%201.svg)

Shopify Disputes: Resolution, Chargebacks, and Response

Estornos?

Não são mais um problema para você.

Recupere 4 vezes mais estornos e evite até 90% dos estornos recebidos, com o apoio da IA e de uma rede global de 20.000 comerciantes.

Uma contestação no Shopify é qualquer situação em que um cliente solicita ao seu banco que analise uma cobrança. Pode ser uma consulta (sem movimentação de fundos ainda) ou um estorno (fundos revertidos imediatamente, com cobrança de taxa). A Shopify não decide os resultados; quem decide é o banco emissor. Normalmente, você tem de 7 a 21 dias para responder com evidências relacionadas ao código de motivo. Ganhar significa receber seus fundos de volta; perder significa perda definitiva. Altas taxas de contestação podem acionar programas de monitoramento da rede de cartões. O segredo é rapidez, evidências sólidas e prevenção, pois nem toda contestação vale a pena ser contestada, mas todas afetam seu perfil de risco.

A Shopify dispute (Shopify's term for a chargeback) happens when a customer contests a charge with their bank rather than requesting a refund through the merchant, triggering Shopify Payments' built-in chargeback workflow and a compressed evidence-submission window.

| Passo | Quem | Ação | Cronograma típico |

|---|---|---|---|

| 1. Reclamação apresentada | Cliente | Contests charge with card issuer instead of merchant | No prazo de 60 a 120 dias após a transação |

| 2. Notification | Shopify | Notifies merchant via Shopify admin with reason code | 1-3 business days |

| 3. Provas apresentadas | Comerciante | Uploads evidence directly in Shopify admin | Typically 7-11 days |

| 4. Resolução | Card network / Issuer | Funds returned to merchant or dispute stands with customer | 30 a 45 dias |

No Shopify, especificamente no Shopify Payments, uma contestação é o termo genérico usado para quando um cliente entra em contato com seu banco ou emissor do cartão para questionar uma transação. As contestações no Shopify podem assumir duas formas: uma consulta, que é um pedido de mais informações sem que os fundos tenham sido movimentados ainda, ou um estorno, em que o banco reverte imediatamente os fundos e cobra uma taxa.

A Shopify não decide o resultado. Quem decide é a administradora do cartão, com base nas provas que você apresentar.

Todo estorno no Shopify é uma contestação, mas nem toda contestação se transforma em estorno. O Shopify acompanha todos esses casos no seu painel de administração, e sua taxa geral de contestação inclui todos os casos, independentemente do resultado. É importante manter essa taxa sob controle. Um número excessivo de contestações pode acionar programas de monitoramento de fraudes e estornos da Visa e da Mastercard, o que pode colocar em risco sua capacidade de processar pagamentos.

Este guia aborda tudo o que você precisa saber sobre disputas no Shopify: como responder, como contestar estornos e como proteger sua loja.

O que é uma contestação no Shopify?

Uma contestação no Shopify é o termo oficial que a Shopify utiliza para qualquer situação em que um cliente entre em contato com seu banco ou emissor do cartão de crédito para tentar reverter uma cobrança feita em seu cartão. Quando isso ocorre, o banco do cliente analisa a transação e responde gerando um estorno ou abrindo uma investigação.

O Shopify agrupa tanto as consultas quanto os estornos sob o único identificador “disputa” no seu painel de administração, relatórios, notificações e API.

Contestações do Shopify x Estornos: Principais diferenças

Na prática, uma contestação não é o mesmo que um estorno, e confundir os dois pode sair caro.

Uma contestação é um alerta inicial de que um cliente questionou uma transação, seja por meio do seu banco ou no Shopify Payments. Geralmente, começa como uma consulta. Nessa fase, o caso permanece em aberto e, em alguns casos, os fundos ainda não foram debitados, o que lhe dá uma oportunidade de resolver a questão antes que ela se agrave.

Um estorno no Shopify, por outro lado, é uma reversão formal iniciada pelo banco emissor. Ele pode ocorrer após uma disputa não resolvida ou sem qualquer aviso prévio.

Principais diferenças entre disputas no Shopify e estornos

Here's how Shopify officially distinguishes between Shopify disputes and Shopify chargebacks:

| Aspecto | Estorno | Contestação (Reclamação) |

|---|---|---|

| O que é | O banco estorna imediatamente o pagamento (um estorno total ou parcial). | O banco investiga a reclamação do cliente, mas ainda não estorna os fundos. |

| Impacto nos seus fundos | O valor em disputa e a taxa de estorno da Shopify são debitados imediatamente do seu saldo ou pagamentos da Shopify. | Não é cobrado nenhum valor imediatamente. |

| Se você ganhar | Os valores e a taxa de contestação serão devolvidos a você. | Não é necessária nenhuma ação; o inquérito é encerrado sem impacto financeiro. |

| Se você perder | Você perde definitivamente os fundos e a taxa. | A contestação pode resultar em um estorno total (com a dedução dos valores e das taxas). |

| Processo de resposta | Você recebe uma notificação com um prazo para enviar as provas. A Shopify encaminha o caso à rede de cartões/emissora para uma decisão final. | O mesmo processo de apresentação de provas, mas com menos pressão imediata. |

| Motivos comuns | Fraude, falta de entrega, produto com defeito, cobrança duplicada, etc. (o mesmo que consultas). | Pelas mesmas razões, mas muitas vezes considerado como uma etapa preliminar. |

Como contestar uma cobrança no Shopify

Como comerciante, você não controla como uma contestação é iniciada. Quem controla é o titular do cartão. Veja a seguir como esse processo se desenrola do ponto de vista dele.

Quando um cliente vê uma cobrança que não reconhece ou com a qual discorda, ele tem duas opções:

1) Entrar em contato diretamente com você,

2) Vá diretamente ao banco deles.

A maioria acessa o banco por meio de um aplicativo ou outros canais. A partir daí, o banco assume o controle. Eles registram a reclamação, atribuem um código de motivo para o estorno e decidem se vão enviar uma consulta ou passar diretamente para o estorno, muitas vezes sem notificá-lo até que a decisão já tenha sido tomada.

O código de motivo atribuído pelo banco é importante. Ele determina quais provas você precisará apresentar para contestá-lo e qual é, de fato, o seu poder de negociação.

Quando a contestação aparece no seu painel, o prazo já começou a correr. A fase de resposta é fundamental. Você está respondendo a um processo mediado pelo banco com um prazo rígido e sem margem para idas e vindas.

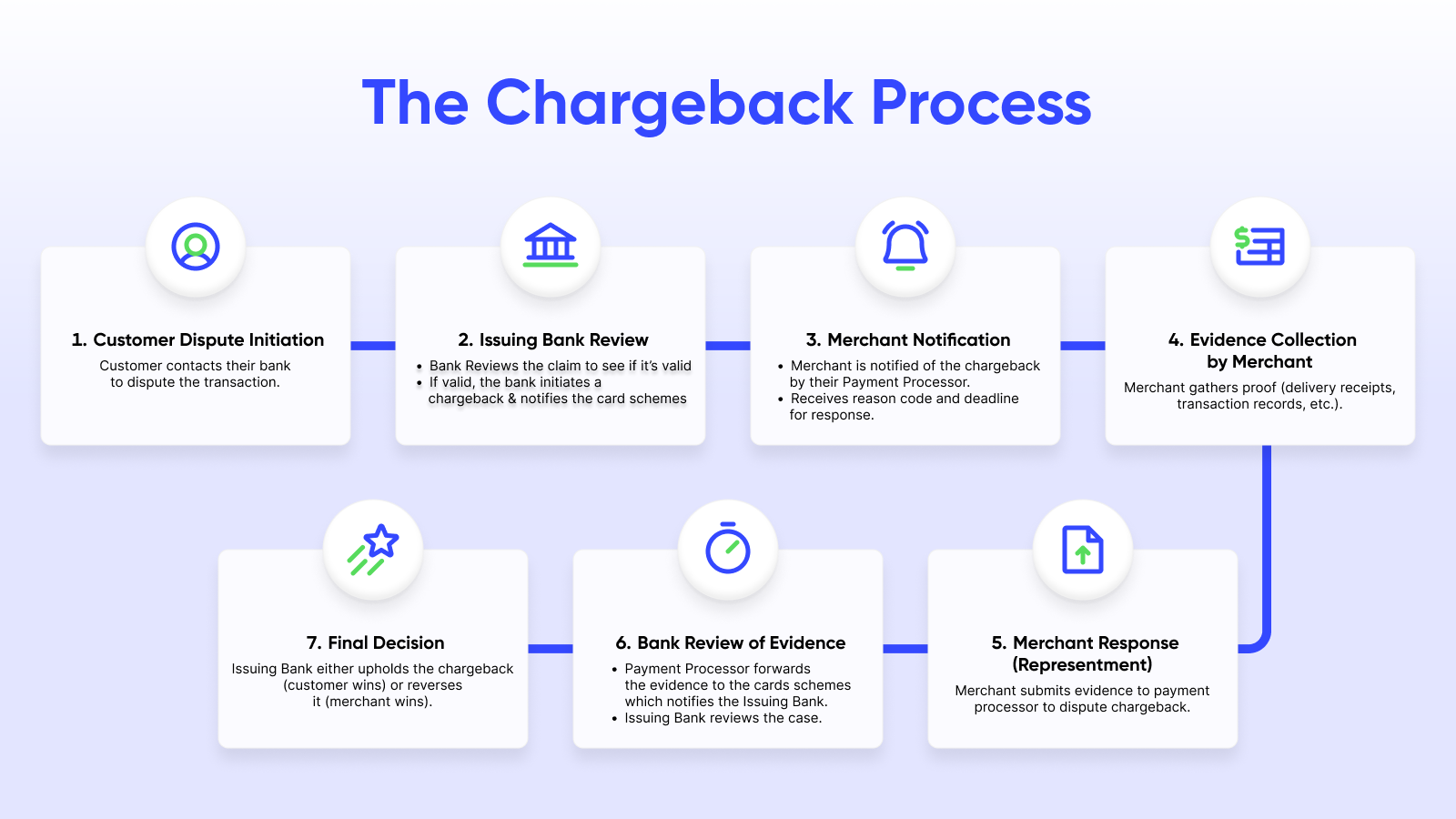

O processo de contestação de estornos do Shopify

Quando surge uma contestação no painel de administração do Shopify, você geralmente tem de 7 a 21 dias para responder. A maneira como você aproveita esse prazo determina se você recuperará os fundos ou se os perderá definitivamente.

Se a contestação parecer ser um mal-entendido (como uma cobrança que o cliente não reconheceu, uma entrega que ele não recebeu ou uma devolução que ficou por resolver), entre em contato diretamente com ele antes de reunir suas provas. É melhor resolver uma contestação do que ganhá-la. Se ele concordar em desistir da reclamação, peça que solicite uma carta de cancelamento ao banco e a envie para você.

Apresente isso como prova; é a solução mais clara possível.

Isso pode não funcionar em todos os casos. Ignore essa etapa em casos evidentes de fraude de pagamento ou com clientes que já tenham reagido de forma agressiva.

Passo 1: Identifique a controvérsia

No painel de administração do Shopify, acesse “Pedidos” e clique em “Pesquisar e filtrar” > “Adicionar filtro ” > “Status de estorno e consulta ” > “Em aberto”.

Verifique este filtro diariamente. Prazos perdidos não podem ser recuperados.

Etapa 2: Analisar a alegação do emissor

Abra o pedido e leia atentamente a descrição do emissor e o código de motivo.

Sua argumentação deve refutar diretamente o motivo específico. Por exemplo:

- A fraude requer provas que comprovem a autorização (correspondência entre AVS e CVV, registros de IP, etc.)

- Para produtos não recebidos, é necessário apresentar comprovante de entrega e documentação de rastreamento.

- Para contestar uma cobrança duplicada, é necessário apresentar comprovantes que mostrem os registros de cobrança do titular do cartão.

Os envios genéricos são automaticamente rejeitados. O uso de uma plataforma de contestação de estornos assistida por IA produz melhores resultados, pois as evidências são adaptadas à reclamação.

Passo 3: Decida se vai lutar

Uma rápida reflexão:

- Você tem provas concretas e específicas?

- O valor do pedido compensa o tempo gasto?

- Essa afirmação é realmente defensável?

Nem todas as disputas precisam ser contestadas. Essa análise de probabilidade de ganho ou perda está integrada a uma plataforma automatizada e nativa do Shopify, como o Chargeflow.

Etapa 4: Elaborar um conjunto de provas estruturado

Clique em “Adicionar evidência ” (abre a página de resposta ao estorno ). Crie um caso claro e conciso:

- Breve explicação por escrito (sua descrição).

- Documentos comprovativos específicos.

- Tudo estava de acordo com o código de motivo.

Você pode salvar o progresso e voltar mais tarde. A clareza é mais importante do que a extensão. Para obter uma descrição detalhada do que enviar e como estruturar o documento, consulte “Formulários de contestação, provas e prazos de resposta do Shopify” abaixo.

Passo 5: Inscreva-se com antecedência

Quando estiver pronto, clique em “Enviar agora”. O Shopify enviará automaticamente tudo o que você tiver salvo na data limite, mas enviar antecipadamente lhe dá mais controle e reduz os riscos.

Passo 6: Aguarde a decisão do emissor

Após o envio, o banco analisa os seus documentos comprovativos. Esse processo pode levar até 75 dias. Você verá o status mudar para “Enviado” e, em seguida, para “Aceito”, “Rejeitado” ou “Em análise”.

Resultado final

- Vitória: O valor contestado e a taxa de estorno são devolvidos a você (o reembolso da taxa depende da sua região).

- Perda: os fundos permanecem com o cliente.

Formulários de contestação, provas e prazos para resposta no Shopify

Você analisou cuidadosamente o código de motivo e decidiu contestar. Agora é hora de elaborar uma contestação que o banco não possa ignorar. Veja aqui exatamente o que o Shopify aceita, como estruturá-la e quanto tempo você tem.

Formulário de resposta a estorno

O formulário de provas para contestação redesenhado da Shopify destaca os campos mais importantes. Ele oferece total transparência, exibindo exatamente o documento em PDF que a Shopify irá gerar e enviar ao banco. Você pode visualizar o envio antes de ele ser enviado, e o que o banco recebe é exatamente o que você vê na visualização.

Requisitos de arquivo

O Shopify impõe regras de formatação rigorosas. Os bancos costumam receber documentos por fax, por isso a legibilidade é imprescindível:

- Formatos aceitos: apenas PDF, JPEG ou PNG.

- Peso máximo por arquivo: 2 MB.

- Tamanho máximo total das provas: 4 MB.

- Os arquivos PDF devem estar em conformidade com o padrão PDF/A e ter menos de 50 páginas.

- Sem áudio, vídeo ou links externos.

Envie no máximo um arquivo por tipo de prova, combinando vários arquivos do mesmo tipo em um único arquivo, se necessário. As imagens devem ter alto contraste e ser imprimíveis em preto e branco.

Como organizar suas provas

Comece com a sua prova mais forte e vá diminuindo a intensidade. Cada documento deve abordar diretamente o código de motivo específico; qualquer coisa genérica enfraquece o conjunto de documentos:

- Provas diretas: confirmação de entrega, rastreamento, registros de assinatura, registros de uso.

- Notificação ao cliente: e-mails ou mensagens confirmando o recebimento, compras anteriores ou informações sobre transações.

- Documentação sobre políticas: Termos de serviço ou política de reembolso com os quais o cliente concordou no momento da finalização da compra.

- Contexto de referência: resultados da verificação de AVS/CVV, registros de endereços IP e histórico de pedidos do mesmo cliente.

Prazos

O prazo varia de 7 a 21 dias após o registro do estorno ou da consulta. Se nenhum prazo específico for exibido, o prazo final é às 23h59 da data indicada no fuso horário da sua loja.

Duas coisas que vale a pena saber sobre o tempo:

- Depois de clicar em “Enviar agora” para enviar sua resposta antecipadamente, você não poderá mais fazer alterações em seus documentos. Não envie antecipadamente, a menos que sua documentação esteja completa.

- Se você não enviar manualmente, o Shopify coleta automaticamente as evidências e as envia à rede do cartão na data de vencimento. Envie sempre manualmente.

Resolução de disputas de pagamentos no Shopify

Quando você processa pagamentos pelo Shopify Payments, todo o ciclo de vida das contestações é gerenciado no painel de administração do Shopify.

O Shopify compila automaticamente os dados disponíveis dos pedidos, caso você não adicione seus próprios comprovantes, e os enviará ao emissor do cartão na data de vencimento da resposta.

No entanto, esse envio padrão costuma ser muito básico. Os comerciantes que elaboram e enviam ativamente evidências estruturadas geralmente obtêm melhores resultados.

A Shopify atua como processadora de pagamentos. Ela debita o valor contestado e a taxa do seu saldo, encaminha sua resposta (conforme discutimos anteriormente) e devolve a taxa recuperada caso você vença.

Algumas palavras sobre o Shopify Protect

Os comerciantes sediados nos EUA que utilizam o Shopify Payments com o Shop Pay podem se qualificar para o Shopify Protect.

Quando um pedido elegível é marcado como “Protegido”, aplica-se o seguinte:

- A Shopify assume automaticamente a responsabilidade por estornos fraudulentos e não reconhecidos.

- Você receberá imediatamente o reembolso do valor total do pedido e da taxa de estorno.

- Não é necessário apresentar provas; a Shopify cuida de todo o processo de resolução de disputas.

Principais limitações

A proteção se aplica apenas a pedidos que contenham exclusivamente produtos físicos entregues em até 7 dias por meio de um sistema de rastreamento compatível. Ela não cobre o checkout padrão, gateways de terceiros, produtos digitais ou disputas não relacionadas a fraudes (como “item não recebido”, “não corresponde à descrição” ou fraudes por estorno).

Isso deixa os comerciantes totalmente expostos à maioria das disputas que realmente afetam seus resultados financeiros. E é por isso que muitas lojas complementam o Shopify Protect com ferramentas específicas de automação de estornos que funcionam para todos os tipos de disputas.

Gestão de disputas: PayPal x Shopify

O Shopify Payments e o PayPal oferecem duas abordagens distintas para o processamento de pagamentos. No entanto, em casos de contestação, a arquitetura de cada sistema proporciona uma experiência fundamentalmente diferente. O Shopify Payments atua como um canal direto com a rede de cartões, encaminhando as contestações diretamente ao banco emissor. O PayPal atua como um intermediário entre você e o banco, com seu próprio Centro de Resolução, regras distintas e, em muitos casos, sua própria decisão.

Como as contestações são apresentadas e acompanhadas

Com o Shopify Payments, as contestações aparecem automaticamente no seu painel de controle. Não é necessário monitorar nenhuma plataforma separada. Tudo é centralizado a partir do momento em que um caso é aberto.

O PayPal opera seu próprio sistema de resolução de disputas por meio do Centro de Resolução. Quando um comprador abre uma disputa, o PayPal retém os fundos da transação enquanto ambas as partes buscam uma solução. Se não conseguirem chegar a um acordo, o comprador pode elevar o caso a uma reclamação. Nesse momento, o PayPal investiga e, frequentemente, toma a decisão final, dependendo da forma de pagamento utilizada na transação. Se o caso evoluir para um estorno pela rede de cartões, o banco emissor assume o caso e toma a decisão final.

Apresentação de provas

O Shopify converte os documentos enviados em um PDF, permite que você visualize o documento exato que será enviado à rede de cartões e o envia em seu nome. O processo é transparente e ocorre inteiramente no seu painel de administração.

Com o PayPal, você envia as provas por meio da Central de Resoluções. O PayPal analisa as provas internamente antes de encaminhá-las ao banco emissor, se necessário. Se você não cumprir o prazo, o PayPal decide automaticamente a favor do comprador.

Os requisitos de comprovação variam de acordo com o tipo de reclamação. No caso de produtos físicos, o item deve ser enviado para o endereço indicado na página da transação, sendo necessária a apresentação de comprovante de entrega. Para pedidos de US$ 750 ou mais, é obrigatória a confirmação por assinatura.

Cronogramas e prazos

O Shopify Payments concede aos comerciantes um prazo de 7 a 21 dias para responder, de acordo com as regras da rede de cartões. O não cumprimento do prazo resulta em uma perda automática.

O prazo do PayPal é mais amplo e mais longo. Os compradores têm até 180 dias a partir da data da transação para abrir uma contestação. Ambas as partes têm então 20 dias para resolver a questão diretamente. Se o comprador levar o caso adiante, o vendedor tem 10 dias para responder. Se esse prazo não for cumprido, o PayPal decide a favor do comprador.

Taxas e impacto financeiro

Com o Shopify Payments, o valor em disputa e a taxa de estorno de US$ 15 são deduzidos do seu saldo imediatamente quando um estorno é emitido. A taxa é devolvida se você vencer a disputa, dependendo da sua região.

Com o PayPal, os fundos da transação ficam indisponíveis após um estorno até que o caso seja encerrado. Para transações pagas com cartão não cobertas pela Proteção ao Vendedor, é cobrada uma taxa de estorno de US$ 20. Quando a Proteção ao Vendedor cobre a transação, essa taxa pode ser dispensada.

Uma análise mais aprofundada dos programas de proteção ao vendedor

O Shopify Protect está disponível para comerciantes sediados nos EUA com uma conta do Shopify Payments nos EUA, cobrindo estornos fraudulentos e não reconhecidos apenas em pedidos elegíveis do Shop Pay. Os pedidos devem conter itens físicos que exijam envio; produtos digitais, retiradas na loja e pedidos com parcelamento do Shop Pay estão excluídos. Para se qualificar, o pedido deve ser atendido dentro de 7 dias após a realização, com um número de rastreamento válido de uma transportadora compatível, e marcado como em trânsito dentro de 10 dias. Quando todas as condições forem atendidas, a Shopify lida com a contestação automaticamente, sem necessidade de envio de provas.

A Proteção ao Vendedor do PayPal abrange duas categorias: transações não autorizadas e reclamações por “Item não recebido” registradas através da Central de Resolução do PayPal. Atualmente, a Proteção ao Vendedor não se aplica mais a reclamações por “Item não recebido” nas quais o comprador solicitou um estorno diretamente junto à administradora do cartão para uma transação paga com cartão. A proteção para a categoria “Item não recebido” se aplica apenas a reclamações feitas no Centro de Resolução do PayPal; ela não se estende a estornos solicitados junto a um emissor de cartão externo. Ao contrário do Shopify Protect, ela não é automática. A elegibilidade depende do tipo de transação, da comprovação de entrega e se o pedido está classificado como “Elegível” no momento da disputa.

Recursos e escalonamento

Assim que uma contestação do Shopify Payments for decidida pelo banco emissor e o prazo tiver expirado, o resultado é definitivo. Não há fase de recurso.

O PayPal oferece maior flexibilidade. Os comerciantes podem recorrer da decisão do PayPal sobre uma reclamação no prazo de 10 dias, caso haja novas informações disponíveis. Em casos de estorno de cartão, o PayPal pode representar o comerciante na fase pré-arbitral ou na arbitragem. Isso é raro, mas está disponível em certos cenários em que a decisão inicial é contestada.

Como prevenir e resolver disputas no Shopify

A melhor contestação é aquela que nunca ocorre. Antes de uma transação, ative as ferramentas de análise de fraudes do Shopify, verifique se os dados AVS e CVV correspondem e sinalize os pedidos de alto risco antes que sejam enviados. Após a transação, envie proativamente confirmações de pedido e notificações de entrega. A maioria das fraudes bem-intencionadas começa com uma cobrança que o cliente simplesmente não reconheceu.

Quando surgir uma contestação, aja rapidamente. Verifique diariamente sua área administrativa, entre em contato com o cliente primeiro nos casos em que a cobrança é recuperável e reúna evidências que comprovem diretamente o código de motivo. Respostas genéricas são inúteis. Além disso, a reapresentação manual nem sempre atende aos padrões de evidência das operadoras, e é por isso que muitos comerciantes obtêm taxas de sucesso de cerca de 20%.

Isso vale especialmente para lojistas com grande volume de vendas. Ferramentas como o Chargeflow, desenvolvidas para o Shopify, automatizam todo o processo de contestação do Shopify. Em vez de gerenciar as contestações etapa por etapa, você conta com um único sistema que lida com o desvio de contestações, alertas, provas, envio de documentos e análise de dados de ponta a ponta.

As disputas relacionadas a pagamentos fazem parte da gestão de uma loja. A maneira como você reage — antes, durante e depois — determina se elas permanecerão controláveis ou se se tornarão uma ameaça à sua capacidade de processar pagamentos.

Can you dispute with Shopify?

Yes - 'dispute' is Shopify's term for a chargeback filed by a customer with their card issuer; merchants respond to disputes directly through the Shopify admin's evidence-submission tools.

Do customers usually win chargebacks?

Chargebacks default in the customer's favor unless the merchant submits compelling evidence in time, so response speed and evidence quality heavily influence the outcome.

Can I get my money back from Shopify?

If you're a customer disputing a purchase, you get funds back from your card issuer via the chargeback, not directly from Shopify, which only facilitates the merchant's evidence response.

Automate Chargeback Disputes for Your Shopify Store

You can automate evidence collection and submission across every Shopify dispute instead of managing them by hand. Chargeflow submits on time, every time, backed by a 4X ROI guarantee.

Comece de graçaEstornos?

Não são mais um problema para você.

Recupere 4 vezes mais estornos e evite até 90% dos estornos recebidos, com o apoio da IA e de uma rede global de 20.000 comerciantes.

.png)