%201.svg)

Visa Chargeback Dispute Rules, Fees & Time Limits (2026 Playbook)

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

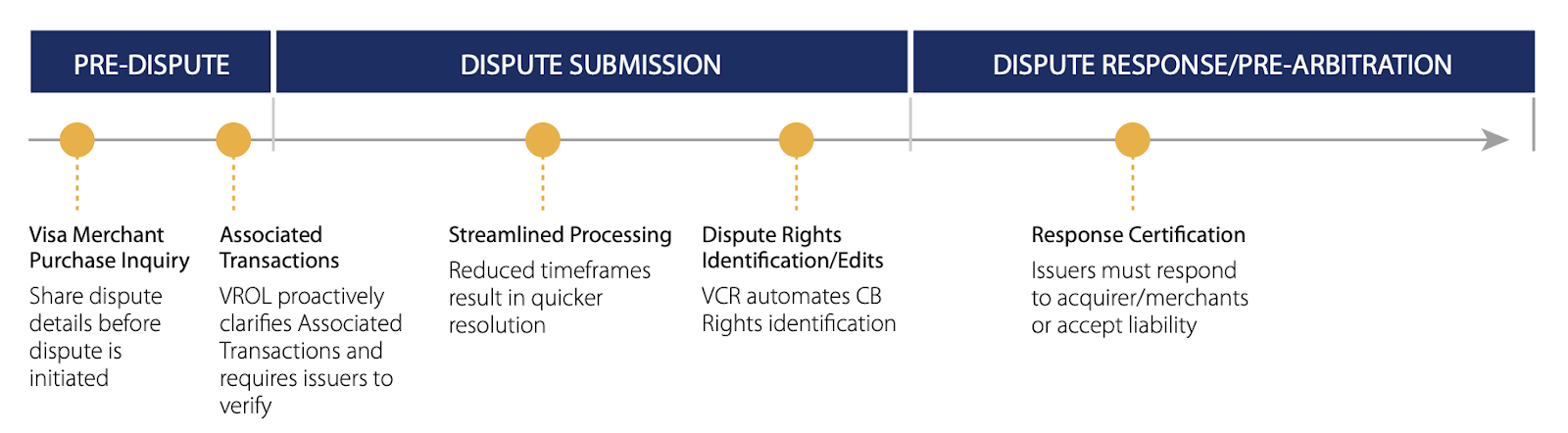

- Visa chargebacks move through five phases — inquiry, first chargeback, pre-arbitration, arbitration, and appeal — each with its own deadline and fees.

- Time limits are tight: cardholders generally have 120 days to dispute, while many processors now give merchants as few as 9–18 days to respond.

- VAMP tightened on April 1, 2026: the merchant "excessive" ratio dropped from 2.2% to 1.5% (150 bps), with an $8-per-dispute fee in the excessive tier.

- VAMP combines fraud (TC40) and non-fraud disputes (TC15) into one ratio against settled CNP transactions — low fraud no longer offsets high chargebacks.

- Prevention plus automated representment wins: manual responses win roughly 8–20% of cases, while automated evidence platforms reach up to 80%.

A Visa chargeback dispute is the process of contesting a payment reversal that a cardholder's issuing bank initiates against a merchant. Merchants fight back through "representment," submitting evidence to prove the transaction was valid. Visa chargebacks move through five phases with strict time limits, and as of April 1, 2026, merchants face a tightened 1.5% VAMP ratio threshold and an $8-per-dispute fee once classified as excessive.

Are you losing revenue to Visa chargebacks? You're not alone. Visa itself calls payment disputes a growing concern, draining billions from merchants each year.

Visa chargebacks occur when customers dispute completed transactions, prompting their card-issuing bank to reverse payments and withdraw funds from your merchant account.

This sudden reversal can disrupt cash flow, especially for small business owners. It also strains processor relationships and can even lead to costly penalties if not managed.

Visa has introduced policy changes to help merchants fight back. But these policies only address a fraction of the problem. Friendly fraud, repeat disputes, and complex evidence requirements still leave revenue at risk.

That's why a structured, proactive chargeback management strategy, grounded in clear chargeback rules, is essential for Visa merchants.

This playbook equips you with battle-tested tactics to minimize disputes, win more Visa chargebacks, and protect your merchant account. You'll learn how to transform Visa's chargeback system from a revenue threat into a manageable process.

Visa Chargeback Fees and Time Limits at a Glance

Before diving into the full process, here's a quick-reference table of the key Visa dispute stages, the deadlines that apply, and the fees involved.

| Stage | Merchant Time Limit | Typical Fees |

|---|---|---|

| Inquiry (VMPI / Order Insight) | 24–72 hours to respond | No direct Visa fee (acquirer refund fees may apply) |

| First chargeback (representment) | ~9 days (US/Canada) to 18 days (other regions); historically 20–30 days | Acquirer $15–$25 per chargeback |

| Pre-arbitration (second chargeback) | 30 days (Allocation) | Filing $25–$50; dispute-expired fee $15 |

| Arbitration | Up to 70 days (Allocation) / 100 days (Collaboration) | Filing $500; case ruling $600; non-compliance $250 |

| Appeal | 60 days (disputes ≥ $5,000 only) | $1,000 |

Cardholder time limit: generally 120 days from the transaction date to file a dispute (up to 540 days for certain fraud cases).

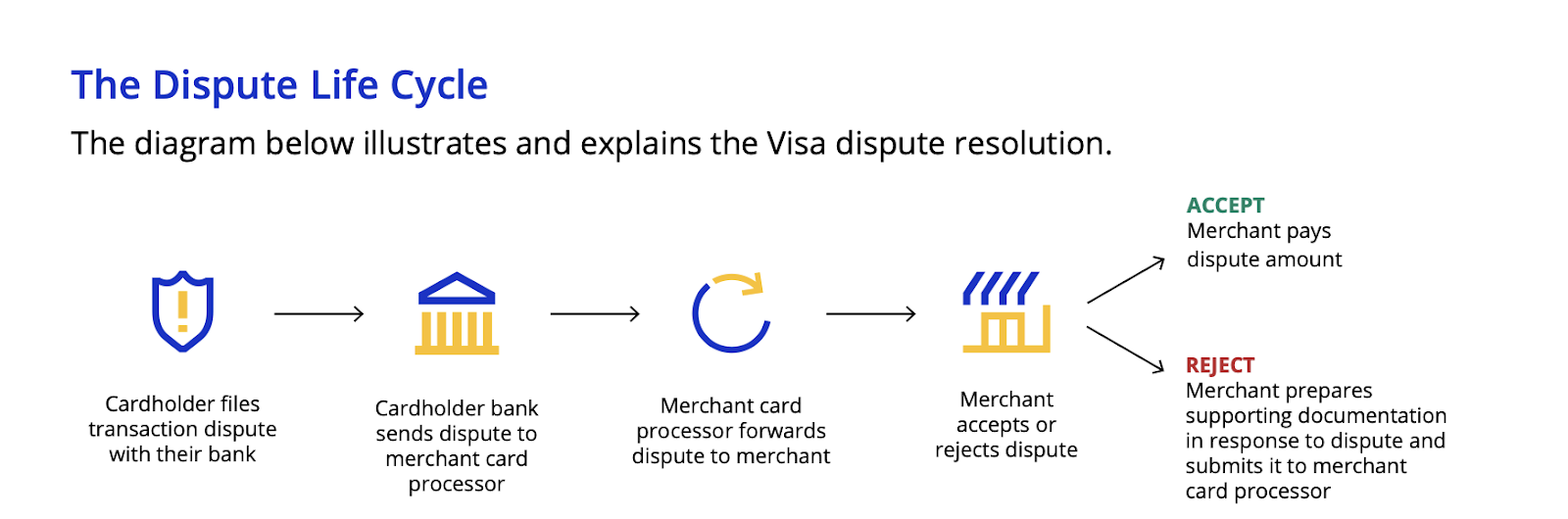

How Do Visa Chargebacks Work? A Complete Breakdown of the Dispute Process

Visa dominates the global payments landscape, with 4.48 billion active cards and over 233 billion transactions processed in 2024 alone. With that scale comes an equally complex dispute process. Visa's chargeback system has distinct rules and timelines that differ slightly from those of Mastercard's chargeback processes. Every merchant must understand the nuances to protect their revenue in these times.

The five-phase process of Visa disputes:

Phase 1: Inquiry Stage (Pre-Chargeback)

Timeline:

- Inquiry Response: 24-48 hours for merchants to respond to Visa Merchant Purchase Inquiry (VMPI)/Order Insight inquiries.

- Resolution Window: Up to 72 hours for inquiry resolution before a potential chargeback

Process:

Step 1: Cardholder Contact: When a cardholder contacts their issuing bank with a transaction concern (e.g., unrecognized charge, item not delivered), Visa requires the issuer to attempt to resolve the issue without filing a formal chargeback.

Step 2: Visa Merchant Purchase Inquiry (VMPI/Order Insight): The issuer submits an inquiry through Visa Resolve Online (VROL), generating an Extensible Markup Language (XML) message. This includes the transaction data to help you, the merchant, identify the transaction. Note: VMPI/Order Insight availability depends on the acquirer's integration with these tools; some issuers may bypass inquiries and initiate a chargeback directly.

Step 3: Merchant Response Options: You can:

- Provide additional transaction details to clarify the charge

- Issue an immediate refund to resolve the dispute

- Do nothing; accept that a chargeback is likely to be filed

Fees: No direct Visa fees for the inquiry stage. Acquirers may charge processing fees for refunds.

Phase 2: First Chargeback (Issuer Initiated)

Timelines:

- Cardholder: 120 days from the transaction date to file most disputes (exceptions exist, e.g., up to 540 days for certain fraud cases).

- Merchants: Effective July 21, 2025, processors like Adyen have put the dispute response timeframes at 9 days for the US and Canada and 18 days for other regions. This used to be 20 days (shortened from 30 days under VCR updates) from dispute day one (the day after chargeback initiation) to represent.

Process:

Step 1: Initial Chargeback: The issuing bank (ideally) evaluates the cardholder's claim under the Visa Claims Resolution (VCR) framework. If valid, the issuer initiates a chargeback through one of two workflows:

- Allocation Workflow: Rules-based, automated decisions for clear-cut cases (e.g., fraud).

- Collaboration Workflow: Manual review for complex disputes requiring evidence evaluation.

The issuer debits the transaction amount from the acquirer, provides provisional credit to the cardholder, and submits a dispute reason code with supporting documentation.

Step 2: Merchant Response (Representment): Merchants must explicitly accept liability or contest the chargeback through representment. Under Visa's updated dispute process (VCR), Visa no longer permits the default "no response" option.

The acquirer submits the merchant evidence to the issuer, who may:

- Accept the representment and reverse the chargeback.

- Reject it and escalate the case to pre-arbitration.

Fees: Visa introduced late response and acceptance fees as shown below. Acquirers typically charge $15-$25 per chargeback, with higher fees for high-risk merchants (fees vary by acquirer).

.png)

Success Rates by Evidence Quality:

- High-quality, reason-code-specific evidence with manual approaches: 8.1-20% win rates.

- Automated evidence compilation (with platforms like Chargeflow): up to 80% win rate.

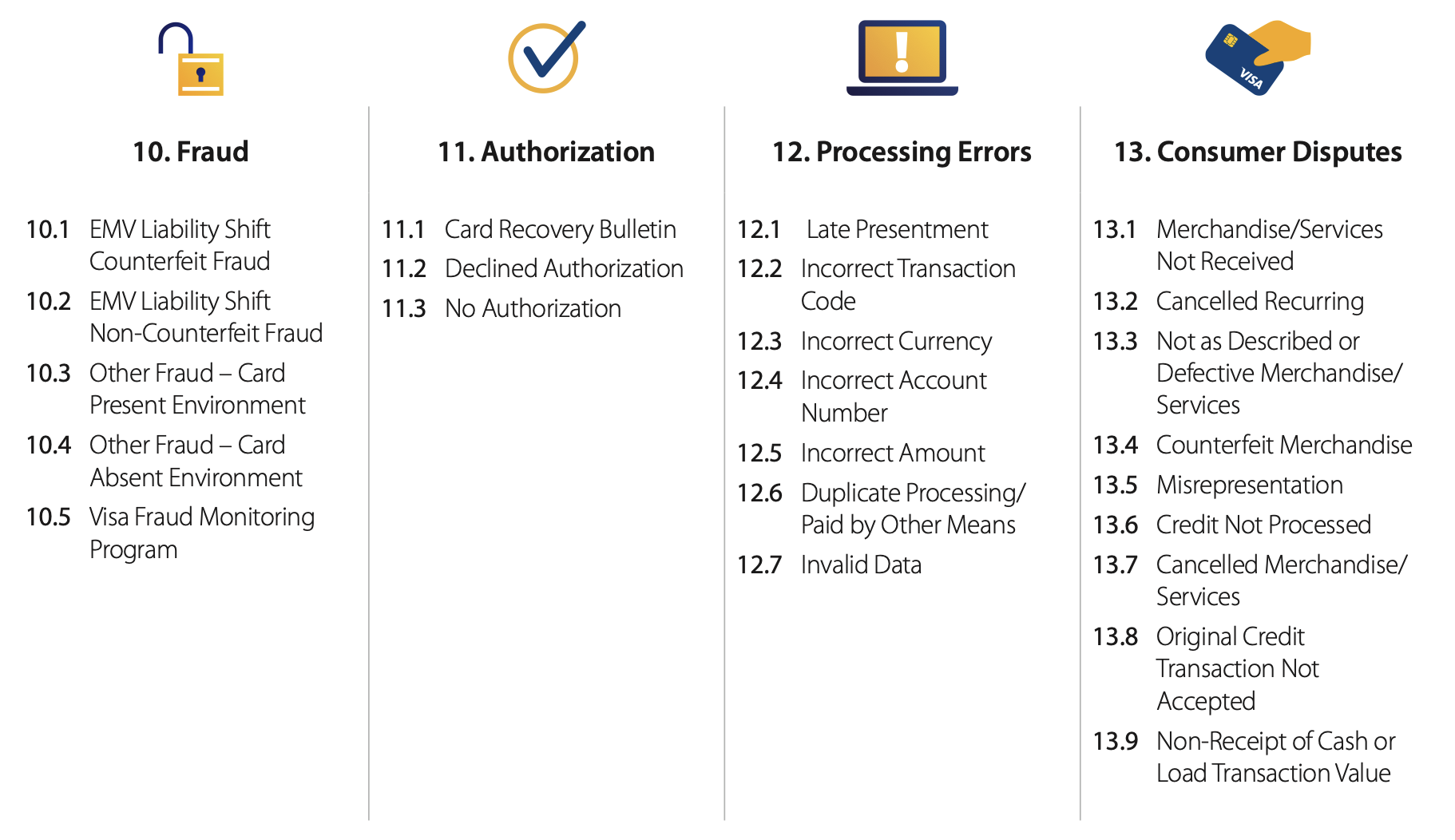

Common Visa Chargeback Evidence Requirements by Reason Codes

Visa periodically updates its chargeback reason codes. Below are the standard types of evidence most commonly required to support representment for frequent Visa dispute categories:

- Fraud (10.4: Other Fraud - Card-Absent Environment): Provide Address Verification Service (AVS)/Card Verification Value (CVV) match results, IP address verification, device fingerprinting, delivery confirmation, and proof of cardholder communication.

- Authorization (11.1: Cardholder Recovery Bulletin): Submit Authorization codes, terminal logs, and proof of proper card processing procedures.

- Processing Errors (12.1: Late Presentment): Provide transaction processing timestamps and evidence of timely submission within required timeframes.

- Consumer Disputes (13.1: Merchandise/Service Not Received): Submit delivery confirmations, tracking information, proof of digital delivery, or service completion documentation.

Phase 3: Pre-Arbitration (Second Chargeback)

Timeline: 30 days for merchants to challenge Allocation workflow decisions; Collaboration workflow timelines vary.

Process:

Step 1: Issuer Pre-Arbitration Filing: If the issuer disagrees with the representment outcome, they may initiate pre-arbitration, providing additional evidence or explaining why the merchant's response was insufficient. Note: Not all cases escalate to pre-arb; it depends on the issuer's decision.

Step 2: Merchant Pre-Arbitration Response: In Allocation workflow cases, merchants have limited conditions to challenge a Visa dispute. Options include:

- Accept financial liability

- Contest with additional compelling evidence

- Take no action (automatic liability assignment)

Fees:

- Filing fees: $25 to $50, depending on the acquirer.

- Dispute expired fee: $15 (introduced April 1, 2025, for automatic liability assignment).

🔥Pro Tip: Pre-arbitration cases have lower merchant win rates due to increased scrutiny. Cost-benefit analysis becomes critical at this stage, as it's often the last chance before arbitration. Either party has 10 days to request Arbitration after a pre-arbitration ruling.

Phase 4: Arbitration

Timeline: Up to 70 days for Allocation cases and 100 days for Collaboration cases.

Process:

Step 1: Issuer Arbitration Filing: The issuer submits the case to Visa's dispute resolution team. Visa requires the issuer to provide comprehensive evidence and justification for upholding the chargeback.

Step 2: Merchant Arbitration Response: The merchant may:

- Accept financial liability at any time before ruling

- Submit a detailed rebuttal with supporting evidence

- Take no action (automatic liability assignment)

Step 3: Visa Ruling: Visa's dispute resolution team evaluates evidence, procedural compliance, and applicable rules, determining:

- Financial liability

- Fee assessments

- Case closure

Fees:

- Filing fee: $500 (assessed to the losing party)

- Case file ruling fee: $600 (increased from $500 as of April 1, 2025).

- Noncompliance penalty: $250 (Discretionary fee for merchant violation of any Visa Merchant Agreement rules)

Phase 5: Appeal

Timeline: 60 days from the arbitration ruling.

Visa chargeback arbitration appeals are rare and subject to strict conditions. The losing party has 60 days from the arbitration decision to file an appeal. That is only if the original dispute amount is at least USD 5,000 (or local equivalent). The appellant must also provide material new evidence that was not reasonably available during the original case. Because Visa's arbitration ruling is typically final and binding, appeals are exceptions reserved for significant cases where fresh evidence justifies the added cost and effort.

Fee: $1,000

Why Do Visa Disputes Happen?

Visa disputes generally fall into four broad categories:

- Fraud

- Authorization

- Processing Errors

- Consumer Disputes

While eliminating Visa chargebacks may be unrealistic, merchants can implement proactive measures to minimize their occurrence. A substantial portion of Visa disputes result from preventable operational errors.

Yet, payment disputes don't exclusively arise from merchant actions or oversight. Contributing factors often include:

- Acquirer processing mistakes

- Issuing bank operational errors

- Cardholder misunderstanding or fraudulent claims (a.k.a. friendly fraud)

The formal dispute resolution process primarily involves communication between the cardholder's issuing bank and the merchant's acquiring bank.

Merchants may not be directly involved in every administrative exchange. However, this doesn't diminish their responsibility for dispute prevention and resolution efforts. After all, it is merchants, not acquirers, who ultimately bear chargeback responsibility.

How Can You Minimize Visa Disputes?

Avoidable Visa disputes stem from processing and customer service errors. With the right training and careful attention to detail, you can prevent many of them.

The following section outlines evidence-based prevention strategies and gives you a compliance roadmap to reduce legitimate Visa chargeback risks.

In-Person Transaction Processing Guidelines

- Transaction Authorization Requirements:

- Never process payments without first securing proper authorization approval.

- Reject any transaction where authorization has been denied.

- Refuse cards that have passed expiration date as shown by "Good Thru" or "Valid Thru" indicators.

- Chip Card Processing Best Practice: When processing chip-enabled cards, the card and terminal will automatically select the most suitable verification method. That can be the cardholder's signature, PIN, or Consumer Device Cardholder Verification Method. Signatures are unnecessary for PIN-verified transactions.

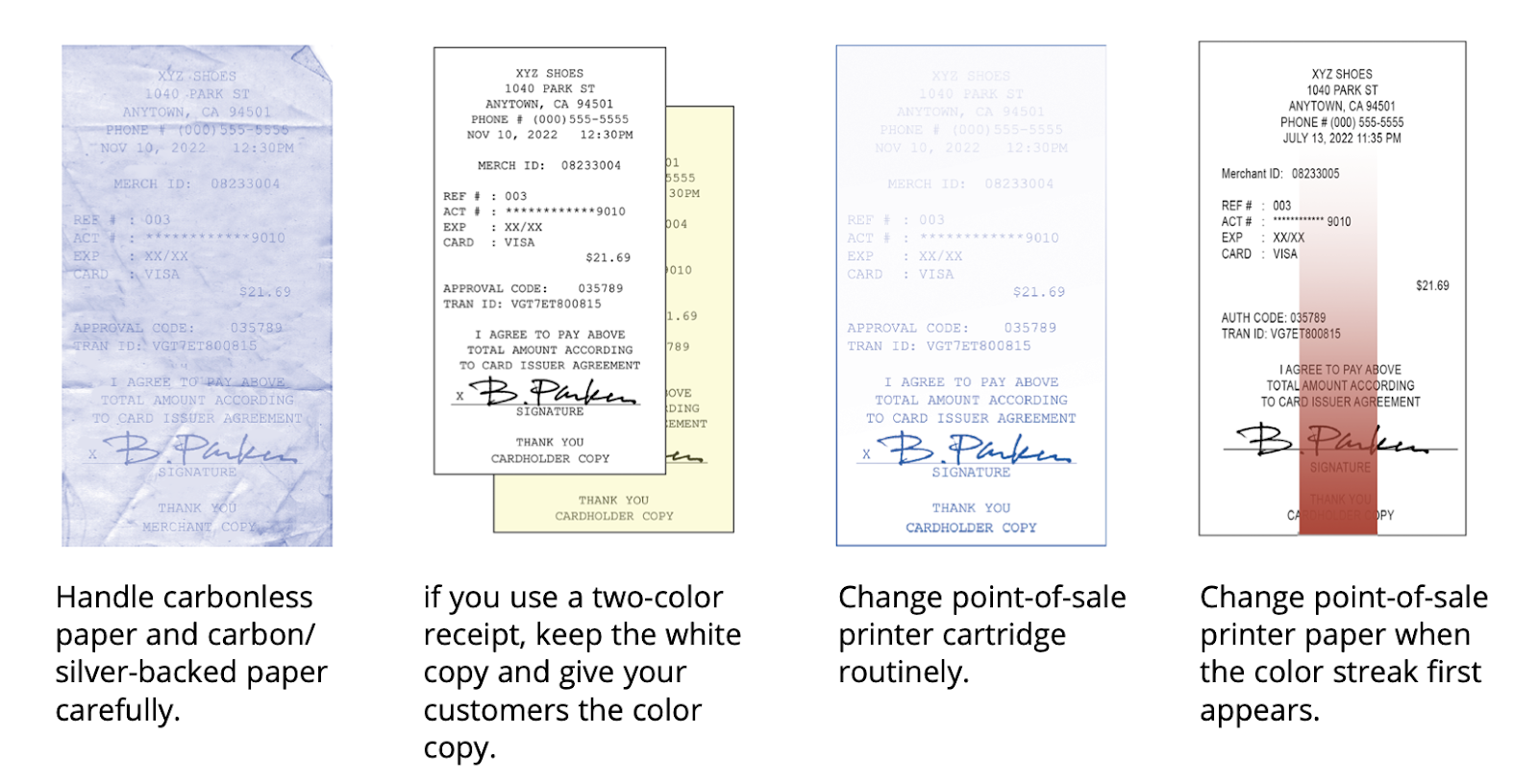

- Manual Entry Procedures for In-Person Sales: When manually entering card information during face-to-face transactions, create a physical impression of the card's front surface on the receipt using a proper imprinting device. Avoid using pencils, crayons, or similar tools, as these methods don't produce acceptable imprints. Without a proper card impression showing payment details and expiration date, fraudulent transactions may result in chargebacks even when authorized and signed.

- This requirement applies to all in-person transactions where manual entry is necessary, including situations involving chip cards and chip-capable terminals.

- Receipt Quality Standards: Verify that all transaction details on receipts are complete, accurate, and clearly readable before finalizing sales. Poor-quality or illegible receipts may be rejected during chargeback processing. With increased use of electronic scanning systems for receipt transmission, ensuring high-quality, readable documentation is crucial.

- Fraud Prevention for In-Person Transactions: When customers are physically present but only have payment credentials without the actual card, decline the transaction. Even with authorization approval, such transactions remain vulnerable to fraud disputes and potential Visa chargebacks.

Card-Not-Present Transaction Processing Guidelines

When you verify transactions using Address Verification Service (AVS) or CVV2, specific protections apply during Visa disputes, allowing your acquirer to contest chargebacks by submitting the appropriate response on your behalf.

Dispute Response Scenarios Requiring AVS Protection:

Your payment processor may defend disputed transactions under these conditions:

- Positive Match Scenario:

- Authorization returned a "Y" (positive match) for AVS verification.

- Billing address matches shipping address.

- Required documentation: Delivery address verification and signed receipt confirmation.

- System Unavailability Scenario:

- AVS inquiry was submitted during transaction approval.

- Received "U" response indicating card issuer system unavailability or lack of AVS support; address information couldn't be verified.

This applies to US, UK, and Canadian merchants.

CVV2 Verification Scenarios:

- Unsupported CVV2 Response: When merchants submit CVV2 verification during transaction authorization and receive a "U" status along with presence indicators 1, 2, or 9, this means the issuing bank does not offer CVV2 verification services.

- Non-matching CVV2 with Transaction Approval: For Mail/Phone Order or Electronic Commerce authorizations, merchants may encounter an "N" response paired with indicator 1 during authorization. In these cases, the issuing bank has approved the transaction despite the CVV2 mismatch.

🔥Pro Tip: CVV2 verification failures significantly weaken merchant chargeback defenses. "U" responses eliminate key fraud protection. "N" responses create vulnerability despite issuer approval. Fraud claims may still succeed. Document these responses to demonstrate you followed proper verification procedures.

Customer Service Best Practices that Stop Visa Chargebacks

Customer Billing and Sales-Receipt Guidelines:

- Billing Identification Requirements: Ensure your business appears clearly on customer credit card statements. Verify your merchant account displays the correct "Doing Business As" name and location.

- Receipt Requirements: Clearly print your company name on all receipts without obscuring transaction details. Keep logos and promotional content separate from payment information.

🔥Pro Tip: Test these by purchasing at your locations and reviewing how transactions appear on statements.

Data Entry and Clerical Error Avoidance Guidelines:

- Process each sale only once through your payment terminal

- Submit only one copy of each transaction receipt to your payment processor

- Avoid duplicate entries that can trigger customer disputes

- Void any incorrect receipts immediately

Deposit Timing Guidelines:

- Submit transaction receipts to your payment processor within 1-5 days. For refunds, process them the same day when possible to minimize customer confusion.

Customer Communication Guidelines:

- Pre-orders and Delays: Notify customers about any shipping delays and provide updated delivery dates.

- Out-of-Stock Items: Contact customers immediately when items are unavailable. Offer alternatives or cancellation options rather than making unauthorized substitutes.

- Shipping Protocol: For online/phone orders, ship merchandise before processing the payment to prevent billing disputes.

- Subscription Cancellation: Honor cancellation requests immediately and provide written confirmation with the effective dates. Stop all future billing once cancellation is requested.

🔥Pro Tip: If you get frequent chargebacks, operate in high-risk verticals, or sell high-value merchandise or services, use a data analytics tool like Insights to easily track chargeback sources. A pre-chargeback framework like Chargeback Alerts also helps prevent incoming cases by approximately 90%.

Advanced Compliance and Risk Management for Visa Merchants

Visa maintains strict oversight of merchant chargeback patterns. Excessive Visa disputes or fraud signal operational problems that can damage the network's reputation.

When cardholders experience frequent transaction issues, they often blame the payment network.

To protect brand integrity and cardholder confidence, Visa proactively identifies problematic merchants. They then mandate their payment processors to implement corrective actions through specialized monitoring programs. This is similar to Mastercard Chargeback Monitoring Programs.

Understanding Visa's Acquirer Monitoring Program (VAMP)

Visa previously tracked merchants' disputes and fraud exposure through the Visa Dispute Monitoring Program (VDMP) and Visa Fraud Monitoring Program (VFMP). Both programs have now been consolidated into the Visa Acquirer Monitoring Program (VAMP), which launched in April 2025 and tightened further on April 1, 2026.

VDMP/VFMP → VAMP: Implications for Merchants

VAMP eliminates the wiggle room merchants once had. You're either compliant or not compliant. Below are specific implications of the policy shift for merchants:

- Stricter Compliance Environment:

- Under VDMP, merchants had "Early Warning" and "Standard" buffers before reaching "Excessive."

- With VAMP, there's only one threshold: Excessive. The result? Less room for error and faster consequences if disputes or fraud escalate.

- Combined Fraud and Dispute Risk:

- Merchants can no longer treat Visa fraud (VFMP) and Visa disputes (VDMP) as distinct indicators.

- Visa now aggregates both in one basket with one ratio.

- Even if your fraud rate is low, too many chargebacks can push you over the edge, and vice versa.

- Tightening Thresholds:

- When VAMP launched in 2025, the merchant "excessive" ratio sat at 2.2% (220 bps).

- Effective April 1, 2026, that threshold dropped to 1.5% (150 bps) for most regions, narrowing the margin for error significantly.

- Merchants who were comfortable under the old rule can now be flagged on the same dispute volume.

- Enumeration Fraud Risks:

- If Visa notices too many bot-driven card testing attempts (≥20% of auths & >300k/month), they'll flag you.

- This forces merchants to adopt stricter bot defenses and fraud screening.

- Stronger Pressure on Acquirers:

- VAMP applies directly to Acquirers, but they'll effectively pass the pressure downstream.

- Expect stricter monitoring, higher reserve requirements, and quicker terminations for risky merchants.

- Less Tolerance for Borderline Merchants:

- Under VDMP, you could be in Early Warning for months with limited action.

- Under VAMP, once you're Excessive, you're exposed to fines, restrictions, and quicker terminations.

- Operational Impact: Merchants must now:

- Invest in dispute prevention tools (chargeback alerts, order validation, chargeback representment).

- Improve fraud detection and authentication (3DS, AVS, CVV, velocity checks).

- Tighten customer service and refund policies to prevent disputes from turning into chargebacks.

- Monitor VAMP ratio monthly, not just chargeback rate.

In summary, this Visa chargeback monitoring policy shift means merchants must now adopt a zero-tolerance strategy toward both fraud and chargebacks if they wish to stay under Visa's radar.

VAMP Formula and Thresholds (2026)

According to the Visa Acquirer Monitoring Program fact sheet, the VAMP ratio compares a merchant's fraud and non-fraud cases against their settled transactions.

- VAMP Ratio = Count of [Fraud Transactions (TC40) + Non-Fraud Disputes (TC15)] ÷ Count of Settled Transactions (TC05)

- Example: assume you have 800 reported fraud cases and 700 non-fraud disputes from 100,000 CNP transactions, your VAMP ratio for the given month will be: 800 TC40 + 700 TC15 ÷ 100,000 CNP transactions = 1.5% VAMP Ratio.

Visa says VAMP:

- Excludes disputes resolved through pre-dispute solutions, contingent on the timing of the data extract.

- Excludes TC40 fraud qualified for Compelling Evidence 3.0, contingent on the timing of the data extract.

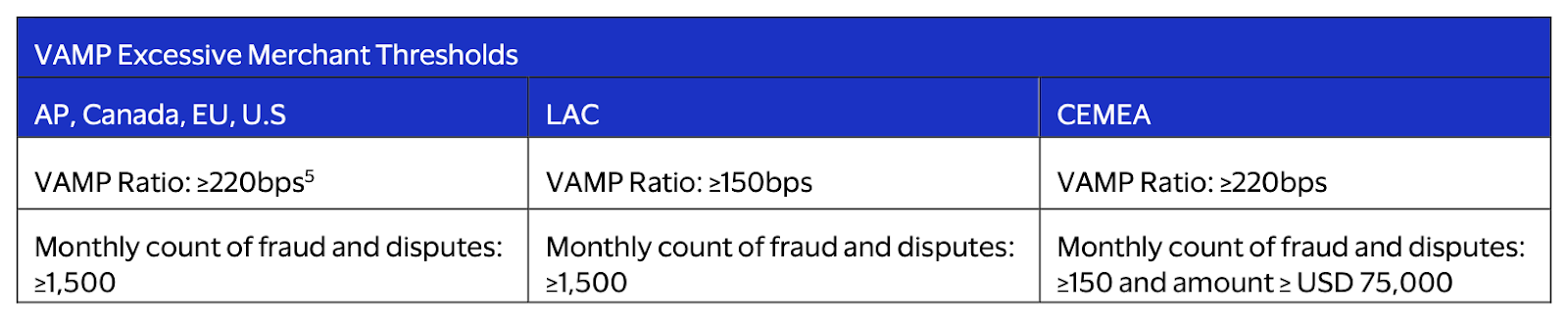

VAMP Thresholds For Merchants (effective April 1, 2026):

- VAMP Ratio: ≥ 1.5% (150 basis points) — reduced from 2.2% when VAMP launched in 2025.

- Minimum volume to qualify: at least 1,500 settled transactions; merchants with more than 1,000 combined fraud and non-fraud disputes in a month are most likely to be flagged.

- Merchant fee: $8 per dispute once classified as Excessive, administered through the acquirer.

- Regional exception: CEMEA merchants retain a 2.2% (220 bps) threshold with a lower monthly count.

- Enumeration Fraud Monitoring:

- Threshold: ≥ 20% of authorization attempts flagged as enumeration (card-testing fraud) on the Visa Account Attack Intelligence (VAAI) system, with a minimum of 300,000 enumerated transactions per month.

- Purpose: Targets brute-force card-testing attacks (e.g., testing card numbers, CVV2, or expiration dates).

VAMP Thresholds For Acquirers:

- Above Standard: VAMP Ratio ≥ 0.3% to < 0.5% (30–50 basis points).

- Excessive: VAMP Ratio ≥ 0.5% (50 basis points), with 1,000+ combined fraud and non-fraud disputes per month.

Consequences of Breaching VAMP Thresholds

Direct Consequences for Merchants

- Excessive Classification:

- Merchants are classified as Excessive if their VAMP Ratio exceeds published thresholds.

- Financial penalties are assessed as follows:

- Merchants: $8 per dispute in the Excessive tier, administered through acquirers.

- Acquirers: penalties scale by tier, applied at the portfolio level.

- Visa may adjust fines at its discretion. They require remediation plans within 15 days.

Indirect Merchant Impact through Acquirers

Because Visa designed VAMP to hold acquirers accountable, merchants feel indirect consequences when their acquirer approaches Excessive levels, as highlighted earlier. The result?

- Stricter Underwriting: Higher reserves, rolling holds, or increased processing fees.

- Account Restrictions: Tighter monitoring or contract non-renewal.

- Mandatory Controls: Acquirers may require merchants to adopt stronger fraud-prevention tools.

- Lower Tolerance Than Visa's Published Thresholds: Acquirers often set stricter internal limits to protect themselves.

VAMP Enforcement Timeline

- Advisory Period (April 1 to September 30, 2025): Merchants received notifications if ratios exceeded thresholds, but Visa did not apply financial penalties during this window. Acquirers, however, could still act preemptively.

- Full Enforcement (October 1, 2025 onward): Visa began formal enforcement actions for merchants above Excessive thresholds.

- Tightened Thresholds (April 1, 2026): The merchant excessive ratio dropped from 2.2% to 1.5%, pulling more merchants into enforcement scope.

How to Win Visa Chargeback Disputes in 2026 and Beyond

The dirty little secret of chargeback disputes is that issuing banks often have financial incentives to side with cardholders. It's true. They collect interchange fees on every transaction. But chargebacks generate more revenue through fees while keeping customers happy.

Here's how to counter-program.

Master The Chargeback Customer Profile

The ideal chargeback customer:

- Views chargebacks as "free refunds with benefits"

- Believes merchants have unlimited money to absorb losses

- May not understand they're committing fraud

Counter-Intelligence Strategy:

- Use data analytics to excavate chargeback patterns and transaction velocity.

- Deploy behavioral triggers: Customers who request refunds after 30+ days are more likely to file a chargeback later.

- Use chargeback alerts to auto-refund or plan evidence collection for such high-risk transactions.

Level Up with Advanced Tactics

- Level 1 (Everyone Does This): Gather transaction receipts, delivery confirmation, and ancillary documents.

- Level 2 (Smart Merchants): Deploy device fingerprinting, IP geolocation, etc.

- Level 3 (Veteran Fraud Fighters): Use the tactics below:

Phase 1: The "Digital Breadcrumb" Method

- Use automated chargeback management to create evidence DURING the transaction, not after:

- Force customers to acknowledge specific terms like return policy in separate steps

- Capture micro-interactions (scroll depth, time on page, mouse movements)

- Screenshot the customer's cart with timestamps overlay

- Record the exact payment flow path they took, etc.

Phase 2: The "Customer Behavior Fingerprint"

Automated chargeback dispute frameworks build profiles that banks can't ignore:

- Track return/refund request patterns

- Document customer support interaction tone and frequency

- Map cardholder's purchase timing

- Analyze their product research behavior pre-purchase

Phase 3: The "Social Proof Dynamite"

- Building on phase 2, the system generates deeper evidence that psychologically pressures bank reviewers:

- Show other customers buying the same product simultaneously

- Include positive reviews from verified purchases posted AFTER the disputed transaction

- Demonstrate ongoing customer engagement (newsletter opens, app usage) post-purchase

Phase 4: Processor Relationship Exploitation

Processors batch dispute responses. Your individual case gets 2-3 minutes of review time. That's one of the reasons manual Visa chargeback disputes fall short.

Automated systems lead with the strongest evidence, format documents adequately, and submit your Visa chargeback evidence before Visa dispute deadlines. You don't run out of time.

Frequently Asked Questions

What is the time limit to dispute a Visa chargeback?

Cardholders generally have 120 days from the transaction date to file a Visa dispute, with exceptions up to 540 days for certain fraud cases. Merchants have far less time to respond — many processors now allow as few as 9 days (US/Canada) to 18 days (other regions) to submit representment evidence.

How much does a Visa chargeback cost a merchant?

Acquirers typically charge $15–$25 per chargeback. Escalation adds more: pre-arbitration filing runs $25–$50, arbitration filing is $500 with a $600 ruling fee, and appeals cost $1,000. Merchants in VAMP's Excessive tier also pay an $8-per-dispute fee.

What is the Visa VAMP threshold for 2026?

As of April 1, 2026, the merchant "excessive" VAMP ratio threshold is 1.5% (150 basis points), down from 2.2% when the program launched in 2025. The VAMP ratio combines fraud (TC40) and non-fraud disputes (TC15) divided by settled CNP transactions. CEMEA merchants keep a 2.2% threshold.

Can merchants win Visa chargeback disputes?

Yes. Win rates depend heavily on evidence quality and speed. Manual representment with reason-code-specific evidence wins roughly 8–20% of cases, while automated platforms like Chargeflow reach up to 80% by compiling stronger evidence and submitting before deadlines.

What is the difference between a Visa inquiry and a chargeback?

An inquiry (VMPI/Order Insight) is a pre-chargeback request for information that lets you resolve a concern before it becomes a formal dispute. A chargeback is the formal reversal of funds, which carries fees and counts toward your VAMP ratio.

Final Thoughts on Visa Chargebacks and Next Steps

The uncomfortable truth about Visa chargebacks is that your merchant account is under siege. Consumers increasingly favor chargebacks over refunds for convenience. They've weaponized the system.

Merchants reported a 10% increase in chargeback cases in 2024. But the real story lies in VAMP. Merchants must now manage a combined fraud and dispute ratio, and as of April 2026 that threshold tightened from 2.2% to 1.5%.

So while everyone is talking about staying under thresholds, what no one is telling you is that your processor's internal "soft limits" matter more than Visa's published thresholds. With acquirers facing an Above Standard line as low as 0.3%, they'll push the risk down to you. They'll restrict you before Visa even notices you exist.

Yet, your processor gets paid whether you lose or win disputes. You're the only one with skin in the game.

Merchants who win Visa chargeback disputes today aren't just fighting chargebacks. They are using automation to crack consumer psychology, master chargeback time limits, and transform information gaps into profits.

Next Steps:

For All Merchants:

Dispute patterns are predictable within merchant categories. If you map your first 90 days of chargebacks by customer behavior markers, you can predict future disputes with up to 80% accuracy.

The Method:

- Install Chargeflow Insights (free). Track every data point on customers who chargeback in your first quarter.

- Apply those patterns to flag future risky customers.

- Use Chargeback Alerts to auto-refund and blacklist these problematic actors.

- Implement chargeback automation to prevent disputes from slipping through the cracks.

- This single technique can cut your Visa dispute rates by 40-60%.

For Merchants With Excessive VAMP Ratios:

Understand how processors think. Small merchants can actually operate in higher-risk categories if they understand processor math. Your individual impact on their portfolio might be negligible. Negotiate based on this.

Your processor makes more money from you staying than from terminating you. High-risk merchants pay 3-5x normal rates. Use this.

- If you're borderline on ratios, offer to pre-pay reserve increases instead of termination.

- Work with chargeback specialists like Chargeflow to lower your ratios.

- Remember: Processors lose money on merchant turnover; they have discretionary authority even if they claim they don't.

If you've been playing checkers, you're now equipped to play chess! Manage Visa chargebacks like a pro. Start for free.

This guide represents current industry best practices and Visa requirements based on publicly available information as of the time of writing.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)

.avif)

.avif)