%201.svg)

Handleiding voor geschillen met Apple Pay: hoe u terugboekingen en transactieherroepingen kunt aanvechten

Terugboekingen?

Dat is niet langer jouw probleem.

Vorder 4 keer meer terugboekingen terug en voorkom tot 90% van de inkomende terugboekingen, dankzij AI en een wereldwijd netwerk van 20.000 handelaren.

Geschillen met betrekking tot Apple Pay doorlopen verschillende fasen voordat ze uitmonden in formele terugboekingen, te beginnen met klachten van kaarthouders en soms gevolgd door verzoeken om terugvordering. Zodra een geschil uitmondt in een terugboeking, worden er kosten in rekening gebracht en heeft dit invloed op uw ratio, ongeacht de uitkomst. Om uw verwerkingsrechten te beschermen, kosten voor geschillen te vermijden en verliezen tot een minimum te beperken, moet u gebruikmaken van waarschuwingen vóór het ontstaan van een geschil om legitieme gevallen in een vroeg stadium op te sporen en op te lossen, voordat ze escaleren tot formele terugboekingen die uw ratio schaden.

- Een geschil via Apple Pay begint bij de kaartuitgever, niet bij Apple. Handelaars hebben de meeste invloed voordat het tot een terugvordering komt.

- Er zijn twee belangrijke reactietermijnen: de opvraagtermijn (grote controle) en de termijn vóór de terugboeking (hiervoor is actie van de handelaar vereist).

- De meeste geschillen komen voort uit oorzaken die verkopers kunnen voorkomen: onduidelijke omschrijvingen op de afrekening, onherkenbare terugkerende afschrijvingen of verwarring rond het soepele afrekenproces.

- Handelaren behouden hun recht op herziening, op bewijsmateriaal gebaseerde verdediging en escalatie, zelfs nadat een geschil is ingediend.

- Zowel het aantal geschillen als het aantal terugboekingen heeft invloed op de status van een verkopersaccount, zelfs als een verkoper een geschil uiteindelijk wint.

Er is sprake van een Apple Pay-geschil wanneer een kaarthouder bezwaar maakt tegen een transactie die via Apple Pay is uitgevoerd. Meestal verloopt deze transactie via Apple Card, Apple Cash of de onderliggende kaartuitgever, aangezien Apple Pay zelf bij de meeste transacties een betaalmethode is en geen kaartuitgever.

| Stap | Wie | Actie | Typisch tijdschema |

|---|---|---|---|

| 1. Geschil ingediend | Kaarthouder | Meldt transacties via Apple Support, de Apple Card-app of de kaartuitgever | Binnen 60 tot 120 dagen na de afrekening |

| 2. Terugvordering uitgevoerd | Uitgever / Netwerk | Er is een formele terugvordering met een redencode verzonden naar de acquirer van de handelaar | 5-10 werkdagen |

| 3. Overgelegd bewijsmateriaal | Handelaar | Reageert met een afleverbewijs, kwitanties en correspondentie | 20-30 dagen |

| 4. Beoordeling | Netwerk / Uitgever van de Apple Card (Goldman Sachs/andere) | Beoordeelt bewijsmateriaal aan de hand van de criteria voor foutcodes | 7-30 dagen |

| 5. Besluit | Netwerk / Uitgever | Teruggestorte bedragen aan de handelaar of geschillen met de kaarthouder | 30-45 dagen |

Wanneer een kaarthouder bezwaar maakt tegen een Apple Pay-transactie, doen de meeste handelaren een van de volgende twee dingen: ze geven zonder nadenken een terugbetaling of ze wachten af in de hoop dat het geschil vanzelf verdwijnt. Beide reacties kosten je geld dat je niet hoefde te verliezen.

Een geschil is elke betwisting van een transactie door een kaarthouder. Elk geschil doorloopt verschillende fasen voordat het daadwerkelijk een formele terugvordering wordt. Sommige Apple Pay-geschillen monden uit in terugvorderingen omdat handelaren ze vanaf het begin als terugvorderingen behandelen. De geschillen die dat niet doen, zijn die waarbij de handelaar in de juiste fase heeft ingegrepen, wat leidt tot een snellere afhandeling, lagere kosten en een geschillenpercentage dat laag blijft.

Deze handleiding leidt u vanuit het perspectief van de handelaar door het volledige verloop van een Apple Pay-geschil, vanaf het moment dat een kaarthouder voor het eerst een transactie aanvecht tot aan de definitieve afhandeling. U komt te weten wat de aanleiding is voor Apple Pay-betalingsgeschillen, wat uw rechten als handelaar zijn en hoe u een reactiesysteem kunt opzetten waarmee u voorkomt dat geschillen onnodig escaleren.

Wat in deze gids niet uitgebreid aan bod komt, is het formele terugboekingsproces zelf: de netwerkspecifieke termijnen, het bewijsmateriaal voor herziening en de escalatieregels die van toepassing zijn zodra een geschil zo ver is gekomen. Als je je in die situatie bevindt, sluit onze gids over Apple Pay-terugboekingen naadloos aan op deze gids.

Wat is een Apple Pay-geschil?

Omdat Apple Pay bovenop het onderliggende kaartnetwerk draait, blijft de betalingsdienstaanbieder van de handelaar achter de schermen verantwoordelijk voor de daadwerkelijke afhandeling van geschillen.

Een Apple Pay-geschil is een terugvordering die wordt ingediend tegen de kaart die een klant via Apple Pay heeft gebruikt. Het gaat hier niet om een claim die door Apple wordt afgehandeld, aangezien Apple Pay in de eerste plaats een betaalmethode is en geen betalingsverwerker. Zodra een transactie is voltooid, wordt een eventueel geschil ingediend tegen de onderliggende kaart van de klant en volledig afgehandeld door diens bank en kaartnetwerk.

Wat geschillen rond Apple Pay voor handelaren zo bijzonder maakt, is de verschuiving van de aansprakelijkheid. Omdat Apple Pay biometrische authenticatie vereist, verschuift de aansprakelijkheid voor fraude doorgaans van u af zodra die authenticatie plaatsvindt. Geschillen die geen verband houden met fraude (niet-geleverde goederen, misleidende informatie en niet-verwerkte terugbetalingen) vallen echter niet onder deze regeling. Die worden op dezelfde manier afgehandeld als elke andere terugvordering.

Apple Pay-geschil versus Apple Pay-terugboeking, en waarom dit verschil belangrijk is voor handelaren

Een Apple Pay-geschil en een terugvordering zijn niet hetzelfde voorval met verschillende ernstgraden. Het zijn veeleer twee verschillende situaties voor een handelaar: de ene waarbij je zelf de regie hebt, en de andere waarbij je moet vechten om die regie terug te krijgen.

Er ontstaat een geschil wanneer een kaarthouder contact opneemt met zijn bank om een transactie te betwisten. Wat dat in de praktijk voor jou betekent, is dat er nog niets is beslist. Ook al loopt er een zaak tegen je, er is nog geen geld overgemaakt. Er is je nog niets in rekening gebracht. Het geschil is een signaal. En in dit stadium kun je er op jouw voorwaarden op reageren. Zo ziet ‘high agency’ er in dit proces uit. Geen wettelijk recht, geen formeel beroep, gewoon een open venster.

Maar de meeste handelaars beseffen dit niet; ze weten niet hoeveel vensters er nog over zijn voordat die optie verdwijnt.

Er zijn twee vensters:

Venster 1: Opvraagverzoek (hoog beheer)

Over het algemeen vraagt de uitgevende bank om transactiegegevens voordat er een geschil wordt ingediend over transacties waarbij de kaart niet fysiek aanwezig is. Door op dergelijke verzoeken te reageren met de relevante documentatie, kunt u het geschil op uw eigen voorwaarden oplossen.

Venster 2: Venster vóór terugboeking (hoge bemiddelingsgraad vereist)

De tweede is een waarschuwing vóór een chargeback, een signaal van netwerken zoals Verifi of Ethoca dat er op korte termijn een chargeback-aanvraag zal worden ingediend. Door hier snel op te reageren, kun je het geschil nog net op tijd afwenden. Je kunt het programma zelfs zo instellen dat er automatisch een terugbetaling wordt uitgevoerd en dat er waarschuwingen van beide netwerken worden verzonden.

Na deze twee fasen volgt de formele terugvordering, en vanaf dat moment wordt de tijdspanne steeds korter. En in sommige gevallen valt de deur zelfs met een klap dicht.

Je reageert niet langer op een betwisting. Je dient een herzieningsverzoek in dat wordt behandeld door de eigen bank van de klant, waarbij al kosten in rekening zijn gebracht en er al een aantekening is toegevoegd aan je geschillenratio, ongeacht of je wint of verliest.

Dat laatste detail is juist hetgeen dat onopgemerkt een steeds grotere rol gaat spelen. En het is de maatstaf die kaartnetwerken hanteren om te bepalen of je überhaupt nog betalingen mag verwerken.

Kan ik een Apple Pay-transactie bij mijn bank betwisten?

Veel gebruikers stellen deze vraag wanneer ze te maken krijgen met een transactieprobleem dat moet worden opgelost. Dit is wat u moet weten over de aanleiding voor geschillen bij Apple Pay: niet alle geschillen ontstaan om dezelfde reden, en door ze wel als zodanig te behandelen, verliezen handelaren zaken die ze zouden kunnen winnen en verspillen ze middelen aan zaken die ze zouden kunnen winnen.

Redenen waarom klanten geschillen over Apple Pay indienen

Het vroegtijdig onderscheiden van opzettelijke fraude en geschillen die voortkomen uit wrijving is precies waarvoor een bredere strategie ter voorkoming van e-commercefraude is bedoeld.

De redenen waarom klanten geschillen indienen met betrekking tot Apple Pay vallen uiteen in drie categorieën, die elk iets anders zeggen over uw risico en die elk een andere reactie vereisen.

Geschillen die je waarschijnlijk zelf hebt veroorzaakt

Dit zijn de meest voor de hand liggende en best te voorkomen gevallen. Een klant kreeg een verkeerd bedrag in rekening gebracht. Er werd een terugbetaling verwerkt, maar deze werd nooit bijgeschreven. Een bestelling is nooit aangekomen, of er is een verkeerde bestelling geleverd. Een factureringsomschrijving op het afschrift kwam de klant onbekend voor, en hij heeft bezwaar gemaakt zonder eerst nader onderzoek te doen. Geen van deze voorbeelden is specifiek voor Apple Pay; het zijn standaardfouten bij de afhandeling en facturering. Ze komen bij elke betaalmethode voor.

Wat Apple wellicht zou kunnen veranderen, is de snelheid waarmee dergelijke zaken worden geëscaleerd. De Wallet-app geeft transactiegegevens direct en duidelijk weer, waardoor klanten afwijkingen sneller opmerken dan wanneer ze aan het einde van de maand een papieren afschrift zouden doornemen.

Geschillen die zijn ontstaan door het soepele betaalproces van Apple Pay

Bij de meeste Apple Pay-transacties verloopt de geschillenafhandeling via de bank die de kaart in de Wallet van de klant heeft uitgegeven. De geschillenprocedure van de bank is al klantvriendelijk en eenvoudig. Betalingen met Apple Cards maken dat nog gemakkelijker.

De Apple Card wordt uitgegeven door Goldman Sachs en volledig beheerd binnen de Wallet-app. Hiermee kunnen kaarthouders met een paar tikken bezwaar maken tegen een afschrijving. Geen telefoontjes, geen formulieren, je hoeft het platform niet te verlaten. Zodra een bezwaar is bevestigd, ontvangen ze een voorlopige creditering. Dit soepele proces verlaagt de drempel om een bezwaar in te dienen. Bezwaren die bij een bank wellicht halverwege het proces zouden zijn afgeblazen, worden hier wel ingediend.

Het delen binnen het gezin maakt dit nog erger. Aankopen die door het ene gezinslid zijn gedaan, kunnen voor een ander gezinslid onherkenbaar zijn, en de procedure voor het indienen van een geschil is dezelfde reeks tikken. Apple raadt kaarthouders aan om eerst de activiteit op het gedeelde account te controleren. Maar de menselijke aard zorgt ervoor dat die stap vaak wordt overgeslagen.

Opzettelijke geschillen

De derde categorie oorzaken van geschillen bij Apple Pay is fraude door terugboekingen. Biometrische authenticatie maakt het voor een klant daadwerkelijk moeilijk om te beweren dat een Apple Pay-transactie niet geautoriseerd was. Het authenticatierecord is apparaatspecifiek en gekoppeld aan het moment van aankoop. Hierdoor verschuift de aansprakelijkheid voor fraude naar de uitgevende bank wanneer de transactie op de juiste wijze is verwerkt. Voor geschillen die als fraude worden aangemerkt, biedt dit een belangrijke bescherming.

Maar fraudeurs die via chargebacks misbruik maken van Apple Pay, gebruiken zelden fraudecodes. Een klant die de goederen bewust heeft ontvangen en de afschrijving wil betwisten, beweert niet dat de transactie ongeautoriseerd was. Ze weten dat dit een kansloze argumentatie is tegen een biometrisch profiel. In plaats daarvan voeren ze niet-frauduleuze redencodes aan: artikel niet ontvangen, artikel niet zoals beschreven, dienst niet geleverd. Authenticatie speelt bij deze geschillen geen rol. De beslissing wordt volledig gebaseerd op bewijs van levering, dus de biometrische gegevens die je tegen een fraudeclaim zouden hebben beschermd, helpen hier niets.

Rechten van handelaren bij een geschil over Apple Pay

De meeste handelaren beschouwen een kennisgeving van een chargeback als een definitief oordeel. Dat is het echter niet. De regels van de kaartnetwerken geven u het recht om bezwaar te maken, de zaak door te verwijzen en – als u de kneepjes van het vak kent – de beslissing ongedaan te maken. Het maakt een wereld van verschil als u begrijpt waar die rechten beginnen en waar ze eindigen.

Het recht op herziening

Wanneer er een terugvordering wordt ingediend, bent u niet verplicht deze te accepteren. Elk groot kaartnetwerk kent handelaren het recht op 'representment' toe: de formele procedure waarbij bewijsmateriaal wordt ingediend om een betwiste transactie aan te vechten. U stelt uw dossier samen, dient dit binnen de door het netwerk gestelde termijn in via uw acquirerende bank, waarna de uitgevende bank het beoordeelt. Als uw bewijs overtuigend is en uw indiening tijdig plaatsvindt, kan de chargeback worden teruggedraaid en het geld worden terugbetaald. Handelaren die effectief gebruikmaken van chargeback-representment, herwinnen zo inkomsten die anders als verlies zouden worden afgeschreven.

Het gemiddelde succespercentage van handelaren bij herzieningsprocedures ligt rond de 20. Dat cijfer stijgt aanzienlijk dankzij goed geordend bewijsmateriaal en redencode-specifieke documentatie die je krijgt via automatisering van terugvorderingen. Het daalt tot nul voor handelaren die de deadline missen, die – afhankelijk van het netwerk – al na 20 tot 30 dagen na de kennisgeving kan verstrijken.

Het recht op een op bewijs gebaseerde verdediging

Als onderdeel van het chargeback-proces hebt u recht op de redencode die aan het geschil is toegekend; de specifieke categorie die de uitgever heeft gebruikt om de claim van de kaarthouder in te delen. Die chargeback-redencode bepaalt welk bewijsmateriaal relevant is, waar de uitgever naar op zoek is en hoe uw bewijsmateriaalpakket moet worden samengesteld. Een geschil met een fraudecode vereist andere documentatie dan een claim wegens niet-ontvangst. Het afstemmen van uw bewijsmateriaal op de redencode is geen optie, aangezien verkeerd samengestelde bewijsdossiers worden afgewezen, zelfs wanneer de onderliggende feiten in het voordeel van de handelaar spreken.

Met name voor Apple Pay-transacties is het bewijs van biometrische authenticatie beschikbaar via de infrastructuur van het kaartnetwerk. U hebt geen rechtstreekse toegang tot de systemen van Apple; deze gegevens worden via het kaartnetwerk doorgegeven en kunnen worden opgenomen in uw herzieningsdossier. Zoals eerder aangegeven, vormt dit uw sterkste bewijsmiddel bij geschillen met een fraudecode.

Rechten inzake aansprakelijkheidsverschuiving

De tokenisatie en biometrische authenticatie van Apple Pay zorgen bij de meeste correct verwerkte contactloze transacties voor een verschuiving van de aansprakelijkheid bij fraude. Dit betekent dat als er een terugvordering wegens fraude wordt ingediend voor een transactie die correct is geauthenticeerd, de uitgever – en niet de handelaar – de financiële verantwoordelijkheid draagt. Visa heeft biometrie expliciet erkend als de veiligste beschikbare authenticatiemethode, en Apple Pay-transacties die aan de authenticatie-eisen voldoen, komen doorgaans in aanmerking voor deze bescherming.

Het recht om de zaak naar een hoger niveau te tillen

Als uw bezwaar wordt afgewezen en u van mening bent dat de uitspraak onterecht is, hebt u het recht om de zaak verder aan te vechten. De pre-arbitrageprocedure is de volgende stap; een tweede kans om het geschil aan te vechten voordat het voor definitieve beslechting bij het kaartnetwerk terechtkomt. Als de zaak in de pre-arbitrageprocedure niet kan worden opgelost, volgt de arbitrageprocedure, waarbij het kaartnetwerk als hoogste instantie optreedt en een bindende uitspraak doet.

Arbitrage is een recht, maar er gelden wel aanzienlijke beperkingen. De verliezende partij betaalt arbitragekosten bovenop het transactiebedrag dat al op het spel staat. Escalatie is financieel alleen zinvol bij geschillen met een hoge waarde, ondersteund door overtuigend bewijs dat in overeenstemming is met de redencode, waarbij de potentiële opbrengst duidelijk opweegt tegen de kosten van een nederlaag.

Wat je niet mag doen

Handelaren kunnen Apple Pay niet selectief blokkeren als betaalmethode voor individuele kaarthouders. Aangezien Apple Pay via een onderliggend kaartnetwerk wordt verwerkt, bestaat er geen mechanisme om de Apple Pay-transacties van een specifieke kaarthouder te identificeren en te blokkeren. Om specifiek de Apple Card te blokkeren, zouden alle Mastercard-transacties moeten worden geblokkeerd, wat operationeel niet haalbaar is en bovendien volgens de meeste handelsovereenkomsten niet is toegestaan.

De regels van kaartnetwerken verbieden handelaren ook om klanten extra kosten in rekening te brengen voor het betalen met een bepaalde methode, of om sancties op te leggen aan klanten die een geschil indienen. Wat handelaren wel mogen doen, en wat buiten deze verboden valt, is het gebruik van tools zoals Chargeflow om kaarthouders te blokkeren die ongefundeerde geschillen indienen, en om zelf beslissingen te nemen over toekomstige dienstverlening. Dat is een zakelijke beslissing, geen overtreding van de netwerkregels. Het verschil zit hem in het beheer van uw eigen klantrelaties enerzijds en het gebruik van het accepteren van betalingen als wapen tegen iemand die gebruik heeft gemaakt van een recht dat het kaartnetwerk expliciet toekent, anderzijds.

Hoe reageer je in 6 stappen op een geschil via Apple Pay?

Het onderstaande chronologische reactieprotocol is afgestemd op de specifieke werkwijze van Apple Pay-transacties en de termijnen die het snelst verstrijken, zodat u geschillen effectief kunt afhandelen.

Stap 1: Handel binnen het waarschuwingsvenster

Als er een waarschuwing vóór een chargeback is binnengekomen, bedraagt de termijn om actie te ondernemen voordat het geschil officieel wordt vastgelegd 24 tot 72 uur. Een terugbetaling die binnen die termijn wordt uitgevoerd, beperkt het verlies tot de transactiewaarde, zonder chargeback-kosten, zonder verlies op basis van een percentage en zonder herverwerkingscyclus. De waarschuwingsintegratie Chargeflow koppelt inkomende waarschuwingen aan de DAN-geïndexeerde transactie en verwerkt de terugbetaling automatisch binnen die termijn.

De rest van het protocol heeft betrekking op zaken die u wilt vertegenwoordigen.

Stap 2: Identificeer de transactie

Apple Pay-transacties worden in de administratie van de handelaar weergegeven onder een Device Account Number (DAN), niet onder het daadwerkelijke kaartnummer van de kaarthouder. Wanneer er een melding van een geschil binnenkomt, moet deze aan de hand van dat DAN worden gekoppeld aan de oorspronkelijke verkoop. Deze koppeling zet de rest in gang: het opvragen van bewijsmateriaal, uw beslissing over de eerste beoordeling en de reactie op het geschil. Een tool zoals Chargeflow haalt de getokeniseerde transactiegegevens na ontvangst van het geschil naadloos op. Het koppelt deze automatisch aan de oorspronkelijke bestelling in uw betalingsverwerker, OMS en CRM, zodat de zaak al geïdentificeerd en ingevuld is voordat iemand van uw team ermee aan de slag gaat.

Stap 3: Bevestig het authenticatierecord

Controleer of er op het moment van aankoop biometrische authenticatie of authenticatie via een toegangscode heeft plaatsgevonden. Bij geschillen over fraude vormt dit gegevensrecord de basis voor de aansprakelijkheidsverschuiving. Bij codes die geen verband houden met fraude is dit minder relevant voor de uitkomst, maar het geeft wel aan met welke geschilcategorie je te maken hebt, wat bepalend is voor het bewijsmateriaal dat je vervolgens nodig hebt.

Stap 4: Verzendgegevens ophalen

Verzamel de gegevens die de redencode vereist: trackinggegevens van de vervoerder en een leveringsbevestiging voor fysieke goederen, toegangs- of gebruikslogboeken voor digitale producten, en indien van toepassing servicegegevens. Het bewijspakket moet aansluiten bij de redencode; het volstaat niet om alleen aan te tonen dat de transactie in het algemeen legitiem was. Chargeflow dit pakket automatisch Chargeflow . Het haalt tegelijkertijd gegevens op uit verzendintegraties, CRM-communicatie en toegangslogboeken, en structureert deze op basis van de redencode en netwerkspecifieke vereisten voordat het wordt ingediend.

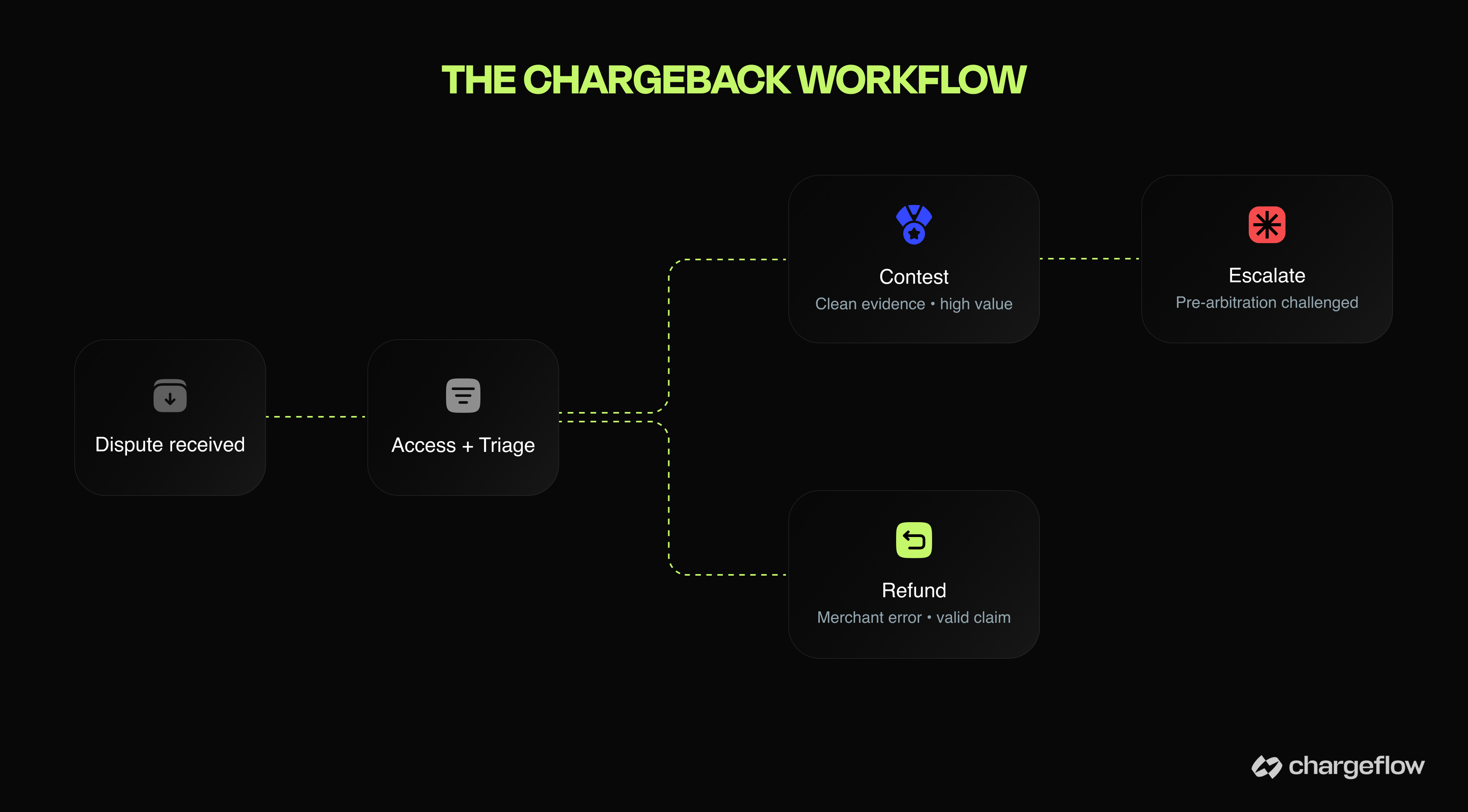

Stap 5: Triage

Nu de transactie is geïdentificeerd en het bewijsmateriaal is verzameld, gaat het niet meer om de vraag of het geschil te winnen is. Het gaat erom of het financieel gezien de juiste beslissing is om het geschil aan te vechten. Een geschil dat als fraude is aangemerkt, met duidelijke authenticatie en een bevestigde levering, is het waard om aan te vechten. Een claim wegens niet-levering waarbij uit de tracking blijkt dat het artikel nog onderweg is, is een fout van de verkoper; los dit op.

Een geschil waarbij de klant het product wel heeft ontvangen en toch een klacht heeft ingediend, zonder dat er sprake is van wezenlijke hiaten in het bewijsmateriaal, kan goedkoper zijn om af te wikkelen dan om te betwisten. Chargeflow de kans op winst op basis van de redencode, het netwerk en de kwaliteit van het bewijsmateriaal. Het systeem geeft aan welke zaken een heroverweging rechtvaardigen en leidt de overige zaken naar een oplossing, voordat ze reactietijd en ruimte in de ratio opslokken.

Stap 6: Bewaar alles

Elk authenticatierapport, elk afhandelingsdocument, elke communicatie met de klant en elke triagebeslissing die vanaf stap één wordt genomen, moet vanaf het moment dat het geschil wordt gemeld worden bewaard en geordend. Chargeflow bewijsmateriaal met betrekking tot geschillen Chargeflow om een volledig, gestructureerd dossier bij te houden dat in elke fase beschikbaar is voor escalatie, zonder dat het opnieuw hoeft te worden samengesteld.

Welke invloed hebben geschillen over Apple Pay op uw verkopersaccount?

Elk Apple Pay-geschil dat je ontvangt – of je het nu betwist, het bedrag terugbetaalt of het negeert – wordt ergens geregistreerd. Waar het terechtkomt en hoe het wordt meegeteld, bepaalt of je je verkopersaccount mag behouden.

Twee ratio’s, één bedrijf in gevaar

De meeste handelaren houden hun chargeback-percentage bij. Minder handelaren houden hun percentage geschillen bij. Onder het vernieuwde toezichtskader van Visa komt die achterstand hen nu duur te staan.

Visa heeft zijn afzonderlijke programma’s voor het monitoren van fraude en geschillen (het VFMP en het VDMP) samengevoegd tot één enkel kader: het Visa Acquirer Monitoring Program, oftewel VAMP. De belangrijkste verandering is niet louter administratief van aard. VAMP heeft een nieuwe gecombineerde ratio geïntroduceerd die zowel TC40-fraudemeldingen als TC15-geschillen die geen fraude betreffen, meet aan de hand van één enkele drempelwaarde. Een transactie die zowel een fraudemelding als een formeel geschil oplevert, kan in de ratio van dezelfde maand twee keer worden meegeteld. Voorheen kon een handelaar de blootstelling aan fraude en geschillen afzonderlijk beheren. Onder VAMP versterken deze elkaar.

De handhavingsdrempels geven aan hoe serieus Visa dit neemt. Toen de handhaving in oktober 2025 van start ging, werden handelaren bij een VAMP-ratio van 2,2% aangemerkt als „Excessive“. Die drempel is nu gedaald naar 1,5%. Het praktische streefcijfer, rekening houdend met het mechanisme van dubbeltelling, ligt ruim onder de 1%. Handelsbedrijven in de categorie ‘Excessive’ krijgen boetes van 8 tot 10 dollar per geschil, die maandelijks worden opgelegd totdat de ratio weer op peil is. Om uit deze categorie te komen, moet de ratio drie opeenvolgende maanden onder de drempel blijven.

Het Excessive Chargeback Program van Mastercard functioneert afzonderlijk en houdt het percentage chargebacks bij ten opzichte van het transactievolume. De ECM-drempel ligt op 1,5% bij 100 of meer chargebacks per maand. Aan beide voorwaarden moet worden voldaan. Het HECM-niveau treedt in werking bij 3,0% bij 300 of meer chargebacks. De boetes lopen elke maand op zolang een handelaar boven de drempel blijft.

Welke invloed hebben geschillen op je ratio die niet door een overwinning teniet wordt gedaan?

Een ingediende chargeback telt mee voor uw ratio. Een chargeback die u vervolgens via een herzieningsprocedure wint, wordt niet van uw ratio afgetrokken. De ratio meet het aantal ingediende claims, niet de uitkomsten. Dit is de rekensom die ervoor zorgt dat ingrijpen in de geschillenfase – voordat een formele chargeback wordt ingediend – financieel gezien verschilt van een herzieningsprocedure in de chargeback-fase. Geschillen die worden opgelost via instrumenten voor geschillenpreventie, zoals Chargeflow , voordat een TC15 wordt gegenereerd, worden niet meegeteld in de VAMP-telling. Die uitsluiting geldt niet voor geschillen die al het stadium van een formele terugvordering hebben bereikt.

Onbetwiste terugboekingen maken dit nog erger. Elke terugboeking die zonder reactie wordt geaccepteerd, is een registratie die nooit wordt aangevochten. En elke terugboeking blijft permanent in de ratio meewegen, ongeacht of de onderliggende claim terecht was.

De verborgen kosten die niet in de verhouding tot uiting komen

De beoordeling door de betalingsverwerker en de beëindiging van de rekening zijn de zichtbare eindpunten van een ratio-probleem. De kosten in de aanloop daarnaartoe zijn minder zichtbaar. Aan elke chargeback zijn kosten verbonden, doorgaans $15 tot $30 per incident, afhankelijk van de betalingsverwerker. Deze kosten worden in rekening gebracht, ongeacht de uitkomst. De tijd die medewerkers besteden aan het verzamelen van bewijsmateriaal, het opstellen van een tegenvordering en het beheren van deadlines wordt nergens meegeteld, maar legt wel een druk op de operationele capaciteit.

Acquirers houden toezicht op de prestaties van handelaren op het gebied van geschillenafhandeling als voorwaarde voor de verwerkingsrelatie; handelaren met hoge percentages krijgen te maken met hogere verwerkingskosten, verplichte reserves of contractuele beperkingen nog voordat ze in een formeel toezichtsprogramma terechtkomen.

Laatste overwegingen en directe actiepunten

Het is ook interessant om te volgen hoe de aansprakelijkheid voor terugboekingen door AI-agenten zich ontwikkelt, aangezien steeds meer Apple Pay-aankopen worden geïnitieerd door een geautomatiseerde agent in plaats van door de kaarthouder zelf.

Apple Pay zou naar verluidt 9,5 biljoen transacties verwerken voor meer dan 800 miljoen klanten. Naarmate het aandeel van Apple Pay in het transactievolume van een handelaar toeneemt, stijgt ook het aantal transacties waarover geschillen ontstaan.

De aansprakelijkheidsverschuiving biedt handelaren bescherming bij Apple Pay-geschillen die als fraude zijn aangemerkt, mits de authenticatie correct is verlopen. Deze regeling biedt geen bescherming tegen geschillen die geen fraude betreffen; deze kunnen onder VAMP nu meetellen voor dezelfde verhouding als fraudemeldingen.

Om duurzaam te blijven, moet je geschillen beschouwen als een levenscyclus die je in een vroeg stadium moet beheersen, en niet als een uitkomst waartegen je achteraf moet vechten.

Dat betekent dat het voorkomen van geschillen voorop moet staan:

- Los problemen van klanten op voordat er überhaupt een TC15 wordt aangemaakt.

- Gebruik geschillenwaarschuwingen om zaken binnen het tijdsbestek van 24–72 uur op te vangen.

- Zorg voor meer consistentie in de afhandeling, de factureringsbeschrijvingen en de communicatie met klanten, zodat er überhaupt minder geschillen ontstaan.

De verkopers die onder de controledrempels blijven, hebben deze aanpak onder de knie: zo vroeg mogelijk ingrijpen, zo snel mogelijk oplossen en het aantal geschillen dat het netwerk bereikt tot een minimum beperken.

Ontdek hoe Chargeflow je Chargeflow helpen om dat allemaal volledig automatisch te realiseren.

Veelgestelde vragen

Hoe kan ik bezwaar maken tegen een Apple Pay-transactie?

Je kunt een Apple Pay-transactie betwisten via Apple Support als het om Apple Card of Apple Cash gaat, of via de uitgever van je kaart als Apple Pay met een andere kaart is gebruikt.

Regelt Apple terugboekingen voor verkopers?

Apple verwerkt voor de meeste Apple Pay-transacties geen terugvorderingen aan de kant van de handelaar; het geschil wordt afgehandeld door de uitgevende bank van de kaarthouder volgens de standaardnetwerkregels, met uitzondering van Apple Card en Apple Cash, die rechtstreeks door de bankpartners van Apple worden beheerd.

Kan een handelaar een geschil over Apple Pay winnen?

Ja – handelaren die overtuigend bewijs kunnen leveren, zoals een afleverbewijs, ondertekende ontvangstbewijzen en transactiegegevens die overeenkomen met de reden voor het geschil, kunnen een Apple Pay-geschil met succes aanvechten.

Kunnen Apple Pay-betalingen worden teruggedraaid?

Ja, maar alleen via de geschillenprocedure van de kaartuitgever, niet rechtstreeks via Apple. Zodra een geschil uitmondt in een terugboeking, verloopt de terugboeking volgens de standaardregels van het kaartnetwerk.

Automatiseer uw reactie op geschillen via Apple Pay

U kunt het verzamelen en indienen van bewijsmateriaal bij elk Apple Pay-geschil automatiseren, in plaats van dit handmatig te doen. Chargeflow altijd op tijd Chargeflow , met een garantie op een viervoudig rendement op uw investering.

Gratis beginnenTerugboekingen?

Dat is niet langer jouw probleem.

Vorder 4 keer meer terugboekingen terug en voorkom tot 90% van de inkomende terugboekingen, dankzij AI en een wereldwijd netwerk van 20.000 handelaren.

.png)

.avif)