%201.svg)

Códigos de motivo de estorno: a lista para comerciantes de 2026

Estornos?

Não são mais problema seu.

Recupere 4 vezes mais estornos e evite até 90% dos estornos recebidos, com o apoio da IA e de uma rede global de 15.000 comerciantes.

Os códigos de motivo de estorno são códigos alfanuméricos padronizados que classificam as disputas de pagamento em fraude, autorização, reclamações do consumidor ou erros de processamento. Eles não são veredictos. São sinais de diagnóstico que indicam quais evidências você precisa para vencer. Cada rede de cartões possui códigos, regras e estruturas de responsabilidade distintas. A fraude amigável se aproveita de códigos de motivo de estorno como “transação não autorizada” ou “item não recebido”, mesmo em compras legítimas. Para vencer disputas, é necessário alinhar suas evidências ao teste de responsabilidade específico da rede, e não à alegação do titular do cartão.

Os códigos de motivo de estorno são como as classificações de filmes.

Quando você vê um filme classificado como G, PG ou R, já sabe que tipo de conteúdo esperar. Da mesma forma, os códigos de motivo de estorno, como o 10.4 da Visa ou o 4853 da Mastercard, identificam instantaneamente a categoria de contestação de pagamento com a qual você está lidando.

Mas sempre há uma reviravolta na história.

Assim como a classificação de um filme não revela toda a história, um código de motivo apenas indica o que o titular do cartão informou ao seu banco. Ele aponta o motivo da contestação. Não confirma a verdadeira intenção nem um erro do comerciante. Os códigos de motivo também não determinam a responsabilidade.

Os comerciantes que encaram os códigos de motivo de estorno como um veredicto, em vez de um sinal de diagnóstico, acabam perdendo disputas que poderiam vencer.

Mas essa mudança de perspectiva requer conhecimento. Não apenas sobre quais são os códigos, mas também sobre por que os códigos de motivo de estorno atribuem a responsabilidade da maneira como o fazem, como as redes de cartões aplicam esses códigos em seus modelos de risco e quais evidências influenciam a decisão.

O que é um código de motivo de estorno?

Um código de motivo de estorno é um código alfanumérico padronizado atribuído por um banco emissor para descrever a reclamação do titular do cartão.

Os códigos de motivo de estorno têm três finalidades principais:

- Encaminha a disputa por meio das regras de rede apropriadas

- Define o ônus da prova

- Indica o tipo de comprovante exigido dos comerciantes

Não se trata de confirmações de irregularidades. Em vez disso, elas classificam as reclamações dos titulares de cartão em categorias de contestação reconhecidas pelas redes de cartões.

Essa distinção é fundamental. Pois o que os comerciantes estão realmente enfrentando não é uma reclamação, mas uma avaliação de responsabilidade.

Por que os códigos de motivo de estorno são importantes para os comerciantes

Alguns comerciantes encaram os códigos de motivo de estorno como recibos de dinheiro já perdido. Ao verem “fraude”, eles simplesmente a consideram um custo inerente aos negócios online.

É exatamente com isso que os ladrões digitais estão contando.

Veja o que você ganha ao tratar os códigos de motivo como sinais de diagnóstico, em vez de julgamentos definitivos:

1) Pare de cobrir suas próprias perdas

Cada código de motivo indica a reclamação do titular do cartão, não necessariamente o que aconteceu.

Pense nisso como uma transmissão de rádio. O código do motivo do estorno é o sinal. Os dados da transação subjacente são a gravação completa.

Por exemplo:

- Um código de “transação não autorizada” indica que o titular do cartão alega que a transação foi fraudulenta. Isso não confirma que a compra tenha sido realmente fraudulenta.

- Um código de “produto não recebido” indica uma reclamação por não entrega. Ele não confirma que o item não foi entregue.

O segredo está em separar o ruído do sinal. Os códigos de motivo são pontos de partida. Quando combinados com evidências e análises de padrões, eles deixam de ser meros rótulos para se tornarem informações úteis que permitem contestar alegações falsas e evitar perdas recorrentes.

2) Veja os sinais de uma crise iminente

O reconhecimento de padrões é o que faz de você um verdadeiro mestre em sua área. A interpretação dos códigos de motivo de estorno funciona da mesma maneira.

Quando se analisam os códigos de motivo isoladamente, eles podem parecer problemas aleatórios que exigem soluções distintas. Mas, quando se analisam em conjunto, o quadro muda. Surgem padrões.

Um exemplo: três estornos por “produto diferente do descrito” em itens premium em duas semanas podem parecer apenas azar. Mas isso é quando você lida com eles um por um. Analise-os em conjunto, e isso aponta para uma falha no sistema.

Os veteranos do comércio eletrônico dominam isso. Eles analisam os padrões nos dados. Obtêm uma visão geral dos pagamentos e estornos e corrigem os pontos fracos antes que as perdas se agravem.

3) Lute com inteligência, não com força

Nem todos os estornos apresentam a mesma probabilidade de recuperação. As disputas por fraude em transações devidamente autenticadas podem ser elegíveis para a transferência de responsabilidade, dependendo das regras da rede, do resultado da autenticação e dos critérios de elegibilidade.

Os litígios de consumo em que a documentação de entrega é insuficiente podem ter menores chances de sucesso, mesmo que você disponha de provas convincentes.

Tratar todas as disputas da mesma forma é coisa de 2016. Uma triagem eficaz questiona:

- Este caso cumpre as condições formais para a transferência de responsabilidade?

- Existe continuidade histórica?

- A documentação de atendimento está completa?

- É possível evitar essa disputa na prática?

A gestão moderna de estornos não se resume ao volume. Trata-se de alinhamento de regras.

Códigos de motivo de estorno por rede de cartão (Visão geral estratégica)

Cada rede de cartões possui um sistema de contestação próprio. Os códigos de motivo podem parecer semelhantes. No entanto, as regras, os padrões de prova e os mecanismos de responsabilidade diferem. Essas diferenças determinam os resultados.

Muitos comerciantes não perdem disputas porque seus produtos são ruins. Eles perdem porque suas provas não estão de acordo com as regras do sistema. Atualizações recentes nas redes Visa, Mastercard, American Express e Discover mudaram discretamente a forma como se faz a gestão de estornos.

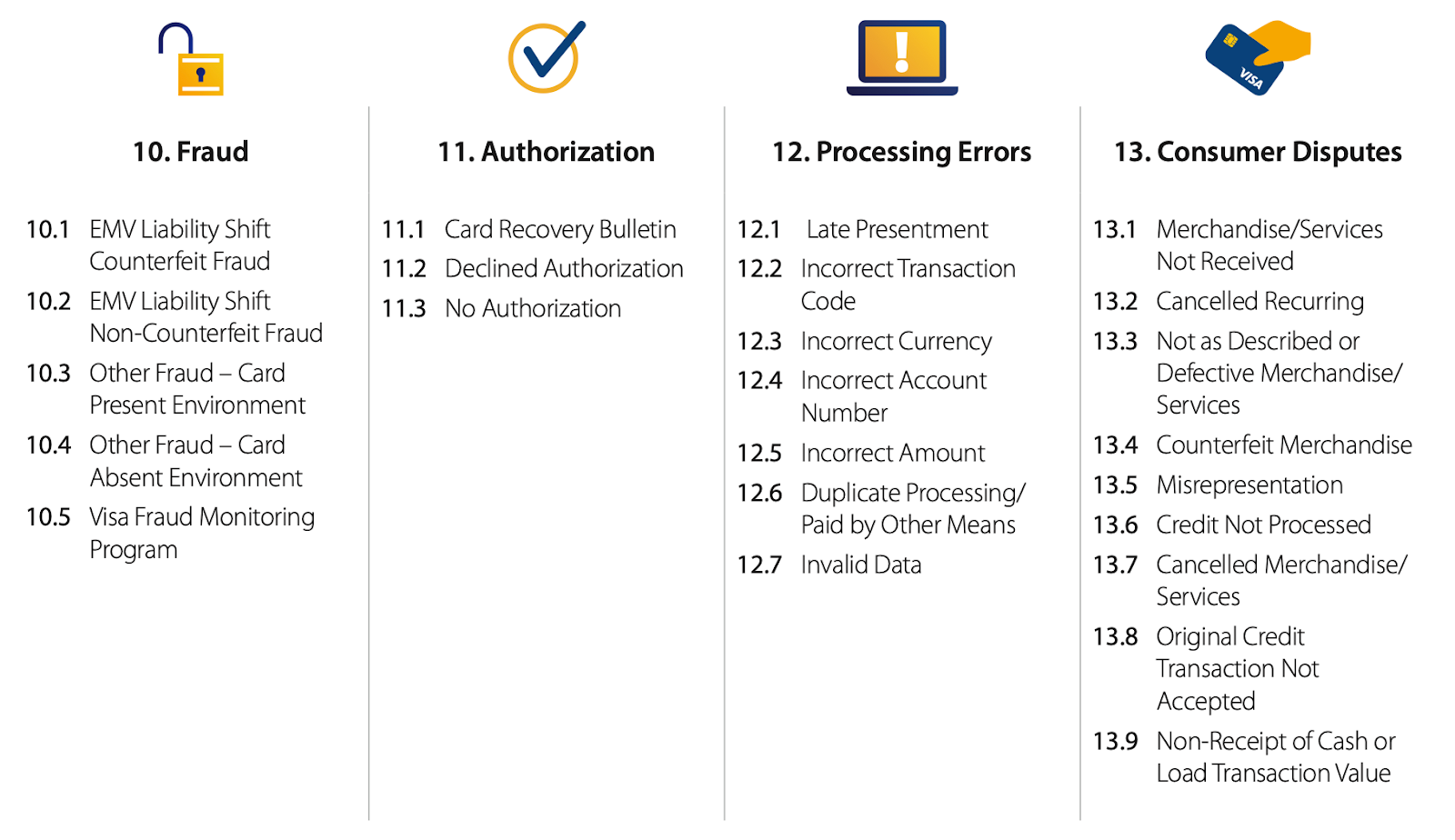

Códigos de motivo de estorno da Visa

Formato: Códigos decimais de dois dígitos (10.x = fraude; 11.x = autorização; 12.x = erros de processamento; 13.x = disputas com o consumidor).

Vantagem Estratégica – CE 3.0

A estrutura “Compelling Evidence 3.0” da Visa permite que disputas por fraude (nomeadamente 10.4 – Fraude, Transação sem a Presença do Cartão) sejam elegíveis para a transferência automática de responsabilidade quando um comerciante cumpre condições rigorosas relativas aos dados.

Para se qualificarem, os comerciantes devem comprovar:

- Pelo menos duas transações anteriores não contestadas

- Identificadores correspondentes (por exemplo, endereço IP, ID do dispositivo, endereço de entrega, credenciais da conta)

- Padrões de uso consistentes

De acordo com a Mastercard, as grandes empresas ganham mais disputas de cobrança do que as empresas de médio porte porque automatizam a coleta de provas.

Consulte a lista completa de códigos de motivos para estornos da Visa e os requisitos de comprovação

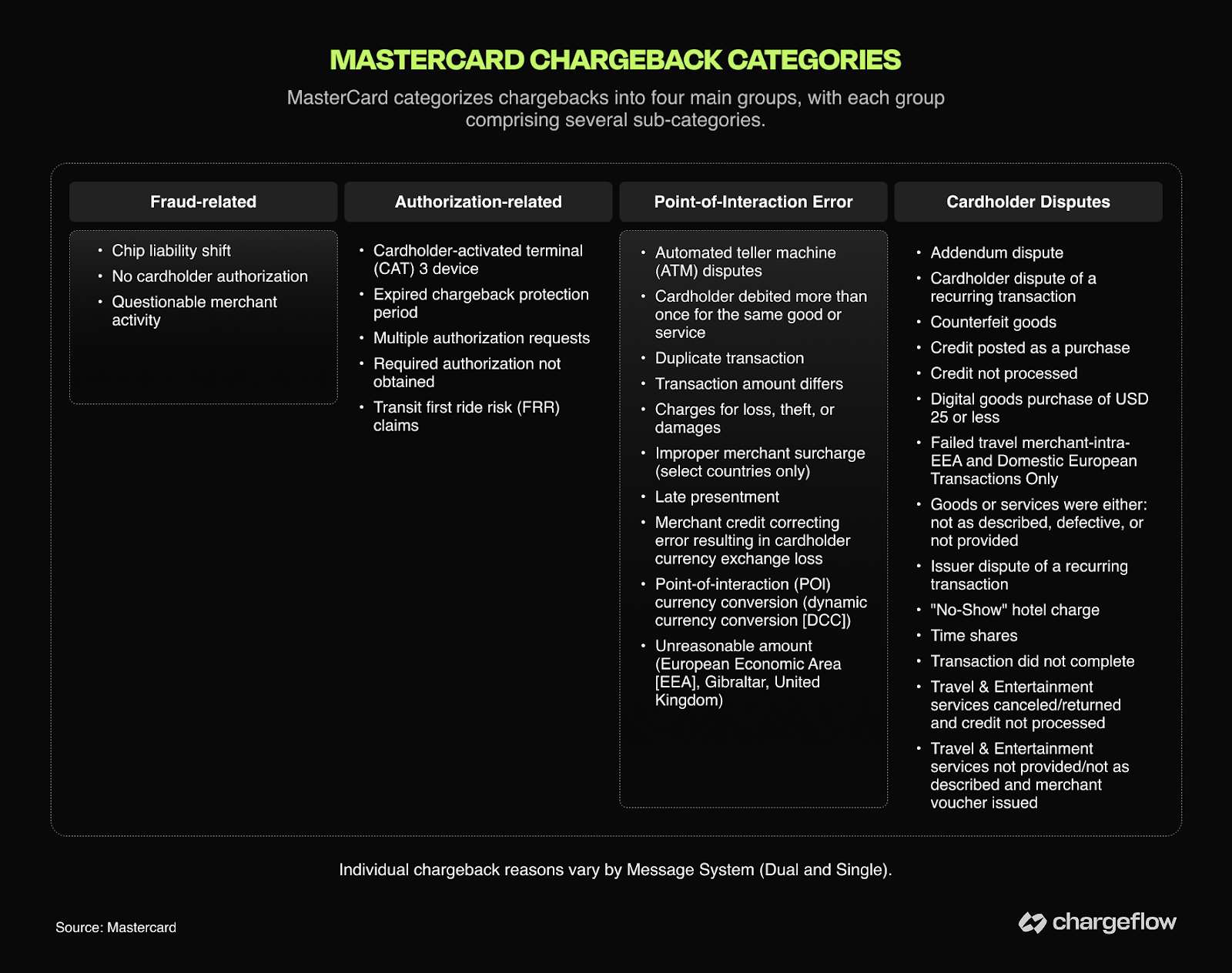

Códigos de motivo de estorno da Mastercard

Formato: Códigos de quatro dígitos (por exemplo, 4837 = Sem autorização do titular do cartão; 4853 = Mercadorias/serviços não recebidos; 4870/4871 = Transferência de responsabilidade por chip/variantes de fraude).

O quadro de contestação da Mastercard difere significativamente do da Visa, especialmente no que diz respeito à interação entre a responsabilidade por fraudes e a autenticação.

Vantagem estratégica - 3D Secure e a realidade da responsabilidade

A transferência de responsabilidade do 3DS da Mastercard depende da autenticação bem-sucedida (Sim/Não), de regulamentações regionais como a PSD3 e da conformidade precisa com as diretrizes de comunicação. A Mastercard agora espelha o CE 3.0 da Visa por meio de seu First-Party Trust Program, oferecendo transferências automatizadas de responsabilidade por fraudes (4837) com base em dados históricos, especificamente duas transações anteriores não contestadas realizadas no último ano. Consequentemente, os resultados das contestações dependem tanto da solidez da autenticação em tempo real quanto da continuidade da identidade verificada para todos os clientes recorrentes.

A estrutura da Mastercard dá ênfase à coerência entre o comportamento legítimo anterior e a transação contestada. Mesmo pequenas lacunas nos metadados podem enfraquecer significativamente as defesas contra fraudes.

Códigos de motivo de estorno da American Express

Formato: Alfanumérico (por exemplo, F29 = Fraude sem apresentação do cartão; C08 = Mercadorias/serviços não recebidos; R03 = Sem resposta).

A American Express atua tanto como emissora quanto como rede. Essa estrutura permite que a Amex analise as transações, as autorizações e os dados dos titulares de cartão internamente, antes e durante o processo de contestação.

Vantagem estratégica: a fase de investigação

Em muitos casos, a Amex inicia uma investigação antes de um estorno formal. Os comerciantes geralmente têm cerca de 20 dias para responder. A falta de resposta pode resultar em um estorno R03 (Sem resposta).

Respostas bem fundamentadas e oportunas na fase de investigação podem evitar que a situação se agrave.

Programas como o de recibos digitais e o compartilhamento aprimorado de dados de transações melhoram o reconhecimento dos titulares de cartão e podem reduzir as reclamações por fraudes “não reconhecidas” antes que se transformem em estornos.

Consulte a lista completa de códigos de motivos para estornos da Amex e os requisitos de comprovação

Descubra os códigos de motivo de estorno

Formato: Códigos de quatro dígitos (por exemplo, 4553 = Não corresponde à descrição; 4554 = Bens/serviços não fornecidos; 7030 = Fraude)

A estrutura de códigos de estorno da Discover segue o modelo da Mastercard, mas opera com uma tolerância menor em relação a erros no descritor de cobrança.

Vantagem estratégica

A Discover prioriza a clareza. A rede oferece um processo simplificado para os comerciantes que mantêm registros de autorização “em dia”. Além disso, responder à Solicitação Formal de Informações (consulta) da rede de cartões no prazo de 20 dias evita que a solicitação se transforme em um estorno com taxas elevadas.

A Discover recompensa igualmente os comerciantes que fornecem indicadores de identidade. A continuidade histórica do endereço reforça a refutação de fraudes, mas não garante a transferência de responsabilidade.

Categorias de códigos de motivo de estorno: Fraude, Autorização, Disputas com o consumidor e Erros de processamento

As redes de cartões classificam os códigos de motivo em quatro categorias: Fraude, Autorização, Disputas do Consumidor e Erros de Processamento. Mais do que simples rótulos organizacionais, essas categorias correspondem a indicadores de ônus da prova que determinam o que você precisa para vencer estornos indevidos.

A árvore de decisão: a quem recai a responsabilidade

Os códigos antifraude avaliam principalmente a solidez da autenticação e a continuidade histórica da identidade.

- Se a autenticação for confirmada, a responsabilidade poderá recair sobre o emissor do cartão.

- Caso contrário, você perderá, a menos que comprove o histórico do relacionamento ou utilize uma estratégia de desvio de estorno para se antecipar à contestação.

Os códigos de autorização exigem a validade da aprovação e o cumprimento dos prazos.

- Se sim, você ganha.

- Se a resposta for não, você perde, independentemente do cumprimento do pedido. Concentre-se nos alertas de estorno ou na prevenção de contestações para evitar isso.

Os litígios de consumo avaliam as provas de cumprimento e a clareza das políticas.

- Existem transferências automáticas de responsabilidade.

- A qualidade das provas determina o resultado da contestação. A automação do estorno se destaca nesse aspecto, pois permite compilar e enviar a documentação rapidamente.

Os erros de processamento avaliam a conformidade com os procedimentos e o prazo para correção.

- Esses erros podem ser evitados pelo comerciante (duplicações, valores incorretos ou crédito atrasado).

- Provas como reembolsos corrigidos, prazos ou recibos podem resolver a contestação se o problema for resolvido prontamente (os prazos variam de acordo com a operadora, geralmente com um prazo de resposta de 20 a 30 dias).

Entender qual critério se aplica é mais importante do que discutir a alegação em si.

Códigos de motivo de estorno e fraudes relacionadas a estornos

Os emissores atribuem códigos de motivo com base nas descrições dos titulares dos cartões. Não se trata necessariamente de uma investigação independente. É por isso que os códigos de motivo não correspondem à realidade.

Estudos do setor mostram consistentemente que a maioria dos estornos no comércio eletrônico decorre de clientes que contestam transações legítimas. Até mesmo as redes de cartões reconhecem essa mudança.

A Mastercard afirma: “Uma parcela cada vez maior disso está ocorrendo porque os consumidores recorrem ao processo de contestação e estorno como forma de recuperar seu dinheiro.”

Como essas reclamações são apresentadas por meio dos canais oficiais do banco, utilizando códigos de motivo legítimos, elas são procedimentalmente válidas até que se prove o contrário. Os códigos servem de disfarce.

Fraude por pessoas próximas e uso indevido de códigos de motivo: os códigos mais frequentemente utilizados indevidamente

Certos códigos aparecem com frequência desproporcional em casos de fraude amigável. Aqui estão alguns exemplos:

Fraude (Visa 10.4/Mastercard 4837)

“Eu não autorizei isso.”

Uma contestação classificada como fraude pode, na verdade, ser:

- Falha na autorização

- Um mal-entendido sobre a assinatura

- Um problema relacionado à insatisfação com o produto

Essas reclamações costumam surgir entre 30 e 60 dias após a compra, especialmente no caso de renovações de assinaturas ou itens com atraso na entrega. Os códigos de fraude têm um peso moral. Eles recebem créditos provisórios rapidamente.

A defesa requer solidez na autenticação, continuidade da identidade e registros históricos das transações.

Mercadoria/serviço não recebido (Visa 13.1/Mastercard 4855/Amex C08/Discover 4554)

“Meu pacote nunca chegou.”

Em muitos casos, a entrega foi efetuada. A disputa depende da solidez das suas provas.

A defesa exige comprovação de entrega ou cumprimento ao titular do cartão (ou a um destinatário autorizado) no endereço, data ou forma acordados.

Como usar os códigos de motivo de estorno para vencer disputas

Não é possível alterar o código atribuído. No entanto, você pode adaptar sua contestação ao teste de responsabilidade desencadeado por esse código.

Como já estabelecemos anteriormente:

- Os códigos de segurança testam a robustez da autenticação e a comprovação de identidade.

- Os códigos de autorização verificam a validade da aprovação.

- As disputas de consumo colocam à prova a documentação de cumprimento.

- Os erros de processamento testam a conformidade operacional.

Extrair esses documentos manualmente pode ser uma tarefa difícil, e é por isso que as disputas de estorno são uma batalha árdua.

Como contestar códigos de motivo de estorno fraudulentos ou incorretos

Contestar códigos de estorno incorretos exige precisão.

Primeiro, você precisa verificar se o código de motivo atribuído corresponde à reclamação do titular do cartão e aos fatos da transação. Os códigos de motivo geralmente refletem a formulação do titular do cartão, e não a realidade da transação.

Se você defender o rótulo em vez de reconstruir o acontecimento, estará permitindo que quem o atribuiu defina o caso e o desfecho.

Em seguida, procure por padrões. Trata-se de um cliente que reclama constantemente? Verifique se há reclamações repetidas do mesmo cliente, códigos de motivo agrupados ou momentos suspeitos.

Mas não dá para fazer isso manualmente e esperar um resultado ideal. Os comerciantes que utilizam fluxos automatizados de comprovação apresentam um desempenho consistentemente superior ao dos processos manuais.

Eis o motivo:

- Os registros de autenticação são capturados automaticamente.

- As confirmações de entrega são vinculadas diretamente aos registros dos pedidos.

- As comunicações com os clientes mantêm a data e a hora registradas e o contexto.

- Os metadados da transação permanecem preservados e podem ser consultados.

Isso transforma as disputas por estornos de investigações frenéticas em respostas simplificadas e padronizadas.

Responda aos estornos com base em uma estratégia de códigos de motivo, e não por impulso

Se os códigos de motivo de estorno são como classificações de filmes, os metadados são o filme completo.

No panorama atual dos pagamentos, essa “reviravolta” não é nenhuma surpresa. É um resultado previsível das lacunas nos dados. Estamos na era da avaliação algorítmica, em que mecanismos automatizados determinam os vencedores comparando instantaneamente os detalhes da sua transação com registros históricos.

Vencer disputas de estorno tornou-se hoje um exercício metódico de equilíbrio de dados. Seja ao acionar o CE 3.0 da Visa ou o First-Party Trust da Mastercard, o sucesso depende de satisfazer a lógica de um computador. Não a compaixão de um ser humano.

Mais uma vez, os códigos de motivo de estorno deixaram de ser um instrumento para padronizar disputas e passaram a ser uma arma para a própria fraude. Pare de ver os códigos como receitas perdidas. Trate-os como sinais de diagnóstico.

As redes escrevem o roteiro. Mas você controla as evidências. Organize seus dados hoje mesmo com o Chargeflow: capture registros, vincule entregas e preserve sinais de continuidade. Com a automação por IA, a fraude amigável se torna uma formalidade que você vence sem precisar levantar um dedo.

Estornos?

Não são mais problema seu.

Recupere 4 vezes mais estornos e evite até 90% dos estornos recebidos, com o apoio da IA e de uma rede global de 15.000 comerciantes.

.png)

ARTIGOS relacionados

Dúvidas?

. Temos as respostas.

O Chargeflow coleta dados de dezenas de fontes externas de forma automática. Isso permite uma cobertura muito maior e taxas de sucesso muito melhores, pois as evidências apresentadas são muito mais abrangentes e convincentes.

O Chargeflow coleta dados como informações sobre pedidos, mensagens de clientes e detalhes de pagamento. Ele monta um processo completo de contestação para você, sem que você precise fazer nada.

Sim! O Chargeflow é compatível com mais de 50 processadores de pagamentos. Isso significa que você tem uma única ferramenta para todos os seus estornos, independentemente da forma como processa os pagamentos.

Você paga apenas uma porcentagem da receita que ajudamos você a recuperar. Sem taxas iniciais, sem assinaturas — apenas uma estrutura de preços baseada no sucesso.

Sim. A Chargeflow possui certificações SOC 2 Tipo 2, GDPR e ISO. Utilizamos os mais elevados padrões de segurança para proteger seus dados.

Precisa de mais ajuda?

Tem alguma dúvida? Estamos aqui para ajudar. Basta clicar no botão de chat para iniciar uma conversa com o suporte.