%201.svg)

Friendly Fraud: The $132 Billion Threat to eCommerce Merchants – and How to Fight It in 2026

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

- Friendly fraud (chargeback abuse) drives up to 75% of chargeback losses and costs merchants an estimated $132 billion a year.

- It happens when a real customer disputes a legitimate, delivered purchase instead of requesting a refund, whether by mistake or on purpose.

- Verify buyers, clarify billing descriptors, and use dispute alerts to catch disputes before they become chargebacks.

- Automated chargeback representment now outperforms manual processes, with win rates above 75% versus an 8.1% industry average.

Ecommerce brands carry the brunt of this problem, which is why dedicated friendly fraud prevention for ecommerce combines automated alerts with evidence-backed recovery.

Friendly fraud doesn't come from stolen cards or criminal rings. It comes from your own customers. You fulfilled the order. The payment cleared. The product arrived. Then a chargeback hit anyway.

At $132 billion in annual losses, it's now the dominant driver of chargebacks in eCommerce, real customers, disputing real transactions.

This guide breaks down why it happens, how to prevent it, and how to win when it does.

Quick answer: Friendly fraud happens when a real customer disputes a legitimate, delivered purchase with their card issuer instead of asking the merchant for a refund. Nothing about the transaction was fraudulent: the payment was authorized and the order arrived, but the customer files a chargeback anyway. It now drives up to 75% of all chargebacks and costs merchants an estimated $132 billion a year.

What is Friendly Fraud?

Friendly fraud, also known as chargeback abuse or first-party fraud, is when a cardholder disputes a legitimate purchase by claiming it is unauthorized or fraudulent to obtain a refund, while often retaining the product.

Friendly fraud differs from other chargeback cases because the instigator, the cardholder, is most likely a customer rather than a third-party fraudster. In other words, the disputed transaction warrants no chargeback claim.

While the triggers and circumstances vary from case to case, cardholders commit friendly fraud for two main reasons:

- They Forgot About the Transaction: Cardholders may not recognize a charge due to unclear merchant names on the statement or forgotten subscriptions. Cases resulting from this scenario are known as unintentional friendly fraud.

- They Want to Steal From the Business: Some cardholders exploit the chargeback system to obtain free goods or services by disputing a purchase even when there is no merchant misrepresentation. They use this strategy to get their money back if they regret or dislike a purchase. This scenario is the dictionary definition of chargeback fraud.

“First-party misuse has become more widespread and more damaging, both to merchant businesses and to the issuers, acquirers, and other payment partners that support eCommerce transactions.” – Merchant Risk Council

The Evolution of Friendly Fraud: Why AI Matters More Than Ever

Friendly fraud was first observed in the chargeback timeline in 2010. Before then, chargebacks categorized under fraud reason codes were generally rare. They’re almost always indicative of genuine card fraud.

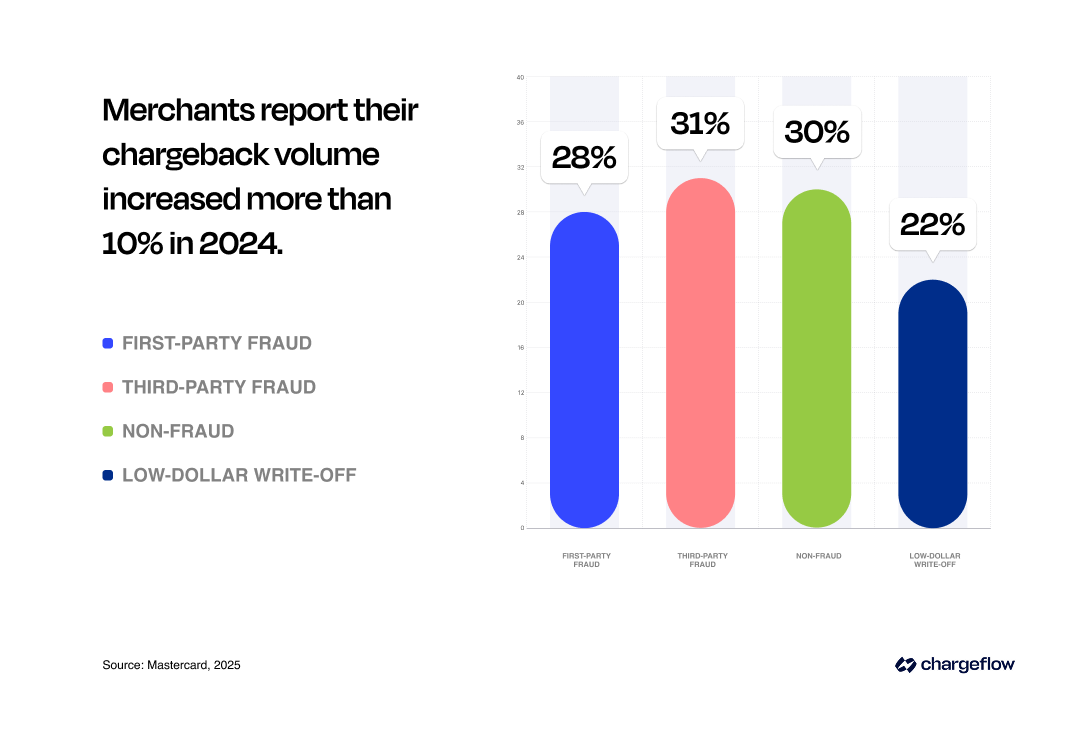

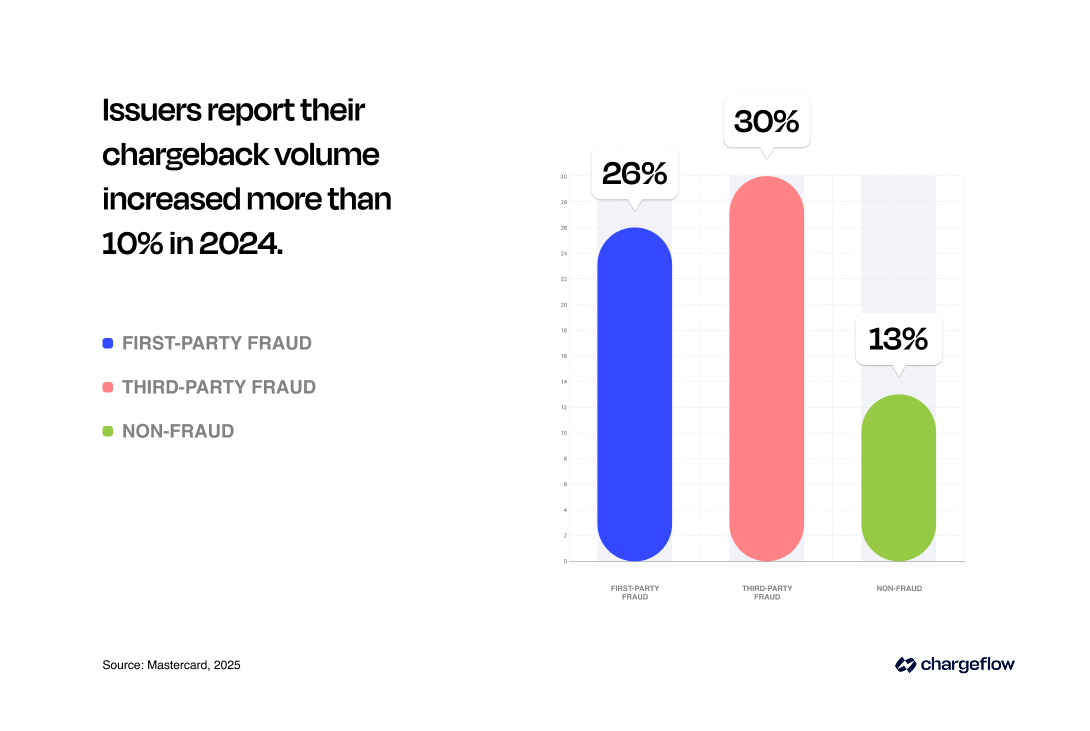

Today, friendly fraud is the main driver for the increase in cardholder disputes, with 79% of merchants reporting first-party fraud in 2024, up from 34% in 2023 (Visa Acceptance Solutions, 2024). The average dispute costs merchants $74 (this varies by industry, as you can see in the image below).

The spike in disputes has pushed merchants and banks to adopt AI-based fraud prevention, real-time data checks, and automated representment tools.

Why the Surge?

What’s driving this meteoric rise in fraud losses, you ask? Let's break it down:

1. Digital Commerce Explosion

More online transactions correlate to higher payment disputes, legitimate or not. eCommerce's convenience isn't without a downside. It's increasingly easier for cardholders to dispute a transaction than to contact a merchant for remediation.

2. Shifting Consumer Behavior

Cardholders expect fast, frictionless service. When disappointed, they turn to chargebacks. Behavioral AI models can now detect unusual buying or dispute patterns early, minimizing losses.

3. Flawed Chargeback System

The chargeback system was originally designed as a fair mechanism for resolving payment disputes. But it's deeply flawed. Banks and card networks prioritize the consumer. This systemic imbalance makes it much easier for cardholders to commit friendly fraud intentionally.

Many cardholders prefer to dispute a charge at the first sight of a problem rather than contact the seller. Winning those cases is no easy task for merchants. According to Mastercard, merchants win only a minuscule 8.1% of disputes they represent.

4. Social Media Influence & Emerging Trends

Platforms like TikTok popularized "chargeback hacks," where users share tips for disputing legitimate transactions (Forbes, 2024). This trend amplifies friendly fraud among younger consumers.

Over in Europe, the payments industry has recorded a new form of friendly fraud involving bank transfers rather than credit card payments. Fraudsters exploit SEPA bank transfer rules to recall payments after settlement, bypassing merchant consent. This has heightened as some banks mishandle SEPA SCT Recall requests, reversing payments without consulting the payee, thereby allowing fraudsters to reclaim funds after receiving goods or services.

5. The Tech Tug-of-War

The ongoing AI arms race enables fraudsters to bypass traditional security measures. Merchants often struggle to detect fraudulent disputes until it's too late. As Stripe noted, today's fraudsters operate with industrial precision, employing sophisticated teams of engineers, managers, and data analysts to execute their schemes at scale. Fraudsters are leveraging artificial intelligence at every stage of the attack, which means merchants must adopt AI as well to keep up, reduce false claims, and spot first-party misuse faster than manual systems ever could. This risk is compounding as AI shopping agents start making purchases on a customer's behalf, raising new AI agent chargeback liability and agentic commerce chargeback questions merchants haven't had to answer before.

However, AI is not just a tool for fraudsters. It's also a powerful weapon for prevention across different industries. For example, ScienceSoft’s experience shows that insurance fraud detection solutions can unlock 200% to 1,000% ROI when supported by the right automation and analytics factors. The U.S. Treasury recently announced that machine learning AI helped prevent and recover over $4 billion in fraud in FY24. We'll shed more light on AI-driven chargeback prevention in a subsequent section.

Unraveling The Detrimental Impact of Friendly Fraud

Friendly fraud affects merchants, banks, and even the perpetrators themselves. It creates a ripple effect across the eCommerce ecosystem. Here’s how friendly fraud affects these parties:

How Friendly Fraud Affects Merchants

The frequency of friendly fraud means businesses now spend more time and resources disputing meritless cases. The result?

- Revenue loss and financial difficulties.

- Sales cannibalization, since lost goods often appear in secondary markets.

- Extensive labor costs due to additional headcount to handle fraud-related issues.

- Loss of goodwill; frequent friendly fraud drives away new customers and undermines trust with existing clientele.

- Loss of sales due to strict store policies to combat rising fraud cases.

- Penalties from payment partners, including, in extreme cases, loss of payment privileges.

Despite new policies, like Visa’s Compelling Evidence 3.0, aimed at mitigating severe consequences for merchants, friendly fraud continues to be a costly problem with downstream impacts.

But it also complicates matters for banks as they become pulled into disputes between customers and merchants, which they would ordinarily not be involved in.

How Friendly Fraud Affects Banks

Card networks like Visa, Mastercard, Amex, and Discover set participation requirements for banks that issue and process their cards. These networks use chargebacks as a consumer protection mechanism to build trust in card payments and encourage card usage, while also helping them avoid regulatory backlash. However, chargebacks also expose banks to operational and financial risks.

- Dispute Costs: Banks must handle the transaction reversal process, pay additional fees, and invest in processing and investigations. These tasks are resource-intensive, and while banks may pass some costs to merchants through chargeback fees, they often still absorb significant losses, especially in high-volume or high-dispute environments.

- Trust Erosion: Card issuers are expected to protect cardholders. But routinely siding with them in weak or meritless claims, especially when merchants cannot submit compelling evidence, can damage relationships with legitimate businesses. Over time, this erodes merchants' trust in the payment ecosystem.

- Compliance Pressures: Excessive friendly fraud increases compliance burdens for financial institutions, which raises operational costs.

How Friendly Fraud Affects Cardholders

False and fraudulent chargebacks hurt merchants the most. But it also has some repercussions for perps.

While prison time is rare, cardholders who file false chargebacks still face consequences, including:

- Loss of purchasing access as merchants suspend and blacklist cardholders who perpetuate friendly fraud.

- Loss of banking rights as some banks terminate cardholder accounts of individuals known to engage in chargeback fraud.

- A poor credit score, as losing banking rights, damages the cardholder’s credit score due to a lack of credit utilization. Regular credit monitoring can help cardholders spot unexpected changes or unfamiliar activity that may affect their credit profile.

- Filing a frivolous chargeback means the cardholder forfeits any consideration for resolving their grievance, and if you win the case, the matter is permanently closed.

That said, the onus is still on merchants to close all loopholes that could result in friendly fraud.

How to Prevent Friendly Fraud

One of the reasons friendly fraud is incredibly challenging for merchants to deal with is that some claims are valid. Some cardholders are honest. The cardholder might have reported an actual problem.

For instance, a minor made the transaction, and the cardholder is trying to reverse it, but it's taking too long due to your store's policies.

With that in mind, below are preventive measures (part of a broader chargeback mitigation strategy) you can implement to stop friendly fraud from burning a hole in your balance sheet.

1. Before Transactions:

- Authenticate the buyer’s identity to stop unauthorized transactions

- Require customers to review and confirm orders before finalizing their purchase.

- Outline your return policy and ensure the customer accepts the terms.

- Consider making a phone call to confirm the purchase and address discrepancies when a high-value transaction or new customer is involved.

- Use secure payment service providers that comply with necessary security standards.

- Collect as much data as possible, including order history and contact information, to help address potential fraud (see our ecommerce fraud prevention guide for a full framework), and use AI based identity and behavior checks to detect first-party misuse before a dispute occurs.

2. After Transactions:

- Send the buyer a detailed order receipt, including transaction description, order number, and details, and ensure they can access the same online. But adding AI-powered dispute alerts and behivor monitoring greatly reduces risk.

- Provide real-time tracking to limit buyer’s remorse or delivery doubts.

- Follow up with customers after delivery to confirm receipt and satisfaction; you need this tool when a chargeback arises.

- Encourage customer reviews and feedback to identify lapses or showcase your brand image to prospects.

- Follow industry best practices for posting and recording transactions.

- Use chargeback alerts to prevent friendly fraud before it happens.

🔥For Deeper Friendly Fraud Prevention Insights: Explore our guide on actionable strategies for mitigating chargebacks through consumer psychology for more insights. I also suggest you read this piece on how digital goods sellers can combat rising chargeback fraud.

How to Dispute Friendly Fraud Chargebacks Successfully

If you’re wondering whether friendly fraud claims are winnable, the answer is YES!

But success requires robust evidence and efficient processes.

Seriously, you don’t have to keep writing off those losses as the cost of sales, which is a double negative. By doing so, you’re inadvertently telling scammers to keep it coming. And, as we’ve already noted, excessive chargebacks affect your payment processing privileges. If you can't keep your chargeback ratio under the card network-approved margin, you'll move into the card network monitoring program and face severe fines.

So, how do you dispute friendly fraud and win? There are two strategies you can explore:

Option A: Manual Chargeback Representment

If you choose to pursue manual representment, be prepared to gather comprehensive, compelling evidence, such as:

- Delivery proof (e.g., signed receipts, order tracking),

- Cardholder signatures or IP address match for online transactions,

- Copies of purchase receipts,

- Return policy screenshots from checkout.

- Relevant customer communication, e.t.c.

You need to submit your documentation promptly in the correct format, adhering to card network rules, and follow up if additional evidence is requested.

That said, traditional chargeback management practices are becoming increasingly ineffective, as cardholders can now file disputes with a single click. The process is time-consuming, time-consuming, and often yields poor results: only an 8.1% success rate (Mastercard, 2025).

Even major financial institutions and card networks acknowledge the complexity of the traditional chargeback process. Mastercard says, “The chargeback process is costly and time-consuming. So, it should not be surprising that Financial Institutions (FIs) are steering away from manual human review toward analysis supported by automation or AI-based models.”

Option B: Automated Chargeback Dispute

Cutting-edge systems like Chargeflow automate the entire chargeback lifecycle so you can win disputes without lifting a finger. The outcome has consistently been higher than the industry average, above 75%.

The wonderful thing about an automated chargeback management system like Chargeflow is that it:

- Uses AI to scrutinize customer footprint in real-time to pinpoint impending friendly fraud, focusing on customer intent rather than identity.

- Trains machine learning models on historical data to track inconsistencies between real transactions and fraudulent chargebacks, staying ahead of the curve in dispute prevention.

- Streamlines chargeback processing, minimizing manual tasks and empowering merchants to recover revenue with ease.

- Helps you block unwanted customers or stop chargebacks before they happen.

By the way, you only pay for successfully disputed chargebacks.

With chargeback volumes surging, 261 million this year alone, merchants are now prioritizing advanced technology and tools to streamline chargeback management.

🛑Read this case study of Chargeflow client Elementor and see how chargeback automation protects merchants from friendly fraud.

Final Thoughts on Friendly Fraud

Every research, report, or commentary on chargeback trends has one reverberating conclusion: friendly fraud is a growing challenge for eCommerce businesses. It's a $132 billion-per-year challenge with no end in sight. Artificial intelligence is becoming a critical tool in understanding transaction patterns and reducing the impact of first-party misuse.

When cardholders slap a vendor with friendly fraud, the predictable outcome is financial losses, penalties, and a damaged reputation. Without proactive measures, such as addressing fraud loopholes before processing transactions and using automated chargeback management to guard against con artists, it'll be extremely tough to survive friendly fraud. AI powered chargeback systems give merchants a faster and more accurate way to prevent disputes and strengthen evidence in real time, which is now essential for staying ahead of rising fraud trends.

Granted, you can’t possibly stop all friendly fraud cases. But you can minimize occurrences and win meritless claims that slip through the cracks. So act now! Automate your chargebacks today.

eCommerce businesses are facing myriad challenges these days. The last thing you need is to leave your chargeback management to chance.

Key Takeaways

- Scale: At least 75% of chargeback losses (or $132 billion) tie to friendly fraud.

- Prevention: Verify buyers, clarify charges, be responsive, offer refunds when necessary, and use dispute alerts to stop chargebacks in their tracks. AI can also flag high-risk behavior before a dispute occurs.

- Disputes: Merchants are shifting from manual representment to the more effective automated chargeback processing, which offers higher win rates with no stress. AI strengthens evidence, reduces manual work, and improves dispute outcomes.

By blending proactive strategies, AI driven analysis, and industry advocacy, merchants can turn the tide against friendly fraud. All the best!

Friendly Fraud FAQ

What is friendly fraud in simple terms?

Friendly fraud is when a real customer disputes a legitimate charge with their bank instead of asking the merchant for a refund. The purchase was real, the product was delivered, and the payment was authorized, but the customer files a chargeback anyway. Despite the name, there's nothing friendly about it for merchants.

What is accidental friendly fraud?

Accidental (or unintentional) friendly fraud happens when a cardholder genuinely doesn't recognize a charge, often because of an unclear merchant name on their statement or a forgotten subscription, and disputes it without meaning to defraud the merchant. It differs from intentional friendly fraud, where the cardholder recognizes the purchase but disputes it anyway to get free goods or a refund. Clear billing descriptors and proactive order confirmations are the best way to prevent the accidental kind.

What's the difference between friendly fraud and chargeback fraud?

Chargeback fraud is the umbrella term. Friendly fraud is a specific type where the person who made the purchase is also the one disputing it. Criminal fraud involves a stolen card and an unauthorized transaction. Friendly fraud involves a legitimate customer and a valid transaction, which is exactly what makes it harder to detect and fight.

Is friendly fraud illegal?

Intentional friendly fraud, where a customer knowingly files a false dispute to keep goods or get a refund they're not entitled to, is technically fraud under the law in most jurisdictions. In practice, prosecutions are rare. But consequences do exist: merchants can blacklist repeat offenders, and banks can close accounts or restrict dispute privileges for customers with a pattern of abuse.

How do I prove friendly fraud to my bank?

You can't go directly to the bank, you respond through the chargeback representment process to the card network. The evidence that matters most is: proof of delivery (carrier timestamps, signature confirmation), proof of authorization (IP address, device fingerprint, login history for digital goods), customer communication logs, and a clear record of your refund policy shown at checkout. The goal is to connect the cardholder to the transaction in a way the issuer can't ignore.

What happens to customers who commit friendly fraud?

Most face no legal consequences, but the downstream effects are real. Merchants can permanently ban them and share data through fraud networks. Banks monitor dispute patterns, repeat filers can lose dispute privileges or have their accounts reviewed or closed. A lost banking relationship damages credit utilization and credit scores. And if a merchant wins the representment, the case is closed with no further recourse for the cardholder.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)

.webp)

.webp)

%20(1).webp)