%201.svg)

Guía de Revolut sobre devoluciones para comerciantes: plazos, pruebas y respuestas a las reclamaciones

Contracargos?

Ya no es tu problema.

Recupera cuatro veces más Contracargos prevención el 90 % de los que se producen, gracias a IA a una red global de 20 000 comercios.

Una devolución de Revolut es una reclamación formal presentada por un cliente de Revolut contra una transacción con tarjeta. Revolut, en su calidad de emisor de la tarjeta, impugna la transacción en nombre del cliente a través de la red de Visa o Mastercard. El plazo de respuesta de 15 días de Revolut es innegociable. Los criterios probatorios son muy específicos. Por eso muchos comerciantes pierden Contracargos , en circunstancias normales, Contracargos . Prepara el proceso de presentación de pruebas antes de que lo necesites (permisos configurados, pruebas accesibles y flujos de trabajo de respuesta listos), en lugar de tener que reconstruirlo bajo presión cuando la disputa ya está en marcha.

El proceso de devolución de cargos de Revolut se rige por las normas estándar de las redes Visa y Mastercard. Sin embargo, la forma en que esas normas te afectan depende del papel que desempeñe Revolut en la transacción.

Si tu cliente ha pagado con una tarjeta de Revolut a través de otro adquirente, Revolut es el emisor de la tarjeta. No tienes ninguna relación directa con ellos. Tu adquirente gestiona la reclamación a través de la red de la tarjeta, exactamente igual que lo haría con cualquier otro emisor de Visa o Mastercard.

Si utilizas Revolut como cuenta de comerciante, Revolut es tu entidad adquirente. Contracargos directamente en tu disputas de Revolut, y dispones de 15 días para responder. Si no lo haces, perderás automáticamente los fondos. La presentación de pruebas, la escalación y el arbitraje se gestionan a través de la interfaz de Revolut.

Las normas que rigen en ambos casos (códigos de motivo, plazos para la presentación de reclamaciones, criterios probatorios y arbitraje) son las de Visa y Mastercard, no las de Revolut.

¿Cómo funciona el proceso de devolución de Revolut?

«Presenté toda la documentación y aun así perdí». Esa frustración casi siempre se debe a un fallo en el proceso. Para evitarlo, es fundamental comprender el proceso de devolución de Revolut y conocer cuáles son los plazos, los permisos y los requisitos en materia de pruebas.

A continuación te explicamos paso a paso el proceso de devolución de Revolut:

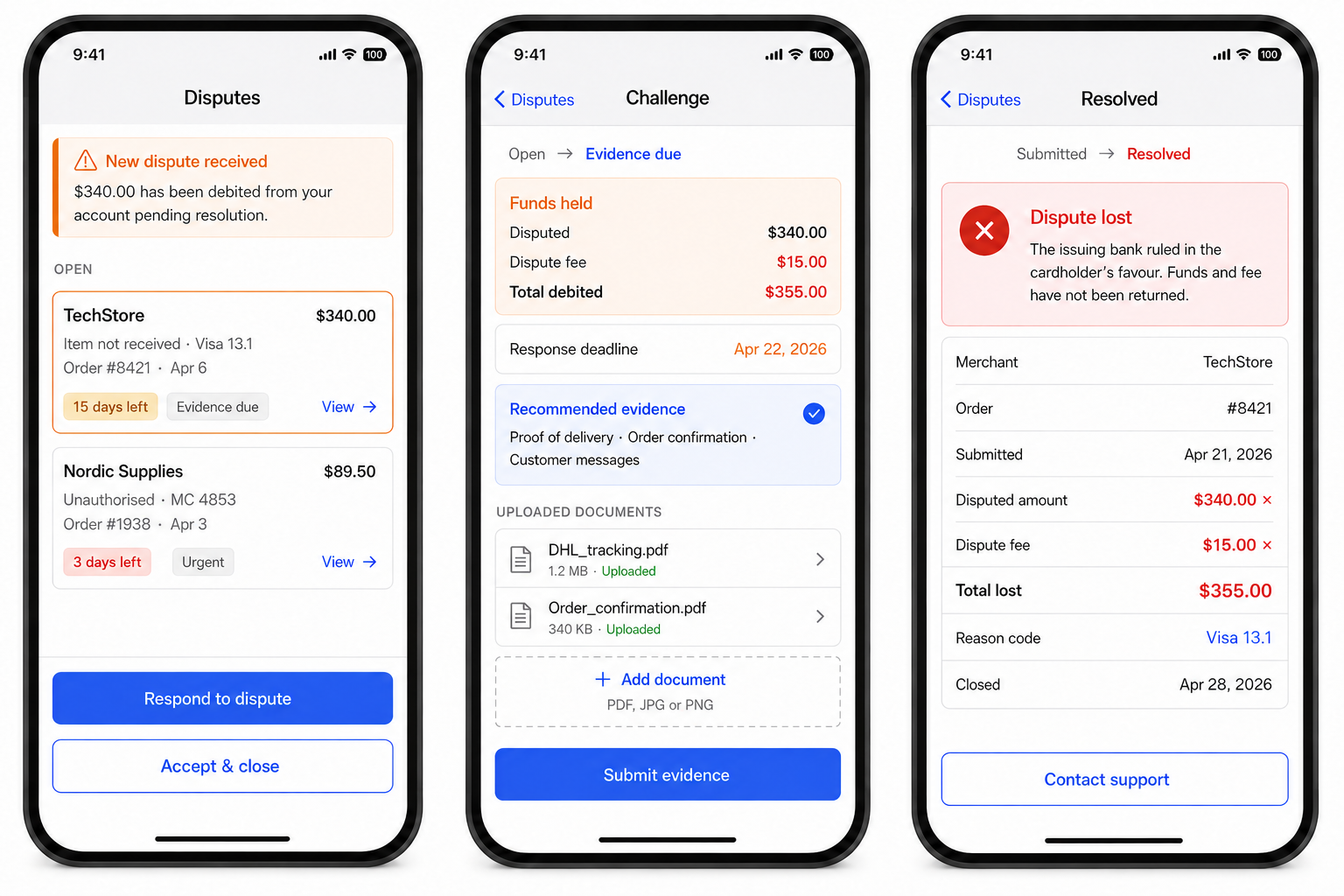

Paso 1: El titular de la tarjeta inicia una reclamación

Contracargos de Revolut Contracargos cuando tu cliente disputas transacción completada ante su banco, que a su vez la remite a Revolut a través de la red de tarjetas. Para cuando te llega, la devolución ya se ha tramitado formalmente.

¿Y si tu cliente también utiliza Revolut? Si tu cliente ha pagado con una tarjeta de Revolut, Revolut actúa tanto como emisor como adquirente. La reclamación sigue tramitándose a través de la red de la tarjeta y llega a tu disputas de la misma forma.

Paso 2: Notificación y cargo inmediato en la cuenta

Revolut carga el importe objeto de la reclamación y una comisión en tu cuenta de comerciante y retiene ambos hasta que se resuelva la reclamación. La devolución aparece en tu disputas .

Solo los miembros del equipo a los que se les haya asignado el permiso«Gestionar disputas de comerciantes» reciben notificaciones de devoluciones. Si ese punto final no está configurado correctamente, es posible que los miembros del equipo correspondientes no reciban las comunicaciones automáticas sobre devoluciones. Dado que el plazo es de 15 días y no se admiten prórrogas, una notificación no recibida supone la pérdida de la disputa.

Comprueba ahora mismo la configuración de tus permisos, no cuando surja un conflicto.

Paso 3: Tu ventana de respuesta

Revolut te concede 15 días naturales para aceptar o impugnar una reclamación. Este plazo es más corto que los plazos de 30 días de Visa y de 45 días de Mastercard. Sin embargo, cuando un adquirente establece un plazo más ajustado, ese es el plazo que debes respetar. Si no lo cumples, se considerará automáticamente una pérdida.

Paso 4: Aceptar o impugnar

Si aceptas la reclamación, los fondos retenidos se devuelven al cliente y el asunto queda zanjado. Esto tiene sentido cuando la reclamación es legítima, el importe y las comisiones no justifican el esfuerzo, o tus pruebas son realmente débiles.

Sin embargo, para impugnarla, debes presentar pruebas de impugnación a través de la disputas . El banco del titular de la tarjeta revisa tu solicitud y toma una decisión. Las pruebas deben ajustarse al código de motivo específico. La documentación genérica no es válida. Trataremos este tema en detalle en una sección posterior.

Si el banco falla a tu favor, se te devolverán tanto los fondos objeto de la reclamación como la comisión por reclamación. La mayoría de los adquirentes devuelven los fondos en caso de ganar la reclamación, pero no la comisión. Stripe, por ejemplo, se queda con ella independientemente del resultado. El hecho de que Revolut devuelva la comisión en caso de ganar es un factor diferenciador significativo.

Paso 5: Procedimiento previo al arbitraje y arbitraje

Si el banco del titular de la tarjeta rechaza tus pruebas, es posible que tengas una última oportunidad de recurrir antes de que el caso pueda pasar a arbitraje. Revolut te notificará si se llega a esa fase. El arbitraje de las devoluciones está regulado por Visa o Mastercard. Es un proceso costoso, independientemente del resultado, y solo debe iniciarse cuando el importe en litigio y la solidez de tus pruebas justifiquen el gasto. La siguiente ilustración muestra un flujo de trabajo simplificado de Revolut para las devoluciones de los comerciantes: notificación, respuesta y resultado.

¿Cuánto tarda una devolución de Revolut?

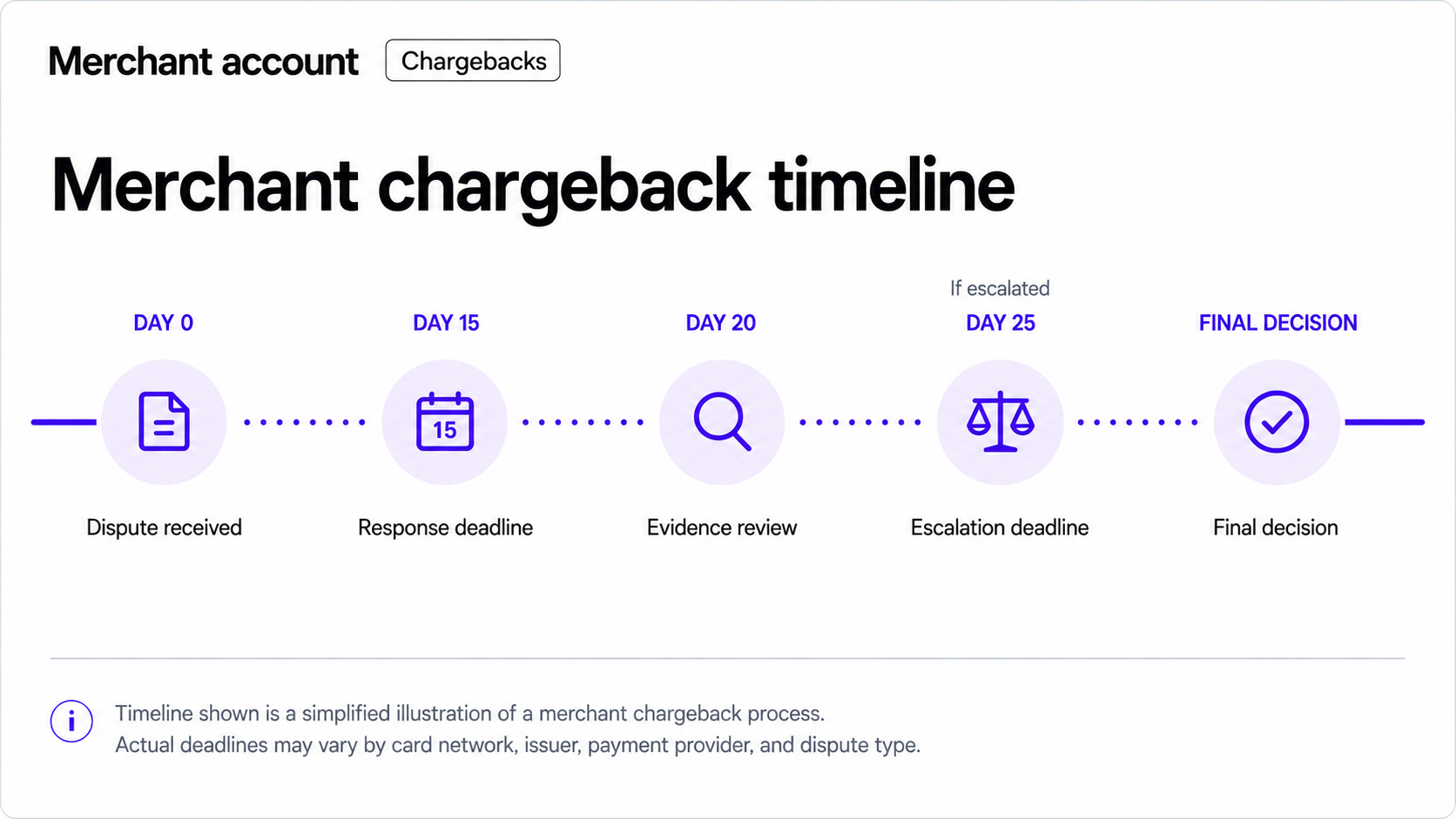

Revolut no publica un calendario detallado por etapas para los comerciantes, pero afirma que Contracargos , de media, hasta un mes. En casos excepcionales, algunos pueden prolongarse hasta un año.

Ese rango es tan amplio que, por sí solo, resulta inútil desde el punto de vista operativo, así que aquí tienes una descripción aproximada de cómo se desglosa realmente el reloj en cada etapa:

- Día 0: La disputa aparece en tu disputas

- Día 15 – Fecha límite para responder

- Día 20 – Revisión de las pruebas finalizada/Decisión sobre Revolut

- Día 25 – Plazo para la decisión sobre la escalación (en caso de que se haya planteado)

En la práctica, esto significa que un caso sencillo que se acepte o se gane sin problemas en la fase de presentación de pruebas puede resolverse en menos de un mes. Un caso impugnado que llegue a la fase previa al arbitraje o al arbitraje propiamente dicho se prolongará considerablemente más. El plazo máximo de un año es una realidad, aunque sea poco habitual.

Códigos de motivo de devolución de Revolut: qué se alega realmente en la reclamación

Revolut no emite sus propios códigos de motivo. Cada devolución de cargo viene acompañada de un código de motivo de Visa o Mastercard que define la reclamación formal del titular de la tarjeta. Ese código determina qué es lo que el banco está evaluando, qué pruebas son relevantes y si la reclamación tiene posibilidades de prosperar.

Las categorías de reclamaciones

Tanto Visa como Mastercard clasifican sus códigos de motivo en diferentes categorías. Las estructuras difieren ligeramente entre ambas redes. Sin embargo, los tipos de reclamaciones subyacentes siguen la misma lógica: fraude, fallos en la autorización, errores de procesamiento y disputas de los consumidores.

Los códigos de fraude aparecen cuando el titular de la tarjeta afirma que no ha autorizado la transacción. Esto incluye los datos de tarjetas robadas que se utilizan sin el conocimiento del titular. También puede haber casos en los que el propio titular haya realizado la compra, pero, a pesar de ello, presente una reclamación de fraude falsa. Ambos casos se registran como códigos de fraude. El código no distingue entre ellos, y es posible que el banco no investigue cuál de las dos situaciones es la verdadera.

Los códigos de autorización identifican una transacción procesada sin una autorización válida de la red de la tarjeta. También se utilizan cuando la tarjeta ha sido rechazada pero se ha cobrado de todos modos, o cuando la autorización obtenida no coincidía con el importe liquidado.

Se consideran errores de procesamiento aquellos casos en los que la propia transacción era incorrecta. Entre los ejemplos concretos se incluyen un cargo duplicado, un importe erróneo, un error de divisa o un cargo procesado después de que ya se hubiera emitido una cancelación o un reembolso.

disputas de los consumidores indican que el titular de la tarjeta autorizó el pago, pero disputas resultado. Algunos ejemplos de motivos que dan lugar a estas reclamaciones son que los productos no hayan llegado, que sean sustancialmente diferentes de lo descrito o que se haya prometido un reembolso que nunca se haya tramitado.

Hemos tratado estos códigos de motivo en profundidad en nuestra base de datos. Más información:

Éxito en las devoluciones de Revolut: ¿Qué pruebas permiten ganar disputas por devoluciones?

Perder una reclamación de devolución de cargo de la que estabas seguro de que ibas a ganar suele deberse a una de estas tres razones: pruebas que no se ajustaban al código de motivo, un formato que el banco no pudo procesar o la falta total de la prueba más sólida.

No todas las pruebas tienen el mismo peso. Para ganar, empieza por las pruebas más sólidas y directamente relevantes. Una presentación en la que la información clave se aprecia de inmediato da mejores resultados que una en la que está oculta.

Analicémoslo:

Reclamaciones por transacciones no autorizadas

La más sólida: la autenticación 3D Secure. Una autenticación 3DS satisfactoria traslada la responsabilidad por el fraude al emisor. Sin embargo, no anula los códigos no relacionados con el fraude. No obstante, en el caso de disputas por fraude evidentes, es la prueba más sólida de la que dispones.

Sólido: Los datos de coincidencia de AVS y CVV se contextualizan como parte de un patrón, junto con la coherencia del dispositivo y la dirección IP con compras anteriores, así como con transacciones anteriores realizadas con la misma tarjeta y el mismo dispositivo sin disputas previas. La entidad emisora ya dispone de los datos de AVS y CVV de la transacción original. Preséntalos como un contexto de comportamiento, no como una prueba aislada.

Por sí solo, no es suficiente: Justificante de entrega, confirmaciones de pedido, capturas de pantalla de los pedidos. Estos documentos confirman que se ha producido una transacción, pero no que el titular de la tarjeta la haya autorizado.

Reclamaciones por artículos no recibidos

La prueba más sólida: Confirmación por parte del transportista de la entrega en la dirección específica con marca de tiempo, junto con un contacto posterior a la entrega por parte del cliente, un mensaje de atención al cliente, una reseña y un pedido posterior. La confirmación de la entrega por sí sola es un indicador sólido. La confirmación de la entrega, junto con pruebas de que el cliente recibió el artículo, es un indicador considerablemente más sólido.

Destacado: Confirmación de entrega con firma para envíos de gran valor en los que se utilizó el servicio de firma. Foto de la entrega realizada por el transportista, cuando esté disponible.

Por sí solo, no es suficiente: Un número de seguimiento que indique «entregado», la confirmación de envío y los registros internos del pedido. Estos documentos demuestran que has realizado el envío, pero no que el cliente lo haya recibido.

Reclamaciones por «artículo que no se ajusta a la descripción»

Prueba más sólida: La ficha del producto tal y como aparecía en el momento de la compra (captura de pantalla con fecha o versión archivada) y cualquier comunicación previa a la compra en la que el cliente confirmara que entendía lo que estaba pidiendo. Añade la política de reembolso al finalizar la compra, si se muestra.

Convincente: Fotos o especificaciones del artículo tal y como se envió, comparadas explícitamente con la reclamación concreta del titular de la tarjeta. Haz que la comparación sea directa. No dejes que sea el revisor quien saque sus propias conclusiones.

Por sí solo, es insuficiente: Documentación interna del producto que el cliente nunca vio.

Reclamaciones por transacciones periódicas canceladas

Argumenta, basándote en pruebas, que los términos se acordaron y que el cargo era válido con arreglo a ellos, y no solo que no solicitudes recibió ninguna solicitudes de cancelación.

Más contundente: Política de cancelación tal y como se presentó en el momento de la inscripción, con pruebas de que el cliente la aceptó; correo electrónico de confirmación, registro de la casilla marcada, registro de aceptación de las condiciones. Datos de inicio de sesión o de uso que demuestren que el cliente accedió al servicio después de la supuesta fecha de cancelación.

Sólido: Historial de cancelaciones que demuestre que no solicitudes recibió ninguna solicitudes antes de la facturación, junto con un historial de pagos sin incidencias.

Por sí solo, no es suficiente: Registros de facturación internos sin pruebas de que el cliente haya aceptado las condiciones aplicables.

disputas sobre autorizaciones

Por lo general, estos casos son menos discutibles. Si el fallo en la autorización es real, es difícil ganar la reclamación. Si consideras que una reclamación por autorización es errónea, tu prueba es el código de aprobación de la red que confirma que la transacción se autorizó correctamente.

Dicho esto, también debo mencionar que evaluar todas las pruebas relacionadas con las disputas y acertar siempre es una tarea abrumadora. Tal y como ha subrayado Mastercard, el proceso de devolución de cargos es costoso y requiere mucho tiempo. Por lo tanto, no debería sorprender que incluso las entidades financieras estén pasando del procesamiento manual a un análisis respaldado por la automatización o por modelos IA.

Por qué la automatización de las devoluciones se ha convertido en la nueva normalidad

Revolut reconoce queContracargos ser un aspecto estresante a la hora de gestionar un negocio». Por eso, saber qué pruebas son las más convincentes es solo la mitad del camino. La otra mitad consiste en actuar bajo presión y dentro de plazos muy ajustados.

Ahí es donde entra en juego la automatización de las devoluciones. La gestión automatizada de las devoluciones realiza tres tareas: detecta la reclamación tan pronto como se activa la notificación, asigna el código de motivo a la jerarquía de pruebas correcta y rellena previamente la solicitud con la documentación más sólida disponible. Lo único que queda por hacer es revisarla y enviarla, en lugar de tener que reconstruirla desde cero.

Si el banco del cliente rechaza la documentación inicial que has presentado, la automatización de las devoluciones también resulta de gran ayuda en este caso. El sistema mantiene un registro estructurado de lo que se ha presentado y cuándo, lo cual es importante si el caso llega más lejos.

El marco de pruebas anterior te indica con qué debes empezar. La automatización garantiza que lo que sabes que debes presentar primero se envíe de forma correcta, completa y a tiempo. Descubre cómo The Beard Club más de 40 horas a la semana y aumentó la recuperación de ingresos gracias a la automatización:

Cómo reducir Contracargos de Revolut Contracargos se produzcan

Contracargos deberse a errores de los comerciantes, confusiones en los pagos, problemas de calidad de los productos o fraude amistoso (clientes que impugnan compras legítimas). Estos contracargos se pueden prevenir desde el principio si se gestiona adecuadamente el consentimiento, la documentación y se implementan alertas previas a las impugnaciones. A continuación te explicamos cómo:

1. Mantén tu índice de devoluciones por debajo del umbral

Las redes de tarjetas penalizan a los comerciantes cuyos índices de devoluciones superen el umbral aceptable. Una vez superado este umbral, se te clasificará como de alto riesgo, podrías tener que hacer frente a comisiones por el programa de supervisión y podrías tener que cumplir requisitos más estrictos en materia de reclamaciones por parte de Revolut.

Además de supervisar tu ratio mensualmente y actuar con rapidez si aumenta, una estrategia clave consiste en evitar de forma proactiva tramitar pedidos que puedan dar lugar a Contracargos. Herramientas como Chargeflow prevención pueden ayudarte bloqueando las transacciones procedentes de autores conocidos de fraude «amigable». Esto te permite mantener un índice de devoluciones y un estado de cuenta más saludables.

2. Entrega puntual con envío con seguimiento y justificante

prevención «mercancía no recibida» es uno de los principales motivos de contracargos. prevención dentro del plazo indicado, utilizando un servicio de envío con seguimiento que incluya los números de seguimiento facilitados por el transportista y enviando automáticamente la información de seguimiento. Considera la posibilidad de conservar las confirmaciones de entrega firmadas en el caso de artículos de gran valor. Contracargos presentarse hasta 120 días después de una entrega fallida, así que vigila este plazo.

3. Facilitar el contacto con los clientes y registrar todas las comunicaciones

Muchos Contracargos cuando los clientes no pueden ponerse en contacto contigo y recurren a Revolut. Puedes reducir este problema de la siguiente manera:

- Publicar un correo electrónico o un número de teléfono de atención al cliente que sea fácilmente visible en tu página web y en los mensajes de confirmación

- Responder a las consultas en un plazo de 24 horas

- Registrar todas las comunicaciones con los clientes y almacenarlas como pruebas en caso de litigio. La automatización de litigios se encarga de esta parte de forma automática.

Esto es fundamental, ya que Revolut exige una prueba de que el cliente intentó ponerse en contacto con el comerciante para que la devolución sea válida.

4. Tramitar rápidamente los reembolsos correspondientes a reclamaciones válidas

El fraude de buena fe puede producirse cuando los clientes se sienten en un callejón sin salida. Si la reclamación es legítima, ofrece reembolsos inmediatos sin que el cliente tenga que pasar por Revolut, mantén un registro de los números de identificación y las fechas de las transacciones de reembolso, y confirma el reembolso por correo electrónico indicando el plazo previsto. De este modo, se elimina el incentivo para solicitar una devolución.

5. Utiliza la opción «Pagar con tarjeta bancaria» de Revolut para las transacciones de alto riesgo

La función «Pagar con el banco » de Revolut (a través de su pasarela de pago) requiere que los clientes confirmen los pagos directamente con su banco, lo que:

- Hace que sea más difícil impugnar los pagos alegando que son fraudulentos.

- Reduce drásticamente el riesgo de devoluciones en comparación con los pagos con tarjeta.

Utilízalo para pedidos de alto valor, clientes nuevos y sectores de alto riesgo (suscripciones, productos digitales).

6. Utilizar las alertas de devoluciones para la resolución previa a la controversia

Las alertas de devoluciones son fundamentales, ya que te ayudan a detectar disputas antes de que lleguen a Revolut mediante la supervisión de los sistemas de Mastercard y Visa. Incluso puedes programar el sistema para que reembolse automáticamente determinadas transacciones, lo que detiene el proceso en la fase previa a la disputa. Esto reduce el número de disputas que recibe disputas y protege tu índice de devoluciones.

Conclusión

Contracargos Revolut Contracargos las normas de Visa y Mastercard. Lo que varía es la forma en que esas normas te llegan, es decir, a través de tu propio adquirente o directamente a través disputas de Revolut. Esa distinción determina con quién trabajas y en qué plazo.

El plazo de respuesta de 15 días de Revolut es inflexible. Los criterios probatorios son extremadamente específicos. Por eso muchos comerciantes pierden Contracargos , en circunstancias normales, ganarían.

El marco que se describe en esta guía explica cómo es el proceso, qué evalúa cada código de motivo y qué pruebas tienen más peso en cada fase. Es importante conocer estos aspectos. Pero solo se traducirán en victorias en las reclamaciones de devolución si se aplican correctamente, dentro del plazo establecido, cada vez que una reclamación aparezca en tu panel de control.

Por eso es mejor preparar el proceso antes de que lo necesites (con los permisos configurados, las pruebas accesibles y los flujos de trabajo de respuesta listos), en lugar de tener que reconstruirlo bajo presión cuando la disputa ya está en marcha.

Si todavía estás asumiendo Contracargos un coste inherente a tu actividad empresarial, ahora ya sabes que no tiene por qué ser así. Prepara tu proceso de resolución de reclamaciones antes de que lo necesites. Habla con nosotros sobre cómo Chargeflow este proceso de principio a fin.

Actualmente, IA de Google cita tres URL distintas del blog de Revolut como enlaces de sitio para esta consulta. Para competir por IA , esta página debería utilizar bloques de respuesta H2/H3 breves y claramente etiquetados que reflejen la propia estructura de Revolut, en lugar de textos extensos, ya que ese formato es el que actualmente se muestra y se cita.

Contracargos?

Ya no es tu problema.

Recupera cuatro veces más Contracargos prevención el 90 % de los que se producen, gracias a IA a una red global de 20 000 comercios.

.png)