%201.svg)

Klarna frente a Affirm: ¿qué proveedor de pagos «compra ahora, paga después» es mejor en 2026?

¿Devoluciones?

Ya no es un problema para ti.

Recupera cuatro veces más devoluciones y evita hasta el 90 % de las que se producen, gracias a la inteligencia artificial y a una red global de 20 000 comerciantes.

¿No sabes si elegir Klarna o Affirm para tu tienda o tu próxima compra? Aquí tienes un resumen rápido:

- Klarna presta servicio a 114 millones de usuarios en 26 países, salió a bolsa en la Bolsa de Nueva York en septiembre de 2025 y acaba de cerrar un acuerdo de colaboración exclusivo con Walmart, lo que la convierte en la mejor opción para los comerciantes internacionales y las empresas de suscripción.

- Affirm presta servicio a unos 23 millones de usuarios, principalmente en Estados Unidos y Canadá, no cobra comisiones a los consumidores, alcanzó la rentabilidad en el ejercicio fiscal 2025 y destaca en la financiación de compras de alto valor (valor medio de los pedidos: 276 dólares), lo que la convierte en la opción más adecuada para los minoristas especializados en compras de gran cuantía.

- Comisiones de Klarna para comerciantes: entre el 3,29 % y el 5,99 % + 0,30 $ por transacción. Comisiones de Affirm para comerciantes: alrededor del 6 % + 0,30 $.

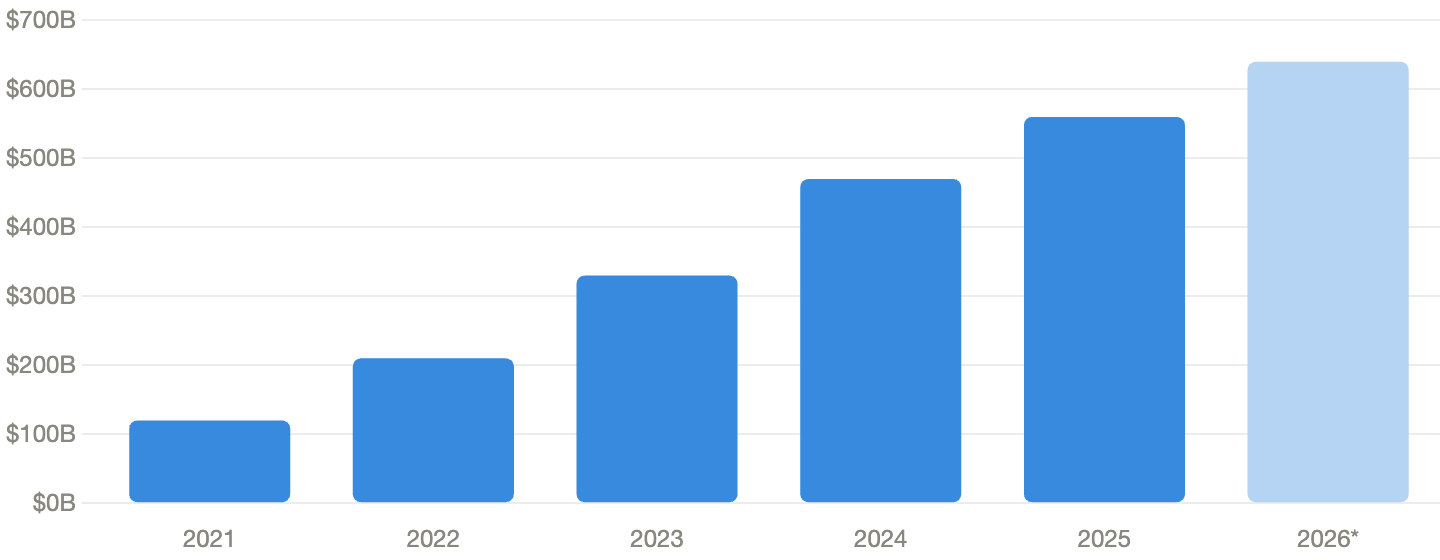

El mercado mundial de «Compra ahora, paga después» (BNPL) alcanzó un volumen bruto de mercancías de aproximadamente 560 000 millones de dólares en 2025, con una tasa de crecimiento anual compuesta prevista del 20,7 %. Por eso, no es de extrañar que los proveedores de pagos BNPL, como Klarna y Affirm, susciten un gran interés en el sector.

Klarna y Affirm Payments están transformando el panorama del comercio electrónico con un conjunto de funciones diseñadas para satisfacer las diversas necesidades de sus clientes. Sin embargo, el debate entre Affirm y Klarna es más complejo de lo que podría parecer a primera vista. Ambas plataformas ofrecen pagos a plazos (BNPL), pero difieren significativamente en cuanto a comisiones, alcance comercial, tipos de interés y mercados objetivo.

Esa es la pregunta que queremos ayudarte a responder en la guía de hoy. Analizaremos los puntos fuertes, las ventajas y los retos de Klarna y Affirm, y te ofreceremos una comparación clara para que puedas decidir qué plataforma se adapta mejor a tus necesidades de pago. Tanto si estás eligiendo entre Klarna y Affirm como comerciante, como si lo haces como comprador, esta guía te ofrece toda la información que necesitas saber.

Klarna vs Affirm: Side-by-Side Comparison (2026)

FactorKlarnaAffirmFounded / HQ2005, Stockholm2012, San FranciscoActive users~114M across 26 countries~23M (US & Canada)Merchant partners~850,000~377,000Merchant fee3.29%–5.99% + $0.30~6% + $0.30Consumer feesLate fee $7 after 10 daysNoneAverage order value~$101~$276FinancingPay in 4, Pay in 30, 6–36 moPay in 4, 3–48 mo (up to $17,500)Chargeback fee$15$15Public statusNYSE (KLAR), Sept 2025Nasdaq (AFRM), 2021Best forGlobal & subscription merchantsHigh-ticket US/Canada merchants

Resumen de las funciones y características de Klarna

Klarna es un proveedor líder de servicios de pago «Compra ahora, paga después» que permite a los consumidores adquirir artículos en tiendas online y físicas sin tener que abonar el importe total por adelantado. Fundada en Estocolmo (Suecia) en 2005, el crecimiento acelerado de Klarna comenzó con la simplificación de los pagos mediante factura para los clientes del comercio electrónico. La reducción de las dificultades en el proceso de pago se tradujo en un aumento de las ventas y en altas tasas de conversión para la empresa.

Sin embargo, la rápida expansión de Klarna se produjo después de que el equipo introdujera el modelo «compra ahora, paga después» a principios de la década de 2000, incorporando a más de 850 000 comercios asociados en todo el mundo y a unos 114 millones de clientes en 26 países, de los cuales unos 34 millones se encuentran en Estados Unidos. Klarna salió a bolsa en la Bolsa de Nueva York en septiembre de 2025, en la mayor salida a bolsa del sector fintech del año, recaudando 1370 millones de dólares y alcanzando una valoración de mercado de más de 17 000 millones de dólares en su primer día de cotización.

En marzo de 2025, Klarna cerró un acuerdo de colaboración exclusiva con Walmart a través de OnePay, una importante iniciativa que anteriormente pertenecía a Affirm. Klarna registró unos ingresos de 2.800 millones de dólares en 2024, con un volumen bruto de mercancías procesadas de 105.000 millones de dólares.

El modelo «compra ahora, paga después» (BNPL) de Klarna ha resultado especialmente beneficioso para los comerciantes online, ya que ha reducido las tasas de abandono de carritos, un problema que había afectado al sector debido a la complejidad de los procesos de pago. La experiencia de pago de Klarna, que genera una mayor tasa de conversión, permite a los compradores pagar sus compras en cuatro plazos sin intereses cada dos semanas o liquidar el importe total en un plazo de 30 días. Se dice que Klarna procesa dos millones de transacciones al día, con usuarios de renombre como Nike, Adidas, H&M y, ahora, Walmart.

¿Cómo funciona Klarna? Características principales

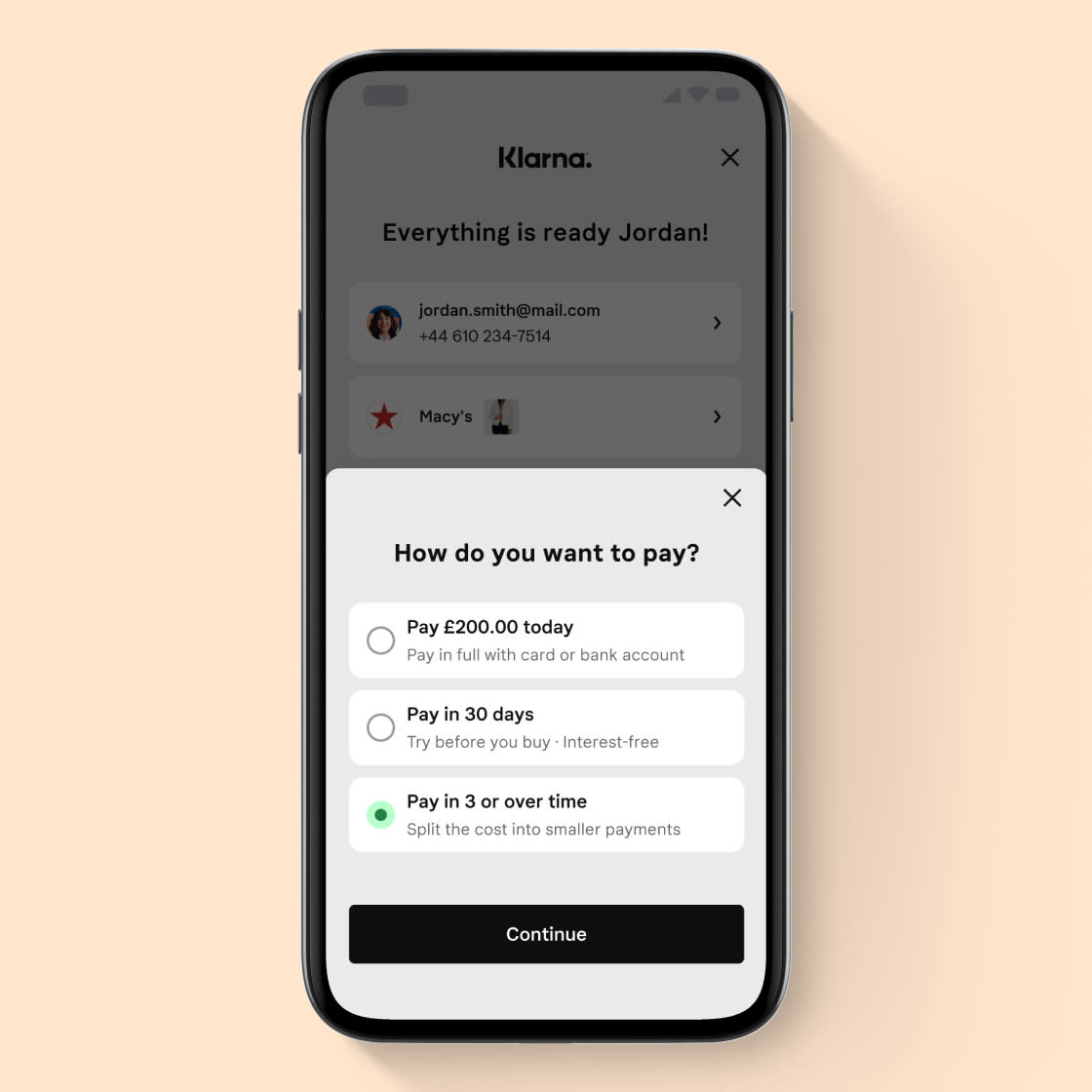

Klarna ofrece a los usuarios un proceso de pago cómodo, tanto si compran en una tienda online, a través de una aplicación móvil o en una tienda física. Entender cómo funciona Klarna es muy sencillo: los compradores eligen Klarna al finalizar la compra y seleccionan un plan de pago.

Klarna ayuda a los usuarios a evitar las deudas abusivas permitiéndoles realizar un seguimiento de sus pedidos, gestionar sus planes de pago y consultar su historial de pagos, así como acceder al servicio de atención al cliente, todo ello desde la aplicación de Klarna. Entre las características más destacadas de Klarna se incluyen las siguientes:

- Paga en 4: Los consumidores pueden dividir sus compras en cuatro plazos sin intereses; el primer pago se abona al finalizar la compra y los tres siguientes se cobran cada dos semanas.

- Paga en 30 días: los clientes pueden comprar ahora y pagar sus compras en un plazo de 30 días si están satisfechos con su compra.

- Préstamos a largo plazo: Klarna ofrece opciones para financiar compras de mayor cuantía a largo plazo —por lo general, entre 6 y 36 meses, con tipos de interés competitivos a partir del 7,99 %— a través de su socio, WebBank.

- Tarjeta Klarna: Los consumidores pueden utilizar una tarjeta virtual de Klarna para pagar a plazos y obtener financiación, incluso si la tienda con la que realizan la transacción aún no ha integrado el servicio. A partir de 2025, Klarna también puso en marcha un programa piloto de tarjetas de débito en Estados Unidos con fondos asegurados por la FDIC.

- Stablecoin KlarnaUSD: Lanzada en noviembre de 2025, Klarna lanzó su propia stablecoin en la cadena de bloques de Stripe para reducir los costes de los pagos internacionales.

- Asistente de compras con IA: Klarna ha puesto en marcha un asistente de compras basado en la tecnología de OpenAI para ayudar a los usuarios a gestionar sus gastos y descubrir productos.

For banks, fintechs, and merchants, Klarna's open banking makes finance "more accessible, fair, and simple for everyone." Klarna achieves this by enabling companies to leverage its connectivity to develop new products that benefit end users. Klarna says 20,000 partners are currently using its open banking API service. Half of the top 100 U.S. online retailers used Klarna's payment tools over the past year, and two-thirds ran advertising campaigns on its platform.

Su integración rápida y sencilla permite a los comerciantes mejorar sus tiendas añadiendo la opción de pagar más tarde. Puedes elegir el método de pago que mejor se adapte a tus clientes, diseñar una solución personalizada o integrarlo a través de proveedores de servicios de pago en plataformas como Shopify, WooCommerce o Magento.

Comisiones de Klarna: ¿cuánto pagan los comerciantes?

El modelo de negocio de Klarna consiste en cobrar a los comerciantes una tarifa fija por transacción y un porcentaje de las ventas, que ronda el 5 % en Estados Unidos. Este porcentaje es ligeramente superior al que aplican los procesadores de tarjetas tradicionales, como Stripe o Shopify Payments. Es importante que los comerciantes comprendan las comisiones de Klarna a la hora de evaluar sus márgenes. Klarna indica que sus comisiones también pueden variar en función del país y del servicio de Klarna que elija utilizar el consumidor:

- Klarna Pay Later: La opción «Pay Later» de Klarna, que permite a los clientes pagar sus compras en un plazo de entre 14 y 30 días, suele conllevar comisiones de tramitación de entre el 3,29 % + 0,30 $ y el 5,99 % + 0,30 $ por transacción.

- Klarna Pay Now: La opción «Pay Now» de Klarna, ofrecida a través de SOFORT —un destacado sistema de transferencia bancaria disponible en Austria, Bélgica, Alemania, los Países Bajos y España—, conlleva una comisión por transacción de aproximadamente el 2,99 % + 40,30 por transacción.

- Financiación de Klarna: La opción de financiación a plazos de Klarna incluye comisiones por transacción que oscilan entre el 3,29 % + 0,30 $ y el 5,99 % + 0,30 $.

- Comisiones para comerciantes de Klarna: Aunque no hay comisiones de alta, las comisiones para comerciantes de Klarna varían cada mes en función del contrato del comerciante y del volumen de ventas.

- Comisiones por devoluciones: Klarna cobra una comisión de unos 15 $ por cada reclamación presentada contra ti.

Los compradores también pueden utilizar la aplicación de Klarna en otras tiendas, con una comisión de servicio de 2,12 $. Puede haber otros costes, como comisiones por conversión de divisas en los pagos internacionales y comisiones de integración. Estos costes varían en función de la plataforma de que se trate.

Las ventajas de Klarna

Klarna se ha consolidado como uno de los principales proveedores de pagos «compra ahora, paga después» (BNPL) en Estados Unidos y a nivel mundial. Entre las ventajas más destacadas de Klarna se incluyen:

- Presencia global con unos 850 000 comercios asociados y unos 114 millones de clientes en 26 países.

- Los procesos de pago acelerados reducen la duración de las transacciones y las tasas de abandono del carrito, un problema recurrente en el comercio electrónico.

- Hay varias opciones de pago disponibles; los clientes pueden elegir entre «Paga en 4», «Paga en 30» o planes de financiación a más largo plazo.

- Las tasas de interés cero en los planes «Paga en 4» o «Paga en 30» fomentan la fidelidad de los clientes, ya que los clientes satisfechos que pueden fraccionar el pago de sus compras son más propensos a volver.

- Klarna protege a los comerciantes de las consecuencias económicas que supone el impago de los clientes al asumir los riesgos asociados a su financiación.

- Klarna is easy to set up and user-friendly, integrating with major eCommerce platforms or shoppable catalogs for quick payment acceptance.

- Las medidas avanzadas de prevención del fraude de Klarna reducen las pérdidas económicas.

- Las consultas de solvencia sin compromiso, con altas probabilidades de aprobación, generan ingresos para las empresas.

- Klarna salió a bolsa en septiembre de 2025, lo que aportó transparencia y credibilidad a nivel institucional a los comerciantes que evalúan el riesgo a largo plazo de la plataforma.

Las desventajas de Klarna

Todas las plataformas tienen inconvenientes que conviene tener en cuenta para tomar una decisión informada. En el caso de Klarna, los inconvenientes señalados son los siguientes:

- Klarna cobra a las empresas una comisión por transacción, que equivale a un porcentaje del importe total de la misma.

- Los consumidores que no cumplan los plazos de pago deberán abonar una comisión de 7 dólares tras 10 días. Sin embargo, Klarna garantiza que el total de las comisiones por demora de un pedido no superará el 25 % del importe total de la compra. Affirm ha calificado estas comisiones como «comisiones innecesarias», un aspecto que conviene tener en cuenta al comparar Klarna y Affirm.

- El impago de una deuda puede dar lugar a que el caso se remita a una agencia de cobro y se comunique a la agencia de información crediticia, lo que afectaría negativamente a la puntuación crediticia de la persona.

- Los analistas han señalado que, dado que los servicios «compra ahora, paga después» utilizan algoritmos internos en lugar de las tradicionales comprobaciones de solvencia crediticia, el sistema puede ser vulnerable al fraude.

Resumen y características principales de Affirm

Affirm es otra empresa muy conocida en el sector de la financiación «compra ahora, paga después». Max Levchin, cofundador de PayPal, fundó esta red de pagos en 2012. La empresa salió a bolsa en el Nasdaq en enero de 2021 y, a principios de 2026, su capitalización bursátil superaba los 28 000 millones de dólares, casi el doble de la valoración de Klarna en su salida a bolsa.

Affirm registró un crecimiento de los ingresos del 46 % en 2024, hasta alcanzar los 2320 millones de dólares, lo que supuso el crecimiento más rápido de todos los principales proveedores de servicios «compra ahora, paga después» (BNPL) ese año, y logró entrar en números negros con un beneficio neto de 52 millones de dólares en el ejercicio fiscal 2025.

Affirm quiere ser una alternativa responsable a las tarjetas de crédito. Los préstamos de Affirm incluyen un plan de pagos fijo, y los compradores conocen sus opciones antes de finalizar cada transacción. De este modo, nunca pagan más de la cantidad acordada. Los usuarios pueden realizar transacciones en línea o mediante la aplicación de Affirm en los comercios participantes, que pueden generar números de tarjeta virtuales para compras en cualquier tienda que acepte Visa. Además, los clientes de Affirm pueden elegir planes de pago de hasta 48 meses, lo que resulta más flexible que las opciones tradicionales de «Paga en 4» que utilizan competidores como Klarna.

Cuando creas una cuenta en Affirm, evalúan tu perfil y te asignan un límite de gasto personalizado. Aunque el límite de gasto varía según cada persona, el límite de gasto de un usuario en Affirm no puede superar los 17 500 $.

Affirm cuenta actualmente con unos 23 millones de usuarios activos y 377 000 comercios asociados, y ofrece integraciones avanzadas con Amazon, Shopify y, hasta marzo de 2025, Walmart.

Características principales de Affirm

Affirm es un servicio de financiación de compras con comercios asociados. A diferencia de otras plataformas que ofrecen préstamos a corto plazo junto con servicios de pago de facturas o de transferencia de dinero, Affirm se centra exclusivamente en la financiación de compras. Entre las características más destacadas de Affirm se incluyen las siguientes:

- Sin comisiones: Los clientes no pagan comisiones por demora en el pago, por pago anticipado, cuotas anuales ni gastos de apertura o cierre de cuenta.

- Paga en 4: La opción «Paga en 4» de Affirm te permite pagar en cuatro cuotas iguales a lo largo de seis semanas, sin intereses ni comisiones, para compras de entre 50 y 1000 dólares.

- Tarjeta Affirm: Los compradores pueden utilizar las tarjetas de débito Affirm para realizar pagos completos, al igual que con las tarjetas de pago tradicionales, o para contratar planes flexibles a través de la aplicación.

- Financiación mensual: Affirm permite a los compradores financiar compras de hasta 17 500 dólares, con plazos de amortización que van de 3 a 48 meses y una tasa de interés anual (TAE) de alrededor del 30 %. Esto depende del riesgo que representes y del comercio en cuestión.

Por lo general, Affirm permite a los comercios establecer límites de crédito para sus clientes, con un límite máximo de 17 500 dólares. Se han asociado con miles de comercios de diversos sectores, como la moda, los viajes, la electrónica, el hogar y el fitness. Puedes comprar con Affirm por Internet o a través de la aplicación móvil, y para las compras en tienda, puedes utilizar la tarjeta virtual.

¿Cuánto cobra Affirm a los comerciantes?

Affirm no cobra comisiones a los compradores. Entonces, ¿cuánto cobra Affirm a los comerciantes? El proveedor de servicios «compra ahora, paga después» cobra un porcentaje de cada transacción. Este es el desglose:

- Tipos de interés de los préstamos de Affirm: La TAE de Affirm oscila entre el 0 % y el 36 %, dependiendo de la solvencia del usuario. Según datos de la Reserva Federal, un usuario puede acabar pagando más con Affirm que con las tarjetas de crédito, cuya TAE media es del 19,07 %.

- Comisiones por procesamiento de transacciones de Affirm: La comisión por procesamiento de transacciones de Affirm para los comerciantes es de aproximadamente un 6 % + 0,30 $ por compra. Esta puede variar en función del riesgo percibido, el tamaño de la empresa y el programa seleccionado.

Affirm ofrece planes personalizados con soluciones a medida para grandes empresas con una estructura de tarifas diferente. Otras comisiones incluyen las comisiones de intercambio y las comisiones de gestión de préstamos que se cobran a los inversores externos.

Ventajas de Affirm

Affirm ofrece tipos de interés a partir del 0 % para plazos de hasta 48 meses. Integrarlo en tu tienda resulta especialmente ventajoso para los vendedores de artículos de alto precio, por encima de los 500 dólares, y para aquellos que se dirigen a los compradores de la Generación Z, cuyo gasto no supera los 100 dólares. Entre las ventajas más destacadas de Affirm se incluyen:

- Empezar es muy fácil; el proceso de registro requiere muy pocos pasos y datos.

- Affirm realiza una evaluación de crédito no invasiva a los compradores para determinar su solvencia sin afectar a su puntuación crediticia.

- Los compradores pueden dividir el importe en cuatro pagos quincenales sin intereses, abonando la primera cuota en el momento de la compra, o bien optar por un plazo de pago ampliado de tres o más meses, lo que supone una elevada tasa de conversión para los comerciantes.

- El servicio «Paga en 4» de Affirmno aplica intereses, lo que lohace muy atractivo para los compradores de la Generación Z y los millennials. Esto podría traducirse en compras recurrentes para ti.

- Los clientes no pagan comisiones por retrasos en los pagos, pagos anticipados, apertura de cuentas ni cierre de cuentas. Este es un factor diferenciador clave en el debate sobre las comisiones de Affirm frente a Klarna.

- Affirm alcanzó la rentabilidad neta en el ejercicio fiscal 2025, un hito importante que aporta estabilidad a largo plazo y confianza a los comercios asociados.

- La plataforma cuenta con valoraciones positivas y se integra con las principales tiendas, como Amazon y Shopify.

Desventajas de Affirm

Los proveedores de servicios «compra ahora, paga después» (BNPL), como Affirm, han sido objeto de críticas por diversos motivos. Las principales desventajas de Affirm son las siguientes:

- Affirm ofrece opciones sin intereses, pero algunos planes a más largo plazo son más caros que la financiación con tarjeta, con tipos de interés de hasta el 36 %.

- Aunque Affirm no cobra recargos por demora, si el impago se prolonga durante más de 120 días, tu préstamo podría pasar a manos de una agencia de cobros, lo que podría afectar negativamente a tu puntuación crediticia.

- Affirm cobra a las empresas una comisión por transacción, que equivale a un porcentaje del importe total de la misma.

- El reembolso de un pedido realizado a través de Affirm es equivalente al reembolso de una tarjeta de crédito, pero Affirm retiene las comisiones de cada transacción.

- En marzo de 2025, Affirm perdió su acuerdo de colaboración exclusiva con Walmart en el ámbito del «compra ahora, paga después» (BNPL) a favor de Klarna, lo que supuso un duro golpe para su presencia en el sector minorista estadounidense.

Klarna frente a Affirm: las diferencias clave

Los servicios «compra ahora, paga después» (BNPL) que ofrecen Klarna y Affirm son bastante similares en muchos aspectos. Sin embargo, existen numerosas diferencias. Al comparar Klarna y Affirm en profundidad, se observan diferencias clave en cuanto a comisiones, alcance y importe de las compras. Analicemos estas diferencias para ayudarte a decidir qué plataforma es la más adecuada para ti.

Formas de pago

- Klarna:

- Ofrece múltiples planes de pago flexibles, como «Paga en 4», «Paga en 30 días» y opciones de financiación a largo plazo a través de WebBank.

- Se requiere un pago inicial del 25 % del importe de la transacción.

- No establece un gasto mínimo ni tiene un límite de gasto predefinido. En su lugar, cada vez que amortizas tu préstamo se toma una decisión de aprobación automática que determina cuánto puedes gastar.

- Afirmar:

- Ofrece planes de pago en 4 o 2 cuotas, planes de pago en 30 cuotas o préstamos a largo plazo que suelen tener una duración de entre 3 y 48 meses.

- Los clientes pueden utilizar el plan «Compra ahora, paga después» en transacciones que cumplan los requisitos y superen los 100 $, y financiar compras de hasta 17 500 $.

- Permite realizar compras sin pago inicial.

Tipos de interés y comisiones

- Klarna:

- Por lo general, ofrece planes de pago sin intereses para opciones a corto plazo.

- Los plazos de financiación más largos tienen un tipo de interés que va del 7,99 % al 29,99 %.

- Se aplica un recargo de 7 dólares tras 10 días de impago.

- Podría comunicar los pagos atrasados y los impagos a la agencia de crédito.

- Las comisiones de los comerciantes varían cada mes en función del contrato del comerciante y del volumen de ventas.

- Afirmar:

- Por lo general, ofrecen pagos con un tipo de interés anual (TAE) del 0 % para los préstamos «Pay in 4».

- Tipos de interés para la financiación a largo plazo de hasta un 36 % TAE.

- No cobra recargos por demora ni intereses compuestos por pagos atrasados.

- Las comisiones para los comerciantes varían en función del riesgo percibido, el tamaño de la empresa y el programa elegido.

Ambas plataformas cobran una comisión por devolución de 15 dólares.

Disponibilidad y aceptación

- Klarna:

- Atiende a una clientela muy variada y colabora con unos 850 000 comercios en 26 países.

- Ampliamente implantado en los principales sectores del comercio minorista, los viajes y la hostelería, la salud y el bienestar, y la automoción.

- 114 millones de consumidores activos en 2025.

- Cotiza en la Bolsa de Nueva York (NYSE) con el símbolo KLAR desde septiembre de 2025.

- Exige que los usuarios sean residentes de los Estados Unidos o sus territorios, tengan al menos 18 años, dispongan de una tarjeta o cuenta bancaria válida, cuenten con un historial crediticio positivo y puedan recibir códigos de verificación por mensaje de texto.

- Mayores índices de aprobación.

- Afirmar:

- Se dirige principalmente a empresas que venden directamente a consumidores de Estados Unidos y Canadá.

- No es compatible con sectores de comercio electrónico de alto riesgo.

- A principios de 2026, contaba con aproximadamente 23 millones de usuarios activos y 377 000 comerciantes activos.

- Exige que los usuarios sean residentes en Estados Unidos, Canadá o Australia, tengan al menos 18 años, dispongan de una tarjeta o cuenta bancaria válida, cuenten con un historial crediticio positivo y puedan recibir códigos de verificación por SMS.

- Menores índices de aprobación.

Público objetivo

- Ambas plataformas atraen principalmente a un público más joven.

- Según Klarna, el 80 % de los seguidores de su cuenta de Instagram tiene menos de 34 años, el 60 % de sus clientes son mujeres y el 40 % son hombres.

- Affirm señala que sus servicios resultan especialmente atractivos para los millennials y la generación Z, ya que el 46,14 % de los usuarios son hombres y el 53,86 % son mujeres.

¿Qué es mejor, Klarna o Affirm? El veredicto definitivo

Klarna y Affirm Payments han transformado la forma en que los consumidores realizan sus pagos y disfrutan de los productos que les gustan. Son seguros de usar y cuentan con numerosas funciones, y los tipos de interés suelen ser asequibles. Integrarlos en tu tienda te ayuda a mejorar el valor medio de los pedidos y a reducir al mínimo el abandono de carritos. Entonces, ¿qué es mejor para tu negocio, Klarna o Affirm? ¿Y qué es mejor para el consumidor, Affirm o Klarna? La respuesta depende de tu caso concreto. Este es nuestro veredicto sobre cuál es mejor, Klarna o Affirm:

Cuándo elegir Klarna

- Servicio de suscripción: Klarna permite a los clientes suscribirse a servicios y guardar sus preferencias de pago para las renovaciones automáticas. Los usuarios pueden gestionar su configuración en la aplicación de Klarna.

- Producto bajo demanda: utilizar Klarna como método de pago preferido en un monedero digital agiliza la compra con un solo clic de artículos bajo demanda, con opciones de pago flexibles.

- Proveedor de servicios de banca abierta: los proveedores que ofrecen servicios «Pagar ahora» pueden permitir a sus usuarios evitar las redes de tarjetas pagando a Klarna directamente desde su cuenta bancaria.

- Pymes con operaciones internacionales: Klarna ofrece una cobertura más amplia.

- Empresas dirigidas a los clientes de Walmart: tras el acuerdo de colaboración exclusivo entre Klarna y Walmart/OnePay, firmado en marzo de 2025, Klarna se ha convertido en el proveedor de pago aplazado (BNPL) preferido por el minorista más grande del mundo.

Cuándo elegir Affirm

- Compras de alto importe: Los compradores suelen utilizar Affirm para realizar transacciones online de gran cuantía, ya que ofrece una solución fiable y rentable. El valor medio de los pedidos de Affirm, de 276 dólares, es casi el triple del de Klarna (unos 101 dólares), lo que lo convierte en la opción ideal para los comercios que venden productos de alto precio.

- Emergencias: Los usuarios de Affirm confían en la plataforma para hacer frente a gastos imprevistos, como reparaciones del coche o emergencias médicas.

- Transacciones locales en EE. UU. o Canadá: si tu clientela se encuentra en EE. UU. y Canadá, y tienes una excelente calificación crediticia, Affirm puede ser la mejor opción para ti.

- Entornos sin comisiones: si a tus clientes les preocupan los recargos por demora y las sanciones, el modelo sin comisiones de Affirm supone una clara ventaja frente a Klarna.

- Vendedores de Amazon: la profunda integración de Affirm con Amazon la convierte en la opción predeterminada de «compra ahora, paga después» (BNPL) para uno de los mercados online más grandes del mundo.

Cómo Chargeflow ayuda a los comerciantes que ofrecen pagos «compra ahora, paga después»

Regardless of which BNPL provider you choose, disputes still reach you as chargebacks. Chargeflow helps Buy Now, Pay Later merchants prevent and recover false and fraudulent chargebacks on autopilot, with automated chargeback protection and real-time chargeback prevention alerts that stop much of the friendly fraud these platforms attract. The success-based pricing means you only pay for cases won, and our dispute win rates have consistently exceeded industry averages.

¡Toma el control de tus devoluciones hoy mismo! Nuestra tecnología avanzada, nuestra integración perfecta y nuestra excepcional tasa de éxito en la resolución de disputas son ideales para las empresas de comercio electrónico que desean mejorar sus procesos de pago y proteger sus ingresos por ventas. A continuación te explicamos cómo empezar.

Preguntas frecuentes: Klarna frente a Affirm

¿Cuál es la diferencia entre Klarna y Affirm?

La principal diferencia entre Klarna y Affirm radica en el alcance geográfico, las estructuras de comisiones y el importe de las compras. Klarna presta servicio a 114 millones de consumidores en 26 países y cobra a los usuarios comisiones por demora a partir de 7 dólares tras 10 días. Affirm presta servicio a aproximadamente 23 millones de usuarios, principalmente en Estados Unidos y Canadá, no cobra comisiones a los consumidores y se adapta mejor a compras de mayor importe, con un promedio de 276 dólares por pedido.

¿Qué es mejor para los comerciantes, Klarna o Affirm?

La elección entre Klarna y Affirm como mejor opción para los comerciantes depende de su base de clientes y del valor medio de los pedidos. Si vende a nivel internacional o a un público amplio, Klarna ofrece un mayor alcance global y tasas de aprobación más altas. Si vende artículos de alto precio en EE. UU. y busca un modelo sin comisiones que sus clientes valoren, Affirm es la mejor opción.

¿Qué es mejor para los consumidores, Affirm o Klarna?

Para los consumidores que dudan entre Affirm y Klarna, la pregunta clave es: ¿prefieres no pagar comisiones o disponer de opciones de pago más flexibles? Affirm nunca cobra recargos por demora, comisiones ocultas ni penalizaciones por pago anticipado. Klarna ofrece una mayor variedad de planes de pago y es aceptada en más comercios de todo el mundo, pero sí cobra recargos por demora.

¿Cuánto cobra Affirm a los comerciantes?

La comisión por transacción de Affirm es de aproximadamente un 6 % + 0,30 $ por compra. Esta comisión es ligeramente superior a la de Klarna, que suele oscilar entre el 3,29 % + 0,30 $ y el 5,99 % + 0,30 $. Ambas plataformas cobran una comisión por devolución de 15 $. Affirm puede ofrecer tarifas personalizadas para comerciantes de gran tamaño.

¿Cuáles son las comisiones de Klarna para los comerciantes?

Las comisiones de Klarna para los comerciantes varían en función del producto que se utilice. Las comisiones de Klarna Pay Later oscilan entre el 3,29 % + 0,30 $ y el 5,99 % + 0,30 $ por transacción. Las de Klarna Pay Now (a través de SOFORT) son de aproximadamente el 2,99 % + 0,30 $. No hay comisiones de alta, pero las cuotas mensuales varían según el contrato y el volumen de ventas. Se aplica una comisión por devolución de 15 $ por cada disputa.

¿Cómo funciona Klarna?

Al finalizar la compra, los clientes seleccionan Klarna como método de pago y eligen una opción: «Pagar en 4» (cuatro pagos quincenales sin intereses), «Pagar en 30» (pago íntegro en un plazo de 30 días) o financiación mensual (de 6 a 36 meses a través de WebBank). Klarna paga por adelantado al comerciante y cobra los pagos al consumidor. Los clientes pueden gestionar los pagos, realizar el seguimiento de los pedidos y acceder al servicio de atención al cliente a través de la aplicación de Klarna.

¿Qué es mejor, Klarna o Affirm, para artículos de alto precio?

Para compras de alto valor, Affirm suele ser la mejor opción. Affirm ofrece financiación de hasta 17 500 $ con plazos de hasta 48 meses, y el valor medio de sus pedidos, de 276 $, es significativamente superior al de Klarna, que ronda los 101 $. Si te preguntas cuál es mejor, Klarna o Affirm, para una compra de más de 1000 $, los planes a más largo plazo de Affirm suelen ser más competitivos, aunque los tipos de interés pueden alcanzar el 36 % TAE en los planes prolongados.

¿Le quitó Klarna a Walmart como cliente a Affirm?

Sí. En marzo de 2025, Klarna cerró un acuerdo de colaboración exclusivo con Walmart a través de su filial de tecnología financiera OnePay, sustituyendo así a Affirm como proveedor de servicios «compra ahora, paga después» (BNPL) de Walmart. Este fue uno de los mayores cambios competitivos en el panorama de la competencia entre Klarna y Affirm de los últimos años y reforzó considerablemente la posición de Klarna en el mercado estadounidense de cara a su salida a bolsa en septiembre de 2025.

Datos de mercado

- Estadísticas de Chargeflow sobre el modelo «Compra ahora, paga después» (BNPL) para 2026: https://www.chargeflow.io/blog/buy-now-pay-later-statistics

Datos de Klarna

- Klarna en Wikipedia (salida a bolsa en 2025, número de usuarios y comerciantes, países, moneda estable, asistente de IA): https://en.wikipedia.org/wiki/Klarna

- Morningstar — Análisis de la valoración de la salida a bolsa de Klarna: https://www.morningstar.com/stocks/whats-behind-klarnas-14-billion-ipo-valuation

- Digital Commerce 360 — Salida a bolsa de Klarna con una valoración de 20 000 millones de dólares: https://www.digitalcommerce360.com/2025/09/12/klarna-ipo-20-billion-valuation/

- PM Insights — Salida a bolsa de Klarna y alianza con Walmart: https://www.pminsights.com/insights/klarna-leads-triple-fintech-ipo-wave-this-week

Datos de Affirm

- Relaciones con los inversores de Affirm: ingresos, rentabilidad y estructura de comisiones: https://investors.affirm.com/news-releases/news-release-details/affirm-difference-building-new-kind-payments-network-money-and

- Business of Apps — Cuota de mercado y estadísticas de ingresos del BNPL: https://www.businessofapps.com/data/buy-now-pay-later-app-market/

Datos comparativos

- Oreate AI — Klarna frente a Affirm: valor medio de los pedidos y número de usuarios: https://www.oreateai.com/blog/klarna-vs-affirm-a-deep-dive-into-the-bnpl-giants/

¿Devoluciones?

Ya no es un problema para ti.

Recupera cuatro veces más devoluciones y evita hasta el 90 % de las que se producen, gracias a la inteligencia artificial y a una red global de 20 000 comerciantes.

.png)

.avif)