%201.svg)

Shopify Disputes: Resolution, Chargebacks, and Response

Terugboekingen?

Dat is niet langer jouw probleem.

Vorder 4 keer meer terugboekingen terug en voorkom tot 90% van de inkomende terugboekingen, dankzij AI en een wereldwijd netwerk van 20.000 handelaren.

A Shopify dispute is any case where a customer asks their bank to review a charge. It can be an inquiry (no funds moved yet) or a chargeback (funds reversed immediately with a fee). Shopify doesn’t decide outcomes; the issuing bank does. You typically have 7–21 days to respond with evidence tied to the reason code. Winning returns your funds; losing means permanent loss. High dispute rates can trigger card network monitoring programs. The key is speed, strong evidence, and prevention, because not every dispute is worth fighting, but every one affects your risk profile.

A Shopify dispute (Shopify's term for a chargeback) happens when a customer contests a charge with their bank rather than requesting a refund through the merchant, triggering Shopify Payments' built-in chargeback workflow and a compressed evidence-submission window.

| Stap | Wie | Actie | Typisch tijdschema |

|---|---|---|---|

| 1. Geschil ingediend | Klant | Contests charge with card issuer instead of merchant | Within 60-120 days of transaction |

| 2. Kennisgeving | Shopify | Notifies merchant via Shopify admin with reason code | 1-3 werkdagen |

| 3. Overgelegd bewijsmateriaal | Handelaar | Uploads evidence directly in Shopify admin | Typically 7-11 days |

| 4. Besluit | Card network / Issuer | Funds returned to merchant or dispute stands with customer | 30-45 dagen |

In Shopify, specifically with Shopify Payments, a dispute is the umbrella term used for when a customer contacts their bank or card issuer to question a transaction. Shopify disputes come in two forms: an inquiry, a request for more information with no funds moved yet, or a chargeback, where the bank immediately reverses the funds and charges a fee.

Shopify does not decide the outcome. The card issuer does, based on the evidence you submit.

Every Shopify chargeback is a dispute, but not every dispute becomes a chargeback. Shopify tracks all of them in your admin, and your overall dispute rate includes every case, regardless of outcome. Keeping that rate matters. Too many disputes can trigger fraud and chargeback monitoring programs by Visa and Mastercard, which can put your ability to process payments at risk.

This guide covers everything you need to know about Shopify disputes: how to respond, how to fight chargebacks, and how to protect your store.

What Is a Shopify Dispute?

A Shopify dispute is the official term that Shopify uses for any situation where a customer contacts their bank or credit card issuer to attempt to reverse a charge made on their card. When this happens, the customer’s bank reviews the transaction and responds by creating a chargeback or opening an inquiry.

Shopify groups both inquiry and chargeback under the single identifier “dispute” in your admin, reports, notifications, and API.

Shopify Disputes vs. Chargebacks: Key Differences

In practice, a dispute is not the same as a chargeback, and confusing the two can be costly.

A dispute is an early-stage alert that a customer has questioned a transaction, either through their bank or within Shopify Payments. It often starts as an inquiry. At this stage, the case remains open, and in some scenarios, funds have not yet been withdrawn, giving you a window to resolve the issue before it escalates.

A Shopify chargeback, by contrast, is a formal reversal initiated by the issuing bank. It can occur after an unresolved dispute or without any prior warning.

Key Differences between Shopify Disputes and Chargebacks

Here's how Shopify officially distinguishes between Shopify disputes and Shopify chargebacks:

| Aspect | Terugboeking | Dispute (Inquiry) |

|---|---|---|

| Wat het is | The bank immediately reverses the payment (a full or partial reversal). | The bank investigates the customer's claim but does not reverse funds yet. |

| Impact on your funds | The disputed amount and Shopify's chargeback fee are withdrawn from your Shopify Balance/payouts right away. | No money is taken immediately. |

| If you win | Funds and the dispute fee are returned to you. | No action needed; inquiry closes with no financial impact. |

| If you lose | You permanently lose the funds and the fee. | Inquiry can turn into a full chargeback (funds and fees then deducted). |

| Response process | You get a notification with a deadline to submit evidence. Shopify forwards it to the card network/issuer for a final decision. | Same evidence submission process, but lower immediate pressure. |

| Common reasons | Fraud, non-delivery, defective item, duplicate charge, etc. (same as inquiries). | Same reasons, but often treated as a preliminary step. |

How to Dispute a Charge on Shopify

As a merchant, you don’t control how a dispute starts. The cardholder does. Here’s what that process looks like from their side.

When a customer sees a charge they don’t recognize or disagree with, they have two options:

1) Contact you directly,

2) Go straight to their bank.

Most go to their bank through an app or other channels. From there, the bank takes over. They log the claim, assign a chargeback reason code, and decide whether to issue an inquiry or immediately escalate to a chargeback, often without notifying you until the decision is already made.

The reason code the bank assigns matters. It determines what evidence you’ll need to submit to counter it, and how much leverage you actually have.

By the time the dispute reports in your dashboard, the clock is already running. The response stage is critical. You’re responding to a bank-mediated process with a hard deadline and no room for back-and-forth.

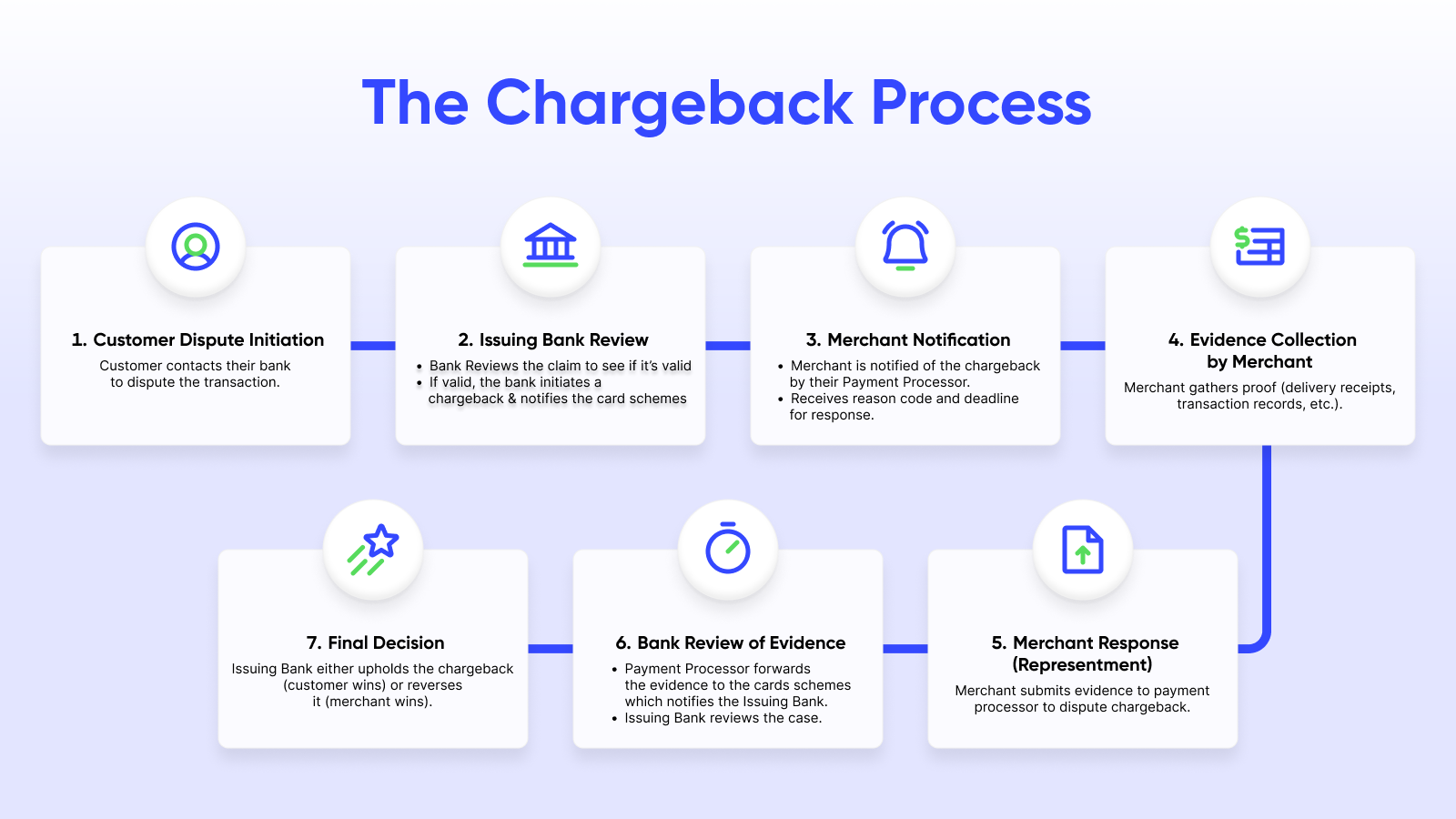

The Shopify Chargeback Dispute Process

When a dispute appears in your Shopify admin, you typically have 7 to 21 days to respond. How you use that window decides whether you recover the funds or lose them permanently.

If the dispute appears to be a misunderstanding (such as a charge the customer didn't recognize, a delivery they missed, or a return that fell through the cracks), contact them directly before building your evidence. A resolved dispute is better than a won one. If they agree to drop the claim, ask them to request a withdrawal letter from their bank and send it to you.

Submit that as your evidence; it's the cleanest possible outcome.

This may not work in every case. Skip it for clear payment fraud claims or customers who have already escalated aggressively.

Step 1: Locate the Dispute

From your Shopify admin, go to Orders, then click Search and filter > Add filter > Chargeback and inquiry status > Open.

Check this filter daily. Missed deadlines cannot be recovered.

Step 2: Analyze the Issuer’s Claim

Open the order and read the issuer claim and reason code carefully.

Your evidence must directly counter the exact reason. For instance:

- Fraud requires evidence that proves authorization (AVS/CVV match, IP logs, etc.)

- Product not received needs proof of delivery and tracking documentation.

- Duplicate charge demands evidence that shows the cardholder’s billing records.

Generic uploads are automatically rejected. Using an AI-assisted chargeback dispute platform produces better results because the evidence is tailored to the claim.

Step 3: Decide Whether to Fight

Quick gut check:

- Do you have strong, specific evidence?

- Is the order value worth the time?

- Is the claim truly defensible?

Not every dispute needs to be contested. This win-lose probability analysis is built into an automated, Shopify-native platform like Chargeflow.

Step 4: Build a Structured Evidence Package

Click Add evidence (opens the Chargeback response page). Create a clear, concise case:

- Short written explanation (your narrative).

- Targeted supporting documents.

- Everything aligned with the reason code.

You can save progress and return later. Clarity beats volume. For a full breakdown of what to submit and how to structure it, see Shopify Dispute Forms, Evidence, and Response Deadlines below.

Step 5: Submit Early

When ready, click Submit now. Shopify will auto-submit whatever you’ve saved on the deadline, but submitting early gives you control and reduces risk.

Step 6: Wait for the Issuer’s Decision

After submission, the bank reviews your evidence. This can take up to 75 days. You’ll see the status change to “Submitted,” then “Won,” “Lost,” or “Under review.”

Final Outcome

- Win: Disputed amount and chargeback fee returned to you (fee refund depends on your region).

- Loss: Funds stay with the customer.

Shopify Dispute Forms, Evidence, and Response Deadlines

You’ve carefully scrutinized the reason code and decided to fight. Now it’s time to build a submission the bank can’t ignore. Here’s exactly what Shopify accepts, how to structure it, and how much time you have.

The Chargeback Response Form

Shopify’s redesigned dispute evidence form puts the most important fields front and center. It provides you with full transparency by showing the exact PDF document that Shopify will generate and submit to the bank. You can preview the submission before it goes out, and what the bank receives is exactly what you see in the preview.

File Requirements

Shopify enforces strict formatting rules. Banks often receive evidence through fax machines, so legibility is non-negotiable:

- Accepted formats: PDF, JPEG, or PNG only.

- Maximum weight per file: 2 MB.

- Maximum evidence weight combined: 4 MB.

- PDFs must be PDF/A compliant and under 50 pages.

- No audio, video, or external links.

Submit a maximum of one file per evidence type, combining multiple files of the same type into a single file where necessary. Images should be high-contrast and printable in black and white.

How to Structure Your Evidence

Lead with your strongest proof and work down. Every document must directly address the specific reason code; anything generic weakens the package:

- Direct proof: Delivery confirmation, tracking, signature records, usage logs.

- Customer acknowledgment: Emails or messages confirming receipt, prior purchases, or transaction awareness.

- Policy documentation: Terms of service or refund policy that the customer agreed to at checkout.

- Supporting context: AVS/CVV match results, IP address logs, and order history with the same customer.

Deadlines

The due date varies from 7 to 21 days after the chargeback or inquiry is filed. If no specific time is displayed, the deadline is 11:59 PM on the date shown in your store’s timezone.

Two things worth knowing about timing:

- After you click Submit now to submit your response early, you can't make any further edits to your evidence. Don't submit early unless your package is complete.

- If you don't submit manually, Shopify automatically collects evidence and sends it to the card network on the due date. Always submit manually.

Shopify Payment Dispute Resolution

When you process payments through Shopify Payments, the entire dispute lifecycle is managed inside your Shopify admin.

Shopify automatically compiles available order data, if you don’t add your own evidence, and will submit that to the card issuer on the response due date.

However, this default submission is often minimal. Merchants who actively build and submit structured evidence typically see better outcomes.

Shopify acts as the acquiring processor. It debits the disputed amount and fee from your balance, forwards your response (as we’ve discussed before), and returns the recovered fee if you win.

A Word on Shopify Protect

US-based merchants using Shopify Payments with Shop Pay may qualify for Shopify Protect.

When an eligible order is marked “Protected,” the following holds:

- Shopify automatically assumes liability for fraudulent and unrecognised chargebacks.

- You are immediately reimbursed the full order amount and chargeback fee.

- No evidence submission is required; Shopify handles the entire dispute.

Key Limitations

Protection applies only to orders that contain exclusively physical goods fulfilled within 7 days using supported tracking. It does not cover standard checkout, third-party gateways, digital goods, or non-fraud disputes (such as “item not received,” “not as described,” or chargeback fraud).

This leaves merchants fully exposed to the majority of disputes that actually impact their bottom line. And that’s why many stores supplement Shopify Protect with dedicated chargeback automation tools that work on all dispute types.

PayPal vs. Shopify Dispute Management

Shopify Payments and PayPal offer two distinct approaches to payment processing. However, in times of disputes, the architecture for each system delivers a fundamentally different experience. Shopify Payments acts as a direct pipeline to the card network, routing disputes straight to the issuing bank. PayPal sits between you and the bank as an intermediary with its own Resolution Center, distinct rules, and in many cases, its own verdict.

How Disputes Are Filed and Tracked

With Shopify Payments, disputes appear automatically in your admin dashboard. There is no separate platform to monitor. Everything is centralized from the moment a case is filed.

PayPal operates its own dispute ecosystem through the Resolution Center. When a buyer opens a dispute, PayPal places a hold on the transaction funds while both parties work toward a resolution. If they can’t reach an agreement, the buyer can escalate to a claim. At this point, PayPal investigates and frequently makes the final ruling, depending on how the transaction was funded. If the case escalates further to a card network chargeback, the issuing bank takes over and makes the final ruling.

Indiening van bewijsmateriaal

Shopify formats your uploaded evidence into a PDF, lets you preview the exact document that will be sent to the card network, and submits it on your behalf. The process is transparent and contained within your admin.

With PayPal, you submit evidence through the Resolution Center. PayPal reviews it internally before forwarding it to the issuing bank if needed. If you miss the deadline, PayPal rules in the buyer’s favor automatically.

Evidence requirements vary by claim type. For physical goods, the item must be shipped to the address listed on the transaction page, and proof of delivery is required. For orders of $750 or more, signature confirmation is mandatory.

Timelines and Deadlines

Shopify Payments gives merchants 7 to 21 days to respond, driven by the card network rules. Missing the deadline results in an automatic loss.

PayPal’s timeline is broader and longer. Buyers have up to 180 days from the transaction date to open a dispute. Both parties then have 20 days to resolve it directly. If the buyer escalates to a claim, the seller has 10 days to respond. Miss that window, and PayPal decides for the buyer.

Fees and Financial Impact

With Shopify Payments, the disputed amount and the $15 chargeback fee are withdrawn from your balance immediately when a chargeback is issued. The fee is returned if you win, depending on your region.

With PayPal, transaction funds become inaccessible upon a chargeback until the case closes. For card-funded transactions not covered by Seller Protection, a $20 chargeback fee applies. Where Seller Protection covers the transaction, that fee may be waived.

Deeper Insights into Seller Protection Programs

Shopify Protect is available to US-based merchants with a US Shopify Payments account, covering fraudulent and unrecognized chargebacks on eligible Shop Pay orders only. Orders must contain physical items requiring shipping, digital goods, in-store pickups, and Shop Pay Installments orders are excluded. To qualify, the order must be fulfilled within 7 days of placement with a valid tracking number from a supported carrier, and marked in transit within 10 days. When all conditions are met, Shopify handles the dispute automatically, no evidence submission required.

PayPal Seller Protection covers two categories: unauthorized transactions and Item Not Received claims filed through PayPal's Resolution Center. Today, Seller Protection no longer applies to Item Not Received claims where the buyer filed a chargeback directly with their card issuer for a card-funded transaction. Protection for the Item Not Received category applies only to claims made within PayPal's Resolution Center; it does not extend to chargebacks filed with an external card issuer. Unlike Shopify Protect, it is not automatic. Eligibility depends on transaction type, delivery proof, and whether the order is rated Eligible at the time of the dispute.

Appeals and Escalation

Once a Shopify Payments dispute is decided by the issuing bank and the deadline has passed, the outcome is final. There is no appeal stage.

PayPal provides more flexibility. Merchants can appeal PayPal’s claim decision within 10 days if new information is available. In card chargeback cases, PayPal may represent the merchant through pre-arbitration or arbitration. It’s rare, but available in certain scenarios where the initial decision is contested.

How to Prevent and Resolve Shopify Disputes

The best dispute is the one that never happens. Before a transaction, enable Shopify’s fraud analysis tools, verify AVS and CVV matches, and flag high-risk orders before they are shipped. After a transaction, send order confirmations and delivery notifications proactively. Most friendly fraud starts with a charge that a customer simply didn’t recognize.

When a dispute does happen, act fast. Check your admin daily, contact the customer first on recoverable cases, and build evidence that speaks directly to the reason code. Generic responses are pointless. And manual representment doesn’t always satisfy networks’ evidence standards, which is why many merchants get ~20% win rates.

That’s especially true for merchants with volume. Tools like Chargeflow, built for Shopify, automate the entire Shopify dispute process. Instead of managing disputes touchpoint by touchpoint, you get a single system that handles deflection, alerts, evidence, submission, and data analysis end-to-end.

Payment disputes are part of running a store. How you respond, before, during, and after, determines whether they stay manageable or become a threat to your ability to process payments altogether.

Can you dispute with Shopify?

Yes - 'dispute' is Shopify's term for a chargeback filed by a customer with their card issuer; merchants respond to disputes directly through the Shopify admin's evidence-submission tools.

Do customers usually win chargebacks?

Chargebacks default in the customer's favor unless the merchant submits compelling evidence in time, so response speed and evidence quality heavily influence the outcome.

Can I get my money back from Shopify?

If you're a customer disputing a purchase, you get funds back from your card issuer via the chargeback, not directly from Shopify, which only facilitates the merchant's evidence response.

Automate Chargeback Disputes for Your Shopify Store

You can automate evidence collection and submission across every Shopify dispute instead of managing them by hand. Chargeflow submits on time, every time, backed by a 4X ROI guarantee.

Gratis beginnenTerugboekingen?

Dat is niet langer jouw probleem.

Vorder 4 keer meer terugboekingen terug en voorkom tot 90% van de inkomende terugboekingen, dankzij AI en een wereldwijd netwerk van 20.000 handelaren.

.png)