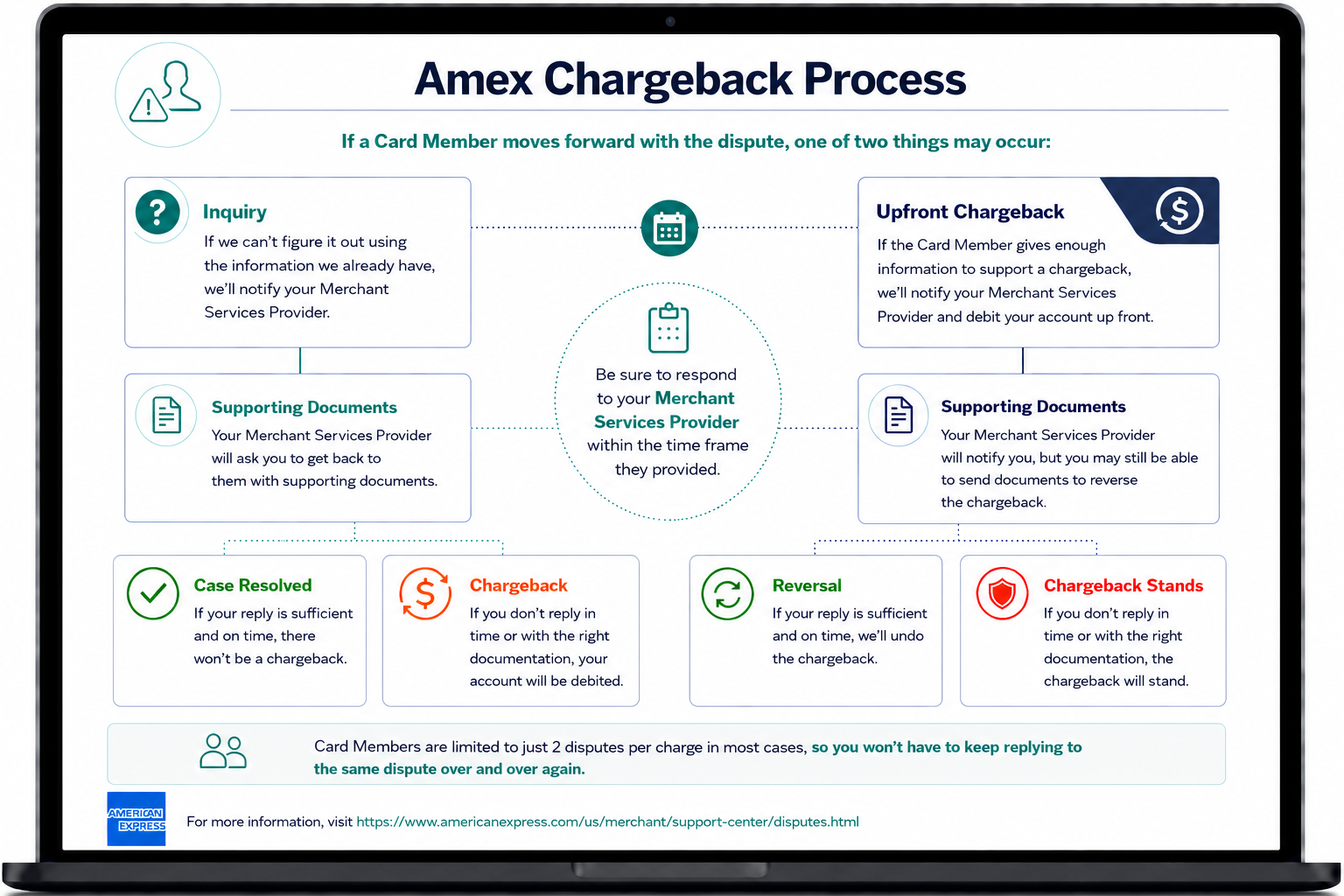

Lorsqu'un titulaire de carte conteste un prélèvement, Amex peut rejeter la réclamation, envoyer une demande de renseignements au commerçant ou procéder immédiatement à un rejet de débit. La phase de demande de renseignements, lorsqu'elle intervient, constitue pour le commerçant la meilleure occasion de régler le litige avant même qu'il ne débouche sur un rejet de débit. Amex envoie une demande de renseignements lorsqu'elle a besoin de plus d'informations ; elle peut toutefois sauter cette étape lorsque la réclamation semble fondée à première vue, en cas de suspicion de fraude ou si le commerçant fait déjà l'objet d'un programme de surveillance.

Si une demande est envoyée, le commerçant dispose de 20 jours à compter de la date de traitement par Amex, appelée « Central Site Business Date », pour y répondre. Cette date correspond au moment où Amex traite le dossier, et non à celui où le commerçant prend connaissance de la notification pour la première fois ; les retards internes peuvent donc réduire ce délai sans que l'on s'en aperçoive. Une réponse insuffisante ou tardive entraîne le traitement du rejet de débit.

Une fois qu’un rejet de débit Amex a été émis et confirmé, les fonds sont débités et la décision est difficile à contester. Contrairement à Visa et Mastercard, qui proposent des procédures d’escalade plus formalisées, le processus de rejet de débit d’Amex laisse aux commerçants peu de possibilités de recours. Il convient de noter que les commerçants qui traitent les paiements Amex via un acquéreur tiers (OptBlue) doivent suivre les procédures de contestation de cet acquéreur, qui peuvent différer des règles directes d’Amex. L'image ci-dessous présente le processus de rejet de débit d'Amex :

Pourquoi les titulaires de cartes Amex demandent-ils des rétrofacturations ? Codes de motif de rétrofacturation American Express

Chaque contestation de paiement American Express est accompagnée d'un code de motif qui précise pourquoi le client a contesté la transaction et quel type de preuve est pertinent. Amex regroupe ces codes en plusieurs catégories principales :

- Codes d'autorisation de la série A , relatifs à des problèmes tels que l'absence ou l'invalidité de l'autorisation.

- Codes de litige relatifs aux titulaires de carte de la série C, concernant des marchandises non livrées, des remboursements ou des annulations.

- Les codes de fraude de la série F, qui sont les plus difficiles à obtenir pour les commerçants.

- Codes divers de la série M, concernant le montant, la devise et d'autres divergences de ce type.

- Codes de fraude de la série FR avec recours intégral, dans lesquels la possibilité pour le commerçant de contester est fortement limitée.

Pour de nombreux commerçants, les pertes les plus évitables sont celles liées aux litiges de type C : descriptions de facturation peu claires, procédures de remboursement lentes ou opaques, et procédures d'annulation complexes. S'attaquer à ces problèmes de manière proactive permet souvent d'éviter les rejets de débit plus efficacement que de les contester a posteriori.

Pour une description détaillée de chaque code et des justifications recommandées, consultez notre guide complet des codes de motif Amex.

Délais de contestation des transactions Amex

Les délais de contestation d'Amex constituent l'un des calendriers les plus déséquilibrés dans le domaine des paiements par carte.

Les titulaires de carte disposent d'un délai de 120 jours à compter de la date de la transaction pour introduire un litige. Pour certaines catégories, ce délai court à compter d'événements tels que la date de livraison prévue ou la date à laquelle la défaillance du service est apparue, et non à compter de la date d'achat. Une transaction effectuée en janvier peut ainsi faire l'objet d'un litige plusieurs mois plus tard.

Les commerçants, en revanche, disposent d’un délai de 20 jours à compter de la date de transaction du site central pour répondre. Étant donné que ce délai commence à courir dès qu’Amex traite le dossier, et non lorsque le commerçant prend connaissance de l’avis, tout retard interne réduit le délai de réponse effectif. Comparé aux quelque 30 jours accordés par Visa et aux 45 jours accordés par Mastercard, le délai de 20 jours d’Amex laisse aux commerçants la marge de manœuvre la plus réduite pour faire face aux retards.

Une fois la réponse envoyée, le règlement des litiges Amex prend souvent plusieurs semaines, période durant laquelle le montant contesté sera bloqué. Pour les commerçants, la conclusion pratique est simple : vérifiez la date de transaction indiquée sur le site central, remontez dans le temps à partir de cette date butoir et considérez chaque jour comme un délai impératif.

Les trois programmes de suivi dont la plupart des commerçants ignorent l'existence

Amex gère trois programmes de surveillance des commerçants destinés à réduire la fraude et à gérer les commerçants faisant l'objet d'un nombre élevé de litiges : le programme de recours intégral en cas de fraude, le programme de rejet de débit immédiat et le programme de rejet de débit immédiat partiel.

Ces trois programmes visent à inciter les commerçants à renforcer leurs pratiques en matière de gestion des transactions et des litiges. Examinons-les de plus près :

Programme de recours intégral en cas de fraude

Le programme de recours en cas de fraude d'Amex se déclenche lorsque le volume de vos transactions frauduleuses dépasse les limites fixées par Amex. Une fois que vous y avez adhéré, Amex peut traiter les rétrofacturations liées à la fraude de manière accélérée et rejettera toute tentative du commerçant de demander une annulation.

Concrètement, vous renoncez totalement à votre droit de contester les litiges liés à la fraude, même si vous êtes certain que la transaction initiale était légitime. Seule exception : si vous pouvez prouver que le titulaire de la carte a déjà été remboursé du montant litigieux, celui-ci peut alors fournir des pièces justificatives en réponse.

Conditions d'admission :

- Adopter des pratiques commerciales frauduleuses, trompeuses, collusoires ou déloyales

- Implication dans des activités illégales ou utilisation frauduleuse de cartes

- Un ratio de frais « fraude sur chiffre d'affaires » (FTG) qui dépasse le seuil de la tranche basse ou de la tranche haute

Le programme de recours intégral en cas de fraude est divisé en deux niveaux : bas et élevé.

Niveau inférieur

Conditions (les deux doivent être remplies) :

- Taux de fraude mensuel égal ou supérieur à 0,9 % du montant brut des frais

- Litiges liés à la fraude portant sur un montant total d'au moins 25 000 dollars au cours d'un même mois

Ce qui se passe : les restrictions prennent effet dès lors que vous dépassez le seuil pendant trois mois consécutifs à compter de la notification d'Amex. À ce stade, le commerçant est soumis à des rétrofacturations avec recours intégral en cas de fraude et perd toute protection contre la responsabilité en cas de fraude précédemment accordée par SafeKey.

Comment sortir du programme : vous devez ramener votre taux FTG en dessous de 0,9 % et maintenir le montant total des litiges liés à la fraude en dessous de 25 000 $ pendant trois mois consécutifs. Amex se réserve également le droit de retirer un commerçant du programme de manière unilatérale.

Haut de gamme

Conditions (les deux doivent être remplies) :

- Taux mensuel de fraude égal ou supérieur à 1,8 % du montant brut des frais

- Litiges liés à la fraude portant sur un montant total d'au moins 50 000 dollars au cours d'un même mois

Ce qui se passe : contrairement au niveau « Low Tier », il n'y a pas de délai de grâce. Les restrictions prennent effet immédiatement après notification par Amex. Le commerçant perd d'emblée ses droits en matière de contestation de rejet de débit ainsi que la protection de responsabilité offerte par SafeKey.

Conditions de sortie : identiques à celles du niveau « Low Tier » : taux de fraude (FTG) inférieur à 0,9 % et litiges liés à la fraude inférieurs à 25 000 $ pendant trois mois consécutifs. Amex peut également décider de retirer des commerçants de ce programme à sa seule discrétion.

Programme de remboursement immédiat

Ce programme s'applique aux commerçants dont le taux global de rétrofacturation, et non pas uniquement celui lié à la fraude, est systématiquement trop élevé. Lorsqu'un commerçant dépasse le seuil de rétrofacturation fixé par Amex pendant trois mois consécutifs, Amex supprime l'étape standard de demande de renseignements. Au lieu d'envoyer au commerçant une demande de renseignements à laquelle il doit répondre, Amex traite immédiatement la rétrofacturation en utilisant un code de motif spécifique. Ce programme indique souvent qu'un commerçant utilise un système de détection de la fraude inadéquat ou n'a pas mis en place les mesures de sécurité de base pour ses transactions.

Le taux de rétrofacturation se calcule comme suit : (Rétrofacturations) ÷ (Montant brut des transactions − Crédits)

Les débits bruts correspondent au montant total des transactions réglées, tandis que les crédits correspondent aux remboursements effectués.

Conséquences de l'inscription :

- Amex peut contourner la procédure d'enquête et procéder directement à un rejet de débit dès lors qu'un titulaire de carte conteste un prélèvement pour une raison autre que la fraude.

- Des frais de rejet de débit excessifs s'appliquent à chaque rejet de débit traité dès lors que le taux du commerçant dépasse le seuil de 1 %.

Programme de remboursement immédiat partiel

Ce programme fonctionne de manière similaire au programme de rejet de débit immédiat, mais introduit un seuil lié au montant de la transaction. Les commerçants ayant dépassé le seuil de rejet de débit pendant trois mois consécutifs sont automatiquement inscrits, mais la procédure de contournement de la vérification ne s'applique qu'aux litiges concernant des transactions dont le montant est inférieur à un seuil défini.

Les litiges concernant les transactions d'un montant plus élevé continuent de suivre la procédure habituelle de contestation et d'enquête d'Amex. Il en résulte un système à deux vitesses : des procédures de contestation accélérées pour les transactions de faible montant et des procédures standard pour les transactions plus importantes.

La même formule de calcul s'applique : (Rétrofacturations) ÷ (Montant brut des prélèvements − Crédits)

Conséquences de l'inscription :

- Les litiges concernant des transactions dont le montant est inférieur au seuil fixé en dollars peuvent faire l'objet d'un remboursement immédiat, sans enquête préalable, pour toute raison autre que la fraude.

- Les litiges concernant les transactions dont le montant est égal ou supérieur au seuil fixé sont traités conformément à la procédure standard d'Amex en matière de rétrofacturation et d'enquête.

- Les frais de rejet de débit excessifs s'appliquent à chaque rejet de débit dépassant le plafond de 1 %.

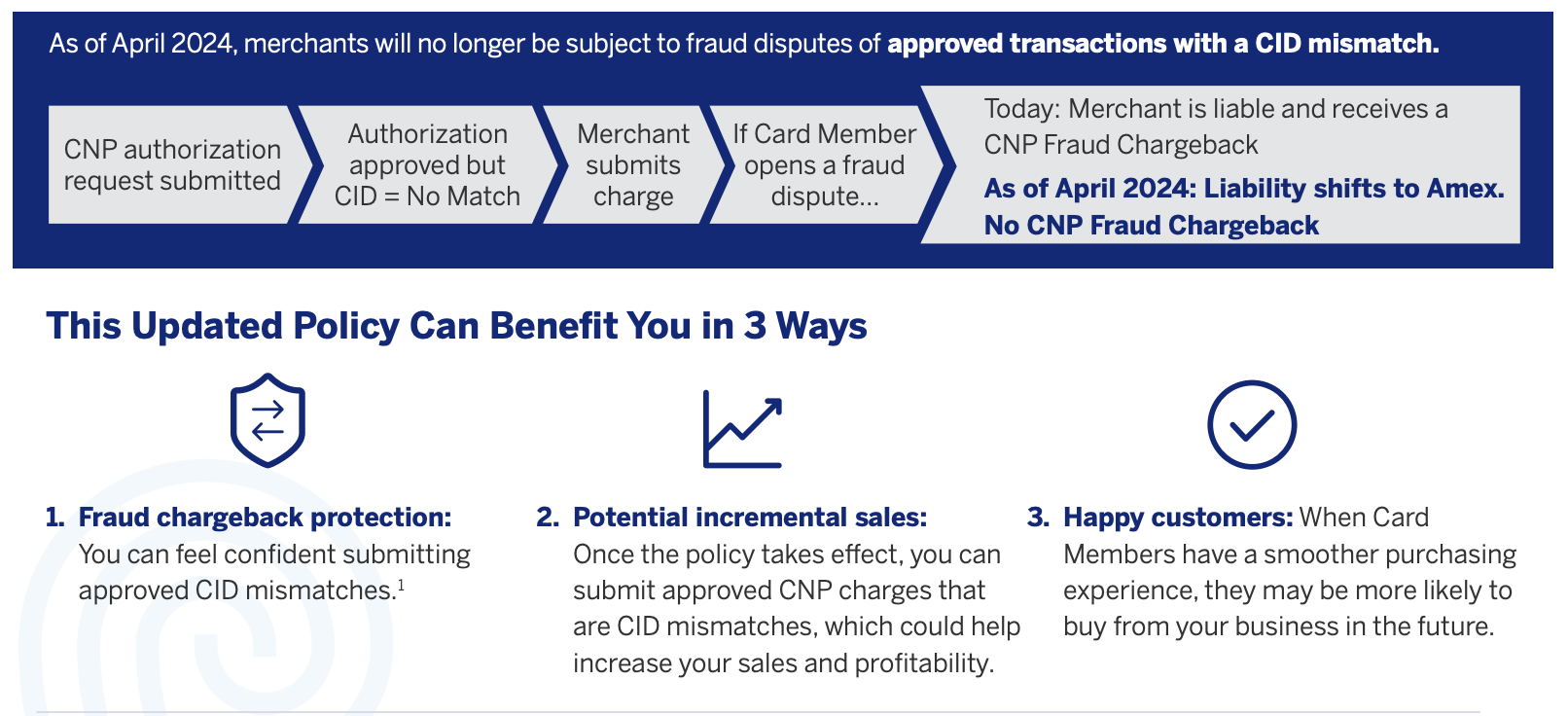

Le point sur la politique CID 2024 : le transfert de responsabilité d'Amex que vous avez peut-être manqué

En avril 2024, Amex a mis à jour sa politique relative à la vérification des informations de carte (CID), qui décharge les commerçants de leur responsabilité en cas de fraude dans certains cas de figure où la carte n'est pas physiquement présente. Lorsqu'un commerçant obtient une autorisation valide pour une transaction en ligne, tente une vérification CID et reçoit une réponse indiquant une non-correspondance (telle que « aucune correspondance », « non vérifié » ou « aucune réponse »), Amex indique qu'elle annulera les litiges liés à la fraude éligibles au lieu de les renvoyer sous forme de rétrofacturation.

Qu'est-ce qui a changé ?

Avant cette mise à jour, un commerçant pouvait encore être tenu responsable d'un rejet de paiement pour fraude dans ce cas de figure, même après une autorisation valide. Cette modification permet aux commerçants de traiter les commandes approuvées présentant une divergence de CID avec davantage d'assurance, à condition qu'ils aient mis en place la logique d'autorisation et de paiement appropriée.

Pourquoi cela devrait vous intéresser

Concrètement, ce changement de politique permet aux commerçants de craindre moins de perdre des commandes valides au moment du paiement simplement parce que la vérification du CID a échoué, ce qui pourrait réduire le taux d'abandon de panier et préserver les ventes. Il réduit également le risque qu'une transaction approuvée vienne ensuite alourdir le fardeau du commerçant en matière de fraude ou de rétrofacturation dans les cas spécifiques couverts par cette politique.

Amex précise que cette modification s'applique aux transactions autorisées sans présentation de la carte. Le commerçant a tenté de valider le CID et a reçu une réponse indiquant une non-correspondance, telle que « aucune correspondance », « non vérifié » ou « aucune réponse ». La fiche d'information indique qu'à compter d'avril 2024, les « transactions approuvées présentant une non-correspondance du CID » ne donneront plus lieu à un rejet de débit pour fraude CNP.

Restrictions importantes

Il ne s'agit pas d'une immunité générale pour tous les litiges. Cette politique concerne un cas précis de fraude et de rejet de paiement lié à une non-correspondance du CID et au statut d'autorisation, et non l'ensemble des codes de motif possibles ou tous les types de litiges. De plus, le commerçant doit toujours appliquer la logique d'autorisation et de finalisation de paiement appropriée. Amex a souligné que les commerçants pourraient devoir mettre à jour leurs processus de paiement afin de ne plus demander à nouveau le CID et d'accepter les non-correspondances.

Cette mise à jour n'élimine pas tout risque de fraude ; elle modifie simplement la répartition de la responsabilité dans le cas d'une divergence de code d'identification de la carte (CID). Il ne s'agit donc pas tant de dire qu'« Amex a supprimé les rétrofacturations » que d'affirmer qu'« Amex a transféré la responsabilité pour une catégorie spécifique de transactions en ligne approuvées ».

Comment contester un rejet de débit Amex : guide étape par étape

Pour contester un rejet de paiement Amex, il faut commencer par examiner attentivement le dossier. Vous devez comprendre le code de motif, ce qu’Amex vous demande, et déterminer si le litige porte sur une fraude, un problème de service ou tout autre sujet. Une mauvaise interprétation de ces éléments entraîne un gaspillage d’efforts et affaiblit vos arguments.

Vient ensuite la collecte des pièces justificatives. Dans la plupart des litiges, cela implique de rassembler les données d'autorisation, les détails des commandes et des factures, les registres de livraison ainsi que les communications pertinentes avec le client. L'objectif est de présenter une documentation concise et pertinente qui réponde directement au motif invoqué, plutôt qu'un dossier volumineux mais décousu.

Le respect des délais est également essentiel tout au long du processus. Les délais imposés par Amex étant serrés, les circuits de transmission et les procédures de validation internes doivent être organisés en fonction de ce délai de 20 jours. Les équipes qui s'appuient sur des échanges de courriels ponctuels ou des transferts informels risquent davantage de ne pas respecter les délais ou de soumettre des réponses incomplètes.

Le rôle de l'automatisation et les raisons pour lesquelles le secteur s'oriente vers cette voie

L'automatisation des rétrofacturations s'intègre naturellement dans le cadre proposé par American Express, car elle aide les commerçants à réagir dans les délais et à gérer efficacement les litiges. Les recommandations d'American Express mettent en avant les outils de résolution automatisée des litiges comme un moyen de rationaliser les processus, de réduire les tâches manuelles et d'améliorer les résultats tant pour les commerçants que pour les clients.

Pour les commerçants, l'intérêt de l'automatisation réside moins dans le remplacement du personnel que dans le soutien apporté à celui-ci. La gestion manuelle des litiges peut fonctionner lorsque le volume est faible, mais elle devient difficile à maintenir lorsque le nombre de cas augmente ou que le traitement des rétrofacturations entre en concurrence avec d'autres priorités. Un système structuré aide les équipes à respecter les délais, à garantir la cohérence et à tirer les leçons des litiges passés, plutôt que de traiter chaque cas comme un événement isolé.

En pratique, on constate que pour remporter un litige auprès d'Amex, il ne suffit généralement pas de disposer d'un seul document irréprochable. Il s'agit plutôt de mettre en place un processus reproductible garantissant que les preuves pertinentes soient transmises au dossier concerné avant l'expiration du délai, et de recourir à l'automatisation pour assurer la fiabilité de ce processus à grande échelle.

Comment prévenir les rejets de paiement Amex avant qu'ils ne surviennent

La plupart des guides sur la prévention des rétrofacturations vous proposent la même liste : des descriptions de paiement claires, des e-mails de confirmation et une politique de remboursement facile à trouver. Ces conseils ne sont pas faux. Mais ils sont incomplets pour Amex, et des conseils incomplets peuvent coûter cher.

Voici ce qui compte vraiment :

C'est au stade de l'enquête que les contestations de paiement sont rejetées, à condition que vous soyez présent.

Amex envoie souvent une demande de clarification avant de procéder à un rejet de débit lorsqu'un litige est ambigu. Une réponse convaincante permet de clore définitivement le dossier. Pas de rejet de débit, pas d'impact sur le taux, pas de frais. Même lorsque Amex passe outre la demande de clarification, il existe un délai au niveau du réseau que vous pouvez exploiter pour déjouer un litige imminent. Les alertes de rejet de débit informent les commerçants dès qu'un litige est lancé, leur laissant un délai de 24 à 72 heures pour effectuer le remboursement et le clore définitivement. Deux étapes différentes, une même opportunité. La plupart des commerçants passent à côté des deux en raison de la lenteur de leurs processus internes.

Gérez les ratios, pas seulement les litiges.

Les trois programmes de surveillance décrits précédemment ne sont pas déclenchés par des rétrofacturations isolées. Ils sont déclenchés par des ratios qui se maintiennent dans le temps. Cela signifie que votre stratégie de prévention ne peut pas être réactive, consistant à examiner les litiges au fur et à mesure qu’ils surviennent et à décider lesquels contester. Lorsque vos chiffres seront suffisamment mauvais pour que vous en ressentiez les conséquences, vous serez peut-être déjà soumis à un programme qui vous prive totalement de votre droit de réponse.

Surveillez vos chiffres chaque mois, comme le fait Amex. Et intervenez avant qu’une hausse ponctuelle ne devienne une tendance. Utilisez l’analyse ci-dessus pour calculer chaque mois votre ratio fraude/chiffre d’affaires et votre taux de rétrofacturation. Si l’un ou l’autre évolue dans la mauvaise direction, considérez cela comme un problème commercial, et non comme un problème relevant du service de facturation.

Sachez qu'Amex a déjà pris connaissance de la transaction.

Lorsqu'un titulaire de carte conteste un prélèvement auprès de Visa ou de Mastercard, la banque émettrice dispose souvent de données limitées au niveau de la transaction. Amex, qui est à la fois le réseau et l'émetteur, a accès en temps réel aux deux côtés de la transaction dès le moment où celle-ci est traitée. Il n'y a donc aucun vide d'information à exploiter ni aucune manipulation susceptible de contredire ce que son système a déjà enregistré.

Cela a son importance pour la manière dont vous constituez votre dossier de défense, mais c'est encore plus crucial pour la prévention. Chaque transaction que vous traitez avec Amex laisse une trace complète. Toute incohérence entre les éléments que vous fournissez comme preuves et ceux dont dispose déjà Amex vous coûtera cher. Disposer de données de transaction précises et complètes au point de vente n'est pas un simple atout. C'est votre future défense. The Beard Club s'est directement heurté à ce problème. Ses pertes liées aux litiges ne provenaient pas de transactions irrégulières, mais de dossiers incomplets qui ne résistaient pas à l'examen du réseau de cartes. Voici comment ils ont résolu le problème :

Identifiez les conflits que vous pouvez éviter et concentrez-vous sur ceux-là.

Les codes de fraude de la série F se caractérisent par un taux de réussite des commerçants particulièrement faible. Vous ne parviendrez pas à prévenir les véritables fraudes en vous contentant d'améliorer vos processus, et vous ne pourrez pas vous en sortir en contestant les transactions une fois qu'elles auront eu lieu. Dans ces cas-là, la prévention relève de la détection de la fraude, et non d'un problème de documentation.

Les litiges concernant la série C sont différents. Ces pertes sont en grande partie de notre propre fait. Elles surviennent parce qu'un client n'a pas reçu ce à quoi il s'attendait, n'a pas réussi à joindre quelqu'un pour régler le problème, ou ne savait pas comment annuler et a estimé qu'il était plus simple de déposer un litige que d'en discuter. Ce sont des problèmes qui peuvent être résolus.

L'objectif est d'éliminer toutes les raisons qui pourraient pousser un titulaire de carte à appeler Amex plutôt que de vous contacter.

Concevez vos registres en tenant compte de la période de 120 jours.

La plupart des commerçants conservent les registres des commandes et des communications pendant 30 à 60 jours. Les titulaires de cartes Amex disposent d'un délai de 120 jours pour introduire une réclamation, et dans certaines catégories de litiges, ce délai commence à courir après la date d'achat. Un client ayant effectué un achat en janvier peut légitimement introduire une demande de remboursement en mai, et si vous avez supprimé ces registres, votre dossier est déjà perdu.

Durée minimale de conservation pour toutes les transactions traitées via Amex : six mois pour les données relatives aux commandes, les confirmations de livraison, les communications avec les clients et les enregistrements d'autorisation. Pour les entreprises proposant des abonnements, cette période est prolongée afin de couvrir l'intégralité de la relation de facturation.

La prévention a ses limites. Ce qui se passe ensuite est encore plus important.

Même une entreprise bien gérée peut être confrontée à des rétrofacturations. Amex donne systématiquement raison au titulaire de la carte, le délai de réponse est le plus court du secteur et la décision est sans appel. La prévention permet d'en réduire le nombre, mais n'élimine pas le risque.

Les commerçants qui ont résolu ce problème associent la prévention à un processus de traitement suffisamment rapide et précis pour remédier à ce que la prévention ne parvient pas à empêcher. American Express l'a clairement démontré : les outils automatisés de résolution des litiges transforment la manière dont les commerçants gèrent les rétrofacturations, en rationalisant les processus, en améliorant l'efficacité et en apportant des résultats tant aux commerçants qu'à leurs clients.

Prévenez ce que vous pouvez. Automatisez le reste avec Chargeflow.

De combien de temps dispose-je pour répondre à un rejet de paiement Amex ?

Les commerçants disposent généralement d'un délai de 20 jours à compter de la date à laquelle Amex les informe d'un litige pour présenter des preuves convaincantes, bien que les délais exacts puissent varier en fonction du code de motif.

Quelle est la différence entre un litige Amex et un rejet de paiement Visa/Mastercard ?

Amex traite les litiges en interne, à la fois en tant que réseau de cartes et en tant que banque émettrice, ce qui permet souvent un règlement plus rapide et réduit le nombre d'étapes intermédiaires par rapport à Visa ou Mastercard, qui font intervenir des banques émettrices et acquéreuses distinctes.

Puis-je obtenir gain de cause dans le cadre d'un rejet de débit Amex ?

Oui : les commerçants qui fournissent des éléments de preuve clairs et présentés en temps utile (preuve de livraison, reçus signés, correspondance correspondant au code de motif) peuvent obtenir gain de cause dans le cadre d'un litige Amex.

Ne vous battez plus manuellement contre les contestations de paiement d'Amex

Vous pouvez automatiser la collecte et la transmission des justificatifs, ce qui vous évite de devoir suivre manuellement les dates limites d'Amex. Chargeflow effectue les transmissions dans les délais, à chaque fois, avec une garantie de retour sur investissement multiplié par 4.

Commencez gratuitementDes rétrofacturations ?

Ce n'est plus votre problème.

Récupérez 4 fois plus de rétrofacturations et prévenez jusqu’à 90 % de celles à venir, grâce à l’IA et à un réseau mondial de 20 000 commerçants.

.png)