%201.svg)

Google Play Just Made Chargebacks Your Problem

¿Devoluciones?

Ya no es un problema para ti.

Recupera cuatro veces más devoluciones y evita hasta el 90 % de las que se producen, gracias a la inteligencia artificial y a una red global de 20 000 comerciantes.

Google Play acaba de trasladar la responsabilidad por las devoluciones a los desarrolladores. Esto es lo que significa en la práctica:

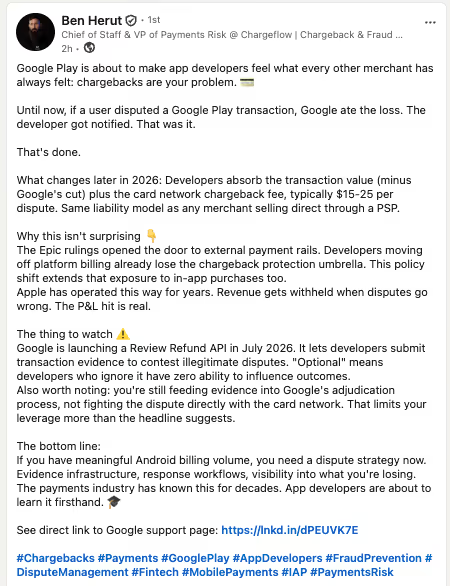

- Google Play deja de asumir las pérdidas por devoluciones; a partir de ahora, los desarrolladores deberán pagarlas

- Cada reclamación te cuesta el importe de la transacción (menos la comisión de Google) más entre 15 y 25 dólares en concepto de comisiones de la red de tarjetas.

- La API de reembolso de reseñas de Google se lanzará en julio de 2026; aunque se califica de «opcional», será la única forma de impugnar las disputas.

- Los datos se envían al sistema de Google, no directamente a la red de tarjetas, por lo que tu capacidad de negociación es limitada

- Las aplicaciones de videojuegos, las suscripciones y la facturación de gran volumen en Android son las más vulnerables; elabora tu estrategia ahora mismo

«Google Play está a punto de hacer que los desarrolladores de aplicaciones sientan lo mismo que siempre han sentido todos los demás comerciantes: las devoluciones son problema tuyo».

Una actualización del servicio de Google Play ha llegado discretamente a los buzones de correo de los desarrolladores y ya está generando un intenso debate en las comunidades dedicadas a los pagos y al desarrollo de aplicaciones. A partir de finales de 2026, los desarrolladores de Google Play comenzarán a compartir los costes de las devoluciones, un cambio estructural que alinea a Play con la forma en que siempre ha funcionado el resto del comercio digital, pero que supone un riesgo financiero real para los editores de aplicaciones que no estaban preparados para ello.

Para los desarrolladores que han basado su estrategia de monetización en el entorno de facturación de Play, históricamente protegido, la realidad financiera está a punto de cambiar radicalmente. En esta entrada se analiza con detalle qué es lo que va a cambiar, qué se esconde en la letra pequeña y cómo debería ser una respuesta adecuada, antes de que la política entre en vigor.

¿Qué ha cambiado realmente?

Hasta ahora, el procedimiento era sencillo: si un usuario impugnaba una transacción de Google Play directamente ante su entidad financiera, Google asumía la pérdida. El desarrollador recibía una notificación. Y eso era todo.

Ese acuerdo está llegando a su fin.

A continuación se detalla exactamente cómo se desglosa el nuevo modelo de reparto de costes:

En concreto: una compra dentro de la aplicación de 9,99 dólares que sea objeto de una reclamación te costará aproximadamente 9,99 dólares, más la comisión por devolución. Google se hace cargo de su comisión por servicio. Tú asumes todos los demás gastos. Se trata del mismo modelo de responsabilidad por devoluciones que el de cualquier comerciante que venda directamente a través de un proveedor de servicios de pago como Stripe, PayPal o Braintree.

Análisis de Chargeflow sobre las tres cifras que todo desarrollador de Google Play debe conocer.

Por qué esto no es sorprendente

El anuncio combina dos aspectos: una detección de fraudes mejorada —Google afirma haber evitado 3.4 mil millones de dólares en fraudes y abusos en 2025— y el reparto de los costes de las devoluciones, presentado como algo acorde con los estándares del sector. Ambos aspectos son ciertos. Pero hay un contexto más amplio que explica por qué este cambio de política era inevitable.

Las sentencias del caso Epic contra Google abrieron la puerta a los sistemas de pago externos en Android. Los desarrolladores que dejaron de utilizar la facturación de la plataforma ya perdieron la protección frente a las devoluciones que esta ofrecía. Esta política amplía ese mismo riesgo a las compras dentro de la aplicación que siguen utilizando el sistema de facturación propio de Google. No se trata de una nueva filosofía, sino de que la filosofía existente se adapta al resto del producto.

Apple lleva años funcionando así. Cuando surgen disputas, se retienen los ingresos, y el impacto en la cuenta de resultados es real. Google se está poniendo al día con la situación actual del sector.

El detalle más importante del que nadie habla

Detrás de las noticias sobre las comisiones por devolución de cargo se esconde algo que, en la práctica, tiene mucha más importancia, y que la mayoría de los medios han pasado por alto por completo al informar sobre este anuncio.

«Opcional» significa que los desarrolladores que lo ignoren no tendrán ninguna capacidad para influir en el resultado de las disputas. Cuando se presenta una devolución de cargo, Google se encarga de resolverla y, si no aportas pruebas, la decisión se tomará en tu contra por defecto. Esta API es tu única herramienta, y la mayoría de los desarrolladores no sabrán que existe hasta que ya hayan perdido disputas que podrían haber ganado.

«Sigues aportando pruebas al proceso de resolución de Google, en lugar de resolver la disputa directamente con la red de tarjetas. Eso limita tu capacidad de negociación más de lo que sugiere el titular».

— Ben Herut, jefe de personal y vicepresidente de riesgo de pagos, Chargeflow

A diferencia de los procedimientos tradicionales de reclamación de devoluciones, en los que los comerciantes envían las pruebas directamente al banco emisor a través de su entidad adquirente, en este caso dependes de que Google actúe como intermediario. La calidad de tus pruebas es importante, pero también lo es su proceso.

¿Qué promotores inmobiliarios corren mayor riesgo?

No todas las aplicaciones tienen el mismo nivel de exposición. El riesgo de devolución aumenta en función del volumen de transacciones, la frecuencia de compra, el tipo de producto y las características de tu base de usuarios.

Por qué la detección de fraudes por sí sola no te salvará

Esto es lo que no abordarán los anuncios de Google sobre la detección mejorada del fraude: la mayoría de las devoluciones de cargo en las tiendas de aplicaciones no se deben a tarjetas robadas ni a redes organizadas de fraude. Se deben a un patrón que el sector de los pagos denomina «fraude amistoso»: clientes legítimos que realizan una compra, utilizan el producto y, a continuación, impugnan el cargo ante su banco.

En el mundo de los productos digitales, esto es especialmente habitual. No hay ningún envío físico que rastrear, ni firma de entrega, ni prueba evidente de recepción. Los usuarios que saben cómo tramitar una reclamación bancaria suelen considerar que es más rápido y fiable que ponerse en contacto con el servicio de asistencia del desarrollador. El resultado, desde su punto de vista, es el mismo, pero ahora el coste recae íntegramente sobre ti.

Las medidas de protección mejoradas de Google están diseñadas para detectar patrones de abuso externos y la manipulación sistemática de los reembolsos. El fraude «amistoso» se mueve en la zona gris entre esos sistemas. La detección automatizada tiene dificultades para distinguir entre un infractor y un comprador que ha cambiado de opinión y ha decidido presentar una reclamación en lugar de solicitar un reembolso. Esa laguna ahora tiene un coste asociado.

El sector de los pagos lleva décadas siendo consciente de este problema. Los desarrolladores de aplicaciones que han trabajado dentro del entorno protegido de Play están a punto de enfrentarse a él por primera vez.

Elaboración de una estrategia para la resolución de litigios antes de julio

El aviso sobre la política indica que, por el momento, no es necesario tomar ninguna medida. Sin embargo, la API de revisión de reembolsos entrará en funcionamiento en julio de 2026, y la responsabilidad por devoluciones, de carácter más amplio, se aplicará más adelante ese mismo año. Los desarrolladores que se preparen ahora podrán asimilar estos cambios sin interrupciones. Los que esperen tendrán que dedicar la segunda mitad de 2026 a ponerse al día, lo que les supondrá un coste.

1. Analiza tu exposición actual a las devoluciones. Recopila los datos sobre reclamaciones de los últimos 6 a 12 meses. ¿Cuál es tu tasa de reclamaciones por producto, zona geográfica y grupo de usuarios? Si nunca has analizado estos datos, es posible que ya tengas un problema del que no eres consciente. Esta referencia determina todo lo demás.

2. Crea ya una infraestructura de pruebas de las transacciones. La API de revisión de reembolsos requiere que se presenten pruebas para que sea efectiva, y es necesario que esas pruebas se recojan en el momento de la transacción, no después de que se haya presentado una reclamación. Empieza a registrar las direcciones IP, las huellas digitales de los dispositivos, los datos de sesión, los eventos de uso y las confirmaciones de entrega de cada transacción.

3. Planifica específicamente para la API de revisión de reembolsos. No consideres el lanzamiento de julio de 2026 como algo que se abordará en el futuro. Es tu principal mecanismo para influir en el resultado de las disputas en Play. Familiarízate con los requisitos de envío, crea flujos de trabajo para las respuestas y realiza pruebas antes de que entre en funcionamiento. Ser reactivo equivale a perder.

4. Revisa tu política de reembolsos. Una política de reembolsos proactiva y accesible reduce las devoluciones. Los usuarios que pueden obtener fácilmente un reembolso a través del servicio de atención al cliente son mucho menos propensos a presentar una reclamación bancaria. Una devolución te cuesta el precio de venta más entre 15 y 25 dólares en comisiones, mientras que un reembolso solo te cuesta el precio de venta.

5. Controla tu tasa de disputas. Las redes de tarjetas establecen unos umbrales —normalmente en torno al 1 %— por encima de los cuales los comerciantes se enfrentan a sanciones o a la cancelación de su cuenta. Los desarrolladores que no hayan estado realizando un seguimiento de este dato deben empezar a hacerlo de inmediato.

6. Implementar medidas de prevención y automatización de las devoluciones. Las alertas de disputas en tiempo real te permiten realizar reembolsos de forma proactiva antes de que se formalice una devolución, lo que evita por completo el pago de la comisión. Los sistemas automatizados de respuesta a disputas garantizan que los expedientes de pruebas se presenten dentro de los ajustados plazos bancarios, sin que ello suponga una carga administrativa manual a gran escala.

Frequently Asked Questions

¿Cuál es la nueva política de devoluciones de Google Play para 2026? A partir de finales de 2026, Google Play exigirá a los desarrolladores que asuman los costes de las devoluciones cuando los usuarios impugnen las transacciones ante su banco. Los desarrolladores pasarán a ser responsables del importe de la transacción (menos la comisión de servicio de Google) más la comisión por devolución de la red de tarjetas, que suele oscilar entre 15 y 25 dólares por impugnación. Anteriormente, Google asumía íntegramente estas pérdidas.

¿Qué es la API de reembolso de reseñas de Google Play y tengo que usarla? La API de reembolso de reseñas se pondrá en marcha en julio de 2026 y permitirá a los desarrolladores presentar pruebas de las transacciones para impugnar las devoluciones de cargo indebidas dentro del sistema de Google. Aunque se califica de «opcional», los desarrolladores que no la utilicen no tendrán ninguna posibilidad de influir en el resultado de las disputas. Técnicamente es opcional, pero ignorarla significa perder automáticamente todas las disputas que podrías haber ganado.

¿Cuánto me va a costar realmente cada devolución? Los desarrolladores asumen el precio total de la compra, menos la comisión de servicio de Google, más la comisión por devolución de la red de tarjetas, que oscila entre 15 y 25 dólares. Una compra dentro de la aplicación de 9,99 dólares que sea objeto de una disputa podría suponer un coste total de entre 25 y 35 dólares. A gran escala, incluso una tasa de disputas modesta supone un importante impacto en los ingresos mensuales.

¿La API de reembolso de Review es lo mismo que la reclamación de una devolución de cargo? No. En la reclamación tradicional, los comerciantes envían las pruebas directamente al banco emisor a través de su procesador de pagos. Con la API de reembolso de Review, las pruebas se introducen en el sistema interno de resolución de disputas de Google. Google actúa como intermediario, lo que limita tu capacidad de negociación en comparación con la resolución directa de disputas con los emisores.

¿Qué es el fraude amistoso y por qué es relevante en este contexto? El fraude amistoso se produce cuando un cliente legítimo realiza una compra, utiliza el producto y, a continuación, impugna el cargo ante su banco. Es la forma más habitual de devolución de cargo en el ámbito de los productos digitales, y los sistemas de detección de fraude de Google no están diseñados para detectarlo de forma fiable. Ahora que los costes de las devoluciones de cargo recaen sobre los desarrolladores, el fraude amistoso se convierte, por primera vez, en un problema directo para la cuenta de resultados.

En resumen

La actualización de la política de devoluciones de Google Play supone un cambio fundamental en la economía de los desarrolladores. Si tienes un volumen significativo de facturación en Android, necesitas ya mismo una estrategia para gestionar las reclamaciones, una infraestructura para recopilar pruebas, procesos de respuesta y una visibilidad completa de lo que estás perdiendo y por qué.

Los desarrolladores que consideren esto como una llamada de atención y creen sistemas adecuados de gestión de devoluciones podrán adaptarse a estos cambios sin grandes trastornos. Los que no lo hagan se darán cuenta de que una tasa de disputas moderada se convertirá, sin que se den cuenta, en una partida mensual significativa, sin posibilidad de impugnarla.

Los picos de temporada, la nueva responsabilidad por cada litigio y el plazo de la API que vence en julio no dejan mucho margen de maniobra. El momento de crear la infraestructura es antes de que la necesites.

Chargeflow automatiza la gestión de las disputas por devoluciones y su prevención para las empresas digitales. Descubre cómo Chargeflow puede ayudarte →

¿Devoluciones?

Ya no es un problema para ti.

Recupera cuatro veces más devoluciones y evita hasta el 90 % de las que se producen, gracias a la inteligencia artificial y a una red global de 20 000 comerciantes.

.png)

.avif)