%201.svg)

, la solution n° 1 en matière de rétrofacturation pour les commerçants Stripe

s à WooCommerce

et des rétrofacturations

Klarna vs Affirm Payments: Which BNPL Provider Is Better in 2026?

Rétrofacturations ?

Ce n'est plus votre problème.

Récupérez 4 fois plus de rétrofacturations et prévenez jusqu’à 90 % de celles à venir, grâce à l’IA et à un réseau mondial de 20 000 commerçants.

Vous hésitez entre Klarna et Affirm pour votre boutique ou votre prochain achat ? Voici un petit résumé :

- Klarna compte 114 millions d'utilisateurs répartis dans 26 pays, est entrée en bourse à la NYSE en septembre 2025 et vient de conclure un partenariat exclusif avec Walmart, ce qui en fait le choix le plus judicieux pour les commerçants internationaux et les entreprises proposant des abonnements.

- Affirm compte environ 23 millions d'utilisateurs, principalement aux États-Unis et au Canada, ne facture aucun frais aux consommateurs, a atteint la rentabilité au cours de l'exercice 2025 et excelle dans le financement d'achats de grande valeur (valeur moyenne des commandes : 276 $), ce qui en fait la solution la mieux adaptée aux détaillants proposant des achats d'envergure.

- Frais Klarna pour les commerçants : environ 3,29 % à 5,99 % + 0,30 $ par transaction. Frais Affirm pour les commerçants : environ 6 % + 0,30 $.

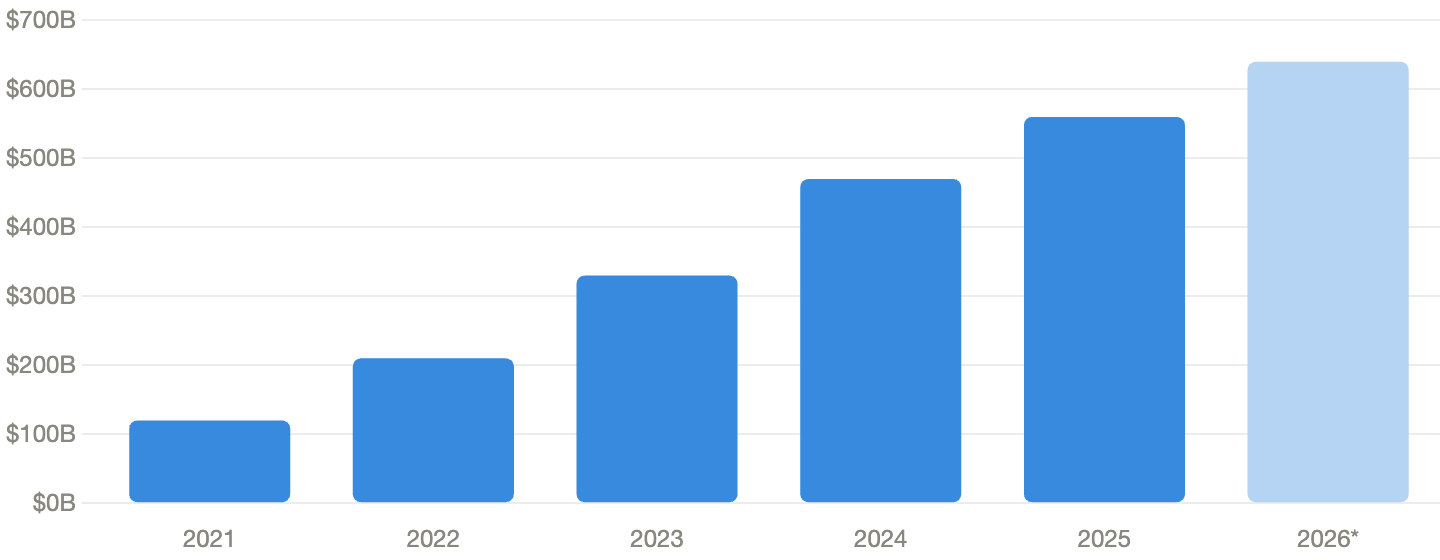

Le marché mondial du « Buy Now, Pay Later » (BNPL) a atteint environ 560 milliards de dollars de volume brut de marchandises en 2025, avec un taux de croissance annuel composé (TCAC) prévu de 20,7 %. Il n'est donc pas étonnant que les prestataires de services de paiement BNPL tels que Klarna et Affirm suscitent un vif intérêt dans le secteur.

Klarna et Affirm Payments sont en train de révolutionner le secteur du commerce électronique grâce à une gamme de fonctionnalités conçues pour répondre aux besoins variés de leurs clients. Mais le débat entre Affirm et Klarna est plus nuancé qu'il n'y paraît à première vue. Si les deux plateformes proposent des paiements échelonnés « achète maintenant, paie plus tard » (BNPL), elles se distinguent nettement en termes de frais, de couverture des commerçants, de taux d'intérêt et de marchés cibles.

C'est la question à laquelle nous souhaitons vous aider à répondre dans le guide d'aujourd'hui. Nous allons passer en revue les atouts, les avantages et les défis de Klarna et d'Affirm, en vous proposant une comparaison claire pour vous aider à déterminer quelle plateforme correspond le mieux à vos besoins en matière de paiement. Que vous choisissiez Klarna ou Affirm en tant que commerçant, ou Affirm ou Klarna en tant qu'acheteur, ce guide couvre tout ce que vous devez savoir.

Klarna vs Affirm: Side-by-Side Comparison (2026)

FactorKlarnaAffirmFounded / HQ2005, Stockholm2012, San FranciscoActive users~114M across 26 countries~23M (US & Canada)Merchant partners~850,000~377,000Merchant fee3.29%–5.99% + $0.30~6% + $0.30Consumer feesLate fee $7 after 10 daysNoneAverage order value~$101~$276FinancingPay in 4, Pay in 30, 6–36 moPay in 4, 3–48 mo (up to $17,500)Chargeback fee$15$15Public statusNYSE (KLAR), Sept 2025Nasdaq (AFRM), 2021Best forGlobal & subscription merchantsHigh-ticket US/Canada merchants

Aperçu des fonctionnalités de Klarna

Klarna est l'un des principaux prestataires de services de paiement « Achetez maintenant, payez plus tard », permettant aux consommateurs d'acheter des articles sur des sites de commerce électronique et dans des magasins physiques sans avoir à régler la totalité du montant à l'avance. Fondée à Stockholm, en Suède, en 2005, Klarna a connu une forte croissance grâce à la simplification des paiements par facture pour les clients du commerce électronique. La réduction des obstacles au paiement s'est traduite par une augmentation des ventes et un taux de conversion élevé pour l'entreprise.

Mais l'expansion rapide de Klarna a pris son essor après que l'équipe a lancé le modèle « acheter maintenant, payer plus tard » (BNPL) au début des années 2000, attirant plus de 850 000 commerçants partenaires à travers le monde et environ 114 millions de clients dans 26 pays, dont environ 34 millions aux États-Unis. Klarna est entrée en bourse à la Bourse de New York en septembre 2025, réalisant la plus importante introduction en bourse (IPO) de l'année dans le secteur des technologies financières, levant 1,37 milliard de dollars et atteignant une valorisation boursière de plus de 17 milliards de dollars dès son premier jour de cotation.

En mars 2025, Klarna a conclu un partenariat exclusif avec Walmart par l'intermédiaire de OnePay, une initiative majeure qui appartenait auparavant à Affirm. Klarna a déclaré un chiffre d'affaires de 2,8 milliards de dollars en 2024, avec un volume brut de marchandises traité de 105 milliards de dollars.

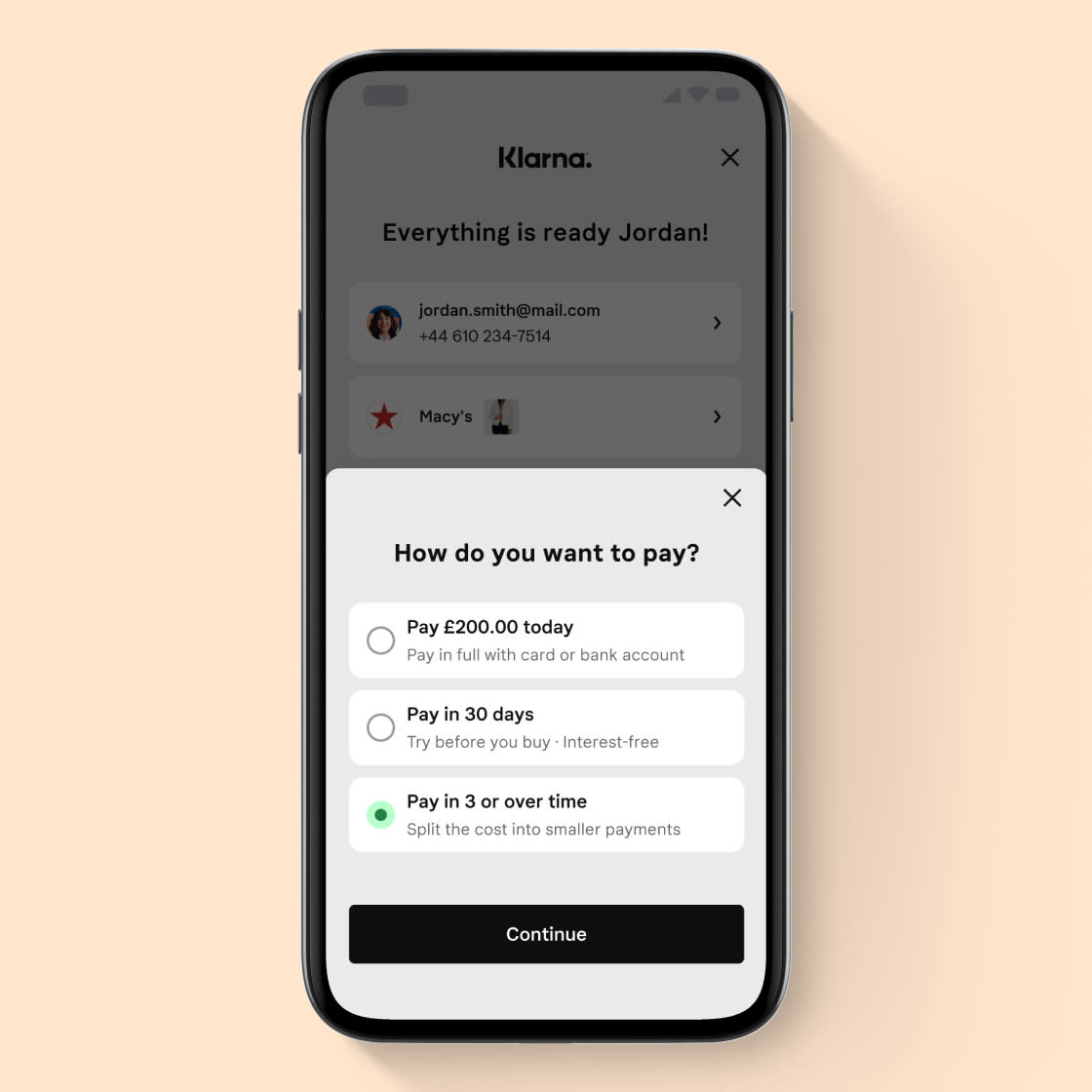

Le modèle « achat maintenant, paiement plus tard » (BNPL) de Klarna s'est révélé particulièrement avantageux pour les commerçants en ligne, car il a permis de réduire les taux d'abandon de panier, qui constituaient un véritable fléau pour le secteur en raison de la complexité des processus de paiement. L'expérience de paiement de Klarna, qui favorise la conversion, permet aux acheteurs de régler leurs achats en quatre versements sans intérêts toutes les deux semaines ou de régler la totalité du montant dans un délai de 30 jours. Klarna traiterait deux millions de transactions par jour, avec des utilisateurs de renom tels que Nike, Adidas, H&M et désormais Walmart.

Comment fonctionne Klarna ? Principales fonctionnalités

Klarna offre aux utilisateurs un processus de paiement pratique, qu'ils effectuent leurs achats sur un site de commerce électronique, via une application mobile ou dans un magasin physique. Le fonctionnement de Klarna est simple : les acheteurs choisissent Klarna lors du paiement et sélectionnent un plan de remboursement.

Klarna permet aux utilisateurs d'éviter les dettes abusives en leur offrant la possibilité de suivre leurs commandes, leurs plans de paiement et leur historique de paiement, ainsi que d'accéder au service client, le tout depuis l'application Klarna. Parmi les fonctionnalités notables de Klarna, on peut citer :

- Paiement en 4 fois : les consommateurs peuvent régler leurs achats en quatre versements sans frais, le premier étant dû au moment du paiement et les trois suivants étant prélevés toutes les deux semaines.

- Paiement différé de 30 jours : les clients peuvent effectuer leurs achats dès maintenant et régler leur commande dans les 30 jours s'ils sont satisfaits de leur achat.

- Crédits à long terme : Klarna propose des solutions de financement pour les achats importants sur une longue durée — généralement comprise entre 6 et 36 mois, avec des taux d'intérêt compétitifs à partir de 7,99 % — par l'intermédiaire de son partenaire WebBank.

- Carte Klarna : les consommateurs peuvent utiliser une carte virtuelle Klarna pour effectuer des paiements échelonnés et bénéficier d'un financement, même si le magasin auprès duquel ils effectuent leur transaction n'a pas encore intégré ce service. En 2025, Klarna a également lancé un projet pilote de carte de débit aux États-Unis, avec des fonds garantis par la FDIC.

- Stablecoin KlarnaUSD : Lancé en novembre 2025, Klarna a mis en circulation son propre stablecoin sur la blockchain de Stripe afin de réduire les coûts liés aux paiements internationaux.

- Assistant d'achat IA : Klarna a mis en place un assistant d'achat basé sur la technologie OpenAI pour aider les utilisateurs à gérer leurs dépenses et à découvrir des produits.

For banks, fintechs, and merchants, Klarna's open banking makes finance "more accessible, fair, and simple for everyone." Klarna achieves this by enabling companies to leverage its connectivity to develop new products that benefit end users. Klarna says 20,000 partners are currently using its open banking API service. Half of the top 100 U.S. online retailers used Klarna's payment tools over the past year, and two-thirds ran advertising campaigns on its platform.

Grâce à leur intégration simple et rapide, les commerçants peuvent enrichir leur boutique en proposant une option de paiement différé. Vous pouvez choisir le mode de paiement le mieux adapté à vos clients, élaborer une solution sur mesure ou procéder à l'intégration via des prestataires de services de paiement sur des plateformes telles que Shopify, WooCommerce ou Magento.

Frais Klarna : combien les commerçants doivent-ils payer ?

Le modèle économique de Klarna consiste à facturer aux commerçants des frais fixes par transaction ainsi qu'un pourcentage sur le chiffre d'affaires, de l'ordre de 5 % aux États-Unis. Ces frais sont légèrement supérieurs à ceux pratiqués par les prestataires de paiement par carte traditionnels tels que Stripe ou Shopify Payments. Il est important pour les commerçants d'avoir une bonne compréhension des frais de Klarna afin d'évaluer leurs marges. Klarna précise que ses frais peuvent également varier en fonction du pays et du service Klarna choisi par le consommateur :

- Klarna Pay Later : l'option « Pay Later » de Klarna, qui permet aux clients de régler leurs achats dans un délai de 14 à 30 jours, entraîne généralement des frais de traitement compris entre 3,29 % + 0,30 $ et 5,99 % + 0,30 $ par transaction.

- Klarna Pay Now : l'option « Pay Now » de Klarna, proposée via SOFORT, un système de virement bancaire réputé disponible en Autriche, en Belgique, en Allemagne, aux Pays-Bas et en Espagne, entraîne des frais de transaction d'environ 2,99 % + 40,30 € par transaction.

- Financement Klarna : l'option de financement à tempérament proposée par Klarna comprend des frais de transaction allant de 3,29 % + 0,30 $ à 5,99 % + 0,30 $.

- Frais de commerçant Klarna : bien qu'il n'y ait pas de frais d'inscription, les frais de commerçant Klarna varient chaque mois en fonction du contrat du commerçant et du volume de ventes.

- Frais de contestation : Klarna facture des frais de contestation d'environ 15 $ pour chaque litige lié à une transaction qui vous est opposé.

Les acheteurs peuvent également utiliser l'application Klarna chez d'autres commerçants moyennant des frais de service de 2,12 $. D'autres frais peuvent s'appliquer, tels que des frais de conversion de devises pour les paiements internationaux et des frais d'intégration. Ces frais varient en fonction de la plateforme concernée.

Les avantages de Klarna

Klarna s'est imposée comme l'un des principaux prestataires de services de paiement « achat maintenant, paiement plus tard » (BNPL) aux États-Unis et dans le monde entier. Parmi les principaux avantages de Klarna, on peut citer :

- Une présence mondiale avec environ 850 000 commerçants partenaires et environ 114 millions de clients répartis dans 26 pays.

- Les processus de paiement accélérés réduisent la durée des transactions et le taux d'abandon de panier, un problème récurrent dans le commerce électronique.

- Plusieurs options de paiement sont proposées ; les clients peuvent choisir entre « Pay in 4 », « Pay in 30 » ou des plans de financement à plus long terme.

- Les taux d'intérêt nuls proposés dans le cadre des formules « Pay in 4 » ou « Pay in 30 » favorisent la fidélisation de la clientèle, car les clients satisfaits qui peuvent étaler le paiement de leurs achats sont plus enclins à revenir.

- Klarna protège les commerçants contre les conséquences financières liées au non-paiement en assumant les risques liés à son financement.

- Klarna is easy to set up and user-friendly, integrating with major eCommerce platforms or shoppable catalogs for quick payment acceptance.

- Les mesures avancées de prévention de la fraude mises en place par Klarna permettent de réduire les pertes financières.

- Les vérifications de solvabilité informelles, qui offrent un taux d'acceptation élevé, permettent aux entreprises de générer des revenus.

- Klarna est entrée en bourse en septembre 2025, renforçant ainsi sa transparence et sa crédibilité auprès des commerçants qui évaluent les risques à long terme liés à la plateforme.

Les inconvénients de Klarna

Chaque plateforme présente des inconvénients qu'il convient d'examiner afin de prendre une décision éclairée. En ce qui concerne Klarna, les inconvénients signalés sont les suivants :

- Klarna facture aux entreprises des frais de transaction correspondant à un pourcentage du montant total de la transaction.

- Les consommateurs qui ne respectent pas les délais de remboursement se voient facturer des frais de 7 $ après 10 jours. Cependant, Klarna garantit que le montant total des frais de retard pour une commande ne dépassera pas 25 % du montant total de l'achat. Affirm a qualifié ces frais de « frais abusifs », un point à prendre en compte lorsqu'on compare Klarna et Affirm.

- Tout manquement au remboursement peut entraîner le transfert du dossier du client à une agence de recouvrement et la transmission d'informations à l'agence d'évaluation du crédit, ce qui aura un impact négatif sur sa cote de crédit.

- Selon certains analystes, comme les services « achat maintenant, paiement plus tard » (BNPL) s'appuient sur des algorithmes internes plutôt que sur les vérifications de solvabilité traditionnelles, le système peut être vulnérable à la fraude.

Présentation d'Affirm et aperçu des fonctionnalités

Affirm est un autre acteur incontournable du secteur du financement « achetez maintenant, payez plus tard ». Max Levchin, cofondateur de PayPal, a créé ce réseau de paiement en 2012. La société est entrée en bourse sur le Nasdaq en janvier 2021 et affichait, début 2026, une capitalisation boursière supérieure à 28 milliards de dollars, soit près du double de la valorisation de Klarna lors de son introduction en bourse.

En 2024, Affirm a enregistré une croissance de son chiffre d'affaires de 46 %, atteignant 2,32 milliards de dollars, soit la croissance la plus rapide parmi les principaux prestataires de services de paiement différé cette année-là, et est devenue rentable avec un bénéfice net de 52 millions de dollars au cours de l'exercice 2025.

Affirm se veut une alternative saine aux cartes de crédit. Les prêts Affirm s'accompagnent d'un échéancier de remboursement fixe, et les acheteurs connaissent leurs options avant de finaliser chaque transaction. Ainsi, ils ne paient jamais plus que le montant convenu. Les utilisateurs peuvent effectuer des transactions en ligne ou via l'application Affirm chez les commerçants participants, qui peuvent générer des numéros de carte virtuels pour les achats dans n'importe quel magasin acceptant les cartes Visa. De plus, les clients d'Affirm peuvent choisir des plans de paiement allant jusqu'à 48 mois, ce qui est plus flexible que les options traditionnelles de paiement en 4 versements proposées par des concurrents comme Klarna.

Lorsque vous créez un compte Affirm, la société évalue votre situation et vous attribue une limite de dépenses personnalisée. Bien que cette limite varie d'une personne à l'autre, elle ne peut en aucun cas dépasser 17 500 $.

Affirm compte aujourd'hui environ 23 millions d'utilisateurs actifs et 377 000 commerçants partenaires, et dispose d'intégrations poussées avec Amazon, Shopify et, jusqu'en mars 2025, Walmart.

Principales fonctionnalités d'Affirm

Affirm est un service de financement d'achats proposé en collaboration avec des commerçants partenaires. Contrairement à certaines plateformes qui proposent des prêts à court terme en plus de services de paiement de factures ou de transfert d'argent, Affirm se concentre exclusivement sur le financement des achats. Voici quelques-unes des principales fonctionnalités d'Affirm :

- Aucuns frais : les clients ne paient ni frais de retard, ni frais de remboursement anticipé, ni frais annuels, ni frais d'ouverture ou de clôture de compte.

- Paiement en 4 fois : l'option « Paiement en 4 fois » d'Affirm vous permet de régler vos achats en quatre versements égaux sur six semaines, sans intérêts ni frais, pour des montants compris entre 50 $ et 1 000 $.

- Carte Affirm : les clients peuvent utiliser les cartes de débit Affirm pour régler la totalité du montant, comme avec une carte de paiement classique, ou opter pour des plans de paiement flexibles via l'application.

- Financement mensuel : Affirm permet aux acheteurs de financer des achats jusqu'à 17 500 $, avec des durées de remboursement allant de 3 à 48 mois à un taux annuel effectif global (TAEG) d'environ 30 %. Ce taux dépend de votre profil de risque et du commerçant concerné.

Affirm permet généralement aux commerçants de fixer des limites de crédit pour leurs clients, avec un plafond de 17 500 $. L'entreprise a conclu des partenariats avec des milliers de détaillants dans des secteurs tels que la mode, les voyages, l'électronique, la maison et le fitness. Vous pouvez effectuer vos achats via Affirm en ligne ou via l'application mobile, et pour les achats en magasin, vous pouvez utiliser la carte virtuelle.

Quels sont les frais facturés par Affirm aux commerçants ?

Affirm ne facture aucun frais aux acheteurs. Alors, combien Affirm facture-t-il aux commerçants ? Le prestataire de services de paiement différé prélève un pourcentage sur chaque transaction. Voici le détail :

- Taux d'intérêt des prêts Affirm : le taux annuel effectif global (TAEG) d'Affirm varie entre 0 % et 36 %, en fonction de la solvabilité de l'utilisateur. Selon les données de la Réserve fédérale, un utilisateur peut payer plus cher avec Affirm qu'avec une carte de crédit, dont le TAEG moyen s'élève à 19,07 %.

- Frais de traitement des transactions Affirm : les frais de traitement des transactions Affirm pour les commerçants s'élèvent à environ 6 % + 0,30 $ par achat. Ce montant peut varier en fonction du risque estimé, de la taille de l'entreprise et du programme choisi.

Affirm propose des formules personnalisées avec des solutions sur mesure aux grandes entreprises, selon une structure tarifaire différente. Parmi les autres frais figurent les commissions d'interchange et les frais de gestion des prêts facturés aux investisseurs tiers.

Les avantages d'Affirm

Affirm propose des taux d'intérêt pouvant descendre jusqu'à 0 % pour des durées allant jusqu'à 48 mois. L'intégrer à votre boutique est particulièrement avantageux pour les vendeurs d'articles haut de gamme dont le prix dépasse 500 $ et pour ceux qui ciblent les consommateurs de la génération Z, dont les dépenses sont inférieures à 100 $. Parmi les principaux avantages d'Affirm, on peut citer :

- C'est très simple de commencer ; la procédure d'inscription ne nécessite que quelques étapes et un minimum d'informations.

- Affirm procède à une vérification de solvabilité sans incidence sur le dossier de crédit des acheteurs afin d'évaluer leur solvabilité.

- Les acheteurs peuvent répartir le montant de leurs achats en quatre versements bihebdomadaires sans intérêts, le premier étant dû au moment de l'achat, ou opter pour un remboursement échelonné sur trois mois ou plus, ce qui se traduit par un taux de conversion élevé pour les commerçants.

- Le service «Pay in 4 » d'Affirmne génère aucun intérêt, ce qui lerend particulièrement attrayant pour les consommateurs de la génération Z et de la génération Y. Cela pourrait se traduire par des achats répétés pour vous.

- Les clients ne paient aucun frais en cas de retard de paiement, de remboursement anticipé, d'ouverture ou de clôture de compte. C'est là un élément clé qui distingue Affirm de Klarna en matière de frais.

- Affirm a atteint la rentabilité nette au cours de l'exercice 2025, une étape majeure qui renforce la stabilité à long terme et la confiance de ses partenaires commerçants.

- La plateforme bénéficie d'avis positifs et s'intègre aux principales boutiques en ligne, notamment Amazon et Shopify.

Les inconvénients d'Affirm

Les prestataires de services « acheter maintenant, payer plus tard » (BNPL) tels qu'Affirm ont fait l'objet de critiques pour diverses raisons. Les inconvénients notables d'Affirm sont les suivants :

- Affirm propose des options sans intérêts, mais certains plans à long terme sont plus coûteux que le financement par carte, avec des taux d'intérêt pouvant atteindre 36 %.

- Bien qu'Affirm ne facture pas de frais de retard, un défaut de paiement de plus de 120 jours pourrait entraîner le transfert de votre prêt à une agence de recouvrement, ce qui pourrait nuire à votre cote de crédit.

- Affirm facture aux entreprises des frais de transaction correspondant à un pourcentage du montant total de la transaction.

- Le remboursement d'une commande Affirm équivaut à un remboursement par carte de crédit, mais Affirm prélève des frais sur chaque transaction.

- En mars 2025, Affirm a perdu son partenariat exclusif avec Walmart dans le domaine du paiement différé au profit de Klarna, ce qui a porté un coup dur à sa présence sur le marché américain de la vente au détail.

Klarna vs Affirm : les principales différences

Les services de paiement différé proposés par Klarna et Affirm sont, dans une large mesure, assez similaires. Mais les différences ne manquent pas. En comparant de près Klarna et Affirm, on constate des différences notables en matière de frais, de couverture géographique et de montant des achats. Examinons ces distinctions afin de vous aider à déterminer quelle plateforme vous convient le mieux.

Modes de paiement

- Klarna :

- Propose plusieurs formules de paiement flexibles, notamment le paiement en 4 fois, le paiement dans les 30 jours et des options de financement à long terme via WebBank.

- Un acompte de 25 % du montant de la transaction est exigé.

- Il n'y a pas de montant minimum de dépenses requis et aucune limite de dépenses n'est prédéfinie. À la place, une décision d'approbation automatique est prise à chaque fois que vous remboursez votre prêt, ce qui détermine le montant que vous pouvez dépenser.

- Affirmer :

- Propose des formules de paiement en 4 ou 2 versements, en 30 versements, ou des prêts à long terme d'une durée généralement comprise entre 3 et 48 mois.

- Les clients peuvent bénéficier du programme « Payez plus tard » pour les transactions éligibles supérieures à 100 $ et financer des achats jusqu'à 17 500 $.

- Permet d'effectuer des achats sans apport initial.

Taux d'intérêt et frais

- Klarna :

- Propose généralement des facilités de paiement sans intérêts pour les options à court terme.

- Les financements à plus long terme sont assortis d'un taux d'intérêt à partir de 7,99 % pouvant aller jusqu'à 29,99 %.

- Des frais de 7 $ sont facturés après 10 jours de retard de paiement.

- Pourrait signaler les retards et les défauts de paiement à l'agence d'évaluation du crédit.

- Les frais de commission varient chaque mois en fonction du contrat du commerçant et du volume des ventes.

- Affirmer :

- En général, les prêts « Pay in 4 » sont proposés sans frais d'intérêt.

- Taux d'intérêt pour les financements à long terme pouvant atteindre 36 % TAEG.

- Ne facture ni frais de retard ni intérêts composés en cas de paiement tardif.

- Les frais facturés aux commerçants varient en fonction du risque perçu, de la taille de l'entreprise et du programme choisi.

Les deux plateformes facturent des frais de rejet de paiement de 15 $.

Disponibilité et acceptation

- Klarna :

- Elle s'adresse à une clientèle variée et collabore avec environ 850 000 commerçants répartis dans 26 pays.

- Largement adoptée dans les principaux secteurs de la distribution, du voyage et de l'hôtellerie, de la santé et du bien-être, ainsi que de l'automobile.

- 114 millions de consommateurs actifs d'ici 2025.

- Cotée à la Bourse de New York (NYSE) sous le symbole KLAR depuis septembre 2025.

- Les utilisateurs doivent être résidents des États-Unis ou de leurs territoires, être âgés d'au moins 18 ans, disposer d'une carte bancaire ou d'un compte bancaire valide, avoir un historique de crédit positif et être en mesure de recevoir des codes de vérification par SMS.

- Des taux d'approbation plus élevés.

- Affirmer :

- S'adresse principalement aux entreprises qui vendent directement aux consommateurs américains et canadiens.

- Ne fonctionne pas avec les secteurs du commerce électronique à haut risque.

- Environ 23 millions d'utilisateurs actifs et 377 000 commerçants actifs début 2026.

- Les utilisateurs doivent être résidents des États-Unis, du Canada ou d'Australie, être âgés d'au moins 18 ans, disposer d'une carte bancaire ou d'un compte bancaire valide, avoir un historique de crédit positif et être en mesure de recevoir des codes de vérification par SMS.

- Des taux d'approbation plus faibles.

Public cible

- Ces deux plateformes attirent principalement les jeunes.

- Selon Klarna, 80 % des abonnés de son compte Instagram ont moins de 34 ans, 60 % de ses clients sont des femmes et 40 % des hommes.

- Selon Affirm, ses services séduisent particulièrement les milléniaux et la génération Z, 46,14 % des utilisateurs se déclarant hommes et 53,86 % femmes.

Quel est le meilleur : Klarna ou Affirm ? Le verdict final

Klarna et Affirm Payments ont révolutionné la manière dont les consommateurs effectuent leurs paiements et profitent des produits qu'ils aiment. Ces solutions sont sûres, regorgent de fonctionnalités et proposent généralement des taux d'intérêt raisonnables. Les intégrer à votre boutique vous aide à augmenter le panier moyen et à réduire le taux d'abandon de panier. Alors, quelle est la meilleure option pour votre entreprise : Klarna ou Affirm ? Et pour les consommateurs, quelle est la meilleure solution : Affirm ou Klarna ? La réponse dépend de votre cas de figure. Voici notre verdict pour savoir lequel est le meilleur, Klarna ou Affirm :

Quand choisir Klarna

- Service d'abonnement: Klarna permet aux clients de s'abonner à des services et d'enregistrer leurs préférences de paiement pour les renouvellements automatiques. Les clients peuvent gérer leurs paramètres dans l'application Klarna.

- Produit à la demande: le fait de choisir Klarna comme mode de paiement par défaut dans un portefeuille numérique simplifie l'achat en un clic d'articles à la demande grâce à des options de paiement flexibles.

- Fournisseur de services bancaires ouverts: les prestataires proposant des services « Pay Now » peuvent permettre à leurs utilisateurs de contourner les réseaux de cartes bancaires en payant Klarna directement depuis leur compte bancaire.

- PME actives à l'international : Klarna offre une couverture plus étendue.

- Les entreprises qui ciblent les clients de Walmart : suite au partenariat exclusif conclu en mars 2025 entre Klarna et Walmart/OnePay, Klarna est désormais le prestataire de services de paiement différé (BNPL) de référence pour le plus grand détaillant au monde.

Quand choisir Affirm

- Achats importants: les consommateurs ont souvent recours à Affirm pour leurs transactions en ligne d'un montant élevé, car cette solution est à la fois fiable et économique. Le montant moyen des commandes sur Affirm, qui s'élève à 276 dollars, est près de trois fois supérieur à celui de Klarna (environ 101 dollars), ce qui en fait une solution idéale pour les commerçants proposant des produits haut de gamme.

- Urgences: les utilisateurs d'Affirm comptent sur la plateforme pour faire face à des dépenses imprévues, telles que des réparations automobiles ou des urgences médicales.

- Transactions locales aux États-Unis ou au Canada: si votre clientèle est basée aux États-Unis et au Canada et que vous disposez d'une excellente solvabilité, Affirm pourrait être la solution la plus adaptée à vos besoins.

- Offres sans frais : si vos clients sont sensibles aux frais de retard et aux pénalités, le modèle sans frais d'Affirm constitue un avantage concurrentiel indéniable par rapport à Klarna.

- Commerçants Amazon : grâce à son intégration poussée à Amazon, Affirm s'impose comme l'option de paiement différé par défaut sur l'une des plus grandes places de marché au monde.

Comment Chargeflow accompagne les commerçants proposant le paiement différé

Regardless of which BNPL provider you choose, disputes still reach you as chargebacks. Chargeflow helps Buy Now, Pay Later merchants prevent and recover false and fraudulent chargebacks on autopilot, with automated chargeback protection and real-time chargeback prevention alerts that stop much of the friendly fraud these platforms attract. The success-based pricing means you only pay for cases won, and our dispute win rates have consistently exceeded industry averages.

Prenez le contrôle de vos rétrofacturations dès aujourd'hui ! Notre technologie de pointe, notre intégration transparente et notre taux de réussite exceptionnel dans le règlement des litiges sont parfaits pour les entreprises de commerce électronique qui souhaitent améliorer leurs processus de paiement et protéger leur chiffre d'affaires. Voici comment vous lancer.

Foire aux questions : Klarna ou Affirm ?

Quelle est la différence entre Klarna et Affirm ?

La principale différence entre Klarna et Affirm réside dans leur couverture géographique, leurs structures tarifaires et le montant des achats. Klarna dessert 114 millions de consommateurs dans 26 pays et facture des frais de retard à partir de 7 $ après 10 jours. Affirm dessert environ 23 millions d'utilisateurs, principalement aux États-Unis et au Canada, ne facture aucun frais aux consommateurs et est mieux adapté aux achats de montant élevé, avec une moyenne de 276 $ par commande.

Quel est le meilleur choix pour les commerçants : Klarna ou Affirm ?

Le choix entre Klarna et Affirm dépend de votre clientèle et du montant moyen de vos commandes. Si vous vendez à l'international ou à un large public, Klarna offre une plus grande portée mondiale et des taux d'acceptation plus élevés. Si vous vendez des articles haut de gamme aux États-Unis et que vous recherchez un modèle sans frais que vos clients apprécieront, Affirm est le meilleur choix.

Quel est le meilleur choix pour les consommateurs : Affirm ou Klarna ?

Pour les consommateurs qui hésitent entre Affirm et Klarna, la question clé est la suivante : préférez-vous ne payer aucun frais ou bénéficier d'options de remboursement plus souples ? Affirm ne facture jamais de frais de retard, de frais cachés ni de pénalités de remboursement anticipé. Klarna propose une plus grande variété de plans de paiement et est acceptée par un plus grand nombre de commerçants à l'échelle mondiale, mais facture des frais de retard.

Combien Affirm facture-t-il aux commerçants ?

Les frais de transaction d'Affirm s'élèvent à environ 6 % + 0,30 $ par achat. Ce taux est légèrement supérieur à celui de Klarna, qui varie généralement entre 3,29 % + 0,30 $ et 5,99 % + 0,30 $. Les deux plateformes facturent des frais de rejet de paiement de 15 $. Affirm peut proposer des tarifs personnalisés aux commerçants professionnels.

Quels sont les frais facturés par Klarna aux commerçants ?

Les frais Klarna pour les commerçants varient en fonction du produit utilisé. Les frais liés à Klarna Pay Later vont de 3,29 % + 0,30 $ à 5,99 % + 0,30 $ par transaction. Les frais liés à Klarna Pay Now (via SOFORT) s'élèvent à environ 2,99 % + 0,30 $. Il n'y a pas de frais d'installation, mais les frais mensuels varient en fonction du contrat et du volume des ventes. Des frais de rejet de paiement de 15 $ s'appliquent par litige.

Comment fonctionne Klarna ?

Au moment de passer commande, les clients sélectionnent Klarna comme mode de paiement et choisissent une formule : « Pay in 4 » (quatre versements bihebdomadaires sans intérêts), « Pay in 30 » (paiement intégral dans les 30 jours) ou un financement mensuel (de 6 à 36 mois via WebBank). Klarna règle le commerçant d'avance et recouvre les remboursements auprès du consommateur. Les clients peuvent gérer leurs paiements, suivre leurs commandes et accéder à l'assistance depuis l'application Klarna.

Quel est le meilleur choix, Klarna ou Affirm, pour les achats coûteux ?

Pour les achats de montant élevé, Affirm est généralement plus avantageux. Affirm propose des financements allant jusqu'à 17 500 $ sur des durées pouvant atteindre 48 mois, et le montant moyen de ses commandes, à 276 $, est nettement supérieur à celui de Klarna, qui s'élève à environ 101 $. Si vous vous demandez quelle est la meilleure option, Klarna ou Affirm, pour un achat de plus de 1 000 $, les plans à plus long terme d'Affirm ont tendance à être plus compétitifs, même si les taux d'intérêt peuvent atteindre 36 % de TAEG sur les plans prolongés.

Klarna aurait-il ravi Walmart à Affirm ?

Oui. En mars 2025, Klarna a conclu un partenariat exclusif avec Walmart par l'intermédiaire de sa filiale de fintech OnePay, remplaçant ainsi Affirm en tant que fournisseur de services de paiement différé (BNPL) de Walmart. Il s'agit là de l'un des changements les plus marquants survenus ces dernières années dans la rivalité entre Klarna et Affirm, et cela a considérablement renforcé la position de Klarna sur le marché américain avant son introduction en bourse prévue en septembre 2025.

Données de marché

- Statistiques Chargeflow sur le BNPL pour 2026 : https://www.chargeflow.io/blog/buy-now-pay-later-statistics

Données Klarna

- Klarna sur Wikipédia (introduction en bourse prévue en 2025, nombre d'utilisateurs et de commerçants, pays, stablecoin, assistant IA) : https://en.wikipedia.org/wiki/Klarna

- Morningstar — Analyse de la valorisation de Klarna en vue de son introduction en bourse : https://www.morningstar.com/stocks/whats-behind-klarnas-14-billion-ipo-valuation

- Digital Commerce 360 — Introduction en bourse de Klarna : valorisation à 20 milliards de dollars : https://www.digitalcommerce360.com/2025/09/12/klarna-ipo-20-billion-valuation/

- PM Insights — Introduction en bourse de Klarna et partenariat avec Walmart : https://www.pminsights.com/insights/klarna-leads-triple-fintech-ipo-wave-this-week

Données Affirm

- Affirm Relations avec les investisseurs — chiffre d'affaires, rentabilité, structure tarifaire : https://investors.affirm.com/news-releases/news-release-details/affirm-difference-building-new-kind-payments-network-money-and

- Business of Apps — Parts de marché et chiffres d'affaires du BNPL : https://www.businessofapps.com/data/buy-now-pay-later-app-market/

Données comparatives

- Oreate AI — Klarna vs Affirm : valeur moyenne des commandes et nombre d'utilisateurs : https://www.oreateai.com/blog/klarna-vs-affirm-a-deep-dive-into-the-bnpl-giants/

Rétrofacturations ?

Ce n'est plus votre problème.

Récupérez 4 fois plus de rétrofacturations et prévenez jusqu’à 90 % de celles à venir, grâce à l’IA et à un réseau mondial de 20 000 commerçants.

.png)

.avif)