%201.svg)

Estornos da Amex: O guia definitivo para prevenir e resolver disputas em 2026

Estornos?

Não são mais um problema para você.

Recupere 4 vezes mais estornos e evite até 90% dos estornos recebidos, com o apoio da IA e de uma rede global de 20.000 comerciantes.

Os estornos da Amex deixam pouco margem para erros aos comerciantes: o processo é centralizado, o prazo para resposta é curto e os programas de monitoramento podem restringir os direitos de pagamento. Os titulares de cartão geralmente têm 120 dias para contestar uma cobrança, e os comerciantes normalmente têm 20 dias para responder. Como comerciante, você precisa de medidas de prevenção, coleta de provas e um processo de resposta a contestações elaborado para cumprir os prazos e os requisitos de documentação da Amex.

- Amex disputes move faster and with less back-and-forth than Visa/Mastercard chargebacks because Amex is both network and issuer.

- Merchants typically have only 20 days to respond with evidence once notified - shorter than many other networks.

- Common Amex reason codes include fraud (Chargeback Codes 4526/F24), goods/services not received (C08), and credit not processed (C05).

- Proactively managing Amex disputes with automated evidence submission reduces response-time risk and revenue loss.

An Amex chargeback (called a "dispute" by American Express) lets cardholders reverse a charge directly with Amex, since Amex acts as both card network and issuing bank. Merchants have a limited window (typically 20 days) to respond with compelling evidence before the dispute defaults in the cardholder's favor.

| Passo | Quem | Ação | Cronograma típico |

|---|---|---|---|

| 1. Reclamação apresentada | Titular do cartão | Contacts Amex online or by phone to dispute a charge | Within 120 days of transaction |

| 2. O comerciante foi notificado | Amex | Sends dispute notice with reason code to merchant | 1-3 business days |

| 3. Provas apresentadas | Comerciante | Uploads receipts, delivery confirmation, correspondence | 20 days from notice |

| 4. Amex reviews | Amex | Avalia as evidências em relação aos critérios do código de motivo | 7 a 30 dias |

| 5. Resolução | Amex | Charge reinstated to merchant or refund stands with cardholder | Varia |

A American Express é a terceira maior rede de cartões dos Estados Unidos. A Amex é aceita em mais de 160 milhões de estabelecimentos em todo o mundo e processou mais de US$ 1,67 trilhão em transações faturadas em 2025. É também a rede de cartões que a maioria dos comerciantes menos compreende, e essa lacuna tem um custo elevado.

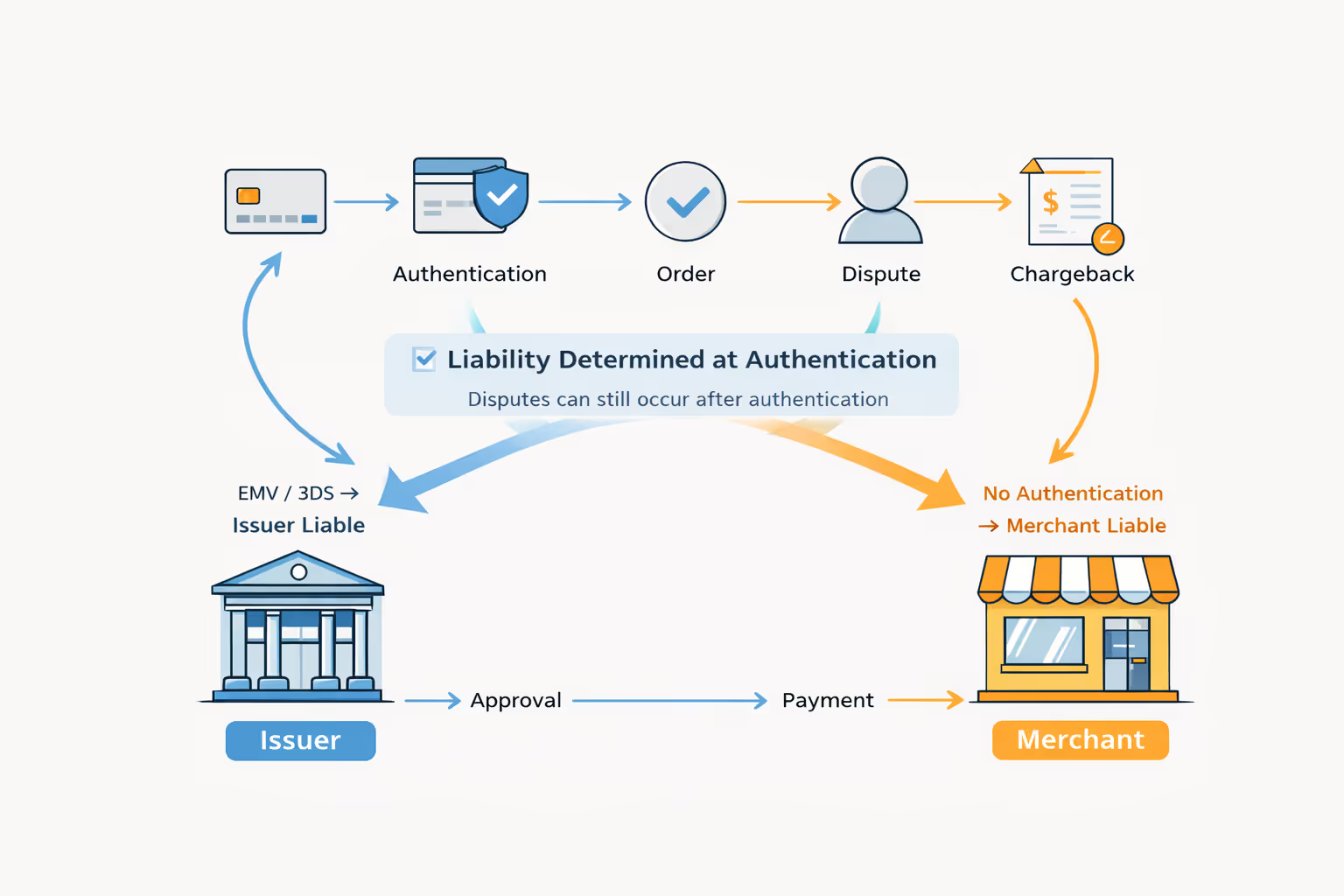

Ao contrário da Visa ou da Mastercard, a Amex costuma atuar tanto como rede quanto como banco emissor, por isso controla a maior parte do processo de estorno. Os titulares de cartão geralmente têm até 120 dias para contestar uma cobrança, com poucas oportunidades para tentativas adicionais. Os comerciantes normalmente têm 20 dias para responder, um prazo menor do que o de qualquer outra grande rede, e exatamente uma única chance de resolver a questão corretamente.

Se você perder esse prazo, não responder adequadamente ou ultrapassar os limites relacionados aos índices de fraude e estornos, poderá acabar sendo incluído em um dos três programas de monitoramento punitivos, cuja existência muitos comerciantes só descobrem depois de terem sido inscritos. Para lidar com os estornos da Amex, é preciso primeiro entender o panorama geral.

Como funcionam os estornos da American Express

Um estorno da Amex é uma reversão forçada de transação iniciada pelo titular do cartão e processada dentro do sistema de circuito fechado da Amex, no qual a Amex atua simultaneamente como rede de cartões, emissora e principal tomadora de decisões.

Como a Amex tem acesso a ambos os lados da transação, ela possui maior visibilidade do que as redes que dependem de bancos emissores distintos. A Visa e a Mastercard dependem de bancos membros que nem sempre têm a mesma visibilidade sobre as transações.

Essa estrutura tem vantagens e desvantagens. A American Express informa que, em 2025, apenas uma pequena fração das transações com cartão resultou em contestações que chegaram aos comerciantes. Isso sugere uma análise interna rigorosa por parte da empresa. Para os comerciantes, isso significa que as contestações que chegam não são reclamações aleatórias, mas casos que a Amex já analisou e decidiu que valem a pena ser encaminhados.

A Amex também está em melhor posição para identificar padrões como a fraude amigável, pois consegue correlacionar o comportamento dos titulares de cartão entre os diferentes estabelecimentos. No entanto, seu processo de contestação ainda tende a favorecer o titular do cartão. E os estabelecimentos têm capacidade limitada para contestar a classificação interna da Amex uma vez que o caso seja definido.

Entendendo o processo de estorno da American Express

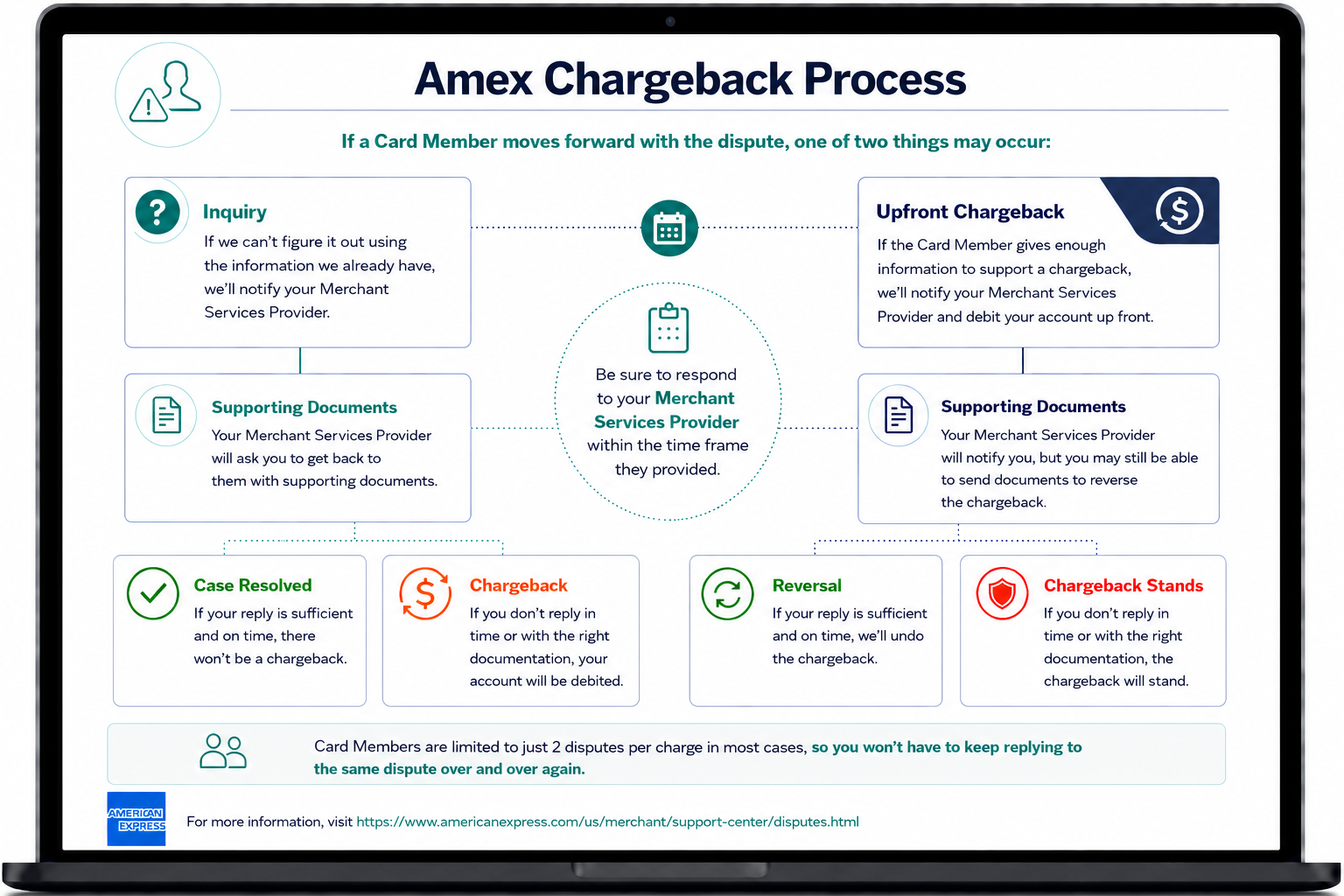

Quando um titular de cartão contesta uma cobrança, a Amex pode indeferir a reclamação, enviar uma consulta ao comerciante ou emitir um estorno imediato. A fase de consulta, quando ocorre, é a melhor oportunidade que o comerciante tem de encerrar o caso antes que ele se transforme em um estorno. A Amex envia uma consulta quando precisa de mais informações; ela pode pular essa etapa quando a reclamação parece fundamentada à primeira vista, quando há suspeita de fraude ou quando o comerciante já está inscrito em um programa de monitoramento.

Se for enviada uma consulta, o comerciante tem 20 dias a partir da data de processamento da Amex, conhecida como “Central Site Business Date”, para responder. Essa data é definida quando a Amex processa o caso, e não quando o comerciante vê a notificação pela primeira vez; portanto, atrasos internos podem reduzir silenciosamente esse prazo. Uma resposta inadequada ou tardia permite que o estorno prossiga.

Uma vez que um estorno da Amex seja emitido e confirmado, os fundos são debitados, e a decisão é difícil de contestar. Ao contrário da Visa e da Mastercard, que oferecem canais de recurso mais formalizados, o processo de estorno da Amex deixa os comerciantes com poucas opções para uma revisão posterior. Uma nuance importante é que os comerciantes que processam transações da Amex por meio de uma operadora terceirizada (OptBlue) seguem os procedimentos de contestação dessa operadora, que podem diferir das regras diretas da Amex. A imagem abaixo destaca o processo de estorno da Amex:

Por que os titulares de cartões Amex solicitam estornos: códigos de motivo de estorno da American Express

Cada estorno da American Express vem acompanhado de um código de motivo que identifica por que o cliente contestou a transação e que tipo de prova é relevante. A Amex agrupa esses códigos em várias categorias principais:

- Códigos de autorização da série A , que abrangem problemas como autorização ausente ou inválida.

- Códigos de contestação de titulares do cartão da série C, relativos a mercadorias não entregues, reembolsos ou cancelamentos.

- Códigos de fraude da série F, que são os mais difíceis de serem vencidos pelos comerciantes.

- Códigos diversos da série M, que abrangem discrepâncias relacionadas a valores, moedas e outros itens semelhantes.

- Códigos de fraude com recurso total da série FR, nos quais a capacidade do comerciante de contestar é fortemente limitada.

Para muitos comerciantes, as perdas mais evitáveis estão relacionadas às disputas da série C: descrições de cobrança pouco claras, processos de reembolso lentos ou pouco transparentes e procedimentos de cancelamento confusos. Lidar com essas questões de forma proativa costuma prevenir estornos de forma mais eficaz do que contestá-los após o fato.

Para obter um mapeamento detalhado de cada código e das evidências recomendadas, consulte nosso guia completo de códigos de motivo da Amex.

Prazos para estornos da Amex

Os prazos para estornos da Amex criam um dos cronogramas mais desequilibrados no setor de pagamentos com cartão.

Os titulares de cartão têm 120 dias a partir da data da transação para apresentar uma contestação. Para algumas categorias, esse prazo começa a contar a partir de eventos como a data prevista de entrega ou a data em que ficou evidente a falha no serviço, e não a partir da data da compra. Uma transação realizada em janeiro pode ser contestada meses depois.

Os comerciantes, por outro lado, têm 20 dias a partir da Data de Transação do Site Central para responder. Como esse prazo começa a contar a partir do momento em que a Amex processa o caso, e não quando o comerciante lê a notificação, qualquer atraso interno reduz o tempo real de resposta. Em comparação com os cerca de 30 dias da Visa e os 45 dias da Mastercard, o prazo de 20 dias da Amex oferece aos comerciantes a menor margem para compensar atrasos.

Depois que uma resposta é enviada, as contestações da Amex costumam levar várias semanas para serem resolvidas, período durante o qual o valor contestado ficará retido. Para os comerciantes, a lição prática é simples: confirme a Data Comercial do Site Central, calcule o prazo retroativo a partir dessa data e considere cada dia como inegociável.

Os três programas de monitoramento que a maioria dos comerciantes nem sabe que existem

A Amex opera três programas de monitoramento de comerciantes destinados a reduzir fraudes e gerenciar comerciantes com alto índice de contestação: o Programa de Recurso Total contra Fraudes, o Programa de Estorno Imediato e o Programa de Estorno Imediato Parcial.

Todos os três programas visam pressionar os comerciantes a tornarem mais rigorosas suas práticas de gestão de transações e contestação. Vamos analisá-los mais detalhadamente:

Programa de Recurso Total contra Fraudes

O programa de recurso contra fraudes da Amex é acionado quando o volume de transações fraudulentas ultrapassa os limites aceitáveis da Amex. Uma vez inscrito, a Amex pode aprovar estornos marcados como fraude de forma acelerada e rejeitará qualquer tentativa do comerciante de solicitar a reversão.

Na prática, você perde totalmente o direito de contestar disputas por fraude, mesmo quando tem certeza de que a transação original era legítima. A única exceção restrita: se você puder comprovar que eles já reembolsaram o titular do cartão pelo valor contestado, eles poderão apresentar documentação em resposta.

Requisitos para inscrição:

- Envolver-se em condutas comerciais fraudulentas, enganosas, colusivas ou desleais

- Envolvimento em atividades ilegais ou uso indevido do cartão

- Um índice de cobranças por fraude em relação ao faturamento bruto (FTG) que ultrapasse o limite do Nível Baixo ou do Nível Alto

O programa de ressarcimento total por fraude está dividido em níveis baixo e alto.

Nível inferior

Condições (ambas devem ser atendidas):

- Índice mensal de fraudes igual ou superior a 0,9% do valor bruto das cobranças

- Contestações por fraude que totalizem pelo menos US$ 25.000 em um único mês

O que acontece: as restrições entram em vigor após o comerciante permanecer acima do limite por três meses consecutivos a partir da notificação da Amex. A partir desse momento, o comerciante fica sujeito a estornos com responsabilidade total por fraude e perde qualquer proteção contra responsabilidade por fraude anteriormente concedida pelo SafeKey.

Como sair do programa: Você deve reduzir sua taxa FTG para menos de 0,9% e manter o valor total das disputas por fraude abaixo de US$ 25.000 por três meses consecutivos. A Amex também se reserva o direito de excluir comerciantes unilateralmente.

Nível Superior

Condições (ambas devem ser atendidas):

- Índice mensal de fraudes igual ou superior a 1,8% do valor bruto das cobranças

- Contestações por fraude que totalizem pelo menos US$ 50.000 em um único mês

O que acontece: Ao contrário do Nível Baixo, não há período de carência. As restrições entram em vigor imediatamente após a notificação da Amex. O comerciante perde imediatamente os direitos de contestação de estornos e a proteção de responsabilidade do SafeKey.

Como sair: Da mesma forma que no Nível Baixo: FTG inferior a 0,9% e disputas por fraude inferiores a US$ 25.000 por três meses consecutivos. A Amex também pode excluir comerciantes a seu critério.

Programa de estorno imediato

Este programa se aplica a comerciantes cuja taxa geral de estornos — e não apenas a de fraudes — se mantém consistentemente elevada. Quando um comerciante ultrapassa o limite de taxa de estornos da Amex por três meses consecutivos, a Amex elimina a etapa padrão de consulta. Em vez de enviar ao comerciante uma solicitação de esclarecimento para que ele responda, a Amex processa o estorno imediatamente utilizando um código de motivo específico. O programa costuma indicar que o comerciante está utilizando métodos inadequados de detecção de fraudes ou não implementou medidas básicas de segurança nas transações.

A taxa de estorno é calculada da seguinte forma: (Estornos) ÷ (Valor bruto das cobranças − Créditos)

Os débitos brutos correspondem ao total das transações liquidadas, enquanto os créditos correspondem aos reembolsos emitidos.

Consequências da inscrição:

- A Amex pode ignorar o processo de investigação e emitir um estorno diretamente sempre que um titular de cartão contestar uma cobrança por qualquer motivo que não seja fraude.

- Uma taxa de estorno excessivo é aplicada a cada estorno processado assim que a taxa de estornos do comerciante ultrapassar o limite de 1%.

Programa de estorno parcial imediato

Este programa funciona de maneira semelhante ao Programa de Estorno Imediato, mas introduz um limite para o valor das transações. Os comerciantes que ultrapassarem o limite de estornos por três meses consecutivos são inscritos no programa, mas a isenção de investigação se aplica apenas a contestações envolvendo transações com valor inferior a um montante específico em dólares.

As disputas relativas a transações de valor mais elevado continuam a seguir o processo normal de estorno e investigação da Amex. Isso cria um sistema de duas vias: estornos acelerados para transações de menor valor e procedimentos padrão para as de maior valor.

Aplica-se a mesma fórmula de cálculo da taxa: (Estornos) ÷ (Valor bruto das cobranças − Créditos)

Consequências da inscrição:

- As contestações relativas a transações abaixo do limite em dólares podem ser estornadas imediatamente, sem necessidade de investigação, por qualquer motivo que não seja fraude.

- As contestações relativas a transações que atinjam ou ultrapassem o limite seguem o processo padrão de estorno e investigação da Amex.

- A taxa de estorno excessivo se aplica a cada estorno que ultrapasse o limite máximo de 1%.

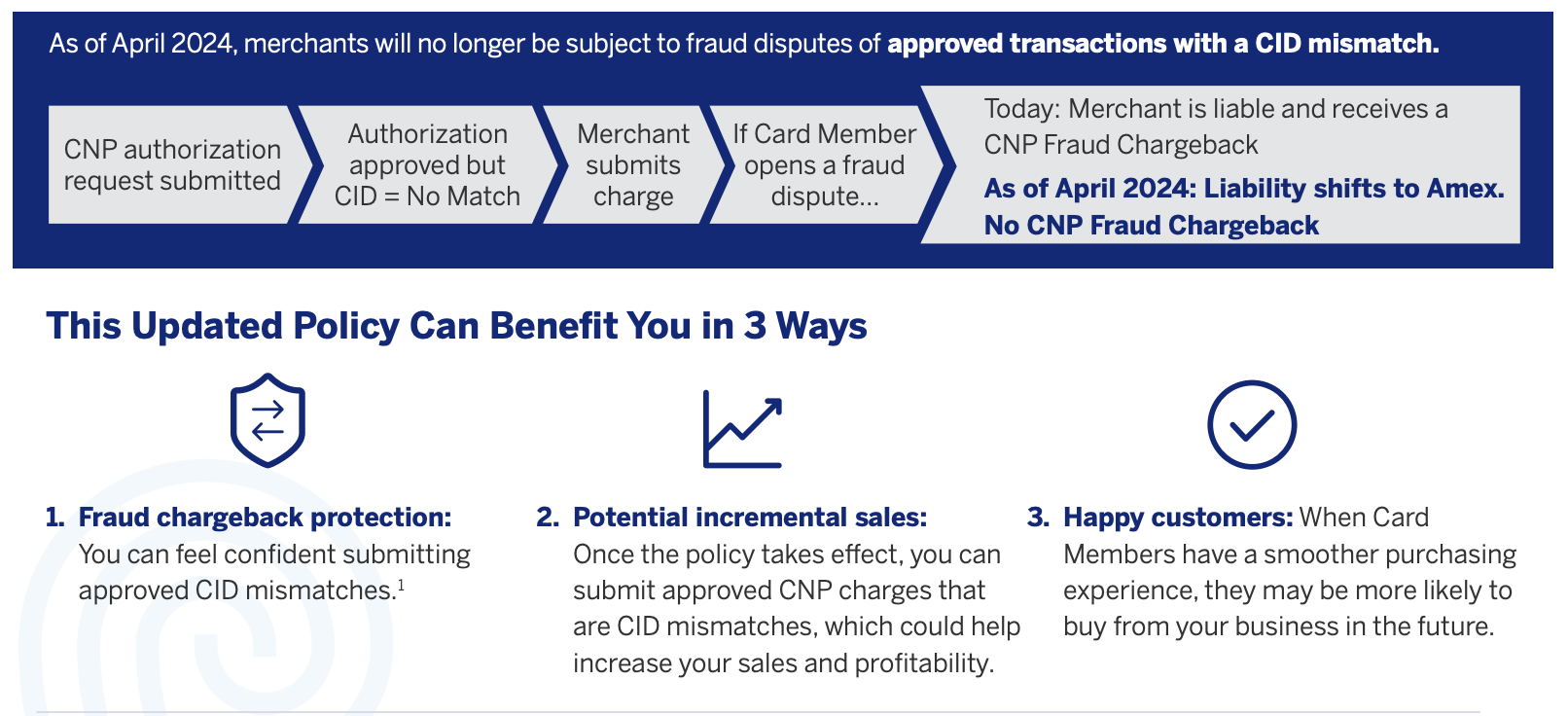

Atualização da Política do CID para 2024: a transferência de responsabilidade da Amex que você talvez não tenha percebido

Em abril de 2024, a Amex introduziu uma atualização na política de CID que isenta os comerciantes da responsabilidade por fraudes em determinados cenários de transações sem a presença do cartão. Quando um comerciante obtém uma autorização válida para uma transação online, tenta realizar uma verificação de CID e recebe uma resposta indicando incompatibilidade, como “sem correspondência”, “não verificado” ou “sem resposta”, a Amex afirma que irá anular as disputas por fraude que se enquadrem nos critérios, em vez de repassá-las como estornos.

O que mudou

Antes desta atualização, um comerciante ainda poderia ser responsabilizado por um estorno por fraude nesse cenário, mesmo após uma autorização válida. A alteração permite que os comerciantes enviem pedidos aprovados com discrepância de CID com mais confiança, desde que tenham implementado a lógica adequada de autorização e finalização de compra.

Por que você deve se importar

O efeito prático dessa mudança na política é que os comerciantes podem ficar menos preocupados com a possibilidade de perder bons pedidos no momento do checkout apenas porque a verificação do CID falhou, o que pode reduzir o abandono de carrinhos e preservar as vendas. Isso também diminui o risco de que uma transação aprovada venha a ser contabilizada posteriormente como parte do volume de fraudes ou estornos do comerciante nos cenários específicos abrangidos pela política.

A Amex descreve a mudança como aplicável a transações autorizadas sem a presença do cartão. O comerciante tentou a validação do CID e recebeu uma resposta de incompatibilidade, como “sem correspondência”, “não verificado” ou “sem resposta”. O informativo indica que “transações aprovadas com incompatibilidade de CID” não darão mais origem a estornos por fraude em transações sem a presença do cartão a partir de abril de 2024.

Limites importantes

Isso não significa uma imunidade geral para todas as contestações. A política se refere a um cenário específico de estorno por fraude relacionado à incompatibilidade do CID e ao status de aprovação, e não a todos os códigos de motivo possíveis ou a todos os tipos de contestação. Além disso, o comerciante ainda precisa utilizar a lógica adequada de autorização e finalização da compra. A Amex observou que os comerciantes podem precisar atualizar os fluxos de pagamento para deixar de solicitar novamente o CID e aceitar incompatibilidades.

A atualização não elimina totalmente o risco de fraude; ela apenas altera quem assume esse risco no caso de discrepância de CID coberta. Portanto, a questão não é tanto que “a Amex tenha eliminado os estornos”, mas sim que “a Amex transferiu a responsabilidade por uma categoria específica de transações online aprovadas”.

Como contestar um estorno da American Express: um guia passo a passo

Para contestar um estorno da Amex, é preciso começar analisando o caso com atenção. É necessário compreender o código do motivo, o que a Amex está solicitando e se a contestação se refere a fraude, serviço ou outra questão. Qualquer falha nessa compreensão resulta em esforço desperdiçado e em provas menos sólidas.

O próximo passo é a coleta de provas. Na maioria dos casos, isso significa reunir dados de autorização, detalhes de pedidos e faturas, registros de entrega e comunicações relevantes com o cliente. O objetivo é apresentar uma documentação concisa e relevante que aborde diretamente o motivo da recusa, em vez de um pacote extenso, mas sem foco.

O cumprimento dos prazos também é fundamental em todas as etapas. Como os prazos da Amex são apertados, os fluxos internos e as aprovações devem ser planejados de acordo com o prazo de 20 dias. Equipes que dependem de trocas de e-mails pontuais ou transferências informais de tarefas correm maior risco de não cumprir os prazos ou enviar respostas incompletas.

Onde a automação se encaixa e por que o setor está migrando para ela

A automação de estornos se encaixa naturalmente na estrutura da American Express, pois ajuda os comerciantes a responderem em tempo hábil e a manterem o gerenciamento de contestações organizado. As próprias orientações da Amex destacam as ferramentas automatizadas de resolução de contestações como uma forma de otimizar os fluxos de trabalho, reduzir o trabalho manual e melhorar os resultados para comerciantes e clientes.

Para os comerciantes, o valor da automação reside menos na substituição das pessoas e mais no apoio a elas. O tratamento manual de disputas pode funcionar quando o volume é baixo, mas torna-se difícil de sustentar à medida que os casos aumentam ou quando o trabalho relacionado a estornos passa a competir com outras prioridades. Um sistema estruturado ajuda as equipes a evitar atrasos, manter a consistência e aprender com disputas anteriores, em vez de tratar cada caso como um evento isolado.

A lição prática é que, para vencer disputas com a Amex, raramente basta um único documento perfeito. O importante é ter um processo padronizado que garanta que as provas certas cheguem ao caso certo antes do prazo final e utilizar a automação para tornar esse processo confiável em grande escala.

Como evitar estornos da American Express antes que eles ocorram

A maioria dos guias sobre prevenção de estornos apresenta a mesma lista: descrições claras nas faturas, e-mails de confirmação e uma política de reembolso fácil de encontrar. Essas recomendações não estão erradas. Mas, no caso da Amex, elas são incompletas — e recomendações incompletas podem sair caras.

O que realmente importa é o seguinte:

A fase de investigação é onde os estornos são resolvidos, desde que você se manifeste.

A Amex costuma enviar uma consulta antes de emitir um estorno quando uma contestação é ambígua. Uma resposta bem fundamentada encerra o caso por completo. Sem estorno registrado, sem impacto no índice, sem cobrança de taxa. Mesmo quando a Amex ignora a consulta, há um intervalo no nível da rede que você pode aproveitar para evitar uma contestação iminente. Os alertas de estorno notificam os comerciantes no momento em que uma contestação é iniciada, com um prazo de 24 a 72 horas para reembolsar e encerrá-la completamente. Duas etapas diferentes, a mesma oportunidade. A maioria dos comerciantes perde ambas devido a processos internos lentos.

Gerencie os índices, não apenas as disputas.

Os três programas de monitoramento descritos anteriormente não são acionados por estornos isolados. Eles são acionados por índices mantidos ao longo do tempo. Isso significa que sua estratégia de prevenção não pode ser reativa, analisando as contestações à medida que elas surgem e decidindo quais contestar. Quando seus números estiverem ruins o suficiente para você perceber o problema, talvez você já esteja em um programa que retira totalmente seus direitos de resposta.

Acompanhe seus números mensalmente, da mesma forma que a Amex faz. E intervenha antes que um pico se transforme em uma tendência. Use a análise acima para calcular mensalmente sua taxa de fraudes em relação ao faturamento bruto e sua taxa de estornos. Se algum desses indicadores estiver evoluindo na direção errada, trate isso como um problema de negócios, e não como uma questão do departamento de cobrança.

Saiba que a Amex já verificou a transação.

Quando um titular de cartão contesta uma cobrança junto à Visa ou à Mastercard, o banco emissor geralmente dispõe de dados limitados sobre a transação. A Amex, na qualidade de rede e emissora, tem acesso a ambos os lados da transação em tempo real desde o momento em que ela é processada. Não há lacunas de informação que possam ser exploradas nem manipulações que possam se sobrepor ao que o sistema já registrou.

Isso é importante para a forma como você elabora sua defesa, mas é ainda mais importante para a prevenção. Cada transação que você processa com a Amex deixa um registro completo. Inconsistências entre o que você apresenta como prova e o que a Amex já possui vão custar caro para você. Dados de transação precisos e completos no ponto de venda não são apenas um luxo. São a sua defesa futura. O Beard Club enfrentou isso diretamente. Suas perdas em disputas não se originaram de transações irregulares, mas de registros incompletos que não resistiram à análise da rede de cartões. Veja como eles resolveram o problema:

Saiba quais são os conflitos que você pode evitar e concentre-se neles.

Os códigos de fraude da série F apresentam uma taxa de aprovação de transações consideravelmente baixa. Não é possível prevenir fraudes reais apenas por meio de melhorias nos processos, e não é possível resolver a situação por meio de contestações depois que ela ocorre. A prevenção, nesses casos, é uma questão de detecção de fraudes, não de documentação.

As contestações da série C são diferentes. Essas perdas são, em grande parte, causadas por nós mesmos. Elas ocorrem porque um cliente não recebeu o que esperava, não conseguiu entrar em contato com alguém para resolver o problema ou não sabia como cancelar e decidiu que contestar era mais fácil do que ter uma conversa. Esses são problemas que podem ser resolvidos.

O objetivo é eliminar todos os motivos pelos quais um titular de cartão possa ligar para a Amex em vez de ligar para você.

Organize seus registros para o período de 120 dias.

A maioria dos comerciantes mantém registros de pedidos e comunicações por um período de 30 a 60 dias. Os titulares de cartões Amex têm 120 dias para apresentar uma reclamação e, em algumas categorias de contestação, esse prazo começa a contar após a data da compra. Um cliente que comprou algo em janeiro pode, legitimamente, solicitar um estorno em maio e, se você já tiver eliminado esses registros, o caso já estará encerrado.

Período mínimo de retenção para todas as transações processadas pela Amex: seis meses de dados de pedidos, confirmações de entrega, comunicações com o cliente e registros de autorização. Para empresas que operam com assinaturas, esse prazo se estende para abranger toda a relação de cobrança.

A prevenção tem um limite. O que acontece depois disso é ainda mais importante.

Mesmo uma empresa bem administrada ainda enfrentará estornos. A Amex tende a dar razão ao titular do cartão, o prazo para resposta é o mais curto do setor e a decisão é definitiva. A prevenção reduz o volume, mas não elimina o risco.

Os comerciantes que resolveram essa questão combinam a prevenção com um processo de resposta rápido e preciso o suficiente para lidar com o que a prevenção não consegue impedir. A American Express deixou isso bem claro: as ferramentas automatizadas de resolução de disputas estão transformando a forma como os comerciantes lidam com estornos, simplificando processos, aumentando a eficiência e gerando resultados tanto para os comerciantes quanto para seus clientes.

Previna o que puder. Automatize o resto com o Chargeflow.

How long do I have to respond to an Amex chargeback?

Merchants generally have 20 days from the date Amex notifies them of a dispute to submit compelling evidence, though exact windows can vary by reason code.

What is the difference between an Amex dispute and a Visa/Mastercard chargeback?

Amex handles disputes internally as both the card network and issuing bank, often resulting in faster resolution and fewer intermediary steps compared to Visa or Mastercard, which involve separate issuing and acquiring banks.

Can I win an Amex chargeback?

Yes - merchants who submit clear, timely evidence (proof of delivery, signed receipts, correspondence matching the reason code) can successfully reverse an Amex dispute back in their favor.

Stop Fighting Amex Chargebacks Manually

You can automate evidence collection and submission instead of tracking Amex deadlines by hand. Chargeflow submits on time, every time, backed by a 4X ROI guarantee.

Comece de graçaEstornos?

Não são mais um problema para você.

Recupere 4 vezes mais estornos e evite até 90% dos estornos recebidos, com o apoio da IA e de uma rede global de 20.000 comerciantes.

.png)