%201.svg)

Litige Google Pay : comment contester et régler des prélèvements

Des rétrofacturations ?

Ce n'est plus votre problème.

Récupérez 4 fois plus de rétrofacturations et prévenez jusqu’à 90 % de celles à venir, grâce à l’IA et à un réseau mondial de 20 000 commerçants.

Les litiges liés à Google Pay ne constituent techniquement pas des rejets de prélèvement classiques. En raison de la tokenisation, de l’authentification biométrique et des règles de responsabilité propres à chaque réseau, les commerçants sont souvent soumis à des exigences de preuve plus strictes et disposent d’une visibilité réduite sur les données transactionnelles. Les litiges sont traités par votre prestataire de paiement, et non directement par Google, et les délais serrés impliquent que des e-mails manqués ou des réponses tardives peuvent entraîner des pertes automatiques. Pour obtenir gain de cause, vous devez vous préparer à l’avance. Conservez les preuves de livraison, comprenez le transfert de responsabilité, réagissez rapidement et utilisez des outils tels que Chargeflow centralisent le suivi des litiges et la soumission des preuves avant l’expiration des délais.

Un litige Google Pay est une réclamation déposée par un acheteur concernant une transaction effectuée via Google Pay, soit via les outils d'assistance de Google, soit auprès de l'émetteur de la carte utilisée, étant donné que Google Pay est un portefeuille électronique et non un émetteur de cartes pour la plupart des achats.

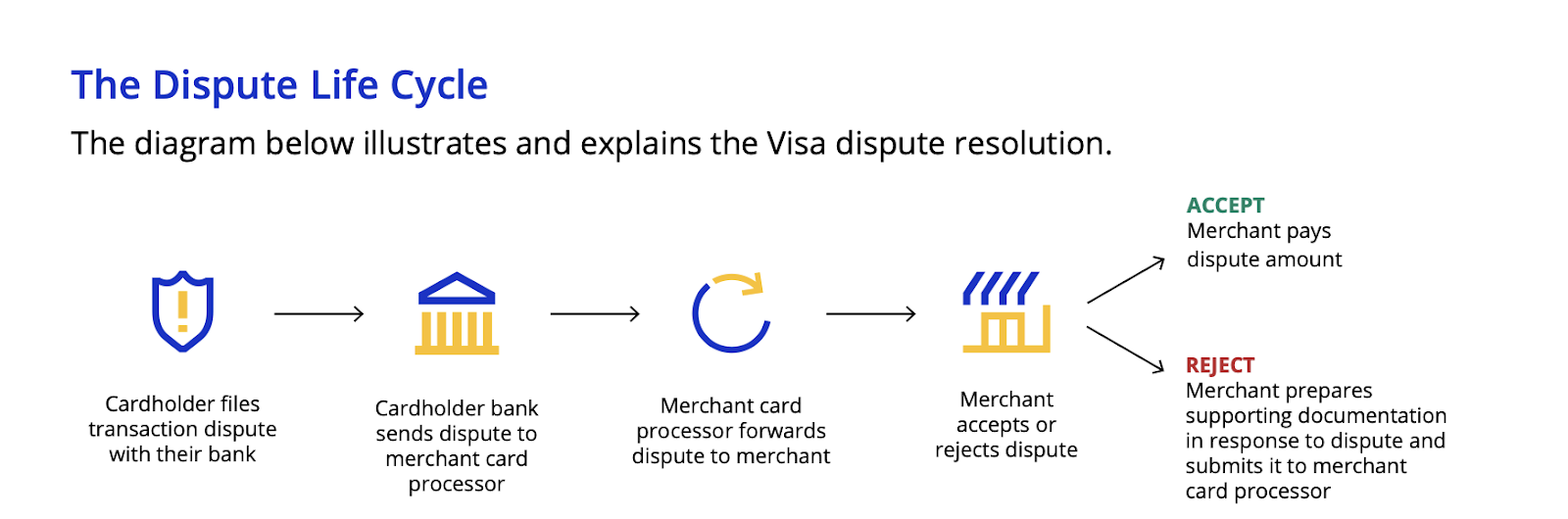

| Étape | Qui | Action | Calendrier type |

|---|---|---|---|

| 1. Recours introduit | Titulaire de la carte | Signaler une transaction via le service d'assistance Google Pay ou l'émetteur de la carte | Dans un délai de 60 à 120 jours à compter de la date du relevé |

| 2. Rétrofacturation émise | Banque émettrice / Réseau | Demande officielle de rétrofacturation envoyée avec le code de motif à l'acquéreur du commerçant | 5 à 10 jours ouvrables |

| 3. Pièces à conviction produites | Commerçant | Fournit des accusés de réception, des reçus et de la correspondance | 20 à 30 jours |

| 4. Résolution | Réseau | Les fonds ont été restitués au commerçant ou le litige est en cours avec le titulaire de la carte | 30 à 45 jours |

Les litiges liés à Google Pay ont une réputation auprès des commerçants que les guides classiques sur les rétrofacturations abordent rarement. Dans plusieurs enquêtes annuelles menées par Ravelin, les litiges liés à Google Pay sont systématiquement cités comme les plus difficiles à contester.

Les raisons sont bien précises. Les exigences en matière de preuves sont plus strictes, et le transfert de responsabilité dépend de la manière dont la transaction a été authentifiée et du pays d'émission de la carte du client. Deux transactions Google Pay qui semblent identiques à première vue peuvent aboutir à des résultats de litige totalement différents, en fonction de facteurs que la plupart des commerçants ne prennent jamais en compte.

C'est la préparation qui distingue les commerçants qui parviennent à régler les litiges de ceux qui en subissent les conséquences. Ce guide explique le fonctionnement du mécanisme de transfert de responsabilité de Google, les documents que Google prend réellement en compte, et les risques liés à vos données transactionnelles que vous ne percevez peut-être pas encore.

Qu'est-ce qu'un litige Google Pay ?

Un litige Google Pay est une contestation officielle déposée par un client à l'encontre d'une transaction traitée via Google Pay. Les termes « litige » et « rejet de débit » sont souvent utilisés de manière interchangeable dans ce contexte, car un litige déclenche généralement la procédure de rejet de débit : les fonds sont bloqués, des justificatifs sont demandés et un tiers statue sur l'issue du litige.

Le rôle de Google dans un litige est similaire à celui de n'importe quel intermédiaire de paiement. Il se positionne entre le réseau de cartes et la banque émettrice, transmettant les notifications de litige, recueillant les éléments de preuve fournis par le commerçant et déposant des demandes de réexamen lorsque le dossier est fondé. C'est la banque émettrice qui prend la décision finale.

Les clients qui souhaitent se faire rembourser trouvent souvent qu’il est plus rapide et plus avantageux de déposer une contestation que de demander directement un remboursement. C’est l’un des principaux facteurs à l’origine de la fraude amicale, que le client en soit conscient ou non. Un remboursement est une démarche initiée par le commerçant. Une contestation contourne entièrement ce canal et, une fois déposée, la procédure relève de la compétence de l’émetteur de la carte.

Puis-je contester un prélèvement sur Google Pay ?

Les clients qui posent cette question cherchent à savoir comment contester un paiement effectué via Google Pay. En tant que commerçant, vous devez bien comprendre ce que la réponse implique pour vous lorsque ce litige est déposé.

Un titulaire de carte peut contester un paiement effectué via Google Pay. Pour ce faire, il doit toutefois passer par sa banque émettrice. La contestation est ensuite transmise via le réseau de la carte, puis Google vous la transmet. C'est donc à vous qu'il incombe de prouver votre innocence.

Comment fonctionnent les litiges Google Pay (et ce que les commerçants doivent savoir pour les remporter)

Lorsqu'un client conteste une transaction Google Pay, la banque examine la réclamation, accorde un avoir provisoire au client (si la réclamation est fondée, ne serait-ce qu'en principe) et transmet la contestation à Google Pay via le réseau de cartes. Vous en serez alors informé.

Google Pay informe les commerçants d'un litige par e-mail via le Centre de paiement Google. La notification comprend les détails de la transaction contestée, le code de motif attribué par la banque émettrice et un délai pour répondre en fournissant des justificatifs. Il n'y a ni appel téléphonique, ni délai de grâce, ni possibilité de négocier ce délai.

C'est là que de nombreux commerçants qui gèrent les litiges manuellement sont perdants d'avance. Dans des boîtes de réception saturées, les notifications de litige peuvent passer inaperçues, être filtrées ou reléguées au second plan. Google n'assure pas le suivi.

Dates limites importantes pour répondre

Les délais de réponse aux contestations Google Pay sont fixés par les réseaux de cartes, et non par Google. Pour les contestations Visa, les commerçants disposent généralement de 20 jours calendaires à compter de la date de notification pour soumettre une réponse. Les contestations Mastercard vous accordent un délai plus long de 45 jours. Le non-respect du délai est considéré comme une acceptation du rejet de débit. Vos fonds sont débités et le dossier est clos.

Réagir rapidement présente également un intérêt pratique qui va au-delà de la simple conformité. Le délai utile est souvent compris entre 10 et 30 jours, le temps de recevoir une notification, de mener un examen interne et de rassembler des preuves. Étant donné que Google examine vos preuves avant de décider de les transmettre ou non, une soumission rapide lui laisse le temps de le faire. Les prestataires de paiement peuvent également raccourcir davantage le délai imposé par les réseaux de cartes grâce à leurs propres politiques internes, ce qui rend la situation encore plus urgente que ne le laisse supposer le délai fixé par les réseaux.

Que deviennent vos fonds en cas de litige avec Google Pay ?

Une fois qu'un litige est déposé, le montant de la transaction est débité de votre compte Google Payments ou retenu sur un paiement en attente. Les conditions générales de Google applicables aux commerçants autorisent Google à bloquer les fonds liés à un litige pendant une période pouvant aller jusqu'à 180 jours. Dans la pratique, les enquêtes standard relatives aux litiges aboutissent généralement bien avant l'expiration de ce délai, mais les commerçants dont la trésorerie est tendue doivent tenir compte de la possibilité d'un blocage prolongé, en particulier si plusieurs litiges sont ouverts simultanément.

Google mettra tout en œuvre, dans la mesure du raisonnable, pour examiner la réclamation et vous représenter dans la mesure du possible. Si Google présente une contestation et que l'émetteur se prononce en votre faveur, le rejet de débit sera annulé et les frais de transaction vous seront remboursés sur votre compte.

Si le litige est confirmé, que ce soit parce que Google a estimé que vos preuves ne justifiaient pas une nouvelle présentation ou parce que l'émetteur s'est prononcé contre vous après examen, le rejet de débit est maintenu, le crédit provisoire devient définitif et des frais de rejet de débit sont facturés sur votre compte.

Pourquoi les clients déposent-ils des réclamations via Google Pay à l'encontre des commerçants ?

Les codes de motif utilisés pour les litiges liés à Google Pay sont les mêmes que ceux que les commerçants voient pour tous les modes de paiement : transactions non autorisées, article non reçu, double facturation et fraude amicale. Ce qui change avec Google Pay, c'est le degré de difficulté à contester chaque cas, et les raisons qui s'y rapportent.

Réclamations relatives à des transactions non autorisées

Une réclamation pour transaction non autorisée est déposée lorsqu'un client affirme ne pas avoir autorisé un paiement. Dans le cadre d'une transaction par carte classique, les commerçants peuvent contrer cela en vérifiant le code CVV et l'adresse. Google Pay élimine ces deux éléments du processus.

Comme Google Pay utilise la tokenisation, les informations relatives au code CVV ne peuvent pas être enregistrées et ne sont pas transmises dans les données de transaction. Les banques peuvent interpréter l'absence de vérification d'adresse et de confirmation du code CVV comme une confirmation de la fraude signalée par le client, surtout si elles ne connaissent pas bien les mesures de sécurité de Google Pay. La fonctionnalité même qui rend Google Pay sûr pour les clients est celle qui prive les commerçants de leurs preuves les plus courantes.

Article non reçu et article ne correspondant pas à la description

Ces deux motifs de réclamation sont distincts sur le plan opérationnel, mais sont souvent traités ensemble car les exigences en matière de preuves se recoupent. Les réclamations pour « article non reçu » nécessitent une preuve de livraison à la bonne adresse. Les réclamations pour « article non conforme à la description » nécessitent une preuve documentée attestant que ce que vous avez livré correspond bien à ce que vous aviez annoncé.

Ces deux aspects peuvent être gérés à condition de disposer d'une documentation adéquate. La difficulté particulière à laquelle sont confrontés les commerçants avec Google Pay réside dans le fait que l'enregistrement de la transaction contient moins d'informations d'identification qu'un paiement par carte classique. Il est donc assez difficile, lors de la procédure de présentation des preuves, de faire correspondre la confirmation de livraison à la transaction spécifique.

Frais en double

Les litiges liés à des prélèvements en double surviennent lorsqu'un client est débité plusieurs fois pour une même transaction. Ce sont généralement les cas les plus simples à résoudre, car les journaux de transactions permettent soit de confirmer, soit d'infirmer la réclamation. Pour les commerçants, le risque est davantage d'ordre opérationnel que probatoire. Les prélèvements en double résultent souvent d'échecs lors du paiement, de nouvelles tentatives de paiement ou d'erreurs d'intégration. Cela indique également l'existence d'un problème technique plus général qui mérite d'être examiné au-delà des litiges individuels.

Fraude amicale

La fraude amicale constitue le principal défi pour les portefeuilles numériques tels que Google Pay. Elle se produit lorsqu'un client effectue un achat en toute légitimité, puis demande une contestation de paiement au lieu de solliciter un remboursement.

Selon le rapport « Global Payments Report 2026 » de Ravelin, les commerçants continuent de classer Google Wallet et Apple Pay parmi les moyens de paiement les plus risqués. Ils sont désormais plus nombreux qu’auparavant à les placer dans leur top 3 des moyens de paiement les plus frauduleux, et un sur quatre les classe même parmi leurs deux premiers. Si ces portefeuilles électroniques réduisent effectivement la fraude réelle par carte absente grâce à la tokenisation et à la biométrie, ils posent un défi particulier en cas de fraude amicale.

Cette raison est directement liée à la manière dont les banques interprètent l'authentification biométrique de Google Pay. Lorsqu'une transaction est effectuée à l'aide d'un jeton de l'appareil et d'une confirmation biométrique, la banque considère cela comme une preuve solide que le titulaire du compte a autorisé le paiement. Ce même enregistrement d'authentification joue alors en défaveur du commerçant lorsqu'un litige pour fraude amicale est déposé. La banque estime en effet que si le client a authentifié la transaction, tout litige ultérieur doit refléter une défaillance du commerçant plutôt qu'une faute du client.

Les dispositifs de sécurité biométriques n'empêchent pas la fraude amicale. Ils compliquent simplement la tâche des commerçants lorsqu'il s'agit de prouver qu'elle a bien eu lieu.

Comment éviter les litiges liés à Google Pay

L'une des principales leçons que le secteur des paiements a tirées de l'année dernière est que la prévention des rétrofacturations s'avère plus rentable que la contestation. Il existe d'ailleurs des stratégies faciles à mettre en œuvre pour réduire au minimum les litiges liés à Google Pay sans nuire aux conversions. Le cadre présenté ci-dessous suit chronologiquement le cycle de vie d'un litige, de la configuration de la transaction au comportement post-achat, de sorte que chaque recommandation de prévention cible une période de risque bien définie.

Commencez par la configuration du transfert de responsabilité

Il s'agit là de la mesure de protection la plus importante avant la transaction que la plupart des commerçants négligent. Mastercard transfère automatiquement la responsabilité des transactions éligibles utilisant un jeton de dispositif. Visa vous demande d'activer manuellement la protection contre la responsabilité en cas de fraude pour le jeton de dispositif Visa dans la console Google Pay.

Si cette option n'est pas activée, vous supportez les pertes qui incombent à la banque émettrice. Remarque : le transfert de responsabilité protège les revenus liés à chaque transaction, mais n'a pas d'incidence sur votre taux global de rétrofacturation.

Sachez quel type de transaction vous traitez

Google Pay utilise deux types de jetons présentant des profils de risque très différents :

- CRYPTOGRAM_3DS : jeton lié à un appareil avec transfert automatique de responsabilité.

- PAN_ONLY : pas d'association à un appareil, risque accru, pas de transfert de responsabilité sauf si vous activez 3D Secure.

Consultez vos rapports PSP pour identifier le jeton qui représente la majeure partie de votre volume et configurez, dans la mesure du possible, des transactions PAN_ONLY vers 3DS.

Inscrivez-vous à Order Insight et Consumer Clarity

Ces deux programmes interviennent au stade préalable au litige, où la prévention s'avère la plus rentable. Order Insight fournit des données sur les transactions aux émetteurs Visa lorsqu'un titulaire de carte conteste un prélèvement. Il permet à la banque émettrice d'extraire des informations détaillées sur la commande, notamment le nom du produit, la description de la transaction, l'adresse de livraison et l'enseigne du commerçant, avant qu'un rejet de débit ne soit déposé. Consumer Clarity remplit la même fonction au sein de l'écosystème Mastercard.

Étant donné que chaque solution est spécifique à un réseau et n'est pas interchangeable, il est recommandé d'activer les deux afin de garantir que les titulaires de carte aient accès aux informations relatives à la transaction, quel que soit le réseau qui traite le paiement.

Mettez en place des alertes de rétrofacturation pour prévenir les litiges dès leur apparition

Les alertes vous informent dans un délai de 24 à 72 heures lorsqu'un client conteste un paiement auprès de sa banque. Cela vous laisse le temps d'effectuer un remboursement et de neutraliser le rejet de débit imminent avant qu'il n'apparaisse sur votre tableau de bord.

Chargeflow est une plateforme de gestion des rétrofacturations de bout en bout couvrant toutes les étapes du cycle de traitement des litiges, depuis l’interception et la prévention jusqu’au recouvrement automatisé et au suivi centralisé. Son produit « Alerts » combine les solutions Ethoca (Mastercard) et Verifi Rapid Dispute Resolution (Visa) pour rembourser automatiquement les transactions problématiques avant qu’elles ne donnent lieu à des rétrofacturations. Les commerçants utilisant ces deux réseaux constatent régulièrement une baisse significative du volume de rétrofacturations.

Utilisez Chargeflow pour lutter contre la fraude après-vente

Les outils anti-fraude classiques se contentent d'analyser les transactions au moment du paiement. Grâce à l'authentification renforcée de Google Pay, les commandes semblent légitimes même en cas de fraude amicale.

L'authentification biométrique renforcée de Google Pay (empreinte digitale, Face ID ou code PIN), associée à des jetons liés à l'appareil, génère un cryptogramme qui prouve que le titulaire légitime de la carte a autorisé la transaction lors du paiement. Par conséquent, les outils standard de détection des fraudes au prépaiement la considèrent comme parfaitement irréprochable et à faible risque. Pourtant, ce même client pourrait être un fraudeur « amical » récidiviste qui contesterait la transaction par la suite, exposant ainsi le commerçant à des risques.

Chargeflow intervient entre le moment du paiement et celui de l'exécution de la commande. Grâce à l'apprentissage automatique et à un réseau mondial de commerçants, il signale en temps réel les commandes à haut risque, ce qui vous permet de bloquer ou de gérer les cas de fraude amicale avant l'expédition. Dans la plupart des cas, les acheteurs signalés renoncent à leur réclamation.

Modifier le libellé de votre facture

C'est le point de contact qui demande le moins d'efforts, mais qui offre le meilleur rendement. Si votre nom commercial ne correspond pas clairement au nom de votre boutique, les clients contestent le paiement simplement parce que le montant ne leur semble pas familier sur leur relevé.

Testez-le avec différentes marques de cartes et corrigez tout problème de troncature ou de non-correspondance.

Préparez la documentation avant que les litiges ne surviennent

Dans le cadre des litiges liés à Google Pay, tout se joue lors de la collecte des preuves, et non lors de leur récupération. Considérez chaque transaction comme un litige potentiel dès qu’elle est validée.

Cela peut s'avérer difficile à gérer manuellement. L'automatisation des litiges enregistre automatiquement les livraisons suivies par le transporteur et associées à la commande, conserve toutes les communications avec le client et consigne l'acceptation des conditions générales du magasin lors du paiement. C'est exactement ce dont Google a besoin pour vous aider lors de la procédure de réclamation.

Comment contester et gagner un litige Google Pay en toute simplicité

Si vous perdez vos litiges Google Pay, ce n’est pas parce que vous manquez de preuves. Vous en produisez déjà en abondance. Le véritable problème tient probablement au fait que vous gérez ces litiges manuellement ou à l’aide de systèmes biaisés, au sein d’un cadre hautement automatisé conçu pour favoriser les titulaires de carte et épuiser les commerçants.

Le taux de réussite moyen du secteur en matière de gestion manuelle des litiges est de 12 %. Chargeflow , les commerçants obtiennent un taux de réussite de 75 % ou plus. Ce n’est pas parce qu’ils travaillent plus dur. L’IA Chargeflow accomplit en quelques secondes ce qui prend des heures à un commerçant. Elle récupère le litige, extrait des éléments de preuve à partir de centaines de points de données, calcule la probabilité de succès grâce à son système propriétaire, élabore une réponse structurée et la soumet avant l’expiration du délai.

En quelques mois seulement, Fanatics a récupéré plus de 800 000 dollars de recettes contestées et a plus que doublé son taux de réussite après avoir adopté Chargeflow. L'entreprise n'a pas eu besoin de recruter une équipe dédiée à la lutte contre la fraude. Elle a simplement intégré une plateforme conçue pour transformer le processus de traitement des litiges, autrefois un véritable cauchemar, en un système entièrement automatisé offrant un taux de réussite élevé.

Voici ce que dit Fanatics :

Commencez dès maintenant à récupérer vos montants contestés via Google Pay.

Comment vérifier l'état d'un litige Google Pay

Google Pay ne propose pas de tableau de bord pour les commerçants permettant de suivre en temps réel l'état d'avancement des litiges. Dans l'écosystème Google Pay, les mises à jour de statut sont diffusées par deux canaux principaux :

1) Notifications directes par e-mail: Google vous informe généralement des litiges via l'adresse e-mail associée à votre Centre de paiement Google. Il s'agit souvent d'alertes ponctuelles. Il n'existe pas de portail en temps réel permettant de suivre l'évolution d'un dossier entre la notification initiale et la décision finale.

2) Le tableau de bord de votre prestataire de paiement: Google Pay s'appuyant sur les infrastructures de paiement par carte classiques, c'est votre prestataire de paiement (par exemple, Stripe, Adyen ou Braintree) qui fait office de « source de référence » en cas de litige. C'est là que vous trouverez les délais exacts, les codes de motif et le portail permettant de fournir des justificatifs.

Le problème de la visibilité

Le principal défi pour les commerçants traitant un volume important de transactions réside dans la fragmentation. Si vous faites appel à plusieurs prestataires de services de paiement, vous ne disposez pas d'une vue d'ensemble unique pour suivre les litiges liés à Google Pay. Cela peut entraîner des délais non respectés et une perte de revenus.

La solution : Chargeflow

Chargeflow résout ce problème en regroupant les données relatives aux litiges provenant de tous vos prestataires de paiement connectés au sein d'une vue unique et centralisée. Au lieu de courir après les e-mails ou de passer d'un compte de prestataire à l'autre, vous bénéficiez d'alertes et d'analyses en temps réel sur l'ensemble des activités liées aux litiges. Cette visibilité fait toute la différence entre un processus réactif et un processus maîtrisé.

Litige Google Pay ou rejet de débit : ce que les commerçants doivent savoir

Les termes « litige » et « rejet de paiement » sont utilisés de manière interchangeable tout au long de ce guide, car, dans la plupart des cas concernant Google Pay, ils désignent le même événement. Cependant, il s'agit techniquement d'étapes distinctes d'un processus qui peut prendre une ampleur bien plus grande que ne le pensent la plupart des commerçants, et cette distinction revêt une importance considérable à mesure que le dossier avance.

Une contestation est la première réclamation déposée par le client auprès de sa banque émettrice. Un rejet de débit est l'annulation financière officielle qui s'ensuit si la banque donne raison au client. Cette distinction est importante, car les alertes de rejet de débit se déclenchent dès la phase de contestation, avant que le rejet de débit ne soit officiellement enregistré. Cette période constitue votre meilleure chance de résoudre le problème à moindre coût avant qu'il n'ait des répercussions négatives sur votre compte.

Une fois qu'un rejet de débit est déposé, la procédure suit un parcours qui va du rejet de débit à la nouvelle présentation, puis à la phase de pré-arbitrage et enfin à l'arbitrage. L'arbitrage marque une étape décisive. Toutes les décisions prises à ce stade sont définitives, et demander à Visa de reconsidérer une décision implique des frais supplémentaires d'environ 1 000 $ ainsi que la présentation de nouveaux éléments de preuve extrêmement convaincants. La plupart des cas ne devraient jamais en arriver là. Si c'est le cas, c'est qu'une étape a échoué plus tôt dans la procédure.

🔥Point clé : chaque litige Google Pay est pris en compte dans votre taux de rejet de paiement dès qu'il est déposé, que vous obteniez gain de cause ou non. Si leur nombre est suffisamment élevé, vous serez soumis au programme de surveillance VAMP de Visa. À ce stade, la question ne porte plus sur les litiges individuels, mais sur votre capacité à continuer à traiter des paiements.

Que se passe-t- contestation Google Pay ?

Le fait de perdre un litige Google Pay entraîne des conséquences à trois niveaux, mais la plupart des commerçants n'en tiennent compte que pour le premier.

Les répercussions financières immédiates

Lorsqu'un litige est retenu, le montant de la transaction et les frais de rejet de débit associés sont définitivement débités de votre compte. Plus vous accumulez de rejets de débit, plus les coûts ont tendance à augmenter.

Vous devez également prendre en charge tous les frais liés à la gestion des commandes, tels que les frais d'expédition, la gestion des stocks et la main-d'œuvre, sans rien pour les compenser. C'est pourquoi un rejet de paiement d'un dollar coûte plus de trois fois plus cher.

La conséquence du rapport

Chaque litige perdu fait grimper votre taux de rétrofacturation. Dans le cadre du programme VAMP de Visa, désormais pleinement opérationnel, ce taux correspond à la somme de tous les litiges (qu'ils soient liés à une fraude ou non) divisée par le nombre total de transactions réglées.

Le dépassement du seuil fixé peut entraîner l'obligation de constituer des réserves sur le compte, des frais supplémentaires par litige ou la résiliation du compte. Les règles de Mastercard sont encore plus strictes. Le programme « Excessive Chargeback » de Mastercard signale les commerçants dont le taux de rejet de débit atteint 1 % et qui enregistrent au moins 100 rejets de débit par mois au niveau standard.

Le risque lié au compte

Des taux de rétrofacturation élevés entraînent la résiliation du compte et l'inscription sur la liste MATCH, une liste noire qui empêche les commerçants d'accéder à de futurs services de paiement. Cela les prive de fait de la possibilité de traiter des paiements.

C'est cela qui mène à la faillite des entreprises. Ce ne sont pas les pertes ponctuelles qui sont en cause, mais les dommages cumulés résultant de pertes non maîtrisées au fil du temps.

Conclusions sur le litige concernant Google Pay

Si vous lisez ce guide, c'est sans doute parce que vous acceptez déjà Google Pay. La question n'a jamais été de savoir s'il fallait l'accepter. Il s'agit plutôt de déterminer si la manière dont vous gérez actuellement les litiges vous coûte plus cher que vous ne le pensez.

Les commerçants qui subissent le plus de pertes échouent parce qu’ils appliquent une approche classique en matière de rétrofacturation à un mode de paiement qui nécessite une approche différente. Le manque de preuves engendré par la tokenisation, le paradoxe de l’authentification biométrique qui favorise la fraude amicale, les délais raccourcis, l’absence d’un centre de résolution interne opérationnel… rien de tout cela n’est insurmontable.

Mais cela nécessite un ensemble de configurations, d'outils et de processus spécifiques qui, soit sont déjà en place dans votre infrastructure avant qu'un litige ne soit déposé, soit n'existent tout simplement pas. Le transfert de responsabilité est soit activé, soit désactivé. La documentation est soit enregistrée au moment de la transaction, soit recherchée à la hâte après coup. Les alertes permettent soit d'intercepter les litiges avant qu'ils ne soient officiellement déposés, soit vous n'en apprenez l'existence qu'à travers un e-mail indiquant un délai déjà en cours.

Ce sont là autant de lacunes que la gestion manuelle des litiges laisse subsister. Comblez-les, et la donne change. C'est précisément pour cela que Chargeflow conçu.

Si vous acceptez les paiements via Google Pay, il est temps d'automatiser le traitement de vos litiges et de combler les failles qui vous font perdre de l'argent.

Commencez dès aujourd'hui à récupérer vos pertes liées aux rétrofacturations.

Puis-je contester un paiement effectué via Google Pay ?

Oui, vous pouvez signaler ou contester une transaction Google Pay via les outils d'assistance de Google Pay ou auprès de l'émetteur de votre carte, car Google Pay achemine les paiements via les réseaux de cartes classiques.

Comment puis-je contacter Google pour contester des frais ?

Vous pouvez ouvrir un litige via le site d'assistance de Google Pay ou via l'outil « Transactions non autorisées », qui transmet la réclamation à l'émetteur de la carte ou au réseau concerné.

Puis-je obtenir un remboursement via Google Pay ?

Un remboursement est possible si le litige est tranché en votre faveur, soit directement par le commerçant, soit par le biais d'un rejet de débit effectué par le réseau de cartes et traité par votre banque émettrice.

Réglez automatiquement vos litiges Google Pay

Vous pouvez consolider vos justificatifs et les envoyer dans les délais, sans avoir à suivre manuellement les échéances de Google Pay. Chargeflow le processus de bout en bout, avec une garantie de retour sur investissement multiplié par 4.

Commencez gratuitementDes rétrofacturations ?

Ce n'est plus votre problème.

Récupérez 4 fois plus de rétrofacturations et prévenez jusqu’à 90 % de celles à venir, grâce à l’IA et à un réseau mondial de 20 000 commerçants.

.png)