%201.svg)

Prevenção de estornos: o guia definitivo

Estornos?

Não são mais um problema para você.

Recupere 4 vezes mais estornos e evite até 90% dos estornos recebidos, com o apoio da IA e de uma rede global de 20.000 comerciantes.

Os estornos representam um risco sistêmico que cresce proporcionalmente à sua receita. Sua prevenção requer três camadas: bloquear transações suspeitas antes da autorização, interceptar contestações na janela de alerta de 24 a 72 horas antes que sejam lançadas e realimentar os dados das contestações em suas operações para corrigir as causas de origem. Processos manuais falham quando a escala aumenta. Se sua taxa de estornos estiver se aproximando dos limites da rede, a lacuna está na infraestrutura. É por isso que Chargeflow .

Se você está enfrentando as consequências de um aumento nos estornos neste momento, saiba que não está sozinho. O padrão é bem conhecido: à medida que o comércio eletrônico cresce, os estornos crescem junto com ele.

A maioria dos casos surge entre 45 e 60 dias após uma transação. Esses casos costumam ser desencadeados por surpresas no extrato, remorso do comprador, arrependimento em relação ao orçamento ou dificuldades com a devolução. Muitos estornos não são necessariamente mal-intencionados. E boa parte deles pode ser evitada.

A boa notícia? Agora é o momento ideal para implementar ou reforçar seus sistemas de prevenção de estornos. Se você fizer isso da maneira certa, evitará que aquela inscrição feita com entusiasmo se transforme em uma contestação do tipo “Não reconheço esta transação” meses depois.

Este guia definitivo explica detalhadamente como funciona a prevenção de estornos no cenário atual. É um guia abrangente. Você descobrirá por que a fraude amigável é responsável por 70% a 80% das contestações, o que é possível prevenir de forma realista, as melhores práticas de prevenção de estornos de cartão de crédito para o comércio eletrônico e quando as ferramentas de automação se tornam essenciais para reduzir drasticamente as taxas de contestação.

O que é a prevenção de estornos

Antes de analisarmos o que significa a prevenção de estornos, é útil relembrar o que são os estornos e por que ocorrem.

O que são estornos?

Os estornos são reversões de pagamento iniciadas pelo consumidor e impostas pelo emissor do cartão. Os estornos são previstos por lei. Eles permitem que os titulares de cartão contornem os comerciantes e revertam transações que considerem fraudulentas, não autorizadas ou insatisfatórias. Em outras palavras, os estornos existem para proteger os titulares de cartão.

Mas e os comerciantes? As chances estão contra eles. Eles precisam processar transações, o que acarreta despesas financeiras e operacionais elevadas, conforme destacado em nosso guia de custos de estornos.

Então, o que é a prevenção de estornos?

A prevenção de estornos refere-se a todas as estratégias, ferramentas, sistemas e melhores práticas que os comerciantes utilizam para reduzir ou evitar estornos. Uma prevenção eficaz de estornos abrange toda a jornada do cliente. Esses protocolos começam antes da autorização da transação e continuam muito depois da conclusão da compra.

Estratégias de prevenção de estornos para comerciantes: a abordagem do ciclo de vida

Uma estratégia abrangente de prevenção de estornos (triagem pré-autorização, controles pós-transação, interceptação de alertas e evidências automatizadas) geralmente reduz as disputas em 40% a 60% em até 90 dias para a maioria dos comerciantes.

Prevenção de estornos pré-transação

- Detecção de fraudes: Ferramentas como verificação de endereço, verificações do CVV, autenticação 3D Secure e filtragem de fraudes baseada em IA (como Chargeflow ) bloqueiam transações não autorizadas.

- Políticas e comunicação claras: descrições transparentes dos produtos, preços, condições de reembolso e devolução, confirmação automática de entrega e atendimento ao cliente padronizado ajudam a minimizar mal-entendidos que poderiam resultar em disputas.

- Alertas pré-contestação: a implementação de alertas de estorno ajuda a interceptar possíveis contestações entre 24 e 72 horas antes que se transformem em estornos formais. Abordaremos esse assunto em detalhes em uma seção posterior.

Prevenção de estornos pós-transação

- Supressão de infratores reincidentes: Ferramentas como Chargeflow utilizam e-mails, dispositivos, endereços IP ou credenciais de pagamento com hash para ajudar a identificar os autores de estornos. É possível restringir facilmente reembolsos, acesso ou transações futuras e impedir que esses fraudadores reincidentes aumentem as perdas pós-transação.

- Controles do ciclo de vida da assinatura: Os provedores de cobrança recorrente implementam sistemas, como lógica de repetição de tentativas, confirmações de cancelamento, opções de pausa ou lembretes de pré-renovação, para evitar disputas pós-transação relacionadas a assinaturas esquecidas.

Agora que você já entendeu como funciona a prevenção de estornos, vamos revisar os tipos de estornos com os quais os comerciantes se deparam.

Os três principais fatores que influenciam os estornos

Existem dezenas de códigos de motivo de estorno entre as redes e os emissores. Na prática, esses códigos podem ser agrupados em três categorias significativas. Compreender as diferenças é fundamental, pois cada uma delas requer uma estratégia de resposta diferente.

1) Fraude por parte de conhecidos

A fraude amigável é o uso indevido intencional (e, às vezes, não intencional) do sistema de estorno. Trata-se de disputas que, em princípio, não deveriam ocorrer, pois o titular do cartão realmente recebeu o produto ou serviço.

O autor não é um criminoso mascarado, mas sim o seu cliente ou alguém próximo a ele. Exemplos de fraude amigável incluem:

- Reclamações de não entrega, apesar da confirmação do cumprimento.

- Taxas de assinatura que o cliente esqueceu que havia concordado em pagar.

- Um familiar ou colega que esteja usando um meio de pagamento salvo.

- Os reembolsos são iniciados, mas não aparecem no extrato com a rapidez necessária.

O que torna a fraude amigável particularmente difícil é a questão da credibilidade. Do ponto de vista do banco, a contestação parte de um titular de cartão legítimo com uma narrativa plausível. Os processos manuais raramente se sustentam em grande escala.

2) Erro do comerciante

Os estornos por erro do comerciante ocorrem quando erros cometidos pelo comerciante dão origem a contestações. Exemplos comuns de erros do comerciante que resultam nessa categoria de estorno incluem os seguintes:

- Erros de cobrança,

- Transações processadas incorretamente,

- Falhas técnicas ou de autorização (cartões vencidos ou falhas na leitura) e

- Reembolsos ou créditos que foram prometidos, mas nunca foram processados.

Essas disputas podem ser evitadas estruturalmente, como veremos a seguir. Quando elas ocorrem repetidamente, você sabe que está lidando com processos ineficientes, e não com pessoas mal-intencionadas.

3) Fraude criminal

Os estornos por fraude criminosa são disputas causadas por fraudes cometidas por terceiros: credenciais roubadas, roubo de identidade ou invasão de conta.

Exemplos de estornos causados por fraudes criminosas incluem:

- Fraude sem a presença do cartão, utilizando dados de cartões comprometidos, tal como ocorreu durante a Operação Chargeback em 2025.

- Acessos não autorizados a contas que resultam em compras não autorizadas.

- Campanhas de verificação de cartões que verificam se as credenciais são válidas.

Do ponto de vista do emissor, essas contestações são válidas. Quando uma transação fraudulenta é autorizada e o verdadeiro titular do cartão percebe, o estorno é inevitável. A prevenção, nesse caso, deve ocorrer antes da aprovação.

Controvérsias que você pode (e não pode) evitar com sistemas de prevenção de estornos

A prevenção de estornos tem a ver com influência, não com regras absolutas. Cada categoria se comporta de maneira diferente. Veja o que você pode e o que não pode, realisticamente, evitar:

1) Erro do comerciante: estruturalmente evitável

Como essas disputas têm origem em falhas internas, os comerciantes têm total autonomia. A prevenção requer:

- Lógica clara de autorização e captura

- Processamento de pagamentos rápido e transparente

- Descrições fáceis de entender para o cliente

Quando os erros dos comerciantes persistem, raramente se trata de um problema de ferramentas. Trata-se de uma falha de coordenação entre os departamentos de pagamentos, finanças e suporte.

2) Fraude por pessoas de confiança: pode ser detectada, mas não evitada

Não é possível impedir objetivamente que um cliente tente contestar uma cobrança indevidamente. O que você pode fazer é eliminar as condições que tornam as contestações fáceis e atraentes.

Isso inclui:

- Reduzindo a confusão nas instruções.

- Facilitar para que os clientes entrem em contato com você antes de falar com o banco deles.

- Resolver disputas antes que se transformem em estornos com cobrança de taxas.

A fraude por parte de pessoas conhecidas é tanto uma questão de timing quanto de confiança. Quanto mais cedo você intervir, maior será sua margem de manobra.

É aí que entra Chargeflow . Ele utiliza dados em tempo real para evitar contestações já no momento da autorização. Mais de 7.000 lojistas já estão usando o serviço para impedir ladrões digitais.

3) Fraude criminal: bastante evitável

No caso de fraudes criminais, a prevenção deve ocorrer totalmente na fase inicial. Uma vez que uma transação com um cartão roubado é processada e aprovada, o resultado está praticamente decidido.

Uma prevenção eficaz de estornos por fraude criminal inclui:

- Autenticação forte (por exemplo, 3DS, quando aplicável)

- Detecção de velocidade e anomalias

- Inteligência de dispositivos e identidades

Os controles pós-transação têm pouca utilidade neste caso. Trata-se de um problema de controle de acesso, não de recuperação.

Principais práticas recomendadas para o comércio eletrônico e a prevenção de estornos de cartão de crédito

Vale a pena reiterar que os estornos no comércio eletrônico são um problema grave para todo o setor. Os bancos e as operadoras de pagamentos são legalmente responsáveis pelos fundos que circulam por suas redes. Se for constatado que estão facilitando a circulação de dinheiro “sujo” ou fraudulento, eles enfrentam multas regulatórias pesadas por parte dos órgãos reguladores e das operadoras de cartão.

Ao tornar os estornos onerosos e punitivos para os comerciantes, o sistema obriga todos os participantes da cadeia de abastecimento a manterem uma vigilância rigorosa.

A seguir, apresentamos as principais práticas recomendadas para a prevenção de estornos em setores específicos:

Produtos e serviços digitais

- Implementar a verificação de e-mail e a autenticação da conta antes da compra

- Registrar endereços IP, IDs de dispositivos e registros de data e hora de download/acesso

- Enviar notificações de uso (“Você acessou este curso em [data]”)

- Considere etapas adicionais de verificação para produtos digitais de alto valor

Produtos físicos

- Exigir confirmação de assinatura em remessas de alto valor

- Utilize métodos de envio com rastreamento para todos os pedidos

- Fotografe os itens com antecedência, sempre que possível

- Considere oferecer serviços de comprovação fotográfica

Negócios baseados em assinaturas

- Envie notificações de cobrança prévia de 3 a 7 dias antes do faturamento

- Simplifique e torne acessíveis os processos de cancelamento

- Ofereça opções de suspensão ou redução do plano como alternativas ao cancelamento

- Implemente uma gestão inteligente de cobranças para pagamentos recorrentes com falha

- Use descrições de cobrança claras e reconhecíveis que incluam o período da assinatura

Setores de alto risco (viagens, eletrônicos, artigos de luxo)

- Implementar a autenticação 3D Secure 2.0 para a transferência de responsabilidade

- Defina limites de transação mais baixos para clientes novos

- Exigir verificação adicional para pedidos de envio expresso

- Fique atento a padrões incomuns de pedidos (vários pedidos, endereços diferentes)

Uma boa prática é implementar alertas e medidas de prevenção de estornos em todos os setores para detectar disputas logo no início.

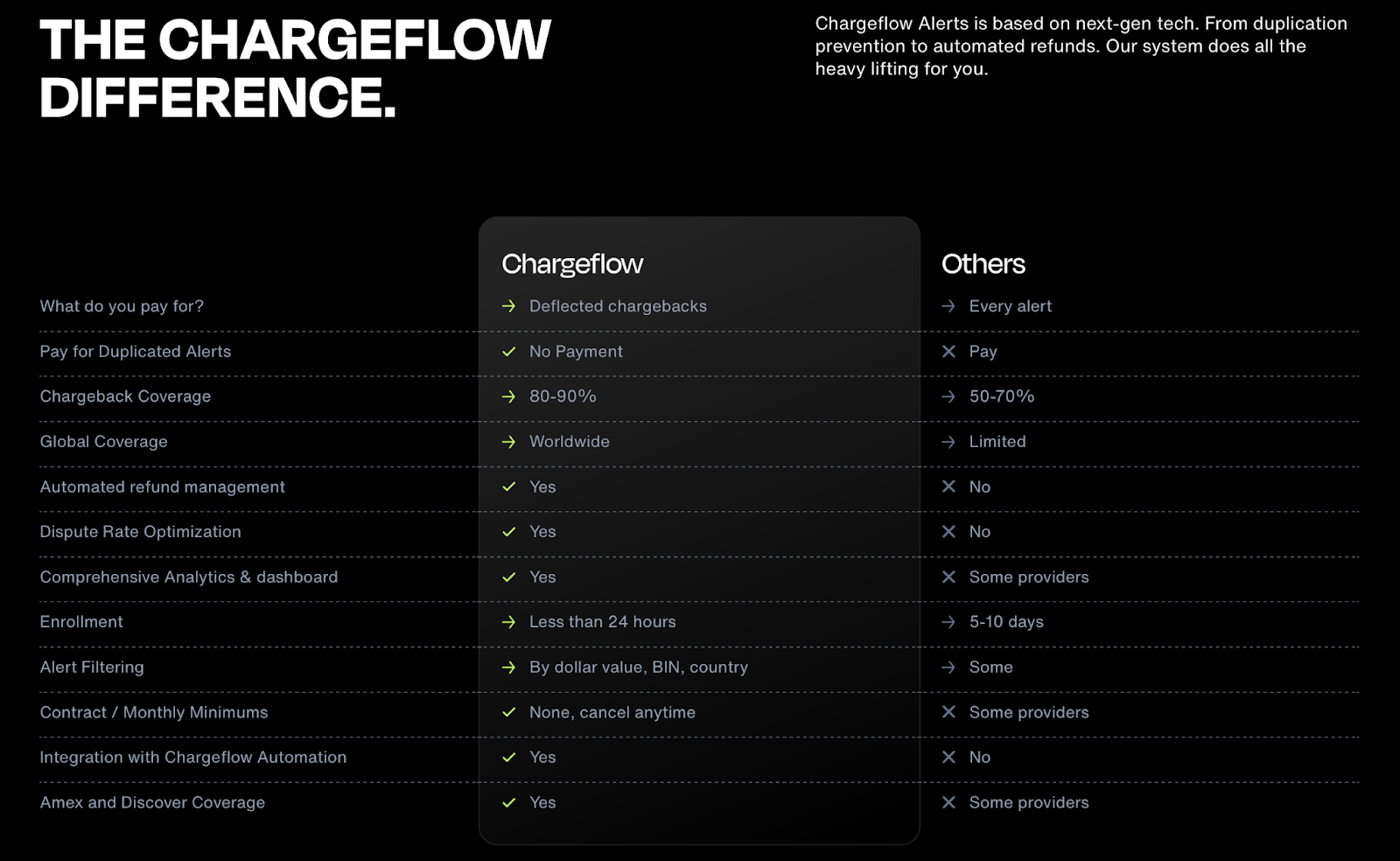

Como os alertas de estorno contribuem para a prevenção de estornos

Os alertas de estorno enviam notificações imediatas assim que um comprador abre uma contestação. O sistema integra os dados das transações às contas dos comerciantes e recebe notificações diretas dos bancos sobre as contestações. Isso suspende temporariamente o processo de estorno, dando aos comerciantes tempo para planejar sua resposta.

Principais benefícios

- Os comerciantes podem resolver disputas de forma proativa diretamente com os clientes ou reembolsar automaticamente a transação antes que o estorno seja registrado.

- Impede que sejam solicitados estornos se o comerciante efetuar o reembolso dentro do prazo de alerta.

- Elimina a necessidade de longos processos de contestação de estornos.

- Ajuda os comerciantes a evitar programas de estornos excessivos.

- Particularmente valioso para comerciantes que vendem produtos de alto valor ou que atuam em setores de alto risco.

O uso de dados de disputas como sistema de controle na prevenção de estornos

Pense nos dados de contestação como o sinal de erro em um sistema de controle. Trata-se de um diagnóstico, não apenas de uma reação. Seu objetivo é diminuir a diferença entre o dinheiro que você ganha e o dinheiro que realmente fica na sua conta bancária.

Os comerciantes que reduzem consistentemente os estornos fazem três coisas:

- Segmente as disputas por produto, canal e grupo de clientes.

- Associar os códigos de motivo às falhas operacionais.

- Incorpore essas informações no processo de checkout, no atendimento de pedidos e no suporte ao cliente.

Siga as etapas abaixo para colocar esse objetivo em prática:

Classificar por fonte verdadeira

Não se limite a analisar os códigos de motivo (que muitas vezes são enganosos). Classifique as contestações por linha de produtos, canal de marketing ou transportadora. Se 40% dos reclamações de “Item Não Recebido” provêm de uma transportadora regional específica, trata-se de uma falha logística, não de um problema de fraude.

Identificar padrões de fraude por parte de clientes de confiança

Analise o prazo para contestação. A fraude genuína geralmente ocorre dentro de 48 horas após a transação. A fraude amigável costuma atingir o pico aos 30 dias, quando chega o extrato do cartão de crédito.

Implementar gatilhos de limite

Configure alertas automáticos. Se a taxa de contestação de um SKU específico ultrapassar um limite pré-definido (por exemplo, 0,5%), o sistema deve acionar uma revisão automática da descrição ou da embalagem desse produto.

Acompanhe sua taxa de estornos

Ultrapassar a taxa de estorno da rede de cartões (contestações divididas pelo total de transações) acarreta multas, aumento das taxas de processamento ou até mesmo o encerramento definitivo da conta.

Chargeflow centraliza e analisa dados de estornos em tempo real. Os comerciantes que adotam essa abordagem de feedback geralmente observam reduções de 20% a 40% nas disputas evitáveis em questão de meses.

Ferramentas e plataformas para prevenção de estornos: quando recorrer a ajuda externa

O problema global dos estornos, que chega a US$ 125 bilhões, não está distribuído uniformemente. Nossas estatísticas de estornos indicam que a fraude amigável é responsável por cerca de 75% de todas as contestações.

No entanto, a maioria dos comerciantes concentra-se excessivamente na prevenção de fraudes criminosas, enquanto investe insuficientemente na interceptação de fraudes não intencionais. Isso cria uma lacuna estratégica: defesas otimizadas para a ameaça menos comum.

Mais uma vez, a prevenção e a correção manuais podem funcionar quando se trata de um ou dois casos. Mas deixam de funcionar quando a escala aumenta.

A automação do estorno é imprescindível quando:

- O volume de estornos excede a capacidade interna de análise.

- As janelas de alerta não são atendidas devido a restrições de tempo ou de pessoal.

- A compilação de evidências fica fragmentada entre os sistemas.

- A fraude por parte de conhecidos é a principal causa das disputas.

- Identificar as causas dos estornos está se tornando um desafio que vai além dos códigos de motivo.

- A taxa de estorno está se aproximando do limite estabelecido pela rede de cartões.

Nesse ponto, a prevenção já não se resume a decisões individuais. Trata-se de sistemas que conectam dados de pagamentos, identidade, atendimento de pedidos e suporte com rapidez suficiente para fazer a diferença.

Plataformas como Chargeflow existem para resolver essa lacuna na execução. Ela unifica alertas de prevenção, automatiza a geração de evidências e o desvio de fraudes amigáveis em um único fluxo de trabalho. Esse nível de coordenação é o que permite a prevenção (e a recuperação) em grande escala.

Considerações finais sobre a prevenção de estornos

A prevenção eficaz de estornos consiste em eliminar falhas sistêmicas que geram risco de contestação.

A maioria dos comerciantes perde receita porque suas medidas de proteção são reativas, fragmentadas ou mal direcionadas.

A verdadeira prevenção cria uma infraestrutura que:

- Bloqueia transações inválidas antecipadamente;

- Garante que todos os pedidos aprovados sejam inequívocos (descrições claras, confirmações, políticas);

- Intercepta disputas na estreita janela de alerta de 24 a 72 horas;

- Utiliza os insights da disputa para resolver as causas fundamentais.

Não é possível fazer isso manualmente ou com sistemas baseados em regras. Como afirma a Mastercard: “As soluções mais eficazes para a prevenção de estornos baseiam-se em uma rede robusta de colaboração global”. Ferramentas automatizadas fornecem, com segurança, informações detalhadas sobre os comerciantes e as compras aos titulares de cartões por meio de seus aplicativos bancários, bem como para as equipes de call center e de back-office das instituições financeiras, ajudando os atendentes a resolver ou evitar uma contestação, ao fornecer às equipes de back-office os dados corretos sobre a transação para permitir uma resolução mais rápida.”

É hora de repensar sua estratégia. Encare os estornos pelo que eles realmente são: o plano para um negócio mais resiliente e lucrativo. O próximo ciclo de faturamento não espera por ninguém. Transforme seus dados em sua principal defesa com Chargeflow.

Evite estornos antes que eles ocorram

Você pode evitar disputas na origem por meio de sinais proativos de fraude e de “fraude amigável”, em vez de ter que lidar com cada estorno após o fato. Chargeflow a prevenção e a resposta a disputas de ponta a ponta, com o respaldo de uma garantia de ROI 4 vezes maior.

Comece de graçaEstornos?

Não são mais um problema para você.

Recupere 4 vezes mais estornos e evite até 90% dos estornos recebidos, com o apoio da IA e de uma rede global de 20.000 comerciantes.

.png)