%201.svg)

Barclays Chargebacks: How to Fight and Win Barclays Disputes

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

Barclays chargebacks reach US merchants through their processor as standard Visa or Mastercard disputes, with no indication Barclays is the issuing bank. The process has four stages (retrieval, chargeback, pre-arbitration, arbitration) each with deadlines that start before you open the letter. An authorisation code is not protection: one merchant lost £10,550 with authorisation codes and signed delivery proof, because neither addressed what the fraud reason code demanded. Win rates and transaction values determine which disputes are worth fighting. But the most expensive chargebacks are decided at checkout, before any dispute exists.

A UK merchant (named L in official documents) accepted 14 phone payments totalling £10,550 from a customer between April and May 2022. They obtained authorisation codes for each transaction, dispatched the goods, and recorded signed proof of delivery.

Then, in June 2022, Barclaycard debited L’s merchant account for the full £10,550, pushing them into overdraft. The reason? The customer had filed Barclays chargebacks.

L escalated to the Financial Ombudsman, arguing that obtaining authorisation meant the payments were verified, and that releasing goods on that basis made them blameless. They lost.

The Ombudsman found Barclaycard had acted within the card network rules. The authorisation L received only confirmed that funds were available and the card hadn’t been reported stolen, nothing more. It was never a guarantee of payment from the cardholder. The Barclays chargebacks were raised for card-not-present fraud, and a signed delivery receipt couldn’t prove the actual cardholder had authorised anything.

The jurisdiction is UK-specific, but the lesson isn't. Barclays operates as a card issuer in the US. American merchants may be on the receiving end of a Barclays chargeback without ever dealing with Barclaycard directly. But the card network rules that decided L's case and the gap between "authorised" and "protected" apply in the same way on both sides of the Atlantic.

Understanding Barclays Chargebacks and How It Works

In an industry where most merchants haven’t fully quantified the impact and have, therefore, accepted chargebacks as a fixed cost, it’s worth starting with a precise definition.

A Barclays chargeback is a dispute filed on a Barclays-issued card transaction that reaches you through your payment processor as a standard card network dispute. Barclays, as the issuing bank, makes the final call on whether the cardholder wins. hey do that within rules set by Visa or Mastercard, not by Barclays itself. The dispute arrives labelled with a Visa or Mastercard reason code, with no definitive indication that Barclays is the issuing bank behind it.

For UK merchants, Barclays enters as Barclaycard, your acquirer. They manage the dispute on your behalf, debit your merchant account, and decide whether to defend you within those same card network rules.

That last point matters. When the Financial Ombudsman ruled against merchant L, Barclaycard's defence was simple: they had acted within card network rules. Not their rules. Visa and Mastercard's rules. Those are the rules your evidence must satisfy.

How the Barclays Chargeback Process Works

One key reason the Barclays chargeback process catches merchants off guard is that you don’t always see it specifically labelled as a Barclays dispute. Barclays is the 9th largest card issuer in the US, with more than 20 million cardholders across co-branded programs with JetBlue, GM, Wyndham, and Carnival.

Every one of those cards is a potential chargeback that reaches you labelled as a Visa or Mastercard dispute, with no visible indication that Barclays is the issuing bank. You cannot readily identify it, track it, or build a response strategy around it unless you understand how the process works.

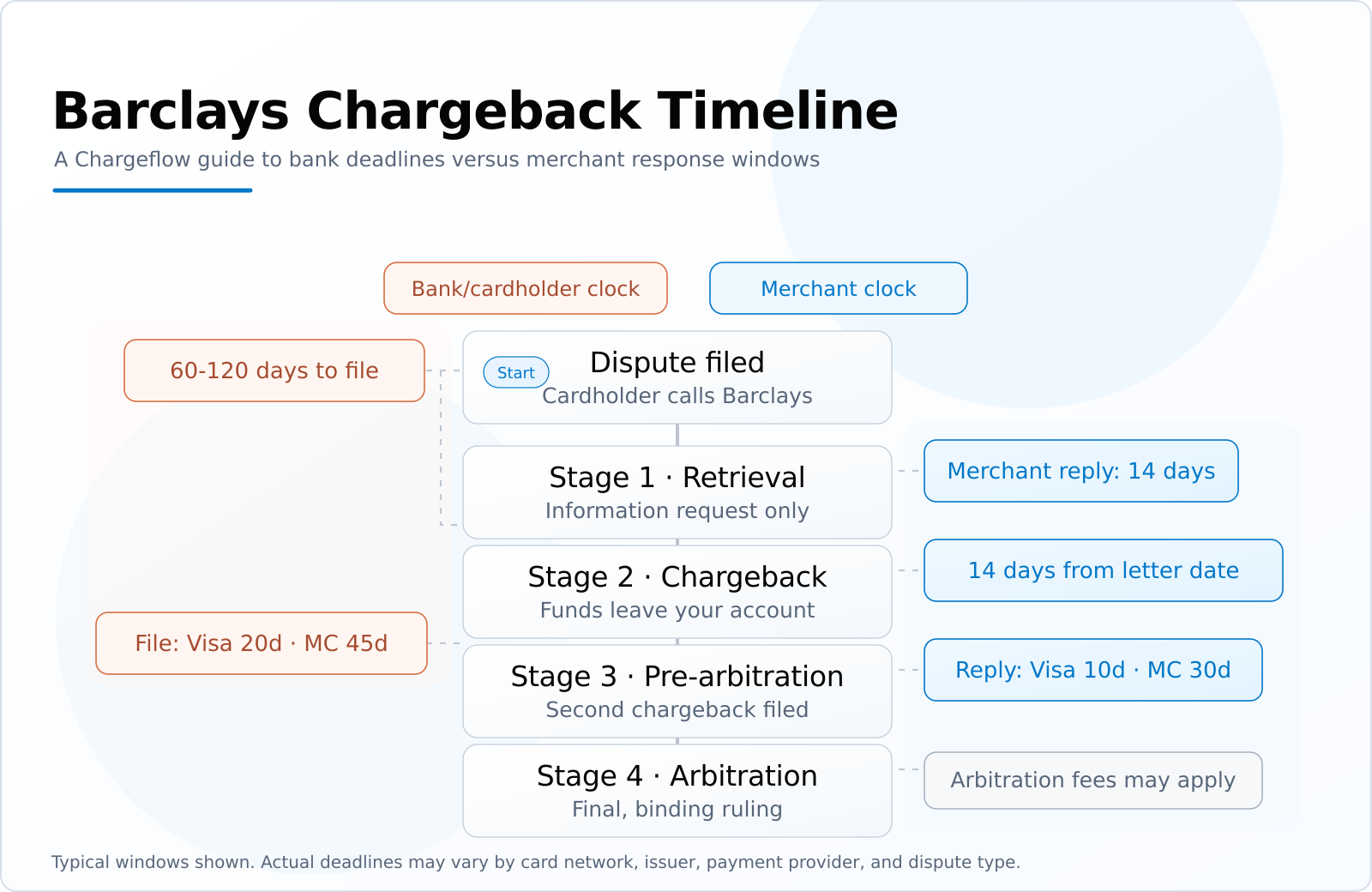

The Barclays Chargeback Process in Four Stages:

Stage one: Retrieval. Before a chargeback is formally raised, the card issuer may ask you to provide additional transaction details. No money moves at this stage. The trap is this: some retrieval requests still result in a chargeback even when the merchant has supplied supposedly correct information. A complete, accurate response is necessary. It is not always sufficient.

Stage two: Chargeback. Sometimes the retrieval stage is skipped entirely, and the Barclays dispute moves directly to a chargeback. The disputed amount is debited from your account, and you have 14 days (from the date on the letter) to respond with evidence. Not from the date you receive the letter. From the date it was written.

Stage three: Pre-arbitration or Second chargeback. Winning your representment does not always end the Barclays dispute. If Barclays, acting on the cardholder's behalf, disagrees with the outcome, it can file a second chargeback (known as a pre-arbitration) to challenge the ruling. This generally happens when the cardholder presents new or stronger documentation to Barclays. At that point, you can accept liability and close the case, or escalate to arbitration.

Stage four: Arbitration. If neither party backs down during pre-arbitration, the case can be escalated to the card network to make a final, binding decision. The losing party pays the disputed amount and arbitration fees. We’ve covered the timelines and fees involved in these subsequent stages in previous guides on Mastercard chargebacks and Visa chargebacks.

Barclays Chargeback Reason Codes

Every Barclays chargeback carries a reason code assigned by the card network. This number tells you why the transaction is disputed. Like all chargeback reason codes, it determines what evidence you need, how strong your defence can be, and in some cases, whether your acquirer can defend you at all.

Barclays chargeback reason codes fall into four categories: fraud, authorisation, processing errors, and consumer disputes. Each group has a different defensibility profile that you must examine carefully.

Fraud Reason Codes

You receive fraud codes on chargebacks where the cardholder denies they authorised or participated in the transaction. This is the highest-stakes category because merchants are generally liable for all chargebacks in card-not-present transactions. For CNP fraud disputes, your defence must establish that the genuine cardholder initiated the transaction, not just that a card was used and authorised. An authorisation code alone, as the L case established, does not meet that standard.

For card-present fraud disputes, EMV chip compliance determines liability. If your terminal processed the transaction as a chip transaction, liability typically shifts to the issuer. If it didn’t, it shifts to you.

Authorisation Reason Codes

These arise when authorisation was not obtained, a declined authorisation was overridden, or a transaction was settled after the authorisation window expired (typically 7 to 30 days depending on merchant type). But that’s for legitimate cases, though. Most chargebacks nowadays are driven by friendly fraud.

Authorisation-related Barclays chargebacks are largely preventable with clean processing practices. They’re also among the more straightforward categories to defend, provided your authorisation logs are complete.

Processing Errors Reason Codes

This Barclays chargeback category covers merchant or system errors, such as duplicate charges, incorrect transaction amounts, wrong currency, incorrect transaction codes, and paid by other means. Most cases are defensible with clean transaction records.

Mastercard consolidates processing errors under code 4834, covering duplicate processing, incorrect transaction amounts, paid by other means, and late presentment. And as of April 2024, Visa retired code 12.1 for late presentment, merging it into authorisation code 11.3. Late presentment now sits under authorisation, and once the settlement window has passed, there is no defence.

Consumer Disputes Reason Codes

Cases like goods not received, services not as described, cancelled recurring transactions, and credit not processed all fall here. Defensibility varies by sub-code. Cancelled recurring payments appear to be the most consistently problematic. Once a cardholder cancels and you continue charging, this category offers limited recourse regardless of the evidence.

For a detailed examination of these reason codes, explore our database:

For UK merchants using Barclaycard as their acquirer, Barclaycard groups the same disputes into three categories rather than four: fraud, authorisation, and consumer disputes, including processing errors (combining Visa and Mastercard’s processing error category into the consumer disputes group). The underlying reason codes remain the same. Your chargeback letter will specify the applicable code.

How to Dispute a Barclays Chargeback: Step by Step

If you’ve read this far, it's either you’re where L once was, or you never want to be. Either way, the key takeaway from L's £10,550 loss is that having evidence isn't the same as having a case.

Winning disputes on Barclays-issued cards comes down to these disciplines: knowing which disputes are worth fighting, knowing what each reason code actually demands you prove, and submitting a package that an analyst (or their automated system) can follow in minutes. You do that inside a deadline that started before you opened the letter. Equally vital, you must treat every outcome, win or lose, as data that stops the next dispute before it's filed.

Let’s explore those disciplines step by step:

Step 1: Run The Math Before You Fight

Disputing a chargeback has a cost: your team's time, resources, and per-dispute fees. Hence, the question becomes "Is the expected recovery worth more than the cost of responding?"

The expected recovery is the transaction value multiplied by your realistic win rate for that dispute type. Win rates vary significantly by category. Transaction size matters too. Put all of these into consideration as you do your math.

For instance, a $200 friendly-fraud dispute at a 44% win rate carries an expected recovery of $88. If preparing the response costs you an hour of staff time and a $25 fee, you fight. You're up roughly $50 in expectation. Now run a $30 true-fraud CNP dispute at 9%: expected recovery of under $3. Fighting that one costs more than it returns every single time.

Three disputes a month, you can run this triage on the back of an envelope. Fifty a month, and the triage itself becomes a full-time job. That is the actual reason merchants at scale automate, and why platforms like Chargeflow operate on the fight-or-accept decision first, not just the paperwork.

Step 2: Prove What The Reason Code Claims Is False, Not What You Wish It Asked

This is where most Barclays disputes are lost, and the L case is the cleanest demonstration on record.

That merchant submitted authorisation codes for all 14 transactions and signed proof of delivery. The evidence looks compelling by any commonsense standard. They lost £10,550 ($14,127.45) anyway.

The reason code claimed the genuine cardholder never authorised the transactions. Authorisation codes prove that a card was valid. A delivery signature proves someone received goods. Neither proves the cardholder was involved in any of those activities. L needed to prove that the claim indicated by the reason code is untrue.

So translate your reason code into the single question it's asking:

A fraud code asks: “Can you tie this transaction to the genuine cardholder?” 3DS authentication records, AVS and CVV matches, device and IP data, and prior undisputed purchases from the same account help answer that question. Receipts and delivery confirmations may not.

A consumer dispute code asks: “Did the cardholder get what they paid for?” Delivery confirmation to the verified address, service access logs, and your communication trail support your answer.

A processing error code asks: “Is the transaction record itself correct?” Matched authorisation and settlement amounts, proof of single submission, and correct currency support your case.

Unfortunately, building your response to answer that one question, and nothing else, is easier said than done. Interpretation varies between banks. What one issuer finds persuasive, another may reject.

Furthermore, packaging and submitting your case early is a different challenge altogether. That’s why you need an automated chargeback management system tailored to answer these questions. No issuer, Barclays included, accepts evidence that doesn't address the claim. And evidence that proves the right thing, but was submitted after the time limit, is indistinguishable from no evidence at all.

Step 3: Treat The Outcome As Data

A pattern of "transaction not recognised" disputes on Barclays-issued cards is a billing descriptor problem. CNP fraud losses clustered on non-3DS transactions are an authentication gap with a known fix. Each dispute fought in isolation teaches you nothing. But tracked by issuer, reason code, and product line? Your Barclays dispute history becomes the cheapest fraud consultant you'll ever hire.

If you don’t use a platform that provides chargeback data analysis as part of the offering, you need to either buy or build one. Anything short exposes you to unnecessary losses.

How to Prevent Barclays Chargebacks

The hard truth in L’s case is that the money wasn't lost when Barclaycard debited the account. It was lost weeks earlier, at the point of sale and pre-fulfillment. From that moment, no authorisation code, no delivery signature, no evidence of any kind could have saved those transactions. The dispute was over before it began.

That's the lens for everything in this section. Some chargebacks are won or lost at the response stage. The most expensive ones are decided at checkout, at fulfilment, and in the billing descriptor your customer sees months later.

Here’s how:

Close The Undefendable Categories First

Think like Barclays. Every card-not-present transaction is high risk. And it's priced into the entire system, not just stated in policy. So, treat 3DS as what it actually is: a liability shift, not a fraud filter. When a 3DS-authenticated transaction is later disputed as fraud, liability generally sits with the issuer, not you. When 3DS fails, isn't attempted, or drops during an outage, that liability is yours. And as the L case showed, no volume of receipts changes that.

For subscriptions: honour cancellations when they're requested and send renewal reminders before each charge. Once a cardholder claims they cancelled and were charged anyway, you're in a category where your evidence barely matters.

Fix The Descriptor Problem That Barclays' Portfolio Makes Worse

Barclays' US portfolio is built almost entirely on co-branded cards, weighted heavily toward travel and hospitality (JetBlue, Carnival, Wyndham, and as of 2025, GM) alongside retail partners like Gap. That profile shapes the cardholder you're dealing with in two ways that matter for your billing descriptor.

Rewards chasers review statements closely, checking that points posted. And travel creates long gaps between charge and fulfilment. A cruise charged in January, sailed in June, under a descriptor the cardholder may not recognise, often comes back coded as fraud. That category has a historically weak merchant position, and it’s undefendable if the transaction was CNP without 3DS.

A billing descriptor that doesn't immediately match what the cardholder remembers buying is a "transaction not recognised" dispute waiting out the months. Your descriptor should carry your customer-facing brand name, not your legal entity, plus a reachable phone number or URL.

Intercept Disputes In The Window Before They Become Chargebacks

There's a stage many merchants often overlook. After the cardholder calls Barclays, there’s a time delay before the dispute formally posts as a chargeback. Visa and Mastercard operate alert systems (Verifi and Ethoca) in exactly this window. Chargeback alerts give merchants 24-72 hours to refund disputed transactions before they become real chargebacks. And for low-value disputes and the undefendable categories, a refund beats a guaranteed loss plus fees.

Screen The Order Before You Fulfil It

For travel, high-ticket, and general CNP transactions typical of Barclays cardholders, the most expensive time to discover fraud is after fulfilment. The cruise sailed, the goods shipped, the service rendered. The best way to intercept this is a checkpoint between payment and fulfilment.

Chargeflow Prevent operates in exactly that gap. It analyses transactions after payment but before fulfilment. It scores the dispute probability from 0 to 100 using cross-merchant network signals and triggers automated rules to proceed, hold, or cancel.

Because the network spans 20,000+ merchants, it flags repeat abusers who've already attacked other businesses. The serial disputer who is invisible in your own data is often well-documented in everyone else's.

Wrapping Up

L did everything a reasonable merchant would think to do, but still lost £10,550 because reasonable isn't the standard. The card network rules are. Those rules decide which Barclays disputes you can win, what evidence counts, and which transactions were lost the moment they were processed.

That's the real takeaway for any merchant taking Barclays-issued cards: the outcome of a Barclays chargeback is mostly determined before the dispute letter arrives. And it boils down to whether 3DS ran, what your descriptor says, and whether you fought the right disputes and refunded the wrong ones.

If you want to stop treating chargebacks as a fixed cost, the rubric is simple. Manage the whole dispute arc, from prevention to triage, evidence, and the data that each outcome leaves behind. The good news? You can automate that entire chargeback management arc, from pre-fulfilment screening to AI-built evidence, and only pay for recovered cases. The merchants winning against chargebacks aren't working harder than L did. They're working on the right end of the timeline.

Search intent here is consumer-heavy (cardholders asking "how do I..."), while the page targets merchants — adding a short signpost near the top for cardholder readers can reduce bounce and improve topical match for AI engines answering both audiences from one query. Chargeflow already holds a top-10 organic position, so incremental content depth is likely to move rank rather than establish it from scratch.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)

.avif)