%201.svg)

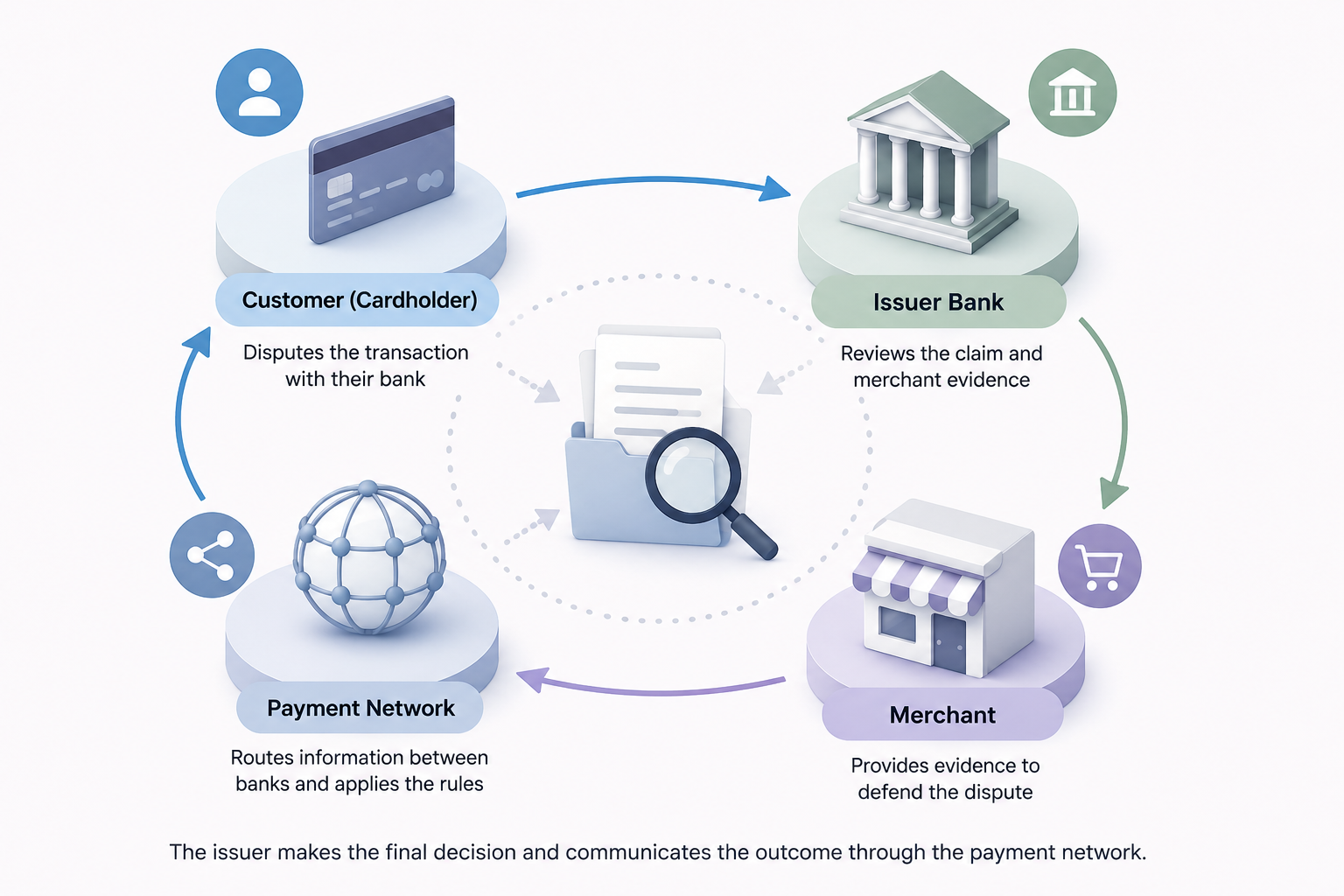

How Do Issuers Evaluate Chargeback Disputes?

Terugboekingen?

Dat is niet langer uw probleem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

Issuers evaluate chargeback disputes by comparing the cardholder’s claim against the merchant’s evidence, transaction data, and card network rules. Clear, relevant evidence tied directly to the dispute reason code usually matters more than volume.

Kort antwoord

When a customer files a chargeback, the issuing bank reviews the transaction details, the cardholder’s explanation, and any evidence submitted by the merchant. The issuer checks whether the merchant followed network rules, delivered what was promised, and responded with evidence that directly addresses the dispute reason.

Issuers are looking for consistency. If the transaction timeline, customer activity, and fulfillment records all match, merchants have a stronger chance of winning.

Stappen om het probleem op te lossen

1. Match Evidence to the Reason Code

Issuers do not evaluate disputes generically. They review them against the specific reason code attached to the claim.

Bijvoorbeeld:

- Unauthorized transaction disputes require login data, device information, or 3DS authentication.

- Item not received disputes require valid delivery confirmation.

- Subscription disputes require renewal disclosures and cancellation records.

2. Focus on Transaction Consistency

Issuers compare:

- Factuur- en verzendgegevens

- Communicatiegeschiedenis met de klant

- Device or IP data

- Purchase history

- Delivery timing

Any mismatch weakens the case quickly.

3. Submit Evidence Early

Late submissions are often ignored automatically by processors and card networks.

Chargeflow Automation can help merchants collect and submit evidence before issuer deadlines expire.

4. Keep Evidence Simple

Issuers review large volumes of disputes daily. Long explanations usually hurt more than help.

Use:

- Clear timelines

- Short summaries

- Organized screenshots

- Relevant receipts and tracking

5. Watch for Repeat Friendly Fraud Patterns

Issuers increasingly monitor repeat dispute behavior from cardholders.

Chargeflow Insights can help merchants identify repeat abusers, high-risk order patterns, and recurring dispute triggers.

Variaties in platform of gebruiksscenario’s

Streep

Stripe disputes often rely heavily on structured evidence fields. Missing required fields can weaken a case even if the merchant has valid proof.

PayPal

PayPal places strong weight on tracking confirmation, delivery status, and documented customer communication.

Digitale producten

Issuers usually expect:

- Login timestamps

- Usage records

- Download confirmations

- Device consistency

Digital goods disputes are harder to win without behavioral evidence.

Bewijs vereist

Issuers commonly expect:

- Orderbevestiging

- Payment authorization details

- AVS/CVV match results

- Proof of delivery or service

- Logboeken voor klantcommunicatie

- Refund or cancellation records

- Device/IP data

- Subscription acceptance records

- Tracking information

The strongest evidence directly disproves the customer’s claim.

Waarom dit gebeurt

Issuers are trying to determine whether the transaction followed card network rules and whether the cardholder’s claim is valid. Most disputes are evaluated quickly, so weak or incomplete evidence often leads to automatic losses.

The merchants who win more disputes are usually the ones submitting cleaner evidence faster, not longer explanations, and Chargeflow helps automate that process at scale.

Terugboekingen?

Dat is niet langer uw probleem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)

Meer artikelen.

Hoe kan ik op grote schaal herhaalde vriendelijke fraude opsporen?

Houd geschillen bij op basis van clusters van klantidentiteiten, en niet alleen op basis van ordernummers, en gebruik die patronen vervolgens om herhaaldelijk misbruik te blokkeren, te beoordelen of automatisch te documenteren voordat het zich verspreidt.

Vragen?

– wij hebben de antwoorden.

Chargeflow verzamelt gegevens uit tientallen externe bronnen, en niet alleen transactiegegevens zoals Stripe Dispute doet. Dit zorgt voor een veel bredere dekking en aanzienlijk hogere slagingspercentages, omdat het ingediende bewijsmateriaal veel uitgebreider en overtuigender is.

Chargeflow verzamelt gegevens zoals bestelinformatie, berichten van klanten en betalingsgegevens. Het stelt een volledig dossier voor geschillen voor je samen, zodat je er zelf geen vinger naar hoeft uit te steken.

Ja! Chargeflow werkt met veel betalingsverwerkers – niet alleen met Stripe. Dat betekent dat je één tool hebt voor al je terugboekingen, ongeacht hoe je betalingen verwerkt.

U betaalt alleen een percentage van de inkomsten die wij voor u binnenhalen. Geen kosten vooraf, geen abonnementen — alleen een succesafhankelijke vergoeding.

Ja. Chargeflow is SOC 2-, AVG- en ISO-gecertificeerd. We hanteren de strengste beveiligingsnormen om uw gegevens te beschermen.

Heb je nog meer hulp nodig?

Heb je een vraag? Wij staan voor je klaar. Klik gewoon op de chatknop om een gesprek met de klantenservice te starten.