%201.svg)

O que é a Proteção “ Chargeback ”? Guia do site Lojista

Chargebacks?

Não é mais problema seu.

Recupere 4 vezes mais chargebacks e PREVENÇÃO — até 90% dos e-mails recebidos —, com tecnologia de IA e uma rede global Rede de 20.000 Lojistas.

Chargeback A proteção, em sua essência, trata de controle. É a combinação de ferramentas, serviços e fluxos de trabalho estruturados que ajudam Lojistas PREVENÇÃO chargebacks , Reduza Disputa a manter os índices e proteger a estabilidade dos pagamentos a longo prazo. Lojista chargeback A proteção pode incluir triagem de fraudes, chargeback Alertas , garantias e segurança de ponta a ponta Disputa Automação . As melhores estratégias de proteção chargeback se concentram, em primeiro lugar, na prevenção; em segundo, na intervenção precoce; e só então na recuperação. Chargeback A proteção não se trata de conquistar mais disputas. Trata-se de controlar o risco antes que ele se agrave.

Chargebacks não são mais questões operacionais isoladas. Elas afetam diretamente a receita, os índices de Disputa , o monitoramento da exposição do programa e o acesso ao processamento a longo prazo.

Além da perda de vendas, o “ chargebacks ” gera:

- Taxas não reembolsáveis do programa “ Disputa ”

- Carga operacional

- Análise do cartão “ Rede ”

- Aumento dos custos de processamento

- Possível encerramento da conta

Um serviço de “ chargeback ” de US$ 120 pode rapidamente atingir um custo real de US$ 200 ou US$ 250, uma vez que se levem em conta as taxas, a mão de obra interna e o impacto da alíquota. Para se ter uma ideia, mesmo um serviço menor de “ chargeback ” de US$ 70, combinado com uma taxa de US$ 25 e 3 horas de trabalho da equipe, torna-se instantaneamente um prejuízo de US$ 125. Multiplique isso por 40 ou 50 “ disputas ” por mês, e os “ chargebacks ” passam a ser um risco estrutural, e não apenas um inconveniente transacional.

É nesse ponto que muitos Lojistas cometem um erro de cálculo. Eles avaliam chargebacks individualmente. As redes de cartões, por sua vez, as avaliam cumulativamente.

Chargeback Existe uma proteção para Reduza esse risco. Para empresas de comércio eletrônico, entender o que é a proteção chargeback e como ela funciona é essencial para manter a estabilidade dos pagamentos à medida que Disputa os volumes aumentam.

Este guia explica:

- O que é a proteçã chargeback ?

- Como funciona a proteçã chargeback e para Lojistas

- A diferença entre a proteção “ Lojista ”chargeback e a proteção contra fraudes

- O que se enquadra na proteçã chargeback

- Como avaliar as melhores opções de proteção contra o vírus “ chargeback ”

O que é a Proteção “ Chargeback ”?

Chargeback A proteção é uma combinação de ferramentas e processos projetados para ajudar Lojistas PREVENÇÃO , gerenciar ou Reduza o impacto de chargebacks.

Em essência, a proteção contra o “ chargeback ” concentra-se em reduzir o “ disputas ” antes que ele ocorra, minimizar as perdas quando o “ disputas ” acontece e proteger o “ Lojistas ” contra taxas excessivas de “ chargeback ”.

Chargeback A proteção pode incluir:

- Chargeback proteção contra fraudes e análise de transações

- Chargeback Alertas e as primeiras notificações do “ Disputa ”

- Reembolso automatizado e reconciliação de “ Disputa ”

- Chargeback garantias ou programas de reembolso

- Ciclo de vida completo do Disputa Automação , incluindo a reapresentação

Nem todas as soluções de proteção contra fraudes chargeback Soluções funcionam da mesma maneira. Algumas se concentram apenas na prevenção de fraudes no momento da finalização da compra, enquanto outras são projetadas para gerenciar todo o ciclo de vida chargeback após a conclusão de uma transação.

A diferença é fundamental. Uma solução voltada exclusivamente para fraudes protege as transações. Um verdadeiro sistema de proteção “ chargeback ” protege seus índices.

Compreender essa distinção é fundamental ao avaliar uma solução de proteção contra o “ chargeback ” para comércio eletrônico Soluções.

Chargeback Proteção para o site Lojistas: Por que isso é importante

Chargeback A proteção em questões relacionadas a Lojistas é importante porque chargebacks tem um impacto que vai muito além das transações individuais.

Cada chargeback pode resultar em:

- Receita perdida na venda original

- Taxas não reembolsáveis do programa “ chargeback ”

- Aumento dos índices de “ chargeback ”

- Inclusão em programas de acompanhamento

- Custos de processamento mais elevados ou encerramento da conta

Lojista chargeback A proteção ajuda as empresas:

- Reduza Disputa volume

- Proteger os privilégios de processamento de pagamentos

- Menor carga operacional

- Manter a estabilidade das receitas a longo prazo

Lojistas pode vencer em nível individual disputas e ainda assim estar sujeito a penalidades se o volume geral chargeback continuar alto.

Vencer no “ disputas ” dá uma sensação de produtividade. Controlar os índices é o que mantém as contas ativas.

Como funciona a proteção “ Chargeback ” para comércio eletrônico e cartões de crédito

Chargeback A proteção para transações de comércio eletrônico e com cartão de crédito abrange várias etapas da jornada do cliente.

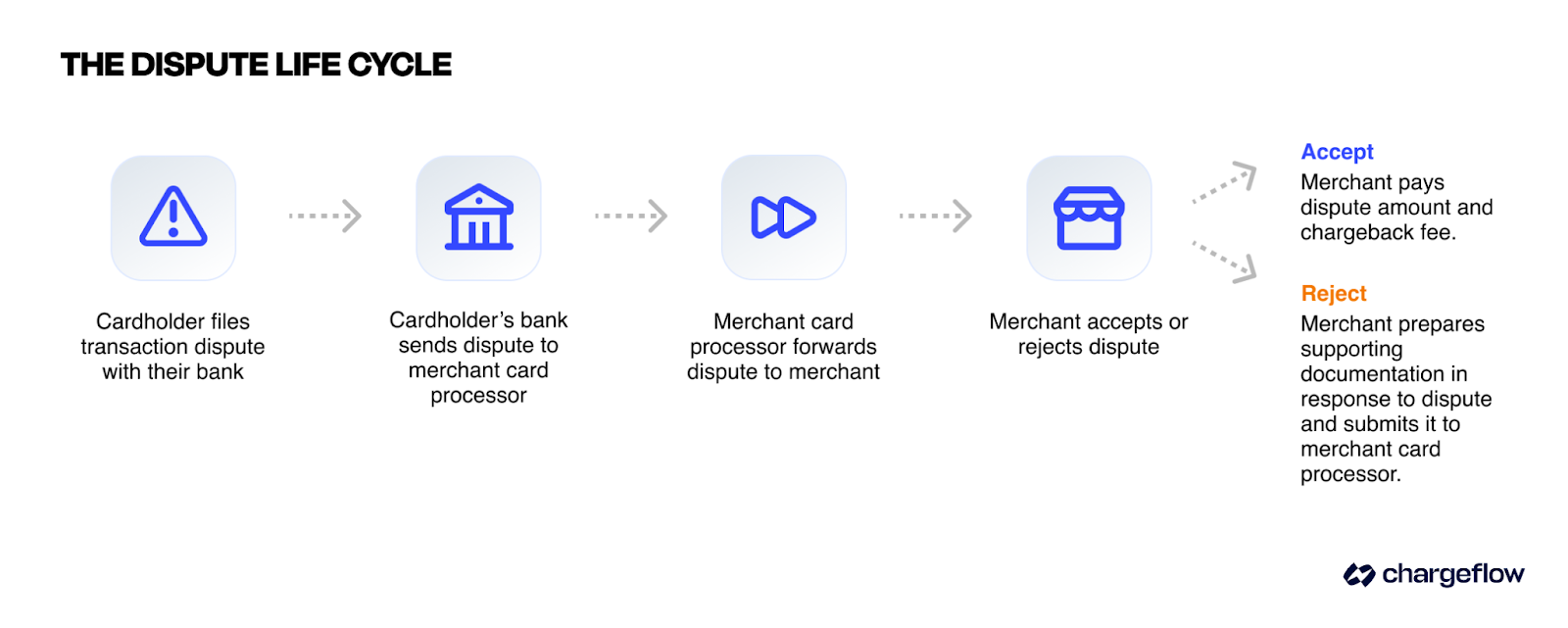

O processo “ Chargeback ”: da “ Disputa ” à resolução

Antes de finalizar a compra

Os sistemas de detecção de fraudes avaliam o risco das transações para PREVENÇÃO ar o uso de cartões roubados e pedidos de alto risco.

Após a compra

Chargeback A proteção pode incluir:

- Alertas quando um pedido de “ Disputa ” está prestes a ser apresentado

- Intervenção de reembolso para PREVENÇÃO chargebacks

- Gestão automatizada da admissão e do fluxo de trabalho do Disputa

- Alegações e apresentação de provas

A proteção contra fraudes no cartão de crédito chargeback deve estar em conformidade com as regras da Visa e da Mastercard, incluindo:

- Códigos de motivo

- Prazos de resposta

- Padrões de prova

Se um sistema de proteção não estiver em conformidade com as regras de conformidade do emissor, ele falhará na etapa mais onerosa: a recuperação.

Lojista Chargeback Proteção x Proteção contra fraudes: principais diferenças

A proteção contra fraudes e a proteção contra o “ chargeback ” estão relacionadas, mas não são a mesma coisa.

A proteção contra fraudes tem como objetivo impedir transações não autorizadas ou de alto risco antes da finalização da compra. A proteção contra fraudes de cartão ( Chargeback ) concentra-se no gerenciamento de fraudes de cartão ( disputas ) após a transação já ter ocorrido.

Principais diferenças:

| Função | Proteção contra fraudes | Chargeback Proteção |

|---|---|---|

| Palco | Pré-venda | Pós-venda |

| Disputa Cobertura | Apenas fraude | Fraude, fraude amigável, serviço “ ” disputas |

| Controle de proporção | Parcial | Direto |

| Representação | Não | Sim (modelos de ponta a ponta) |

Muitos Lojistas acreditam que as ferramentas antifraude são suficientes. Mas não são. As ferramentas antifraude Reduza transações não autorizadas. Elas não controlam Disputa índices de devolução decorrentes de reembolsos, problemas de entrega ou reclamações relacionadas a assinaturas.

Chargebacks s elegíveis versus inelegíveis sob a proteção da Lei de Proteção ao Consumidor de Crédito ( Chargeback )

Nem todos os veículos da linha “ chargebacks ” estão incluídos nos programas de proteção “ chargeback ”.

A elegibilidade depende de:

- O código de motivo “ chargeback ”

- O tipo de proteção implementada (apenas contra fraudes vs. de ponta a ponta)

- Se os dados e as políticas necessários estavam disponíveis no momento da compra

- Cumprimento dos requisitos operacionais e de documentação do prestador

Requisitos gerais:

- Códigos de motivo de fraude específicos

- Transações que atenderam a critérios de risco predefinidos

Casos comuns de inelegibilidade:

Chargebacks são frequentemente excluídos da proteção quando envolvem:

- Não recebimento disputas sem confirmação de entrega

- “Não corresponde à descrição” ou insatisfação com o produto disputas

- Cobranças duplicadas, faltas ou cancelamentos de assinatura

- Transações sem a documentação exigida ou sem as divulgações previstas nas políticas

Essa é uma das áreas mais mal compreendidas da proteção oferecida pelo programa “ Lojista ”. A cobertura é condicional. Não é universal.

Quais informações o site Lojistas deve fornecer para a proteção do Chargeback

Chargeback A proteção é condicional. A cobertura depende da capacidade do “ Lojista” de fornecer dados precisos e verificáveis que atendam aos requisitos da seguradora e do prestador de serviços.

A maioria dos programas de proteção do tipo “ chargeback ” exige que o “ Lojistas ” mantenha:

- Descrições precisas de cobrança que Identifique em claramente a empresa

- Políticas claras de reembolso e cancelamento são exibidas antes da finalização da compra

- Comprovante de entrega ou acesso, quando aplicável

- Registros de comunicação com o cliente, incluindo confirmações e interações de suporte

- Dados de autenticação e transação, como endereço IP, dispositivo ou detalhes de login

A omissão das informações exigidas pode invalidar a cobertura de proteção, mesmo quando a decisão de não divulgação ( Disputa ) subjacente for justificável. Em muitos casos, a proteção é negada não porque a decisão de não divulgação ( Lojista ) estivesse errada, mas porque os dados exigidos estavam faltando, estavam incompletos ou não estavam disponíveis no momento da análise.

Chargeback Seguro de proteção e modelos de cobertura

Algumas proteções do tipo “ chargeback ” Soluções funcionam como modelos de cobertura semelhantes aos de seguros.

Esses modelos normalmente:

- Aprovar ou recusar transações no momento do pagamento

- Garantia de reembolso para pedidos aprovados

- Cobrar taxas com base no volume de transações, na taxa de aprovação ou no perfil de risco

Embora um seguro de proteção contra chargeback s possa Reduza o risco financeiro, ele não necessariamente Reduza:

- Chargeback volume

- Carga de trabalho operacional

- Monitoramento dos riscos do programa

Lojistas deve entender se uma solução de proteção:

- Evita que ocorra o erro “ disputas ”

- Reembolsar as perdas após a ocorrência de um “ disputas ”

- Gerencia todo o processo de “chargeback ” de ponta a ponta

O seguro protege a receita. Ele não protege automaticamente os índices.

Lojistas deve avaliar se uma solução:

- Previne disputas

- Indeniza as perdas

- Gerencia o processo de “ chargebacks ” de ponta a ponta

As melhores opções de proteção contra o “ Chargeback ” para empresas de comércio eletrônico

As melhores opções de proteção contra o “ chargeback ” dependem dos Disputa , da tolerância ao risco e da capacidade operacional.

Comparação entre modelos de proteção:

| Tipo de proteção | Previne disputas | Índice de controle | Reembolsa a perda | Gerencia reclamações |

|---|---|---|---|---|

| Garantias contra fraudes | Sim (apenas em caso de fraude) | Parcial | Sim | Não |

| Alertas | Parcial | Sim | Não | Não |

| Plataformas completas | Sim | Sim | Opcional | Sim |

Plataformas de prevenção de fraudes com garantias

Ideal para Lojistas que enfrentam principalmente problemas relacionados à fraude chargebacks. Essas soluções Reduza tratam de transações não autorizadas, mas não abordam problemas de serviço disputas nem a “fraude amigável”.

Chargeback Alertas e as ferramentas Rede

Ideal para intervenção precoce. Alertas oferece um prazo para reembolso antes que disputas seja finalizado. A cobertura depende da participação da operadora.

Plataformas de proteção de e- chargeback , de ponta a ponta

Ideal para empresas de “ Lojistas ” que enfrentam um alto volume de “ Disputa ” relacionadas a fraudes, fraudes não intencionais e reclamações de serviço.

Esses itens combinam:

- Detecção de fraudes

- Alertas

- Reconciliação de reembolsos

- Representação Automação

- Análise de desempenho

A melhor proteção contra o “ chargeback ” não se resume apenas ao reembolso. Ela é definida pela eficácia com que controla o volume de “ Disputa ” e protege a estabilidade do processamento a longo prazo.

O que realmente significa “a melhor proteção contra o chargeback ”

A melhor proteção contra o chargeback não se resume a um único recurso. Ela é definida pela eficácia com que uma solução:

- Isso reduz o volume d Disputa

- Isso protege sua relação entre Disputa

- Isso limita a exposição financeira

- É escalável em termos operacionais

Lojistas Taxas inferiores a 0,3% Disputa podem se sustentar com fraudes, além de Alertas.

Lojistas . Valores próximos aos limites de monitoramento exigem modelos que priorizem a relação, e não o reembolso.

O site Soluções pode ajudar a Reduza identificar riscos específicos.

Sistemas abrangentes garantem a estabilidade dos pagamentos a longo prazo.

Chargeback Proteção contra fraudes e redução de riscos

Chargeback A proteção contra fraudes tem como objetivo reduzir o “ disputas ” causado por:

- Uso de cartões roubados

- Apropriações de contas

- Fraude por parte de conhecidos

Uma proteção eficaz contra fraudes no chargeback inclui:

- Verificação de identidade e de dispositivo

- Análise comportamental

- Monitoramento de transações

- Validação do uso e do cumprimento após a compra

A prevenção de fraudes reduz uma das principais categorias de disputas, mas deve ser combinada com a proteção pós-compra para controlar totalmente o risco de chargeback .

Principais causas da doença de Chargebacks e como a proteção ajuda

A maioria dos chargebacks se enquadra em um pequeno número de categorias recorrentes. Compreender essas causas ajuda Lojistas a escolher a abordagem correta de proteção chargeback .

As causas comuns da doença de chargebacks , incluem:

- disputas es decorrentes de fraudes envolvendo cartões roubados ou invasão de contas

- Fraude involuntária, em que os titulares dos cartões não reconhecem ou não se lembram de uma compra

- Reclamações por não recebimento decorrentes de problemas ou atrasos na entrega

- Disputa o com o produto ou serviço, como “não corresponde à descrição” ou insatisfação

- disputas es sobre assinaturas e cobranças relacionadas a termos pouco claros ou cancelamentos

Chargeback A proteção contribui para resolver essas causas em diferentes etapas do ciclo de vida da transação.

Como a proteção “ chargeback ” reduz o risco:

- A proteção contra fraudes reduz as transações não autorizadas antes da finalização da compra

- Chargeback Alertas permitir uma intervenção precoce antes que disputas a situação se agrave

- O site Refund Automação resolve problemas antes que os bancos sejam envolvidos

- Disputa As ferramentas de gerenciamento garantem que os disputas válidos sejam defendidos corretamente

Nenhuma ferramenta isolada elimina todos os desafios. A proteção funciona melhor quando se concentra nos fatores específicos por trás de um Lojista’s disputas.

O impacto das altas taxas de “ Chargeback ” sobre Lojistas

As altas taxas de “ chargeback ” afetam muito mais do que apenas a receita de curto prazo.

Quando os limites do chargeback são excedidos, o Lojistas pode enfrentar:

- Inclusão nos programas de monitoramento da Visa ou da Mastercard

- Taxas de processamento mais altas e reservas contínuas

- Maior rigor por parte dos bancos adquirentes

- Limitações quanto à disponibilidade de formas de pagamento

- Encerramento de contas do Lojista em casos graves

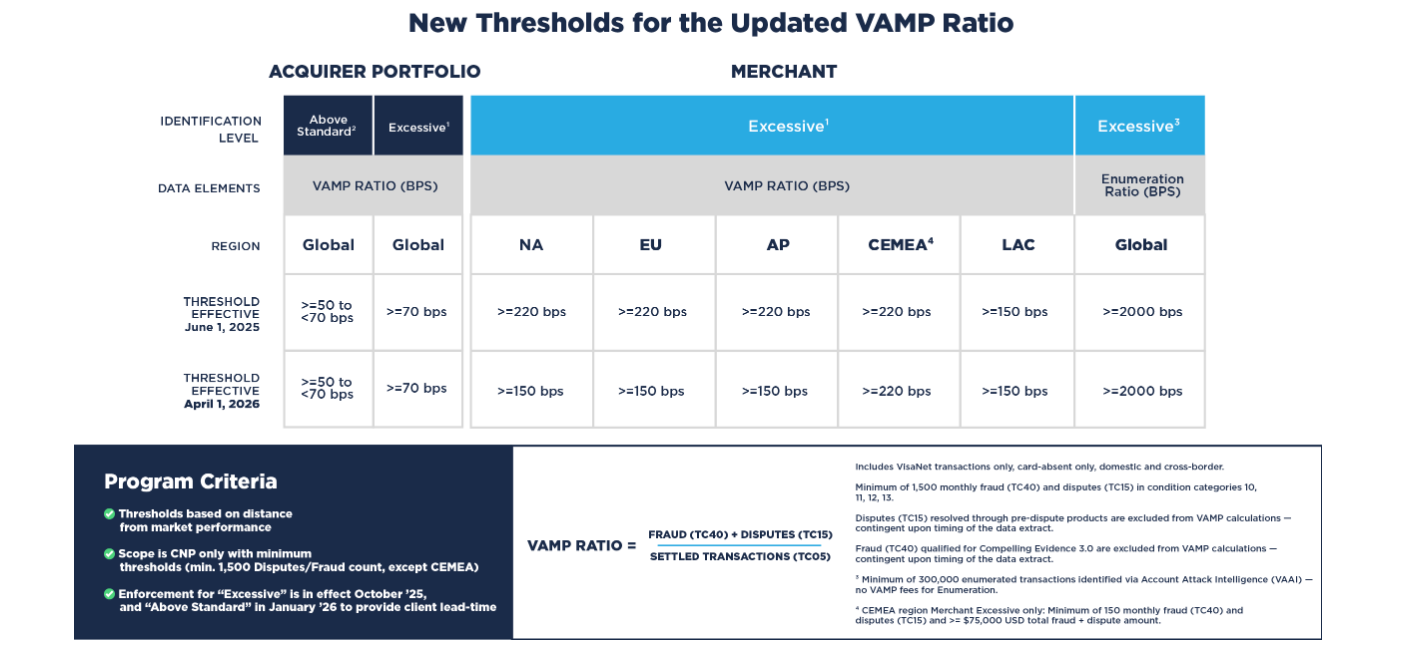

Os limites atualizados do programa VAMP da Visa para 2025 e 2026 tornam significativamente mais restritivos os índices aceitáveis de “ Disputa ”.

As emissoras avaliam o programa “ Lojistas ” de forma automatizada. Os prazos e os índices são determinados pelo sistema e não são negociáveis.

A seguir, apresentamos um detalhamento dos limites atualizados do VAMP da Visa para 2025-2026, ilustrando como os índices de “ Disputa ” (VAMP) são agora avaliados globalmente.

Mesmo Lojistas que obtêm disputas individuais podem sofrer penalidades se o volume geral chargeback continuar alto.

É por isso que a proteção contra a falência chargeback e não se resume apenas à recuperação. Trata-se de controlar índices, manter a conformidade e proteger o acesso a pagamentos a longo prazo.

No comércio eletrônico Lojistas, taxas elevadas e persistentes de chargeback são um dos caminhos mais rápidos para a instabilidade no processamento.

Aspectos-chave de uma estratégia eficaz de proteção contra o vírus da gripe suína ( Chargeback )

Uma estratégia eficaz de proteção contra o chargeback é multifacetada e planejada. Ela não depende de uma única ferramenta ou promessa.

Entre as estratégias eficazes estão:

- Verificação de fraudes antes da compra

- Políticas claras de reembolso e cancelamento

- Chargeback Alertas

- Reconciliação automatizada de reembolsos

- Representação estruturada

- Acompanhamento de desempenho

A prevenção deve sempre ter prioridade sobre a recuperação. Cada chargeback evitado protege os índices de desempenho, a confiança no processador e a receita futura.

Chargebacks não podem ser eliminados. Mas podem ser controlados.

Chargeback Proteção tem a ver com controle, não apenas com cobertura

Chargeback A proteção é frequentemente confundida com seguro ou reembolso.

Na verdade, a proteção mais valiosa é aquela que dá ao Lojistas o controle.

Controle sobre:

- Quais transações são aceitas

- Como são tratadas as “ disputas ”

- Chargeback índices e risco de conformidade

- Estabilidade dos pagamentos a longo prazo

Lojistas aquelas que dependem exclusivamente do reembolso podem recuperar receitas, mas ainda assim perder o acesso ao processamento.

A melhor proteção contra fraudes do tipo “ chargeback ” para empresas de comércio eletrônico combina detecção de fraudes, Alertas antecipada, fluxos de trabalho automatizados Disputa e visibilidade do desempenho em um único sistema operacional.

Compreender o que é a proteção contra fraudes de cartão de crédito ( chargeback ) — e o que ela não é — permite que Lojistas escolha Soluções que protejam a receita hoje e o acesso ao processamento amanhã.

Assuma o controle do seu risco de “ Chargeback ”

Chargeback A proteção não se resume a reagir mais rapidamente. Trata-se de construir um sistema que evite erros evitáveis disputas, controle os índices e proteja a estabilidade do processamento a longo prazo.

Se a sua taxa de “ Disputa ” estiver aumentando, se os limites de monitoramento estiverem se tornando mais restritivos ou se as equipes internas estiverem sobrecarregadas com fluxos de trabalho manuais, talvez seja hora de avaliar se o seu modelo de proteção atual realmente protege seus índices.

Agende uma demonstração para ver como a proteção automatizada contra o “ chargeback ” pode Reduza Disputa volume, garantir o cumprimento dos limites de conformidade e recuperar receitas em grande escala.

Obtenha uma proteçã Chargeback e que realmente funcione

Você pode recuperar a receita perdida devido a chargebacks , em vez de contabilizar cada Disputa como prejuízo. Chargeflow automatiza a coleta e o envio de provas de ponta a ponta, com a garantia de um ROI quatro vezes maior.

Comece de graçaChargebacks?

Não é mais problema seu.

Recupere 4 vezes mais chargebacks e PREVENÇÃO — até 90% dos e-mails recebidos —, com tecnologia de IA e uma rede global Rede de 20.000 Lojistas.

.png)