%201.svg)

Online Dating Site Chargeback: How to Prevent and Win With AI

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

Online dating site chargebacks are burning cashflow for platform owners at rates most merchants would consider catastrophic. The culprits are structural: the inherent buyer’s remorse of paying for romance that didn’t materialize, recurring billing that users forget, and discreet descriptors that spouses don’t recognize. AI-powered dispute automation is not a marginal efficiency gain. It is the mandatory firewall against this unique threat model.

The $3.17 billion online dating market (growing to $3.45 billion by 2029 per Statista) operates on subscription economics that payment processors classify as high-risk. And for good reason. Online dating Chargebacks impact up to 1% of transactions. The business model inherently operates near the card network’s financial and regulatory penalty threshold.

AI changes this calculus drastically. Modern machine learning-based solutions (like Chargeflow) track dating site chargeback patterns invisible to rule-based systems. It predicts disputes before they’re filed, and automates evidence collection. The result is usually 70-90% representment wins!

This guide breaks down the mechanics: which online dating chargeback vectors matter most, where legacy prevention fails, and how to implement AI solutions that move your dispute rate to acceptable levels.

Before we jump in, let’s clarify the basics everyone skips.

What Is an Online Dating Site Chargeback?

An online dating site chargeback is a forced payment reversal that occurs when a user disputes a charge with their bank or card issuer instead of contacting you, the platform owner, for remediation. Like any other chargeback, the customer’s bank simply takes the money from your account, gives it to the customer, and collects extra fees as penalty. You’re left holding the bag, even if the customer actually used your service.

Contrary to what many think, dating site chargeback is by no means a refund. It’s a $15-100 penalty per dispute, plus the cost of the transaction value, customer acquisition, and internal representment labor.

Another thing worth mentioning is that chargeback fees aren’t necessarily what kills your dating app. It’s the sheer volume of disputes. While merchants assume this high volume signal fraud, most online dating chargebacks aren’t fraudulent. At least, not in the way you might expect. Here’s what’s actually happening:

The Uniquely Toxic Chargeback Vectors Facing Dating Platforms

Dating platforms deal with unique chargeback risks because their payment system is intertwined with user emotions. We can group these online dating site chargebacks into three main categories:

1) The “I Paid But Didn’t Get Results” Problem

When a user pays for a dating site, they are buying a chance at a romantic outcome. If they feel the service didn’t deliver what they wanted, they often dispute the charge out of frustration. They claim ‘service not rendered’ even if they accessed and used the platform.

- Example: A premium subscriber who did not secure a date within a promotional period disputes the full charge out of frustration and perceived failure of the product.

2) The Billing Descriptor and Forgotten Subscription Problem

Some dating platforms use discreet billing descriptors instead of recognizable brand names for user privacy. Charges appear as generic names or codes like “WEBSERVICES”, “ONLN SVCS”, or “MEMBER4829” to avoid unwanted disclosures of the service on bank statements.

This often becomes problematic. A user sees the charge three months later and genuinely doesn’t remember signing up. A spouse discovers an unfamiliar descriptor on a shared credit card statement and reports it as fraud, whether to expose infidelity or because they legitimately don’t recognize it. Either way, the bank sides with the cardholder, and you’re slapped with a dating site chargeback for trying to protect user privacy.

The paradox is that users demand discretion during signup. But then dispute charges precisely because they were discreet.

3) The Date Now, Dispute Later Problem

This online dating site chargeback vector keeps platform owners up at night. A growing segment of users treat dating subscriptions as interest-free loans they never intend to repay. They:

- Pay on Friday night,

- Swipe, match, message, and go on dates all month,

- On day 29, call their bank and say “I never authorized this” or “Service not provided, zero matches,”

- Pocket the refund and often re-subscribe the next weekend with the same card!

It’s not out of confusion or forgetfulness. They simply want to exploit a consumer-protection system that was never built for intangible, experience-based services. A prime example is the recent Operation Chargeback investigation. It exposed three criminal networks that allegedly attempted to steal over €750 million ($860 million) across three continents:

The core challenge for dating platforms is proving service delivery. Card-network rules put the burden of proof on you, the merchant, to show:

- Explicit authorization of recurring plan

- The service was delivered and actively used

Under Visa Compelling Evidence 3.0, data such as login IDs, IP address or device-fingerprint matching, and prior undisputed transactions can form a strong defense against fraud-based disputes.

However, for non-fraud codes (e.g., Services Not Provided / Not as Described), digital-service usage logs rarely guarantee success. CE 3.0 does not standardize proof of perceived value or outcome like matches or dates.

Chargeback Reason Codes That Matter for Dating Sites and How to Prevent

These four chargeback reason codes that are predominant in dating-site disputes. Friendly fraud drives the vast majority; true CNP fraud is now less pronounced.

| Code | What Cardholders Claim | Quick Prevention Mechanism |

|---|---|---|

| Visa 10.4 / MC 4837 Fraud – Card-Absent Environment | “Not me / my ex did it” | 3DS 2.0 + device fingerprinting (Sift, Forter) + velocity caps on new cards. Use Chargeflow Alerts to auto block repeat abusers by hashed email/phone. |

| Visa 13.1 / MC 4853 Services Not Provided | “Zero matches, no value” | Instant post-signup SMS/WhatsApp: “You’re live – here are your first 5 likes.” Auto-store IP, login, and message activity. Offer “pause subscription” instead of full cancellation. |

| Visa 13.3 / MC 4859 Not as Described | “Fake profiles / bots everywhere” | Dynamic checkout disclaimer: “X% of users in your area verified.” Screenshot TOS + verification badge at signup. Use Chargeflow Prevent to run periodic AI fake-profile sweeps to ferret out digital shoplifters. |

| Visa 13.2 / MC 4840 Canceled Recurring Transaction | “Forgot to cancel / never agreed” | 3-day pre-bill reminder (“$49.99 bill in 72h”). Add one-click cancel in every email footer. Auto-refund any request in the first 24h (cool-off period). |

Why Legacy Chargeback Prevention Fails Dating Sites

Online dating site chargebacks are predictable outcomes of engagement and billing patterns. Legacy strategies and tools for chargeback prevention fail dating sites because they treat chargebacks as exceptions. In more specific terms, they are:

- They’re not designed for the subscription economy: Most legacy chargeback tools are built for one-time purchases: stolen-card detection, velocity checks, IP flags, AVS/CVV verification. Dating platforms face a different challenge. Most disputes aren’t traditional fraud but first-party/friendly fraud or subscription-based disputes. They are structural byproducts of the business model itself.

- Rule-based filters can’t solve design problems: Static fraud checks (AVS/CVV/Velocity, etc.) are effective at detecting obvious card-not-present or stolen card fraud at checkout. But they generally fail to detect friendly fraud or subscription-based disputes that arise months later, after users successfully log in for months, engage with the platform, then dispute the charge.

- Manual representment doesn’t scale: Gathering logs, screenshots, and drafting rebuttals manually is old school and expensive. Dating platforms with high dispute occurrences cannot manually represent cases cost-effectively. Without automated evidence collection, industry representment win rates for dating platforms remain around abysmally low, meaning the majority of recoverable revenue is lost.

- 3D Secure and PCI compliance aren’t enough: As intimated earlier, authentication tools and PCI adherence prevent stolen-card fraud but do not address friendly fraud, forgotten or unrecognized renewals, or disputes triggered by ambiguous billing descriptors.

- Customer service mitigation arrives too late: By the time a user contacts support, they have often already filed a dispute. Retroactive refunds do not reverse chargebacks. It rather causes double chargeback, with your chargeback ratio taking a nosedive. It also does not reverse transaction value is lost, fees are incurred.

Effective solutions must predict disputes proactively, prevent disputes before they happen, and automate evidence collection and dispute filing for those that slip through, rather than relying on reactive, manual interventions.

How AI Drastically Changes Dating Site Chargeback Management

The challenge is not just detection. It’s contextualizing behavioral risk and automating the winning defenses at scale. Here's how AI is drastically changing dating site chargeback management:

1. Predictive Risk Contextualization

AI shifts the focus from simple fraud detection to behavioral foresight. AI-based chargeback solutions synthesize hundreds of non-linear user signals (engagement decay, payment method volatility, and login inertia) to generate a contextual risk score. This foresight allows intervention before a high-risk user gets to the renewal date.

2. High-Leverage Cohort Identification

Automated chargeback management pinpoints the behavioral segments draining your highest-margin revenue. AI leverages historical data to reveal the subtle cohort patterns, such as promotional sign-ups or rapid usage drop-offs, that exhibit 3-5x higher dispute propensity. This allows for highly targeted retention and pricing strategy adjustments.

3. Smart Dispute Prevention

Proactive intervention maximizes revenue retention by eliminating chargeback events. Using chargeback alerts, AI-based systems drive smart pre-dispute action. You can customize your dispute threshold to eliminate all preventable cases before they happen, with 90% success rate. Another exciting utility value is helping merchants gain useful insights for future chargeback prevention, such as uncovering possible chargeback vectors you might overlook.

3. Scalable, Optimized Representment

Evidence compilation and submission are enhanced for outcome, not just speed. AI instantaneously compiles a complete forensic package (logs, T&Cs, device IDs), and critically, customizes the rebuttal narrative and evidence sequence based on the specific reason code and the issuing bank's known acceptance criteria, elevating win rates to a sustainable 70-90% range.

4. Autonomous Model Evolution

The defense system self-optimizes, eliminating the vulnerability of static defenses. Unlike rules that become pointless over time, the machine learning system continuously ingests and adapts to real-time dispute outcomes. This ensures the predictive models and representment strategies remain effective against evolving fraud tactics without requiring human maintenance.

The Chargeflow Advantage for Online Dating Sites: A Case Study of Fantics

Fanatics Live is a leading sports collectibles marketplace that connects thousands of collectors and sellers through live card breaks and a thriving marketplace. Similar to a dating app, sports collectibles is a high-risk vertical with unusual chargeback risks. And so when Fantics faced rapid growth, it triggered a surge in fraud and chargebacks that threatened seller trust and drained team resources.

Key challenges included:

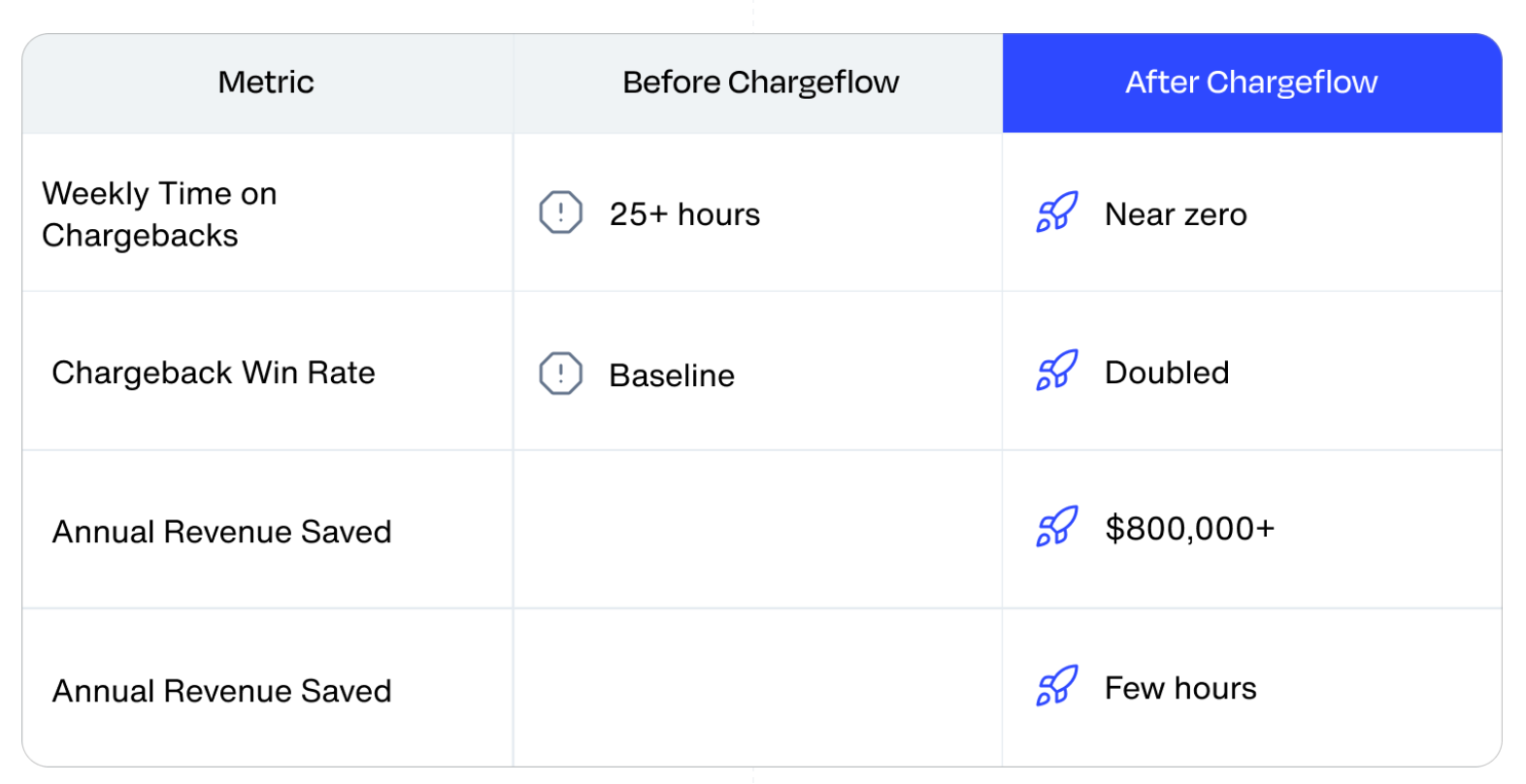

- Time drain: Over 25 hours per week spent manually handling chargebacks.

- Operational strain: Limited bandwidth for proactive fraud prevention and team growth.

- Revenue loss: Fraudulent disputes directly affected both Fantatics’ bottom line.

- Seller payouts at risk: Chargebacks were draining money from real sellers, damaging trust. Shielding them from fraud became a top priority.

- Reputation risk: Repeated disputes eroded seller confidence in the platform.

Solution

After evaluating potential partners, Fanatics chose Chargeflow for its expertise, speed of deployment, and clear alignment with the company’s operational needs. Chargeflow’s strong reputation and proven track record in chargeback automation gave Fanatics confidence that it was partnering with a trusted, industry-leading solution.

Key benefits included:

- 25+ hours saved weekly

- Over $800,000 in revenue was preserved in the first year

- Chargeback win rate doubled

- Improved data visibility for identifying and removing bad actors

- Increased team bandwidth for proactive initiatives

Results

Recovered revenue, stronger trust, and a scalable future:

Final Thoughts on Dating Site Chargeback

The chargeback profile for dating platforms is not a fraud problem. It is a systemic leakage driven by behavioral economics and friendly fraud.

Legacy tools cannot address this because they only detect exceptions at checkout; they are blind to the structural vulnerabilities inherent in the subscription relationships. Consequently, your operational losses are not just the disputed revenue. They are the compound cost of manual failure, escalating chargeback fees, and the constant threat to your merchant account health.

AI-powered dispute automation is no longer a marginal efficiency gain. It is the mandatory firewall against this unique threat model. It shifts the strategy from losing 70% of manual disputes to proactively preventing charges and winning 70-90% of those that remain.

The dating market is growing, and profitable. But margin compression from avoidable dating site chargebacks is a silent killer. If your chargeback rate is currently above 0.65%, you are already operating under processor surveillance.

The decision is simple: Continue funding the consumer behavior that exploits your business model, or implement a scalable, automated defense that secures your revenue and guarantees your merchant viability.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)