%201.svg)

Venmo Chargebacks Explained: How They Work, Reason Codes, and Merchant Protection

Contracargos?

Ya no es tu problema.

Recupera cuatro veces más Contracargos prevención el 90 % de los que se producen, gracias a IA a una red global de 20 000 comercios.

El sistema de reclamaciones de Venmo funciona en dos vías distintas: las reclamaciones internas de Venmo y Contracargos de las redes de tarjetas, cada una con sus propias normas, plazos y responsables de la toma de decisiones. La mayoría Contracargos como un hecho consumado: los fondos ya han sido recuperados y el plazo para responder es muy breve. Para ganar, es necesario disponer de documentación preparada antes de la disputa, no recopilada a toda prisa después. La prevención se basa en políticas claras, reembolsos sencillos y la supervisión de patrones. Eso es lo que evita que un problema gestionable se convierta en uno sistémico.

Venmo se creó para realizar transferencias entre particulares, como dividir cuentas, devolver dinero a amigos y transferir fondos sin las complicaciones de los bancos. Esa premisa inicial marcó todas las decisiones de diseño: contrapartes de confianza, sin intercambio de bienes y sin necesidad de recibos.

Desde entonces, la plataforma se ha convertido en un importante canal de pagos comerciales. Venmo ha adoptado algunas medidas para adaptarse a ese cambio mediante la «Protección de compras», la categoría «Bienes y servicios» y la intermediación en las devoluciones. Sin embargo, esas medidas se limitaban a un ámbito muy reducido de la actividad comercial (bienes físicos, transacciones presenciales, perfiles empresariales consolidados), lo que dejaba sin protección significativa importantes categorías de uso por parte de los comerciantes, en particular los bienes y servicios digitales.

La diferencia es más acusada en el caso de los bienes y servicios digitales. La Protección de Compras excluye explícitamente los bienes intangibles, por lo que clasificar una transacción como «Bienes y servicios» conlleva un riesgo de devolución sin ofrecer la protección que esa etiqueta implica.

Cuando un usuario presenta una devolución de cargo en Venmo, la primera notificación que se suele recibir es una retención de fondos, la pérdida de los mismos, la asignación de un código de motivo y un plazo breve para responder. No hay visibilidad previa a la disputa y las vías de recurso son limitadas. Esta guía explica qué ocurre en cada fase y cómo prepararse antes de la próxima devolución de cargo.

Entender Contracargos de Venmo: ¿disputa o devolución?

Una devolución de cargo en Venmo es la anulación de una transacción con tarjeta de crédito o débito que se inicia cuando un consumidor presenta una reclamación ante su banco emisor por una transacción realizada en Venmo y financiada con su tarjeta. Las reclamaciones de Venmo se presentan exclusivamente a través de la plataforma de Venmo y se gestionan según el marco interno de resolución de Venmo.

Las dos vías de recurso se diferencian en función de la fuente de financiación y de quién toma la decisión. Esa distinción determina directamente tu exposición y tus posibilidades de recurso. A continuación te ofrecemos un breve resumen de los dos protocolos:

Conflictos dentro de Venmo (en la propia plataforma)

Las disputas de Venmo son resueltas por Venmo en el marco de su programa de Protección de Compras. Este se aplica a las transacciones realizadas a través de un perfil empresarial que cumplan los requisitos o a los pagos etiquetados explícitamente como «Bienes y servicios». Si Venmo falla a favor del comprador, el importe se revertirá desde tu saldo de Venmo. No se aplican las comisiones por devolución de la red de la tarjeta, a menos que el comprador también presente una reclamación ante el emisor de su tarjeta, lo cual el proceso interno de resolución de disputas no prevención.

Contracargos de emisores de tarjetas Contracargos fuera de la plataforma)

Una devolución de cargo iniciada a través del banco del titular de la tarjeta elude el proceso interno de resolución de disputas de Venmo y se remite directamente al emisor de la tarjeta de crédito o débito correspondiente (por ejemplo, Chase, AmEx u otro banco). Es importante destacar que esta vía solo está disponible para pagos realizados con tarjeta de crédito o débito, no para pagos con el saldo de Venmo ni para transferencias directas desde una cuenta bancaria. Las normas de la red de la tarjeta prevalecen por completo sobre el marco de Venmo. Venmo remite tus pruebas, pero no decide el resultado. Se aplicarán las comisiones estándar de devolución de la red si el banco falla en tu contra.

La siguiente tabla muestra la comparación operativa entre Contracargos de Venmo Contracargos las «disputas» de Venmo:

El marco jurídico de Contracargos de Venmo

La fuente de financiación determina qué régimen normativo se aplica y, por lo tanto, quién asume la pérdida. Pero antes incluso de que se aplique ese análisis, hay una condición previa: si el vendedor cuenta con un perfil empresarial de Venmo verificado.

Sin él, ni la Protección de compras ni el marco de Bienes y Servicios funcionan a favor del vendedor. La devolución de la red de tarjetas sigue produciéndose, Venmo sigue remitiendo tus pruebas, pero la intermediación interna de la plataforma —el aspecto que ofrece a los vendedores cualificados una vía de respuesta estructurada— no está disponible. Estás asumiendo todo el riesgo de una disputa con la red de tarjetas sin el respaldo procedimental del que disponen los vendedores con Perfil Empresarial. Si actualmente aceptas pagos comerciales en una cuenta personal de Venmo, crear un Perfil Empresarial antes de tu próxima disputa es la solución estructural más eficaz de la que dispones.

En el caso de los vendedores que sí disponen de un perfil empresarial, la fuente de financiación determina todo lo que viene a continuación:

- Los pagos realizados con tarjeta de crédito se rigen por la FCBA y el Reglamento Z. La responsabilidad recae, por defecto, en el emisor, que se resarcirá a través de la red de la tarjeta. Tu exposición es la misma que en cualquier devolución estándar por transacción sin presencia física de la tarjeta.

- Los pagos con tarjeta de débito o financiados mediante cuenta bancaria se rigen por la EFTA y el Reglamento E. La principal consecuencia para los comerciantes es que las reclamaciones en virtud del Reglamento E se limitan estrictamente al acceso no autorizado y a los errores de procesamiento, y no abarcan las reclamaciones por «arrepentimiento del comprador». La carga de la prueba sigue recayendo sobre usted, pero el resultado es menos predecible que en el caso de una devolución de cargo de una red de tarjetas, ya que tanto Venmo como el banco investigan de forma independiente.

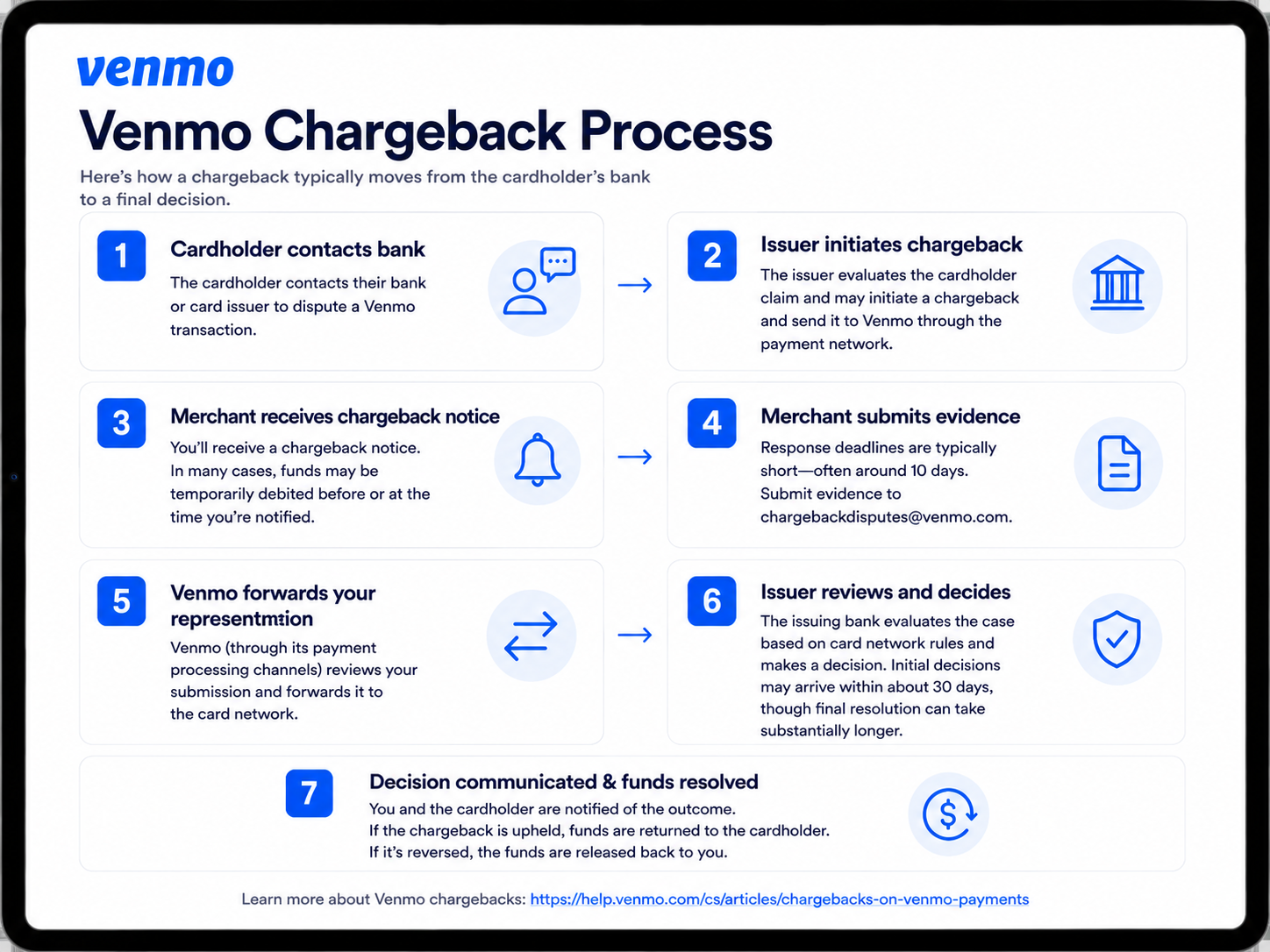

Cómo funciona el proceso de devolución de cargo y de reclamación de Venmo

Las dos vías se separan nada más comenzar, y eso determina todo lo que viene a continuación.

En lo que respecta a las devoluciones, normalmente no se ve cómo empieza el proceso; uno se entera cuando se recuperan los fondos o cuando aparece un aviso de devolución.

El titular de la tarjeta llama a su banco y este emite una anulación con código de motivo (si considera que el caso está justificado). Los fondos se retiran de tu saldo de Venmo antes de que se te notifique. La primera señal suele ser un saldo negativo o un aviso de Venmo en el que se te indica que envíes pruebas a chargebackdisputes@venmo.com. A partir de ese momento, dispones de entre 10 y 20 días para aceptar o impugnar el caso. Como tu adquirente, Venmo remite tu solicitud a la red de la tarjeta, y el banco emisor emite una resolución en un plazo de entre 30 y 75 días.

Las comisiones de procesamiento de todos Contracargos reembolsables, independientemente del resultado. Más información sobre las comisiones por contracargos.

En el proceso de resolución de disputas internas, Venmo te notifica la situación e inicia una revisión. Tienes unos 10 días para responder aportando pruebas. Si Venmo falla a favor del comprador, primero deduce el importe de tu saldo de Venmo. Si este no es suficiente, realiza un cargo en tu cuenta bancaria vinculada. Aunque no se aplican comisiones de las redes de tarjetas, es posible que se apliquen restricciones a la cuenta o que se bloquee el saldo durante y después de la revisión.

La carga de la prueba es similar en ambas vías. Lo que difiere es el plazo, el árbitro y los costes posteriores en caso de perder.

Códigos de motivo de devolución en Venmo y lo que debes saber sobre ellos

Contracargos Venmo Contracargos dos taxonomías de códigos distintas en función de la vía que siga la reclamación (es decir, Contracargos la red de tarjetas Contracargos reclamaciones internas de Venmo), y cada una de ellas conlleva una señal de diagnóstico diferente.

Contracargos de Venmo iniciados por el banco: códigos de red estándar

Contracargos de las redes de tarjetas Contracargos con códigos de motivo estándar, que Venmo recibe y reenvía sin modificaciones. Hemos explicado en detalle los distintos códigos de motivo de las redes de tarjetas. Para obtener más información, consulta los siguientes directorios de códigos de motivo:

- Códigos de motivo de devolución de cargos de Visa

- Códigos de motivo de devolución de Mastercard

- Descubre los códigos de motivo de las devoluciones

- Códigos de motivo de devolución de American Express

Venmo: Conflictos internos: «códigos no oficiales» descriptivos

Las disputas internas no generan códigos de motivo como los numéricos de las redes de tarjetas. En su lugar, la interfaz de Venmo pide al usuario que elija una etiqueta como «No autoricé este pago», «Me han estafado» o «El artículo no ha llegado».

Se trata de etiquetas semiestructuradas, no de códigos formales de cuatro dígitos, pero funcionan como «señales de riesgo» internas que orientan la revisión de Venmo:

- «Uso no autorizado/cuenta pirateada» significa que Venmo se inclinará por la anulación de la transacción si hay algún indicio de que la cuenta ha sido comprometida o de que no se han seguido las medidas de seguridad adecuadas al iniciar sesión.

- En el caso de «Estafa/no he recibido el artículo», Venmo podría tener en cuenta la prueba de entrega, la comunicación y el comportamiento de la cuenta.

Los códigos de devolución de Venmo más utilizados indebidamente

En el contexto de Venmo, hay dos categorías de códigos de motivo de devolución de cargo que se utilizan de forma desproporcionada:

1. Cargos no recibidos y no contabilizados

Estos son los motivos habituales por los que los compradores se arrepienten de sus transacciones. Los casos de «no recepción» y los cargos no reconocidos se producen de tres formas. La primera es un fraude amistoso en toda regla: un comprador paga en la categoría «Bienes y servicios», recibe el pedido y, aun así, presenta una reclamación por «no recepción».

En segundo lugar, un comprador presiona al vendedor para que acepte una transferencia personal con el fin de eludir la comisión por bienes y servicios y, a continuación, reclama ante su banco el cargo en la tarjeta correspondiente alegando que no está autorizado. El banco solo ve un cargo en la tarjeta a nombre de Venmo, sin saber cómo se ha clasificado internamente.

El tercero es la apropiación real de la cuenta, en la que las credenciales robadas se utilizan para financiar una transacción que el titular legítimo de la tarjeta impugna posteriormente. Los dos primeros casos son de carácter conductual; el tercero es un fallo de seguridad previo a la transacción que no se puede resolver únicamente con pruebas.

2. Fraude y uso no autorizado

El fraude y los códigos no autorizados se dividen en dos situaciones que parecen idénticas en el libro mayor, pero que tienen consecuencias opuestas para los comerciantes.

El primero es la apropiación real de la cuenta. Las credenciales robadas se utilizan para financiar una compra; el titular legítimo de la tarjeta la impugna. En este caso, la devolución es válida. El titular de la tarjeta realmente no autorizó nada. Se trata de un problema previo a la transacción.

El segundo es el fraude por devolución de cargo. El comprador realiza la transacción de forma voluntaria, recibe los bienes o el servicio y, a continuación, invoca el código de «no autorizado» para rechazar la transacción. En este caso, las pruebas sí que importan. Los registros de comunicación, la confirmación de entrega y una transacción de «Bienes y Servicios» correctamente etiquetada son argumentos que contradicen la versión del comprador.

La implicación práctica es que, cuando recibes un código de fraude o no autorizado, la primera pregunta no es «¿qué pruebas debo presentar?», sino más bien «¿en qué situación me encuentro realmente?». Una serie de códigos de fraude en pedidos con señales inusuales en la cuenta apunta a una apropiación de la cuenta. Una serie de códigos en transacciones que, por lo demás, son normales y proceden de cuentas consolidadas apunta a un fraude de personas de confianza. La respuesta y las posibilidades reales de ganar difieren sustancialmente entre ambos casos.

Cómo preparar una defensa ante una devolución de pago en Venmo: pruebas que realmente dan resultado

Si abordas una devolución de pago de Venmo como si fuera cualquier otra disputa, eso podría estar perjudicando tus índices de éxito. ¿Por qué? Ese enfoque no da resultado porque las pruebas no están expresadas en el idioma adecuado.

Contracargos de Venmo Contracargos son revisadas por Venmo. Ya lo sabes. Se tramitan a través de la red de tarjetas hasta llegar a Visa, Mastercard, Discover o Amex. Están vinculadas al método de pago que haya utilizado el comprador. Por lo tanto, tu reclamación llega a manos de un analista bancario que sigue los códigos de motivo específicos de la red, y no a un agente de atención al cliente de Venmo que pueda ver el historial de la transacción. Esa distinción debería influir en cómo elaboras tu defensa.

Qué buscan los evaluadores de devoluciones y cómo satisfacer esa demanda

Los analistas de devoluciones (o, más bien, los sistemas tecnológicos que han implantado) buscan una explicación coherente que coincida con los patrones detectados. No un montón de capturas de pantalla.

Cada prueba que presentes debe responder a una de estas tres preguntas: ¿Se realizó la transacción con la autorización del comprador? ¿Se entregó el producto o servicio tal y como se describía? ¿Tuvo el comprador una oportunidad razonable para resolver el asunto antes de llevarlo a un nivel superior?

Tu documentación debe reflejar la secuencia de hechos de la forma más clara posible si quieres ganar Contracargos facilidad Contracargos de Venmo.

La jerarquía de la evidencia

No todas las pruebas tienen el mismo peso. Clasifica tus pruebas en este orden antes de presentar nada:

Mayor peso: confirmaciones de entrega firmadas, envíos con seguimiento y marcas de tiempo de entrega, y cualquier comunicación por escrito (mensaje de texto, correo electrónico, mensaje en la aplicación) en la que el comprador haya acusado recibo o expresado su satisfacción. Un mensaje de texto del comprador en el que diga «paquete recibido, gracias» tras una transacción ha resuelto más disputas de las que jamás resolverá ninguna factura.

Elementos de gran peso: confirmaciones de pedido con detalles detallados, fotos o vídeos del artículo antes del envío, y contratos de servicio con un alcance claramente definido. En el caso de los productos o servicios digitales, los registros de acceso que demuestran que el comprador ha utilizado lo que ha adquirido son especialmente convincentes.

Pruebas de respaldo: registros de transacciones, tu propio historial interno de pedidos y registros de comunicación que demuestren que intentaste resolver el problema directamente. Estas pruebas rara vez bastan por sí solas para ganar un caso, pero sirven para completar la información y demostrar que actuaste de buena fe.

Peso mínimo: Capturas de pantalla del pago de Venmo únicamente. Todos los comerciantes lo presentan. Esto demuestra que se ha transferido el dinero, no que hayas realizado la entrega.

El momento en que ocurre algo es, en sí mismo, una prueba

Las redes de devoluciones tienen plazos de respuesta estrictos. Presentar una respuesta completa y bien organizada el segundo día transmite algo que una respuesta apresurada de última hora no transmite: que gestionas tu negocio con orden y rigor. Los analistas detectan patrones en miles de disputas. Un comerciante que responde con rapidez y con documentación estructurada transmite implícitamente una imagen más creíble que aquel que, claramente, ha tenido que rebuscar entre el papeleo bajo presión.

Aquí es donde contar con un proceso sistemático ofrece ventajas que van más allá de un caso concreto. Los comerciantes que utilizan Chargeflow, por ejemplo, no solo responden más rápido. La plataforma estructura los expedientes de pruebas tal y como las redes de tarjetas esperan recibirlos, lo que reduce la discrepancia entre lo que tú sabes que ocurrió y lo que el revisor puede realmente tener en cuenta. Descubre cómo TruHeight, cliente de Chargeflow, eliminó más de 1.519 horas de trabajo manual dedicado a la gestión de disputas, al tiempo que recuperó 112.617 dólares en ingresos objeto de disputa.

Qué no debes seguir enviando

Las páginas con condiciones generales de uso no demuestran que el comprador las haya aceptado. Capturas de pantalla sin marca de tiempo ni contexto visible. Réplicas escritas con tono de frustración en las que se afirma que el comprador miente, en lugar de demostrar lo que realmente ocurrió. Las emociones no convencen a los analistas; la documentación sí.

Protección contra devoluciones de Venmo: cómo prevención Contracargos prevención Contracargos se produzcan

La tendencia más clara que se perfila para los comerciantes es que la prevención de las devoluciones es una estrategia empresarial. Los costes y el volumen de las disputas están aumentando. Y para los comerciantes que aceptan pagos a través de Venmo, sea cual sea el volumen, cualquier devolución repercute directamente en los resultados: en tiempo, en comisiones y en la tasa de devoluciones, un indicador que las redes de tarjetas vigilan más de cerca de lo que la mayoría de los comerciantes cree.

A continuación te explicamos cómo reducir el riesgo de recibir Contracargos falsos y fraudulentos Contracargos se produzcan:

Establece las expectativas antes de que se produzca cualquier movimiento de dinero

La mayoría de Contracargos en Venmo Contracargos no son un fraude en sí mismas tienen su origen en lo mismo: un comprador que se ha llevado una sorpresa. Una sorpresa por el plazo de entrega, por cómo era realmente el producto o por una política que no había visto. La claridad en el punto de venta es la herramienta de prevención más eficaz que existe, y su implementación no cuesta nada.

Antes de que se complete una transacción, los compradores deben saber exactamente qué van a recibir, cuándo lo recibirán y qué hacer si surge algún problema. Este último aspecto —una vía de devolución o resolución clara y sencilla— reduce las disputas más de lo que la mayoría de los comerciantes esperan. Los compradores que saben cómo ponerse en contacto contigo directamente no necesitan recurrir a su banco.

Haz que tu política de devoluciones sea más sencilla que una reclamación

Esto puede parecer contradictorio para los comerciantes preocupados por el abuso de los reembolsos. Sin embargo, los datos son claros: un proceso de reembolso sencillo reduce el volumen de devoluciones. Un comprador que presenta una reclamación a través de su banco es alguien que o bien no ha podido encontrar tu vía de resolución o bien no ha confiado en ella. Cuando tu política de reembolsos es visible, sencilla y rápida, presentar una reclamación se convierte en la opción más complicada, y la mayoría de los compradores (honestos) no la elegirán.

Esto no significa aceptar todas solicitudes de reembolso solicitudes . Significa facilitar tanto la resolución legítima de los problemas que Contracargos el último recurso, en lugar de en el primero.

Estar atento a los patrones antes de que se conviertan en problemas

La prevención de devoluciones a nivel de transacción es útil. Sin embargo, es en la prevención a nivel de patrones donde realmente se mejora el rendimiento operativo.

Un producto que genera reclamaciones repetidas en torno a la misma causa te da una pista sobre cómo se está comercializando o presentando. Un segmento de compradores con una tasa de reclamaciones más elevada requiere un tratamiento diferente en el proceso de pago.

La mayoría de los comerciantes no detectan estos patrones porque gestionan las disputas una por una, de forma reactiva. Chargeflow Insights los pone de manifiesto en tu historial de transacciones, de modo que no solo resuelves disputas individuales, sino que identificas y subsanas las deficiencias que siguen generándolas. Ese cambio, de un enfoque reactivo a uno sistémico, es lo que te diferenciará de los comerciantes que se pasan la vida lidiando con disputas sin fin.

Comprende que la prevención del fraude es una disciplina

No todas las devoluciones son fruto de un malentendido. Por ejemplo, el «fraude amistoso», que es la causa de la mayoría de las disputas en eCommerce, constituye un problema real y creciente en las plataformas P2P, precisamente porque las barreras para presentar una disputa son mínimas. Se aplican las señales habituales: discrepancias entre las direcciones de facturación y de envío, importes de pedido inusualmente elevados por parte de nuevos clientes, múltiples pedidos en un breve periodo de tiempo y la presión para realizar la transacción rápidamente son señales de alerta conocidas.

Pero no te fíes únicamente de tu instinto para detectar cuándo algo no va bien. Utiliza herramientas tecnológicas diseñadas específicamente para prevención el fraudeprevención , sea cual sea la forma que adopte. El coste de rechazar un pedido sospechoso es casi siempre inferior al coste de la reclamación que se derivaría de él.

Reflexiones finales

Venmo se encuentra en una situación delicada para los comerciantes. Combina la informalidad de los pagos entre particulares con el riesgo de devoluciones propio del procesamiento tradicional de tarjetas. Esa incongruencia (aparentemente informal, pero en el fondo formal) hace que, cuando surgen, las disputas en la plataforma resulten desproporcionadamente perturbadoras.

Sin embargo, los comerciantes que obtienen mejores resultados en Venmo no tratan las disputas como problemas aislados que hay que resolver. Adquieren hábitos de documentación que simplifican la gestión de las disputas, establecen políticas de reembolso que evitan que sea necesario elevar el caso a un nivel superior y cuentan con una visibilidad operativa que permite detectar patrones antes de que se agraven.

Esa es una forma diferente de enfocar Contracargos»: no como incidentes aislados, sino como un sistema con puntos de fallo predecibles que pueden abordarse desde el principio. Si tienes pensado aceptar pagos a través de Venmo a cualquier escala, esta combinación de defensa y prevención no es algo prescindible. Es lo que evita que un problema manejable se convierta en uno sistémico.

Tampoco se han obtenido títulos PAA activos y utilizables para esta palabra clave en esta búsqueda, por lo que esta sección de preguntas frecuentes se basa en los temas del centro de ayuda de Venmo que aparecen en la IA , en lugar de en el texto literal de la PAA. La IA ya recoge más de ocho enlaces secundarios para esta consulta, incluidas dos URL de Chargeflow; reforzar los enlaces internos entre esta página y la entrada del blog que ya aparece en los resultados de búsqueda debería consolidar la autoridad y la cuota IA, en lugar de dejar que compitan entre sí.

Contracargos?

Ya no es tu problema.

Recupera cuatro veces más Contracargos prevención el 90 % de los que se producen, gracias a IA a una red global de 20 000 comercios.

.png)