%201.svg)

Chargeback Reason Codes: The Merchant List for 2026

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

Chargeback reason codes are standardized alphanumeric codes that categorize payment disputes into fraud, authorization, consumer disputes, or processing errors. They're not verdicts. They're diagnostic signals indicating what evidence you need to win. Each card network has distinct codes, rules, and liability frameworks. Friendly fraud abuses chargeback reason codes like "unauthorized transaction" or "item not received" despite legitimate purchases. Winning disputes requires matching your evidence to the network's specific liability test, not the cardholder's claim.

- Chargeback reason codes describe the cardholder’s claim to the bank, not a verified fact — treat them as a diagnostic starting point, not a verdict.

- Each network (Visa, Mastercard, American Express, Discover) uses its own code format and evidence rules, so the same dispute type requires different documentation depending on the card brand.

- Fraud codes hinge on authentication strength and transaction history; authorization codes hinge on approval validity; consumer-dispute and processing-error codes hinge on fulfillment and procedural proof.

- Certain codes (Visa 10.4/13.1, Mastercard 4837/4855, Amex C08, Discover NM) are disproportionately used in friendly fraud, so they warrant extra scrutiny before accepting the claim at face value.

- This page links out to a dedicated guide for all 80 individual Visa, Mastercard, Amex, and Discover reason codes, each with its own evidence checklist.

Chargeback reason codes are like movie ratings.

When you see a movie rated G, PG, or R, you already know what type of content to expect. Similarly, chargeback reason codes, like Visa’s 10.4 or Mastercard’s 4853, instantly identify the category of payment dispute you’re dealing with.

But there’s always a plot twist.

Just like a movie rating doesn’t tell you the full story, a reason code only tells you what the cardholder said to their bank. It tells you the theme for the dispute. It does not verify true intent nor merchant error. Reason codes do not decide liability, either.

Merchants who view chargeback reason codes as a verdict instead of a diagnostic signal lose winnable disputes.

But that shift in optics requires knowledge. Not just of what the codes are, but of why chargeback reason codes allocate liability the way they do, how card networks apply chargeback reason codes within their risk models, and which evidence changes the decision.

What Is a Chargeback Reason Code?

A merchant's Payment Service Provider typically assigns the reason code based on what the issuing bank reports, which is why the code alone does not always tell the full story.

A chargeback reason code is a standardized alphanumeric code assigned by an issuing bank to describe the cardholder’s claim.

Chargeback reason codes serve three primary purposes:

- Routes the dispute through the appropriate network rules

- Defines the burden of proof

- Signals the type of evidence required from merchants

They are not confirmations of wrongdoing. Rather, they translate cardholders’ claims into dispute categories the card networks recognize.

That distinction is vital. Because what merchants are truly facing is not a claim, but a liability test.

Why Chargeback Reason Codes Matter for Merchants

Some merchants treat chargeback reason codes like receipts for money already lost. They see “fraud” and write it off as the cost of doing business online.

That’s precisely what digital shoplifters are counting on.

Here’s what you gain when you treat reason codes as diagnostic signals instead of final judgements:

1) Stop Funding Your Own Losses

Every reason code signals the cardholder’s claim, not necessarily what happened.

Think of it like a broadcast transmission. The chargeback reason code is the signal. The underlying transaction data is the full recording.

For example:

- A “transaction unauthorized” code signals that the cardholder claims the transaction was fraudulent. It doesn’t confirm the purchase was truly fraudulent.

- A “product not received” code signals a nondelivery claim. It doesn’t verify that the item wasn’t delivered.

The key is filtering the noise from the signal. Reason codes are starting points. Paired with evidence and pattern analysis, they transform from mere labels into actionable intelligence that lets you contest false claims and prevent recurring losses.

2) See Patterns of Impending Crisis

Pattern recognition is how you become a true master in your craft. Decoding chargeback reason codes works the same way.

When you view reason codes in isolation, they may appear like random problems requiring separate fixes. But when you aggregate them, the story changes. Patterns emerge.

Case in point: Three “not as described” chargebacks on premium items in two weeks seems like bad luck. But that’s when you’re handling them one at a time. Analyze them together, and it points to a loophole.

eCommerce veterans have mastered this. They read the patterns in the data. They extract a bird’s-eye view of payments and chargebacks, and correct weaknesses before losses scale.

3) Fight Smarter, Not Harder

Not all chargebacks carry the same recovery probability. Fraud disputes on properly authenticated transactions may qualify for liability shift, depending on network rules, authentication result, and eligibility criteria.

Consumer disputes with weak delivery documentation may have a lower recovery likelihood regardless of your compelling evidence.

Treating all disputes equally is so 2016. Effective triage asks:

- Does this case meet formal liability shift conditions?

- Is historical continuity present?

- Is fulfillment documentation complete?

- Is the dispute operationally preventable?

Modern chargeback management is not about volume. It’s about rule alignment.

Chargeback Reason Codes by Card Network (Strategic Overview)

Every card network runs a distinct dispute framework. The reason codes may look similar. But the rules, evidence standards, and liability mechanics differ. Those differences determine outcomes.

Many merchants don’t lose disputes because their products are awful. They lose because their evidence doesn’t match the network’s rulebook. Recent updates across Visa, Mastercard, American Express, and Discover have quietly shifted the art of chargeback management.

Visa Chargeback Reason Codes

High volumes of Visa-coded disputes also feed into a merchant's standing under the Visa Acquirer Monitoring Program, independent of how any single case is resolved.

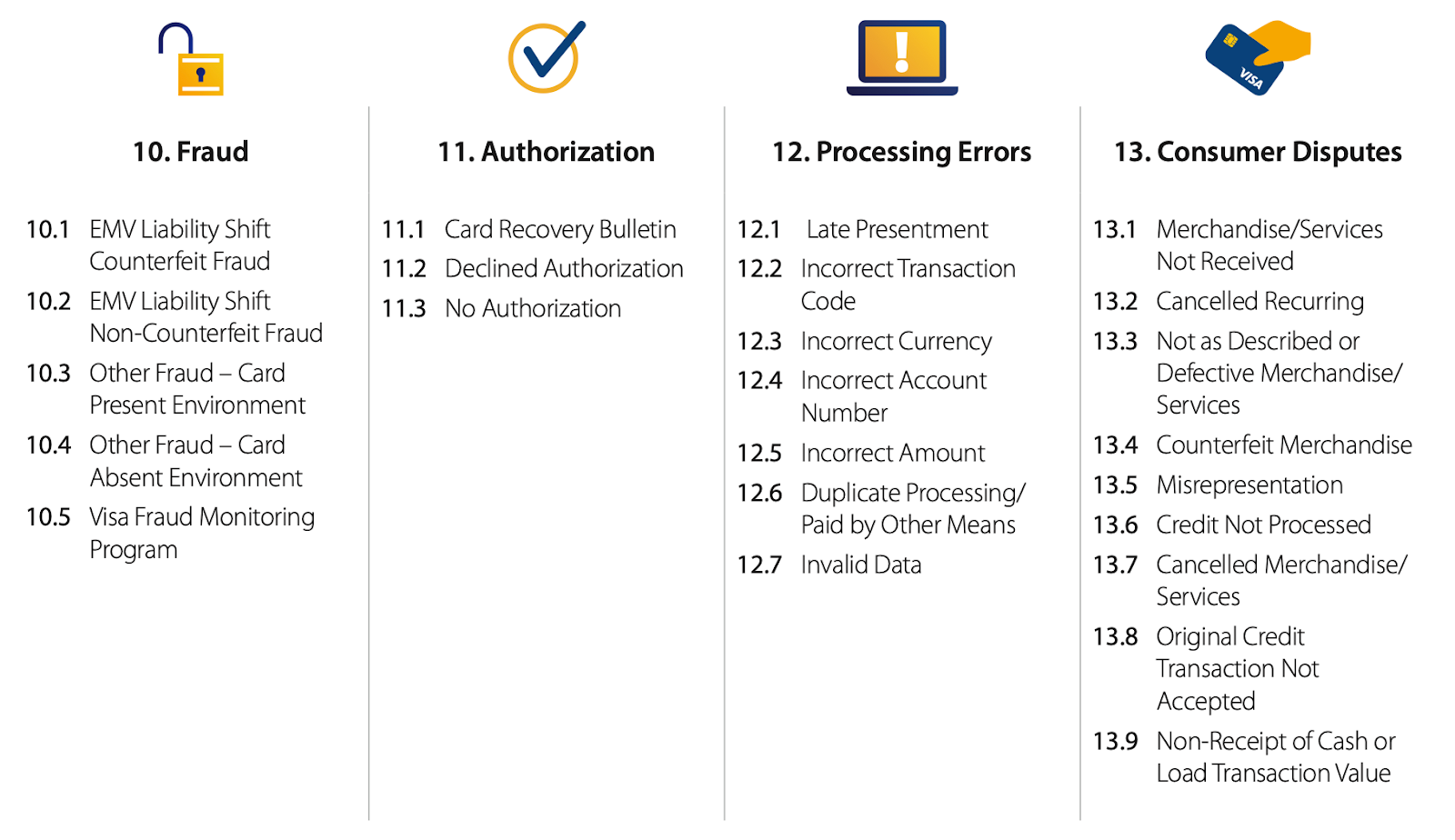

Format: Two-digit decimal codes (10.x = fraud; 11.x = Authorization; 12.x = Processing Errors; 13.x = Consumer Disputes).

Strategic Advantage, CE 3.0

Visa’s Compelling Evidence 3.0 framework allows fraud disputes (notably 10.4-Fraud, Card-Not-Present) to qualify for automatic liability shift when a merchant meets strict data conditions.

To qualify, merchants must show:

- At least two prior undisputed transactions

- Matching identifiers (e.g., IP address, device ID, shipping address, account credentials)

- Consistent usage patterns

According to Mastercard, enterprises win more chargebacks than mid-market businesses because they automate evidence capturing.

Review the full list of Visa chargeback reason codes and evidence requirements

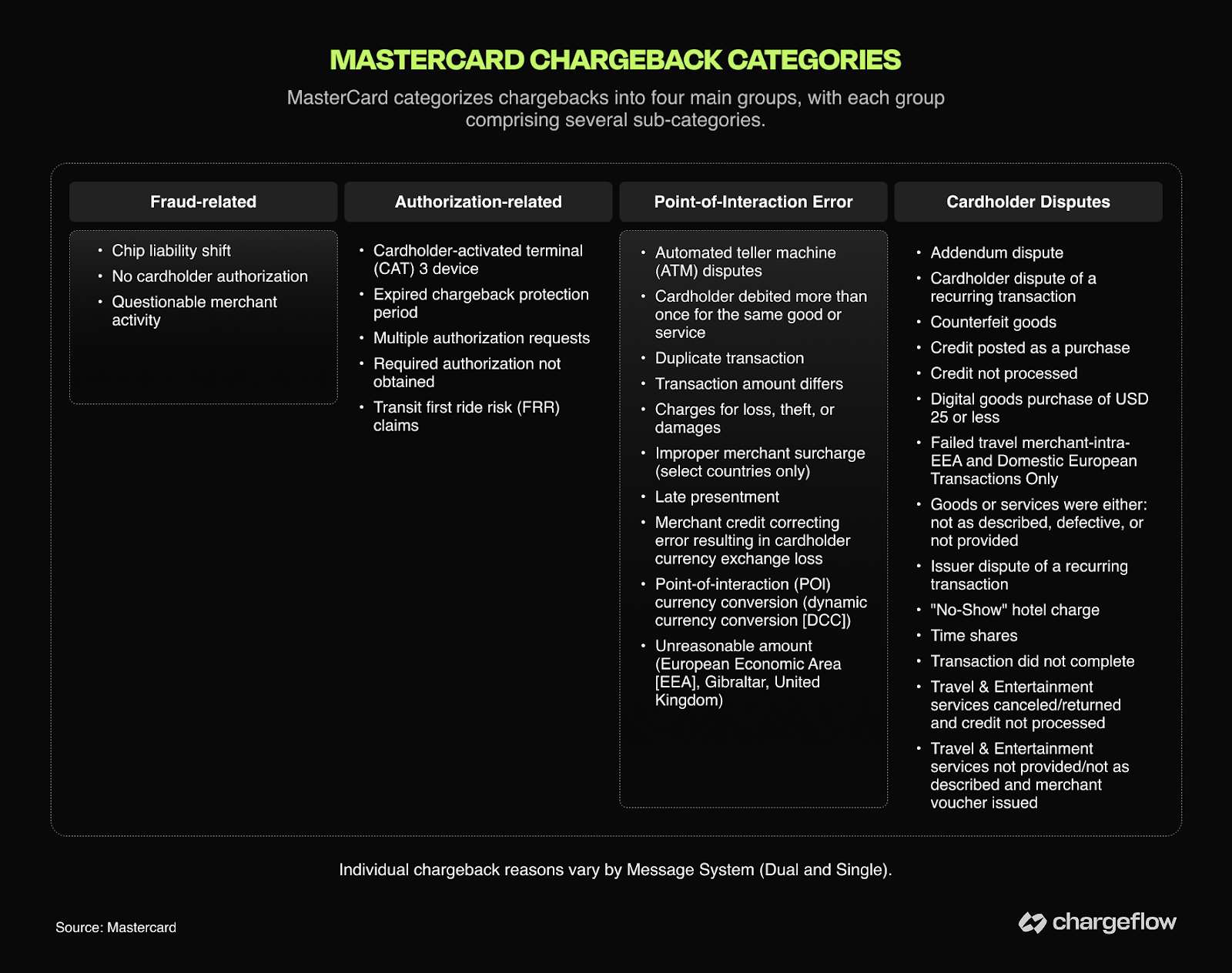

Mastercard Chargeback Reason Codes

Mastercard applies its own separate thresholds too, and merchants who cross them can be enrolled in the mastercard chargeback monitoring program regardless of individual case outcomes.

Format: Four-digit codes (e.g., 4837 = No Cardholder Authorization; 4853 = Goods/Services Not Received; 4870/4871 = Chip Liability Shift/Fraud variants).

Mastercard’s dispute framework differs significantly from Visa’s, particularly in how fraud liability and authentication interact.

Strategic Advantage - 3D Secure and Liability Reality

Mastercard’s 3DS liability shift hinges on successful authentication (Y/A), regional mandates like PSD3, and precise messaging compliance. Mastercard now mirrors Visa’s CE 3.0 through its First-Party Trust Program, providing automated liability shifts for fraud (4837) based on historical data, specifically two prior undisputed transactions within one year. Consequently, dispute outcomes depend on both real-time authentication strength and verified identity continuity for all returning customers.

Mastercard’s framework emphasizes consistency between prior legitimate behavior and the disputed transaction. Even small metadata gaps can materially weaken fraud defenses.

Review the full list of Mastercard chargeback reason codes and evidence requirements

American Express Chargeback Reason Codes

Format: Alphanumeric (e.g., F29 = Card-Not-Present Fraud; C08 = Goods/Services Not Received; R03 = No Reply).

American Express operates as both issuer and network. This structure allows Amex to review transactions, authorization, and cardmember data internally before and during the dispute process.

Strategic Advantage: The Inquiry Stage

In many cases, Amex initiates an inquiry before a formal chargeback. Merchants typically have about 20 days to respond. Failure to respond can result in an R03 (No Reply) chargeback.

Well-documented and timely responses at the inquiry stage can prevent escalation.

Programs such as Digital Receipts and enhanced transaction data sharing improve cardmember recognition and can reduce “unrecognized” fraud claims before they become chargebacks.

Review the full list of Amex chargeback reason codes and evidence requirements

Discover Chargeback Reason Codes

Format: Four-digit codes (e.g., 4553 = Not as Described; 4554 = Goods/Services Not Provided; 7030 = Fraud)

Discover’s chargeback code framework mirrors Mastercard’s structure but operates with a lower tolerance for Billing Descriptor errors.

Strategic Advantage

Discover prioritizes clarity. The network provides a streamlined path for merchants who maintain “clean” authorization records. More so, satisfying the card network’s Formal Information Request (inquiry) within 20 days prevents the request from escalating into a high-fee chargeback.

Discover equally rewards merchants who provide identity markers. Historical address continuity strengthens fraud rebuttals but does not guarantee a liability shift.

Review the full list of Discover chargeback reason codes and evidence requirements

Chargeback Reason Code Categories: Fraud, Authorization, Consumer Disputes, and Processing Errors

Card networks organize reason codes into four categories: Fraud, Authorization, Consumer Disputes, and Processing Errors. Rather than simple organizational labels, these categories correspond to burden-of-proof indicators that determine what you need to win false chargebacks.

The Decision Tree: Where Liability Rests

Fraud codes primarily evaluate authentication strength and historical identity continuity.

- If authentication is obtained, liability may shift to the card issuer.

- If no, you lose unless you prove relationship history or use chargeback deflection to stay ahead of the dispute.

Authorization codes ask for approval validity and timing compliance.

- If yes, you win.

- If no, you lose, regardless of fulfillment. Focus on chargeback alert or dispute deflection to avoid.

Consumer disputes evaluate fulfillment proof and policy clarity.

- There are automatic liability shifts.

- Evidence quality determines dispute outcome. Chargeback automation excels here for compiling and submitting documentation quickly.

Processing errors evaluate procedural compliance and remediation timing.

- These are merchant-preventable (duplicates, incorrect amounts, or late credit).

- Evidence like corrected refunds, timelines, or receipts can overturn the dispute if the issue is fixed promptly (timelines vary by network, often 20, 30 days response windows).

Understanding which test applies is more important than debating the claim itself.

Chargeback Reason Codes and Chargeback Fraud

Issuers assign reason codes based on the cardholders’ descriptions. Not necessarily an independent investigation. This is why reason codes don't match reality.

Industry research consistently shows that a majority of eCommerce chargebacks stem from customers disputing legitimate transactions. Even the card networks acknowledge this shift.

Mastercard says, “A fast-growing share of it is happening as consumers rely on the dispute and chargeback process as a way to get their money back.”

Because these claims are filed through official bank channels using legitimate reason codes, they are procedurally valid until proven otherwise. The codes become the disguise.

Friendly Fraud and Reason Code Abuse: The Most Commonly Abused Codes

Certain codes appear disproportionately in friendly fraud scenarios. Here are some examples:

Fraud (Visa 10.4/Mastercard 4837)

Catching these before they escalate to a formal dispute is exactly what a broader Ecommerce Fraud Prevention strategy is built for.

“I didn’t authorize it.”

A dispute coded as fraud may actually be:

- An authorization failure

- A subscription misunderstanding

- A product dissatisfaction issue

These claims often surface 30-60 days after purchase, especially for subscription renewals or delayed shipping items. Fraud codes carry moral weight. They receive rapid provisional credits.

Defense requires authentication strength, identity continuity, and historical transaction evidence.

Merchandise/Service Not Received (Visa 13.1/Mastercard 4855/Amex C08/Discover 4554)

“My package never arrived.”

In many cases, delivery occurred. The dispute hinges on the strength of your evidence.

Defense requires proof of delivery or fulfillment to the cardholder (or an authorized recipient) at the agreed-upon address, date, or method.

How to Use Chargeback Reason Codes to Win Disputes

You cannot change the assigned code. But you can align your rebuttal to the liability test triggered by the code.

As we established earlier:

- Fraud codes test authentication strength and proof of identity.

- Authorization codes test approval validity.

- Consumer disputes test fulfillment documentation.

- Processing errors test operational compliance.

Extracting these pieces of documentation manually can be a challenging task, which is why chargeback disputes are an uphill battle.

Fighting Fraudulent or Incorrect Chargeback Reason Codes

Fighting incorrect chargeback codes demands precision.

First, you need to confirm the assigned reason code aligns with the cardholder’s claim and your transaction facts. Reason codes often reflect the cardholder’s wording. Not the transaction reality.

If you defend the label instead of reconstructing the event, you let the issuer define the case and the outcome.

Next, scan for patterns. Is this a serial disputant? Look for repeated disputes from the same customer, clustered reason codes, or suspicious timing.

But you can't possibly do this manually and expect optimal outcome. Merchants with automated evidence pipelines consistently outperform manual processes.

Here’s why:

- Authentication logs are captured on autopilot.

- Delivery confirmations link seamlessly to order records.

- Customer communications stay timestamped and contextual.

- Transaction metadata remains preserved and queryable.

This turns chargeback disputes from frantic investigations into streamlined, procedural responses.

Respond to Chargebacks Based on Reason Code Strategy, Not Emotion

It is also worth watching how AI agent chargeback liability develops, since reason codes will need to adapt as more disputed purchases originate from automated agents rather than the cardholder.

If chargeback reason codes are movie ratings, metadata is the full film.

In today’s payment landscape, the “plot twist” is not a surprise. It’s a predictable outcome of data gaps. We’re in the age of algorithmic adjudication, where automated engines decide winners by instantly matching your transaction details against historical records.

Winning chargeback disputes is now a clinical exercise in data parity. Whether triggering Visa’s CE 3.0 or Mastercard’s First-Party Trust, success depends on satisfying a computer’s logic. Not a human’s sympathy.

Again, chargeback reason codes have morphed from being an instrument for standardizing disputes to becoming a weapon for fraud itself. Stop seeing codes as lost revenue receipts. Treat them as diagnostic signals.

The networks write the script. But you control the evidence. Architect your data today with Chargeflow: capture logs, link deliveries, and preserve continuity signals. With AI automation, friendly fraud becomes a formality you win without lifting a finger.

Complete Chargeback Reason Code Reference by Network

Use these tables to find the exact reason code on your chargeback notice. Each row links to a full guide covering evidence requirements and response strategy for that specific code.

Visa Chargeback Reason Codes (Full List)

| Code | Reason | Full Guide |

|---|---|---|

| 10.1 | EMV Liability Shift – Counterfeit Fraud Counterfeit fraud at a chip-enabled terminal that didn't support EMV. | View guide |

| 10.2 | EMV Liability Shift – Non-Counterfeit Fraud Non-counterfeit fraud where EMV liability shift applies. | View guide |

| 10.3 | Other Fraud – Card-Present Environment Fraudulent card-present transaction not covered by 10.1/10.2. | View guide |

| 10.4 | Other Fraud – Card-Absent Environment Fraudulent card-not-present transaction, e.g. online or phone. | View guide |

| 10.5 | Visa Fraud Monitoring Program Transaction flagged under Visa's fraud monitoring program. | View guide |

| 11.2 | Declined Authorization Transaction processed after authorization was declined. | View guide |

| 11.3 | No Authorization Transaction processed without obtaining authorization. | View guide |

| 12.1 | Late Presentment Transaction submitted for processing after the allowed time limit. | View guide |

| 12.2 | Incorrect Transaction Code Wrong transaction code applied, e.g. credit vs. purchase. | View guide |

| 12.3 | Incorrect Currency Transaction processed in the wrong currency. | View guide |

| 12.4 | Incorrect Account Number Charge posted to the wrong cardholder account number. | View guide |

| 12.5 | Incorrect Amount Transaction amount differs from what the cardholder authorized. | View guide |

| 12.6 | Duplicate Processing Same transaction submitted and charged more than once. | View guide |

| 12.7 | Invalid Data Transaction data is invalid or fails required processing rules. | View guide |

| 13.1 | Merchandise/Services Not Received Cardholder paid but never received the goods or service. | View guide |

| 13.2 | Cancelled Recurring Transaction Recurring charge continued after the cardholder cancelled it. | View guide |

| 13.3 | Not as Described or Defective Merchandise/Services Goods or services didn't match the description or were defective. | View guide |

| 13.4 | Counterfeit Merchandise Cardholder received counterfeit goods. | View guide |

| 13.5 | Misrepresentation Merchant misrepresented the goods, services, or terms of sale. | View guide |

| 13.6 | Credit Not Processed Merchant didn't issue a promised refund or credit. | View guide |

| 13.7 | Canceled Merchandise/Services Cardholder cancelled but was still charged. | View guide |

| 13.8 | Original Credit Transaction Not Accepted Cardholder disputes an unexpected credit transaction. | View guide |

| 14.1 | Fraudulent Multiple Transactions Cardholder charged multiple times for one purchase without authorization. | View guide |

Mastercard Chargeback Reason Codes (Full List)

| Code | Reason | Full Guide |

|---|---|---|

| 4801 | Requested Transaction Data Not Received Issuer's documentation request went unanswered. | View guide |

| 4802 | Requested/Required Information Illegible or Missing Submitted documentation was incomplete or unreadable. | View guide |

| 4808 | Authorization-Related Chargeback Transaction processed without valid or required authorization. | View guide |

| 4812 | Account Number Not on File Card number doesn't match any active cardholder account. | View guide |

| 4831 | Transaction Amount Differs Amount charged differs from the amount the cardholder agreed to. | View guide |

| 4834 | Point-of-Interaction Error Error at the terminal or POS resulted in an incorrect charge. | View guide |

| 4835 | Card Not Valid / Transaction Not Authorized Cardholder states the transaction wasn't authorized. | View guide |

| 4837 | No Cardholder Authorization Cardholder denies participating in or authorizing the transaction. | View guide |

| 4840 | Fraudulent Processing of Transactions Merchant fraudulently processed or reprocessed a transaction. | View guide |

| 4841 | Canceled Recurring or Digital Goods Transaction Recurring or digital-goods billing continued after cancellation. | View guide |

| 4842 | Late Presentment Transaction submitted for clearing outside the allowed window. | View guide |

| 4846 | Correct Transaction Currency Code Not Provided Currency code missing or incorrect on the transaction. | View guide |

| 4847 | Requested/Required Authorization Not Obtained Additional authorization requirement not met. | View guide |

| 4850 | Installment Billing Dispute Dispute over an installment payment plan's billing. | View guide |

| 4853 | Cardholder Dispute General dispute over goods, services, or transaction terms. | View guide |

| 4854 | Cardholder Dispute – Not Elsewhere Classified Dispute that doesn't fit a more specific reason code. | View guide |

| 4855 | Goods or Services Not Provided Cardholder paid but never received the goods or service. | View guide |

| 4857 | Card-Activated Telephone Transaction Dispute tied to a card-activated telephone transaction. | View guide |

| 4859 | Addendum, No-Show, or ATM Disputes Dispute over an addendum charge, no-show fee, or ATM transaction. | View guide |

| 4860 | Credit Not Processed Merchant didn't issue a promised refund or credit. | View guide |

| 4863 | Cardholder Does Not Recognize / Potential Fraud Cardholder doesn't recognize the charge; possible fraud. | View guide |

American Express Chargeback Reason Codes (Full List)

| Code | Reason | Full Guide |

|---|---|---|

| C02 | Credit Not Processed Merchant didn't issue a promised refund or credit. | View guide |

| C04 | Goods/Services Returned or Refused Cardholder returned or refused the goods or services. | View guide |

| C05 | Goods/Services Canceled Cardholder cancelled the goods or services. | View guide |

| C08 | Goods/Services Not Received Cardholder paid but never received the goods or service. | View guide |

| C18 | No-Show or Card Deposit Canceled Reservation no-show or deposit charge dispute. | View guide |

| C28 | Cancelled Recurring Billing Recurring charge continued after cancellation. | View guide |

| C31 | Goods/Services Not as Described Goods or services didn't match what was described. | View guide |

| C32 | Goods/Services Damaged or Defective Cardholder received damaged or defective goods or services. | View guide |

| FR6 | Partial/Immediate Chargeback Program Chargeback filed under Amex's partial/immediate program. | View guide |

| P07 | Late Submission Merchant submitted the transaction after the allowed deadline. | View guide |

| P08 | Duplicate Charge Same transaction charged more than once. | View guide |

| P23 | Currency Discrepancy Transaction processed in the wrong currency. | View guide |

| F29 | Card Not Present Fraudulent card-not-present transaction. | View guide |

| F30 | EMV Counterfeit Counterfeit-card fraud at a non-EMV-compliant terminal. | View guide |

| F31 | EMV Lost/Stolen/Non-Received Card Fraud involving a lost, stolen, or never-received card. | View guide |

| FR2 | Fraud Full Recourse Program Chargeback filed under Amex's fraud full-recourse program. | View guide |

| R03 | Insufficient Reply Merchant's response to the dispute was incomplete. | View guide |

| R13 | No Reply Merchant didn't respond to the dispute inquiry. | View guide |

Discover Chargeback Reason Codes (Full List)

| Code | Reason | Full Guide |

|---|---|---|

| AA | Does Not Recognize / Unauthorized Transaction Cardholder doesn't recognize or didn't authorize the charge. | View guide |

| AP | Cancelled Recurring Transaction Recurring charge continued after cancellation. | View guide |

| AW | Altered Amount Transaction amount was altered after the cardholder signed. | View guide |

| CD | Credit/Debit Posted Incorrectly Refund or credit posted incorrectly to the account. | View guide |

| CP | Not Classified Dispute that doesn't fit a more specific reason code. | View guide |

| DA | Declined Authorization Transaction processed after authorization was declined. | View guide |

| DP | Duplicate Processing Same transaction submitted and charged more than once. | View guide |

| EX | Expired Card Transaction processed on a card that had already expired. | View guide |

| IC | Illegible Sales Data Sales draft or transaction data was illegible. | View guide |

| IN | Invalid Card Number Charge processed against an invalid card number. | View guide |

| LP | Late Presentation Transaction submitted for processing after the allowed time limit. | View guide |

| NA | No Authorization Transaction processed without obtaining authorization. | View guide |

| NM | Non-Receipt of Merchandise Cardholder paid but never received the merchandise. | View guide |

| NR | Not as Described or Defective Merchandise Goods didn't match description or were defective. | View guide |

| RG | Non-Receipt of Recurring Goods or Services Recurring goods or services were never delivered. | View guide |

| RN | Non-Receipt of Cash/Load Transaction Receipt Cardholder didn't receive a cash or load transaction receipt. | View guide |

| SV | Services Not Rendered Cardholder paid for a service that was never performed. | View guide |

| UA02 | Fraud, Card-Not-Present Transaction Fraudulent transaction in a card-not-present environment. | View guide |

Win Disputes By Reason Code, Automatically

You can tailor your evidence to the exact reason code behind each chargeback instead of submitting generic responses. Chargeflow automates the process end to end, backed by a 4X ROI guarantee.

Start for FreeChargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)