%201.svg)

Mastercard Chargeback Survival Guide for Merchants (2026)

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

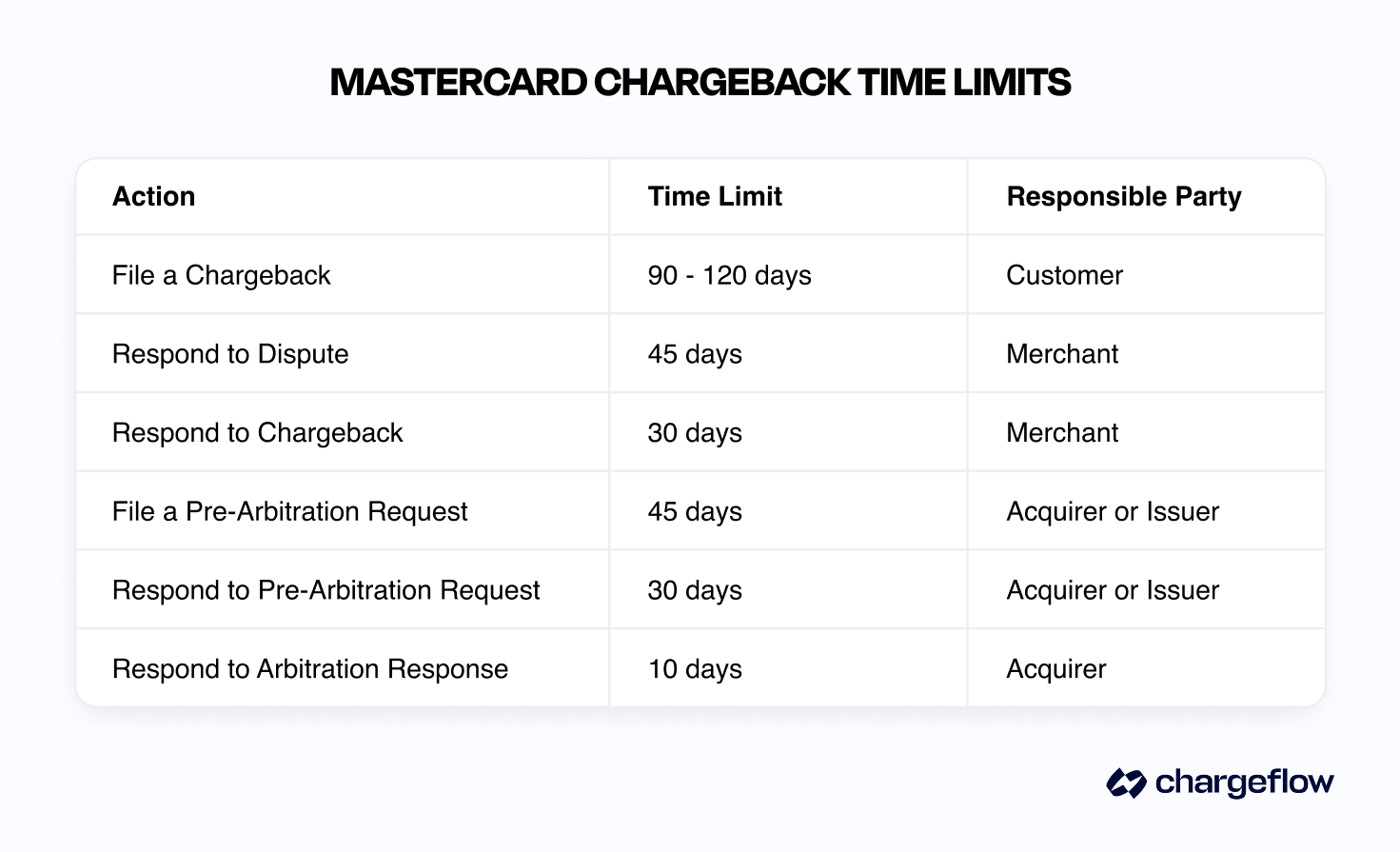

- Timelines: Cardholders get 120 days to dispute (90 for some categories); merchants get 45 days to respond to the first chargeback.

- Process: First Chargeback → Second Presentment → Pre-Arbitration (issuer files within 45 days; you have 30 to challenge) → Arbitration → Appeal.

- Compliance: Mastercard's ECM threshold is a 1.5% ratio or 100–299 chargebacks/month; HECM is 3% or 300+. Breaching triggers escalating fines.

- Win more: reason-code-specific evidence plus automated chargeback protection lifts win rates from ~8–20% (manual) toward ~80%.

Quick answer: To win a Mastercard chargeback, respond within the 45-day merchant window with reason-code-specific evidence. Mastercard's dispute lifecycle runs First Chargeback (cardholders have 120 days to file, 90 for some categories) → Second Presentment (your representment) → Pre-Arbitration (the issuer files within 45 days; you get 30 days to challenge or you lose automatically) → Arbitration → Appeal. Stay under Mastercard's Excessive Chargeback thresholds (1.5% ratio or 100+ monthly) to avoid fines, and automate evidence to push win rates from the ~8–20% manual average toward ~80%.

One click. That's all it takes for a customer to dispute a payment. And for your business to lose revenue, often more than the original transaction amount.

With global chargeback volume expected to reach 324 million by 2028, understanding Mastercard's dispute process is critical for business survival.

This playbook draws on lessons learned from assisting over 20,000 merchants in successfully disputing and winning chargebacks. It pierces the corporate veil of Mastercard's chargeback rules, reason codes, timelines, and recovery strategies. By the end, you will learn:

- Why chargebacks keep climbing

- Mastercard's four-step chargeback process in plain terms

- Industry-specific prevention strategies to cut disputes by 60-80%

- Evidence-based strategies to win Mastercard chargebacks

- Real-world implementation roadmaps for businesses of all sizes

Mastercard Chargeback Timeline at a Glance

PhaseIssuer / cardholder deadlineMerchant responseKey feeFirst ChargebackCardholder: 120 days (90 for some categories)45 days to representAcquirer $15–25Pre-Arbitration (2nd chargeback)Issuer: 45 days to file30 days to challenge$15 filingArbitrationIssuer escalates to Mastercard DRM15 days to respond$150 filing + $250 adminAppeal45 days from rulingWritten appeal with new evidence$500

Understanding the Mastercard Chargeback Landscape

Mastercard chargebacks occur when a customer disputes a completed transaction with their card issuer or bank, resulting in a reversal of funds. This process is similar across all card networks.

Mastercard promotes its chargeback system as a way to build trust and security for consumers. But that safety net often translates to a financial and operational strain for merchants like you.

Why Mastercard Chargebacks Are Rising: The Current Reality

The card network giant processes transactions for over 3.16 billion consumer and commercial cardholders. Within this ecosystem, Mastercard chargebacks represent a growing challenge driven by four key factors.

- Regulatory Environment: Mastercard's consumer-friendly dispute policies have lowered barriers to filing chargebacks. Mobile banking apps now allow disputes with just a few taps, contributing to friendly fraud, where cardholders dispute legitimate transactions.

- Surge in Card-Not-Present (CNP) Transactions: In 2024, 63% of global transactions occurred in CNP environments (37% online and 26% in mobile apps), according to Datos Insights. This shift has made CNP fraud the leading cause of chargebacks across all merchant categories.

- Evolving Fraud Tactics: Cybercriminals increasingly use AI-powered attacks, including account takeovers and synthetic identity fraud. Traditional rule-based fraud systems struggle to adapt, resulting in higher fraud rates and subsequent chargebacks.

- Management Gap: Many merchants, especially small and medium enterprises, still handle chargebacks reactively through manual processes or simply accept them as a cost of business.

Industry Impact by Sector

Our recent chargeback statistics find that different industries face distinct chargeback challenges:

- eCommerce & Retail: Primary challenges include friendly fraud (40-75% of chargebacks) and delivery disputes.

- Average chargeback rate: 0.65-1.2%

- Digital Services & SaaS: Subscription-related disputes dominate Mastercard chargebacks for SaaS verticals, often from forgotten recurring billing or unclear cancellation policies.

- Average chargeback rate: 0.3-1.8%

- Travel & Hospitality: Cancellation disputes and service quality issues drive most chargebacks for the travel and hospitality industry.

- Average chargeback rate: 0.8-1.5%

- Financial Services: Account takeover fraud and unauthorized transaction disputes are primary concerns for the financial industry.

- Average chargeback rate: 0.3–0.8%

With that context in mind, let's now explore Mastercard's chargeback process and learn how to respond effectively.

A Complete Breakdown of the Mastercard Chargeback Process

Mastercard chargebacks follow a multi-phase process with several structured steps. These cycles include First Chargeback (Issuer Initiated), Second Presentment (Merchant Response), Pre-Arbitration, Arbitration, and Ruling/Appeal stages. Each phase has specific timelines, requirements, and fee structures.

Phase 1: First Chargeback (Issuer Initiated)

Timelines:

- Cardholders: 120 days from the transaction date for most cases (90 days for certain authorization and point-of-interaction categories).

- Merchants: 45 days from dispute day one for representment.

Process:

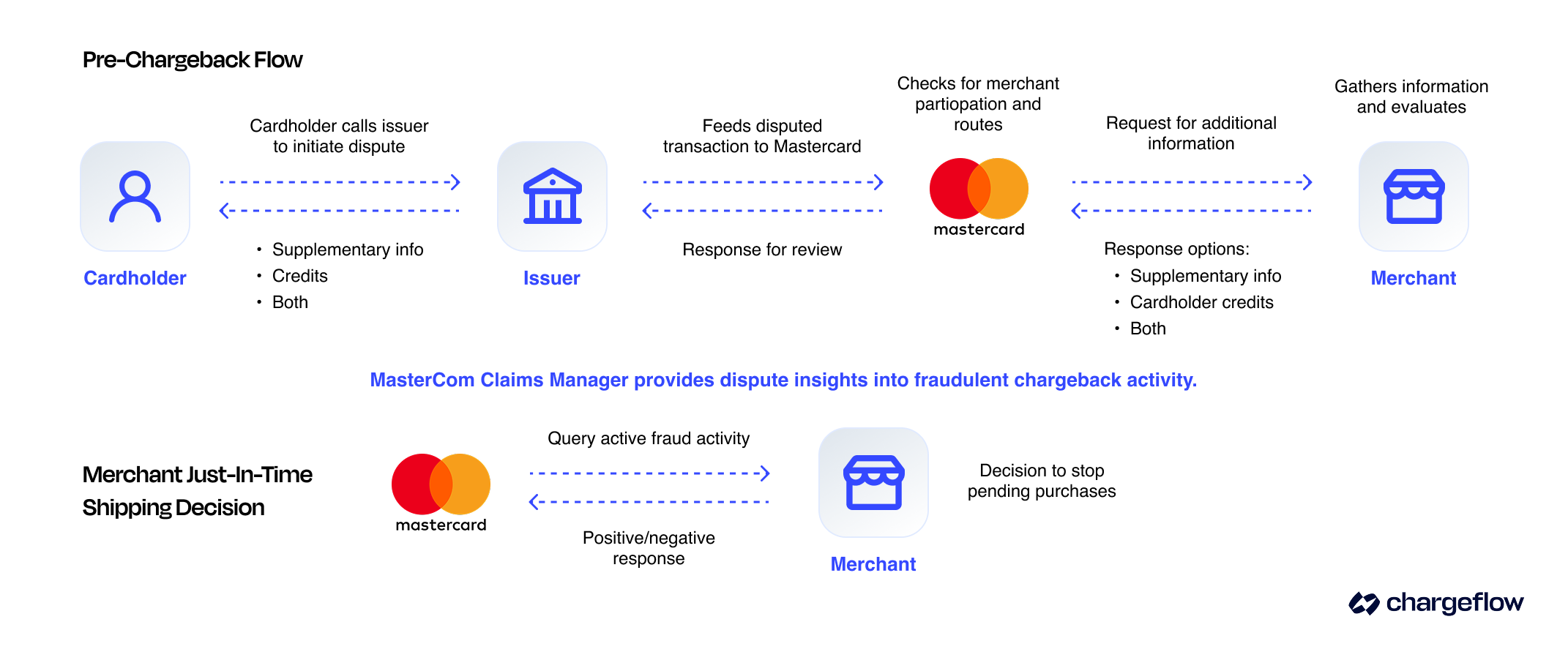

Step 1: First Chargeback: When a cardholder disputes a transaction, the card issuing bank (issuer) evaluates the claim against Mastercard’s Chargeback Guide (e.g., valid reason code). If valid, the issuer initiates a chargeback and debits the transaction amount from the acquirer, crediting it provisionally to the cardholder.

- The issuer provides the acquirer with the dispute reason code and any supporting documentation.

- The acquirer notifies the merchant, who must decide whether to accept the chargeback or contest it.

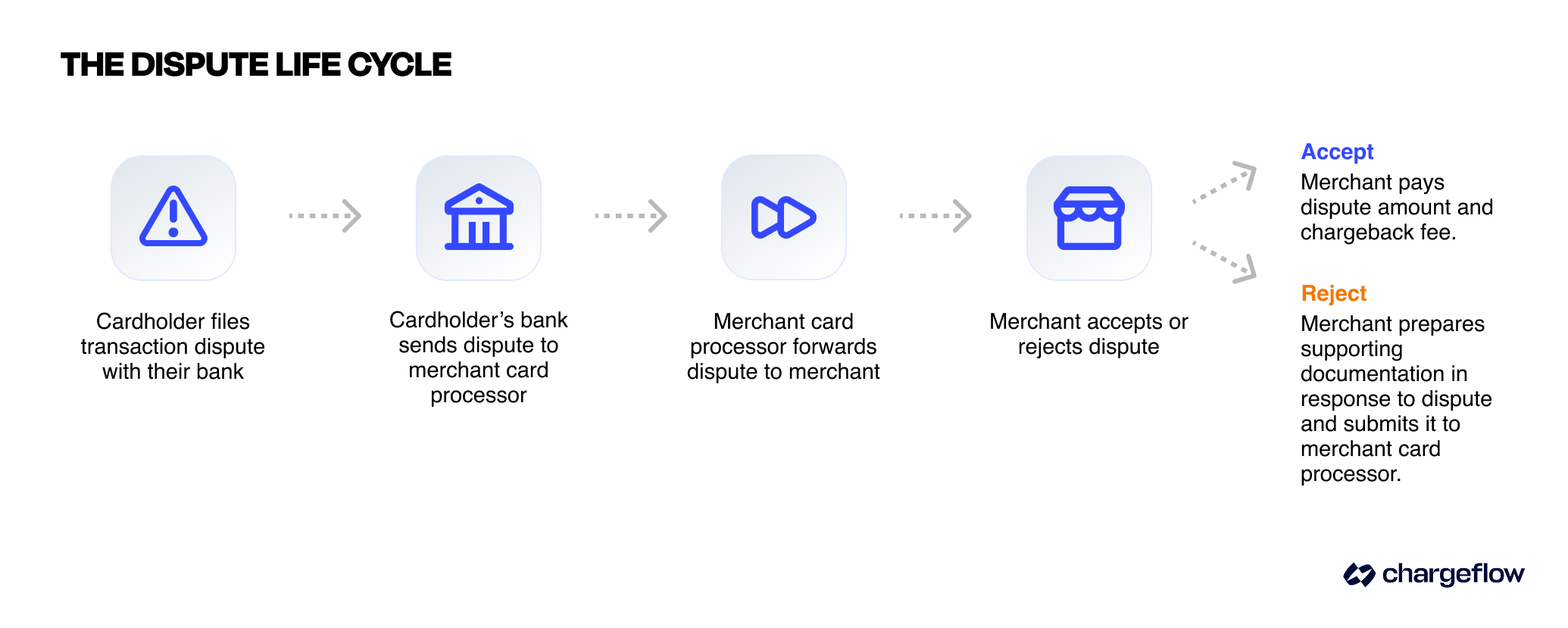

Step 2: Second Presentment (Merchant Rebuttal): If you, the merchant, choose to challenge the chargeback, you must submit a representment. The acquirer submits your evidence back to the issuer, who may:

- Accept the second presentment, taking financial responsibility; or

- Reject it, escalating the case to pre-arbitration if they believe the merchant's response is insufficient.

- Fee: No direct Mastercard fees, but acquirers typically charge $15-$25 per chargeback, sometimes more depending on your risk level or agreement.

Success Rates by Evidence Quality:

- High-quality, reason-code-specific evidence with manual approaches: 8.1-20% win rates.

- Automated evidence compilation (with platforms like Chargeflow): up to 80% win rate.

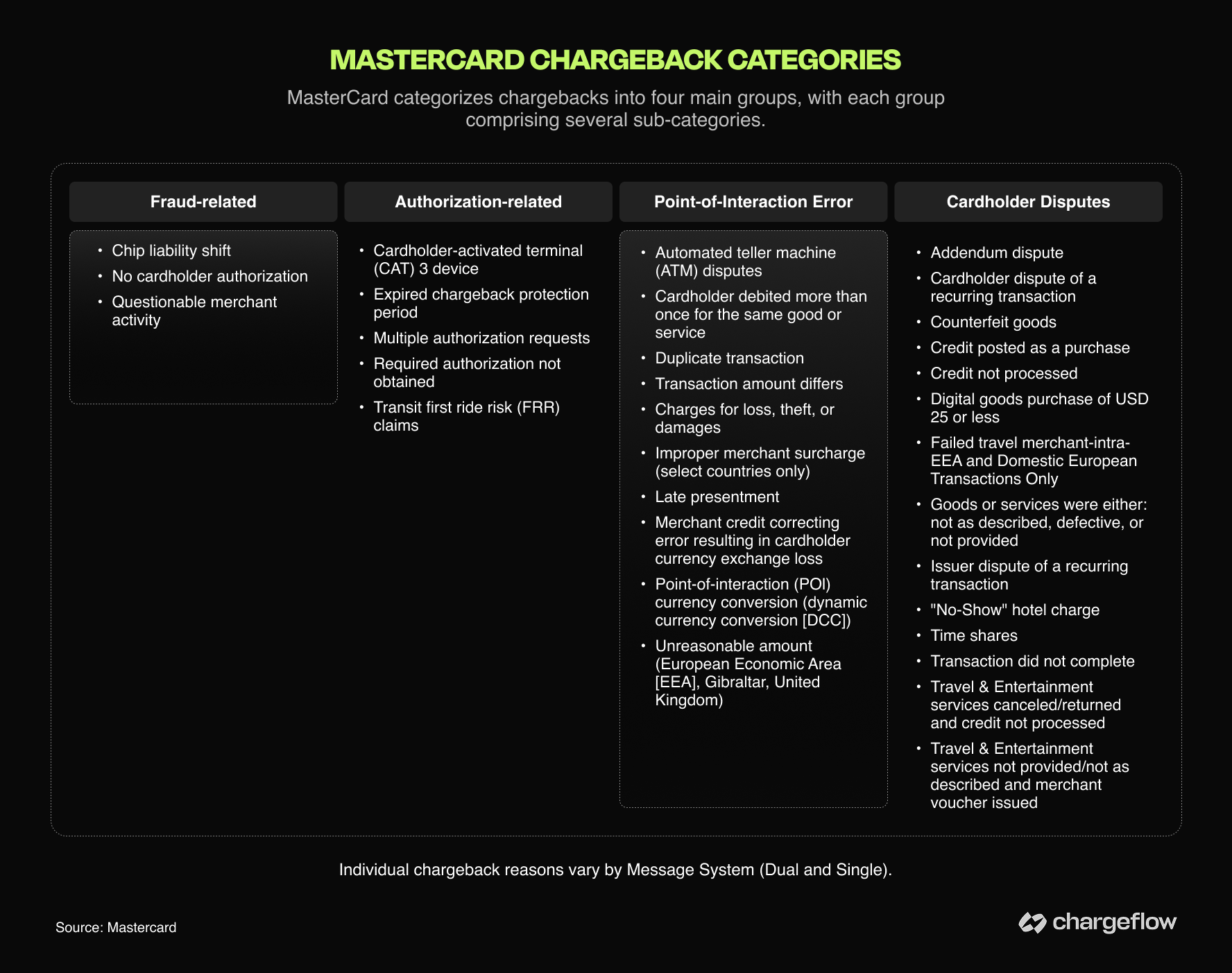

Common Mastercard Chargeback Evidence Requirements by Reason Code

Below are standard evidence requirements for winning chargeback representment on common Mastercard reason codes:

Reason codeDispute typeWinning evidence4837 – No Cardholder AuthorizationFraudAVS/CVV match, IP address, device fingerprint, delivery confirmation4863 – Cardholder Does Not RecognizeFraudClear billing descriptor, proof of customer interaction4855 – Goods/Services Not ProvidedItem not receivedSigned delivery receipt, tracking, proof of digital access/download4853 – Defective / Not as DescribedCardholder disputeProduct description, QC records, customer comms, refund offers4841 – Canceled Recurring BillingSubscriptionService terms, cancellation policy, proof customer did not cancel in time

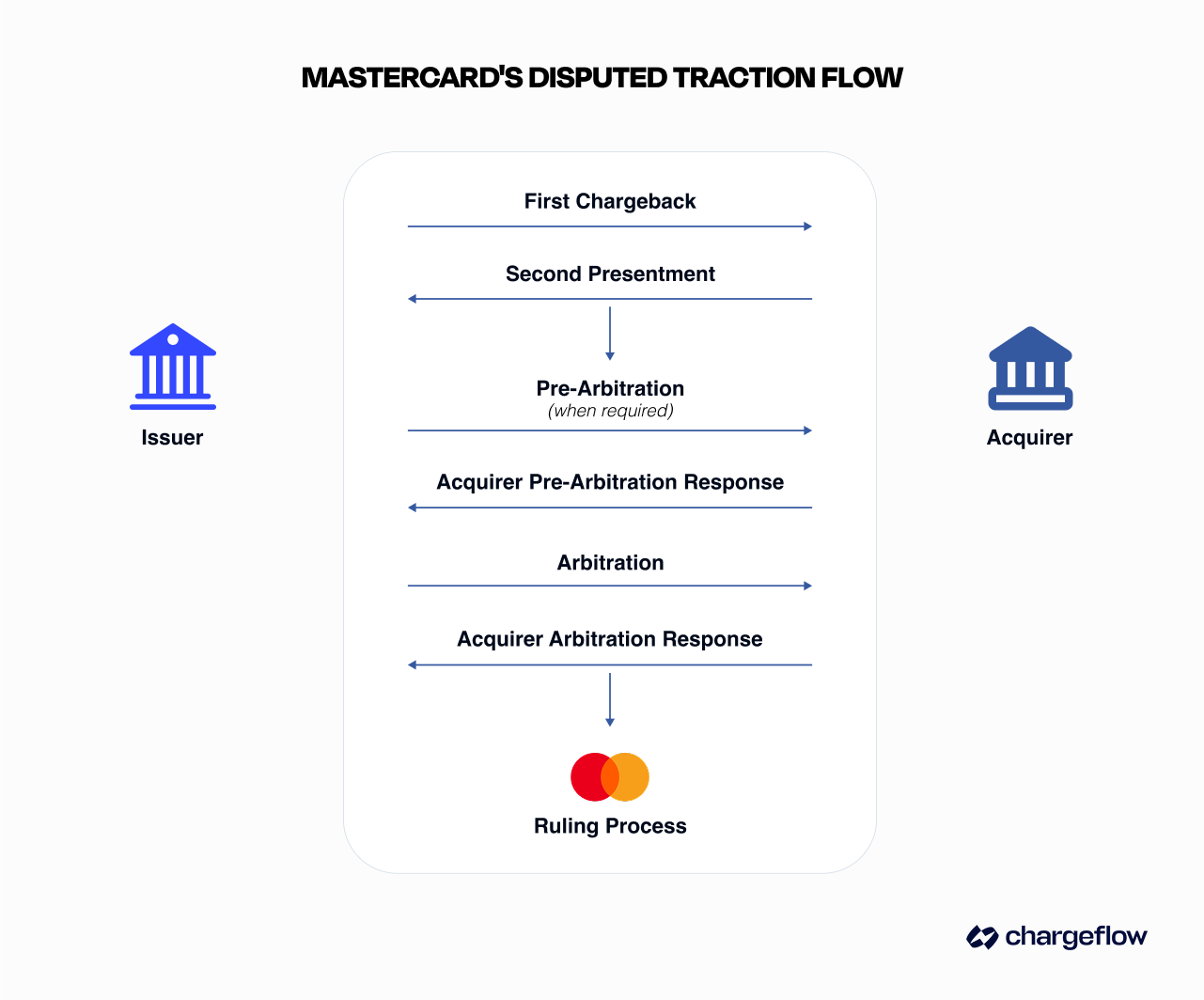

Phase 2: Pre-Arbitration (Second Chargeback)

Timeline: The issuer has 45 days to file pre-arbitration; the merchant then has 30 days to challenge it (and loses automatically if no response is filed).

Process:

- Step 1: Issuer Pre-Arbitration Filing: The issuer may initiate a pre-arbitration (second chargeback) case if it disagrees with the second presentment outcome. This step must be justified with new or additional information explaining why the prior response was invalid.

- Step 2: Acquirer Response to Pre-Arbitration: The acquirer can:

- Accept the case, assuming financial responsibility (Mastercard adjusts funds accordingly),

- Reject the case with a rebuttal and evidence,

- Or take no action, in which case Mastercard automatically assigns financial liability to the acquirer 30 calendar days after submission.

Either party may voluntarily accept financial liability before Mastercard's ruling.

- Fees:

- Filing fee: $15 (Same as the chargeback fee)

💡Pro Tip: Pre-arbitration cases have lower merchant win rates due to increased scrutiny. Cost-benefit analysis becomes critical at this stage.

Phase 3: Arbitration

Timeline: 15 days for acquirer response after issuer filing.

If the acquirer rejects pre-arbitration, the issuer may escalate the case to chargeback arbitration. Arbitration is rare due, in part, to high costs. Arbitration chargeback follows the process below:

- Step 1: Issuer Arbitration Filing: The issuer submits a case to Mastercard's Dispute Resolution Management (DRM) team, including all supporting evidence and an explanation for why the chargeback should be upheld.

- Step 2: Acquirer Arbitration Response: The acquirer may:

- Accept financial liability (at any time before ruling),

- Reject the arbitration case with a rebuttal (within 15 days),

- Or take no action – in which case, 10 calendar days after submission, Mastercard automatically proceeds to review it for ruling.

- Step 3: Mastercard Ruling: The Mastercard DRM team evaluates procedural compliance, evidence merit, and applicable rules. DRM team ruling:

- Determines financial liability,

- Issues adjustments through the Mastercard Consolidated Billing System (MCBS),

- Assesses applicable fees. This process is completed within 10 days from the arbitration case filing submission date.

- Fees:

- Filing fee: $150

- Administrative fee: $250

- Technical violation fee: $100 (losing party)

- Withdrawal fee: $150 (if withdrawn before DRM review)

💡Pro Tip: Arbitration strongly favors issuers due to cumulative evidence requirements and procedural complexity.

Phase 4: Appeal Process

Timeline: 45 days from ruling to file an appeal.

The party held financially liable may submit a written appeal to Mastercard. Appeals must include a valid reason for reconsideration and new or overlooked evidence. Mastercard's decision on the appeal is typically final.

Fee: $500

💡Pro Tip: Appeal ruling reversals have less than 10% success rates for merchants.

Evidence-Based Mastercard Chargeback Prevention Strategies

Winning against Mastercard chargebacks starts before a dispute ever occurs. By leveraging data instruments and applying proven fraud prevention tactics, you can stop avoidable losses and strengthen your defense when challenges arise.

Below are vital strategies worth implementing:

Tier 1: Fundamental Fraud Prevention

- 3D Secure 2.0 implementation

- Function: Adds an authentication layer for CNP transactions

- Impact: Reduces fraud-related Mastercard chargebacks by up to 60%.

- Liability Shift: Qualified transactions shift liability to the card issuer.

- Implementation Cost: Generally priced at $0.05-0.15 per transaction

- ROI Timeline: 3-6 months for most merchants

- AVS and CVV Verification

- Function: Validates billing address and card verification value

- Impact: An estimated 35-45% reduction in fraud-related reason codes when combined with tools like chargeback alerts

- Requirements: Essential for Visa Compelling Evidence 3.0 compliance

- Cost: Typically included in payment processing fees

- Address Verification Services (AVS) Response codes:

- Full match (Y): Process normally

- Partial match (A, Z, W): Enhanced review recommended

- No match (N): High-risk transaction, consider declining

Tier 2: Advanced Risk Management

- Machine Learning Fraud Detection: Modern fraud detection systems analyze hundreds of data points in real time to pinpoint anomalies through:

- Transaction velocity checks: Multiple transactions from the same source

- Device fingerprinting: Hardware and software characteristics

- Behavioral analysis: Deviation from normal purchasing patterns

- Geolocation verification: IP address vs. billing address analysis

- Tokenization for Stored Payment Data

- Function: Replaces sensitive card data with unique tokens

- Impact: Eliminates stored data breach risks

- Compliance: Required for PCI DSS Level 1 merchants

- Implementation: Work with your payment processor or third-party vendor.

Tier 3: Customer Experience Overhaul

If you're using tools like Insights, a free service from Chargeflow, you can easily get a bird's-eye view of chargeback sources. Frequent chargebacks could point to service issues, informing optimization procedures. Below are standard customer service optimization strategies:

- Clear Billing Descriptors: Confusing merchant names cause about 25% of "unrecognized transaction" chargebacks. Best practices include:

- Use a recognizable business name

- Include contact information

- Match marketing/website branding

- Avoid excessive abbreviations or codes

- Example Improvements:

- Poor: "SVC*MRK 4127749021"

- Better: "SKYE STORE 555-123-4567"

- Best: "SKYE OUTDOOR GEAR 555-123-4567"

- Proactive Customer Communication

- Order confirmations: Immediate email with transaction details

- Shipping notifications: Real-time tracking information to avoid uncertainties that cause "transaction not received" chargebacks

- Subscription reminders: Pre-billing notifications for recurring billing charges.

Industry-Specific Chargeback Prevention Implementation Framework

There are no one-size-fits-all chargeback prevention strategies. Merchants often make the mistake of deploying a blanket framework when seeking chargeback prevention. That's counter-productive because each business is unique.

Below are some sector-specific implementation recommendations to consider.

eCommerce and Retail

- Priority Chargeback Prevention Areas:

- Package delivery disputes

- Product not as described

- Friendly fraud

- Recommended Implementation Sequence:

- Month 1-2: Foundation

- Implement 3D Secure 2.0 for transactions >$50

- Update billing descriptors

- Establish delivery confirmation protocols

- Integrate a chargeback alert system

- Install Chargeflow Insights for customer-specific issues

- Month 3-4: Enrichment

- Deploy machine learning fraud detection

- Implement real-time order tracking

- Create customer service escalation procedures

- Month 1-2: Foundation

- Expected Results: 60-80% reduction in preventable Mastercard chargebacks within six months. You can pair this strategy with chargeback automation for complete coverage.

Subscription and SaaS Businesses

- Priority Chargeback Prevention Areas:

- Recurring billing disputes

- Service cancellation issues

- Free trial conversion disputes

- Critical Implementation Elements

- Subscription Management:

- Clear cancellation processes (maximum 3 clicks)

- Immediate cancellation confirmations

- Pause/downgrade options before cancellation

- Pre-billing email notification (7 days, 1 day before charge)

- Trial Period Best Practices:

- Explicit consent for trial-to-paid conversion

- Multiple conversion notifications

- Seamless trial extension options

- Clear and accessible trial terms at signup

- Subscription Management:

- Implementation Timeline: 2-3 months for full deployment

- Expected Impact: Up to 90% reduction in subscription-related Mastercard chargebacks, if complemented with a chargeback alert.

Travel and Hospitality

- Priority Chargeback Prevention Areas:

- Cancellation policy disputes

- Service quality complaints

- Booking modification issues

- Recommended Niche-Based Solutions:

- Dynamic pricing transparency

- Flexible rebooking policies

- Real-time availability updates

- Comprehensive booking confirmations

- Proactive service recovery protocols

- Expected Results: 50-60% reduction in service-related chargebacks, with an estimated 80% reduction if supported with chargeback alerts.

“Card-not-present fraud is driving sustained demand for chargeback and fraud prevention tools. Consumers increasingly prefer chargebacks over direct merchant refunds, with 84% finding chargebacks simpler to process.” – Ariel Chen, Chargeflow co-founder and CEO.

Advanced Compliance and Risk Management

One key compliance challenge for merchants is high chargeback ratios, which threaten their merchant accounts. Whether you operate a small or large enterprise, understanding this challenge and implementing the recommended solutions can save you so much trouble.

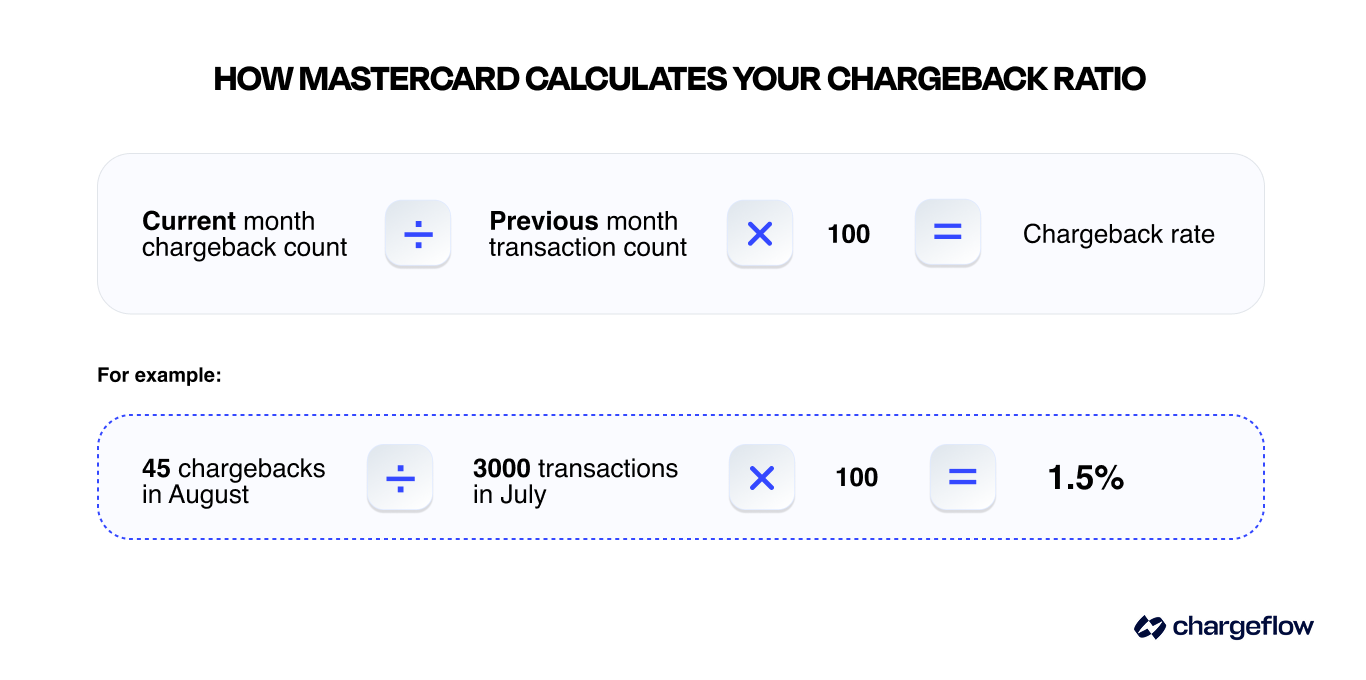

Mastercard monitors merchants' chargeback-to-transaction ratios under its Excessive Chargeback Merchant (ECM) program. Exceeding thresholds can trigger fines or even account termination. Many processors enforce stricter internal limits to reduce risk exposure and maintain network compliance.

Mastercard Monitoring Program Thresholds

Mastercard has divided its Excessive Chargeback Program (ECP) into three categories:

- Standard threshold: 1% chargeback ratio OR 100+ chargebacks per month.

- Excessive chargeback merchant (ECM) threshold: 1.5% chargeback ratio OR 100 to 299 chargebacks per month.

- High excessive chargeback merchant (HECM) threshold: 3% chargeback ratio OR 300+ chargebacks per month.

ECP Program Consequences for Merchants

Breaching any of the stated thresholds has specific consequences for merchants, such as the following:

- Tier 1: Monthly Monitoring and Reporting Burden

- Mastercard enrolls merchants exceeding ECM or HECM thresholds in the ECP program.

- Merchants in Tier 1 ECP must submit a remediation plan to reduce chargebacks and provide monthly progress reports.

- Tier 2: Monthly Fines

- After two months in the ECP, fines apply and escalate as follows:

- Months 2-3: $1,000 (ECM) or $1,000-$2,000 (HECM)

- Months 4-6: $5,000 (ECM) or $10,000 (HECM)

- Months 7-11: $25,000 (ECM) or $50,000 (HECM)

- Months 12+: $50,000-$100,000 (ECM) or $100,000-$200,000 (HECM)

- Additional chargeback fees may apply.

- After two months in the ECP, fines apply and escalate as follows:

- Tier 3: Account Termination

- After 12+ months without reducing Mastercard chargebacks below 100 or a 1.5% chargeback rate, the acquirer may terminate your merchant account.

- Your business may equally be added to a MATCH list, blocking a new Merchant ID.

How to Exit the Mastercard Excessive Chargeback Program

Merchants can only exit the ECP by maintaining chargeback levels below the ECM threshold (100 chargebacks) for three consecutive months. Below are some recommended best practices for achieving that objective.

- Track incoming chargebacks

- Use real-time analytics to monitor chargeback ratios.

- Address root causes such as product quality issues, shipping delays, or confusing billing descriptors.

- Refund and cancel problematic transactions

- A chargeback alert notifies you of impending disputes and allows proactive refunds when necessary to prevent escalation.

- You can also block and blacklist problematic customers when necessary.

💡Pro Tip: Merchants leveraging real-time analytics and alerts see a significant reduction in chargeback rates. This Stripe Case Study showcases how Wordtune, an AI writing assistant service, achieved a 33.5% reduction in fraudulent disputes and a 29.7% reduction in dispute rate within five months.

Chargeback Fraud Management Vendor Evaluation Framework

Shopping occurs across multiple channels, including QR codes, mobile apps, Social Media live streams, online, and in person. Many transactions involve third-party intermediaries, like travel booking apps, rather than directly with the service provider.

This omni-channel environment complicates chargeback management evidence collection due to fragmented data and delayed access to critical transaction records.

Hence, selecting a chargeback fraud prevention vendor is a weighted decision. Choosing the wrong solution may result in submitting incorrect evidence or experiencing high false positives, which can cause legitimate customers to be treated as fraudsters. If you're weighing dedicated dispute platforms, it helps to compare options directly—for example, Chargeflow vs Disputifier and Chargeflow vs Chargeblast.

Here are some vendor selection metrics to consider:

Core Functionality Assessment:

- Dispute prevention capabilities: Fraud detection, alert system, customer tools

- Chargeback recovery services: Automated representment, evidence compilation

- Analytics and reporting: Real-time dashboards, trend analysis

- Integration ease: API quality, setup time, ongoing maintenance

Vendor Comparison Matrix:

- Fraud Detection and Prevention Specialists:

- Recommended: Sift, Kount, Riskified

- Strengths: Advanced Machine Learning, real-time fraud scoring

- Weaknesses: Limited chargeback recovery services, especially in cases involving friendly fraud

- Payment Processor Solutions:

- Recommended: Stripe Radar, PayPal Fraud Protection

- Strengths: Seamless integration, competitive pricing

- Weaknesses: Platform-specific fraud coverage, limited customization, and compelling evidence collection and submission.

- Full-Service Platforms:

- Recommended: Chargeflow, Mitigator, Chargeback Gurus

- Strengths: End-to-end coverage, specialized expertise, set it and forget it

- Weaknesses: Higher cost, false negatives, partial tools, and integration complexity depending on the platform you choose.

- Platform Selection Criteria Weighting:

- Effectiveness: 35% (win rates, prevention success)

- Cost-effectiveness: 25% (ROI, total cost of ownership)

- Integration ease: 20% (setup time, maintenance requirements)

- Support quality: 15% (expertise, responsiveness)

- Scalability: 5% (growth accommodation for various models, feature expansion)

Cost/Benefit Analysis: Manual/Outsourced vs. Automated Chargeback Management

According to Mastercard, merchants and issuers are progressively embracing automated chargeback management (Mastercard 2025 State of Chargebacks Report, p. 5 & 20). This cost/benefit analysis throws more light on the reason for that development.

Manual Process Characteristics:

- Average time investment: 2-4 hours per case

- Typical dispute win rate: 8-20%

- Cost per case: $50-100 (including staff time)

- Scalability: Maximally limited to 10-20 cases per week per person.

Automated Process Characteristics:

- Average processing time: ~20 minutes per case

- Typical win rate: 45-80%

- Cost per case: 25% per recovered chargeback (Chargeflow pricing)

- Scalability: Unlimited (with Chargeflow)

ROI Calculation Example:

For a merchant with 100 chargebacks per month, here’s how their ROI stacks up between manual and automated chargeback management:

- Manual processing cost: $8,000/month + $60,000 in lost revenue

- Automated processing cost: $2,500/month + $25,000 in lost revenue (depending on the platform chosen)

- Net monthly savings: $40,500

- Annual savings: $486,000

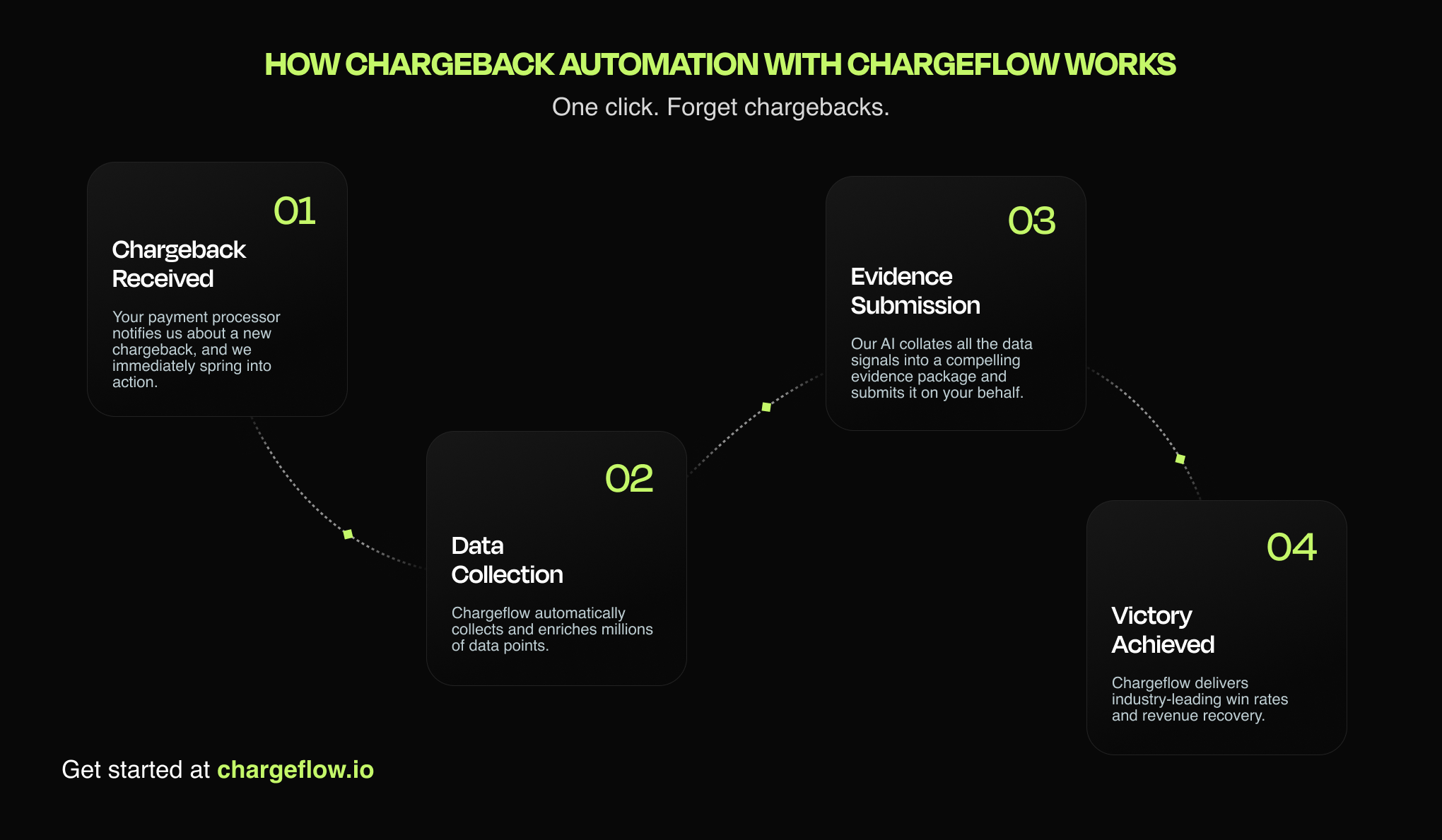

💡Pro Tip: Many chargeback solutions offer partial tools, such as alerts or manual recovery, leaving merchants to piece together evidence across platforms. Choosing the right solution, especially one like Chargeflow that offers complete coverage with a 4X ROI guarantee, makes all the difference.

Key Performance Indicators (KPIs)

If you’re seeking to exit the Mastercard ECP program, you must target essential KPIs that fast-track your objectives. Below are some examples to consider.

Primary Metrics:

- Chargeback Ratio: Target <0.5 for most industries

- Dispute Win rate: Target 45-65% for representments

- Cost Per Chargeback: Target reduction of at least 50%

- Prevention Rate: Target at least 60% of preventable chargebacks

Secondary Metrics:

- Customer Satisfaction: Track the impact of chargeback fraud prevention on legitimate customers and ensure positive outcomes.

- Payment Authorization Rates: Ensure fraud prevention does not reduce legitimate approvals.

- Payment Processing Speed: Maintain <2-second transaction processing times.

- False Positive Rate: Target <5% for fraud prevention systems.

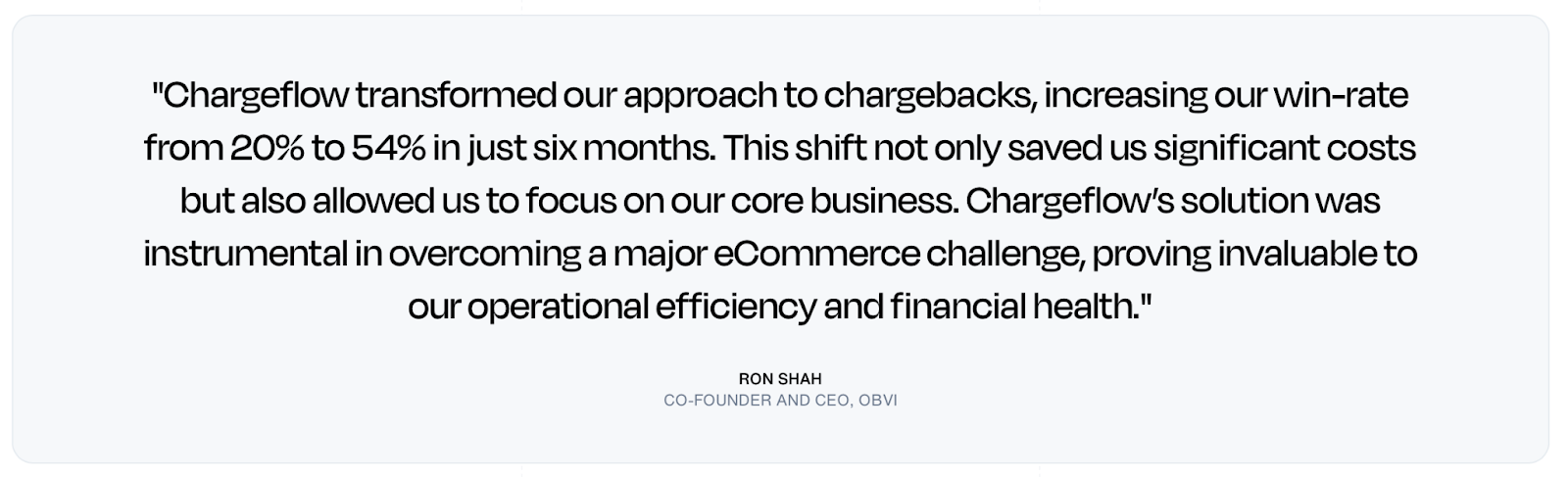

Case Study: Obvi’s 170% Win-Rate Boost with Automation

Obvi is a fast-growing eCommerce company in the competitive health and wellness supplement industry. The omnichannel vendor has achieved $40 million in revenue as of 2023, serving 200,000+ customers across over 75 countries. Despite its success, Obvi faced growing chargeback rates due to friendly fraud.

The manual process of handling chargebacks (via a freelancer or customer support) was time-intensive, costly ($40 per case), and yielded a low 20% win rate. This resulted in significant revenue losses.

Solution:

Obvi automated chargeback management with Chargeflow, a platform known for handling chargebacks from start to finish. This shift yielded immediate results.

Results:

- 54% Win Rate

- $10,427 Recovered In Lost Revenue

- 170% Increased Win Rate

- Increased Customer Satisfaction

Products Used:

- Chargeback automation

- Alerts

- Insights

Mastercard Chargeback FAQs

How long does a merchant have to respond to a Mastercard chargeback?

Merchants generally have 45 days from dispute day one to submit a representment (second presentment). If the case escalates to pre-arbitration, you have 30 days to challenge it or you lose automatically.

How long do cardholders have to file a Mastercard chargeback?

Cardholders typically have 120 days from the transaction date, though some authorization and point-of-interaction categories carry a shorter 90-day window.

What are Mastercard's ECM and HECM thresholds?

The Excessive Chargeback Merchant (ECM) threshold is a 1.5% chargeback ratio or 100–299 chargebacks per month; the High Excessive (HECM) threshold is a 3% ratio or 300+ chargebacks per month. Breaching either triggers escalating fines.

What evidence wins a Mastercard fraud chargeback?

For reason code 4837 (no cardholder authorization), submit AVS/CVV match results, IP address, device fingerprinting, and delivery confirmation. For 4863 (does not recognize), a clear billing descriptor and proof of customer interaction usually win.

Final Thoughts on Mastercard Chargebacks and Next Steps

Effective Mastercard chargeback management requires a systemic approach that combines prevention, early detection, and strategic recovery efforts. Industry records and our internal data clearly show that merchants implementing comprehensive chargeback management programs see:

- 60-85% reduction in preventable chargebacks;

- 45-65% win rates on disputed cases (vs. 8-15% for manual processes);

- 70-80% reduction in total chargeback costs;

- Improved customer satisfaction and retention rates;

- 4x return on investment guarantee.

With that in mind, here are immediate action items to consider:

Immediate Action Items

For All Merchants:

- Conduct a comprehensive chargeback audit and baseline establishment

- Update billing descriptors and customer communication protocols

- Implement basic fraud prevention measures (3D Secure, AVS/CVV)

- Establish chargeback monitoring and response procedures with automated chargeback protection

For High-Volume Merchants:

- Deploy advanced fraud detection and machine learning systems

- Implement automated chargeback representment processes

- Integrate comprehensive analytics and reporting platforms

- Work with your service provider to track key metrics for long-term success

Chargeflow provides these essential services on a pay-per-success basis. Contact our specialists if you require additional information. As Mastercard said, "merchants that re-examine their approach and implement advanced automated technologies will reap the rewards of reducing chargebacks while improving customer satisfaction and loyalty." – (Mastercard 2025 State of Chargebacks Report, p. 4)

This guide represents current industry best practices and Mastercard requirements based on publicly available information as of the time of writing.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)

.avif)