%201.svg)

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

Here is the difference between the four terms merchants and shoppers often mix up.

- Dispute: a customer’s formal complaint about a charge, filed with their bank; the first step, not a resolution

- Chargeback: a forced payment reversal the bank imposes on the merchant if it sides with the customer

- Refund: a voluntary reversal the merchant initiates directly with the customer, no bank and no fee involved

- Representment: the merchant’s evidence-based rebuttal to a chargeback, submitted to try to win the funds back

The eCommerce landscape has shifted dramatically over the last five years. AI, tariffs, inflation, tightening financial conditions...you name it. Things aren't what they used to be.

For merchants, managing financial transactions has become a growing battleground. Economic pressures fuel a new surge in chargebacks, disputes, and refunds. Understanding these concepts and how to protect your business is more consequential today than ever.

This guide will break down the chargeback vs dispute vs refund vs representment confusion and explore current trends shaping payment dispute management. You’ll see how Chargeflow's tools can strengthen your friendly fraud prevention.

Chargeback vs Disputes vs Refund vs Representment

If you're new to the eCommerce business, the terms can be overwhelming. Like most, you find the challenges of digital payments quite mind-numbing. Deciphering the jargon alone seems like full-time work. It's easy to feel lost in the complexity.

- What does it mean to dispute a transaction?

- Does dispute mean refund?

- What is a chargeback?

- What is chargeback representment?

- Is a chargeback the same as a refund?

- What is the difference between a chargeback and a dispute?

Don’t fret…we’re here to answer all the questions. Let’s take the chargeback prevention and eCommerce dispute management concepts one at a time:

What Does It Mean to Dispute a Transaction?

To dispute a transaction means a buyer challenges a bill on their credit or debit card, ideally because they believe the transaction is incorrect, unauthorized, or unsatisfactory.

In other words, payment disputes are customer grievances about a specific transaction. They involve the customer contacting their bank or card issuer to report the issue and seek remediation.

Customer disputes precede chargebacks. A dispute is essentially the first step in the chargeback process. If you don’t have a friendly fraud solution like Chargeflow Alert to intercept the impending chargeback at this stage, the outcome will be a payment reversal by the institution.

Does Dispute Mean Refund?

The answer is no. A dispute does not automatically equate to a refund. Think of a dispute as the preliminary stage of the case. It's the customer's first step in contesting the transaction. A refund can be an eventual outcome of a payment dispute if and when you, the merchant, voluntarily return the buyer's cash. For instance, if you've installed Chargeflow Alert, which gives you information about payment disputes immediately after the customer lodges a complaint, and you determine they have a valid case, you can refund the transaction.

That said, payment disputes often lead to chargebacks. That happens when you have taken no action to mediate the case at that initial stage.

Even though people frequently use “chargeback” and “dispute” interchangeably when talking about payment disputes, they don’t quite mean the same thing. Some even use "chargeback dispute" to refer to the entire process. Others call it chargeback. The meaning of chargeback will help you see where both parties go wrong.

What is a Chargeback?

A chargeback is when a cardholder disputes a credit card transaction and requests payment reversal from their bank. As noted earlier, chargebacks are often the ultimate penalty of payment disputes, and they are backed by Federal law. The card issuer or financial institution is required to reverse disputed payments after proper due diligence.

But that’s only a “paper promise,” not how chargebacks are processed in real time. Industry data, and even statements from major payment processors, indicate that merchants are often guilty by default when cardholders file chargebacks. This leads to chargeback abuse, also known as friendly fraud: buyers use chargebacks to defraud merchants.

“While common fraud narratives focus on stolen accounts or identity theft, in reality, a significant portion of fraud cases are chargeback abuse. Up to 75% of chargebacks stem from first-party misuse or friendly fraud.” – Visa

So are merchants supposed to stomach all these policy abuse and deductions? No. Card networks have established a formal channel for merchants to contest false chargebacks. That brings us to the next point:

What is Chargeback Representment?

Chargeback representment is merchants' rebuttal, a process for challenging customer claims with hard evidence.

The concept is similar to a civil court case. The judge here is the card issuer or customer's bank. They're most likely to rule against you. So your job is to "re-present" the transaction, convincingly demonstrating why the customer's claim that the transaction went wrong or never should've happened is meritless.

So first, you gather proof to demonstrate reasonable doubt. Next, you craft a concise rebuttal letter. And then you submit the documentation to your acquirer within the stipulated deadline. Your acquirer will then forward your package to the issuer for evaluation, and ultimate verdict.

"Over 80% of consumers report that merchants fail to respond to their chargeback claims. Merchants often relax fraud filters in slow markets to avoid turning away legitimate customers, inadvertently increasing fraud exposure. Many smaller merchants lack the resources to handle the complexities of cross-border or tariff-related chargebacks." – Ariel Chen, Chargeflow co-founder and CEO

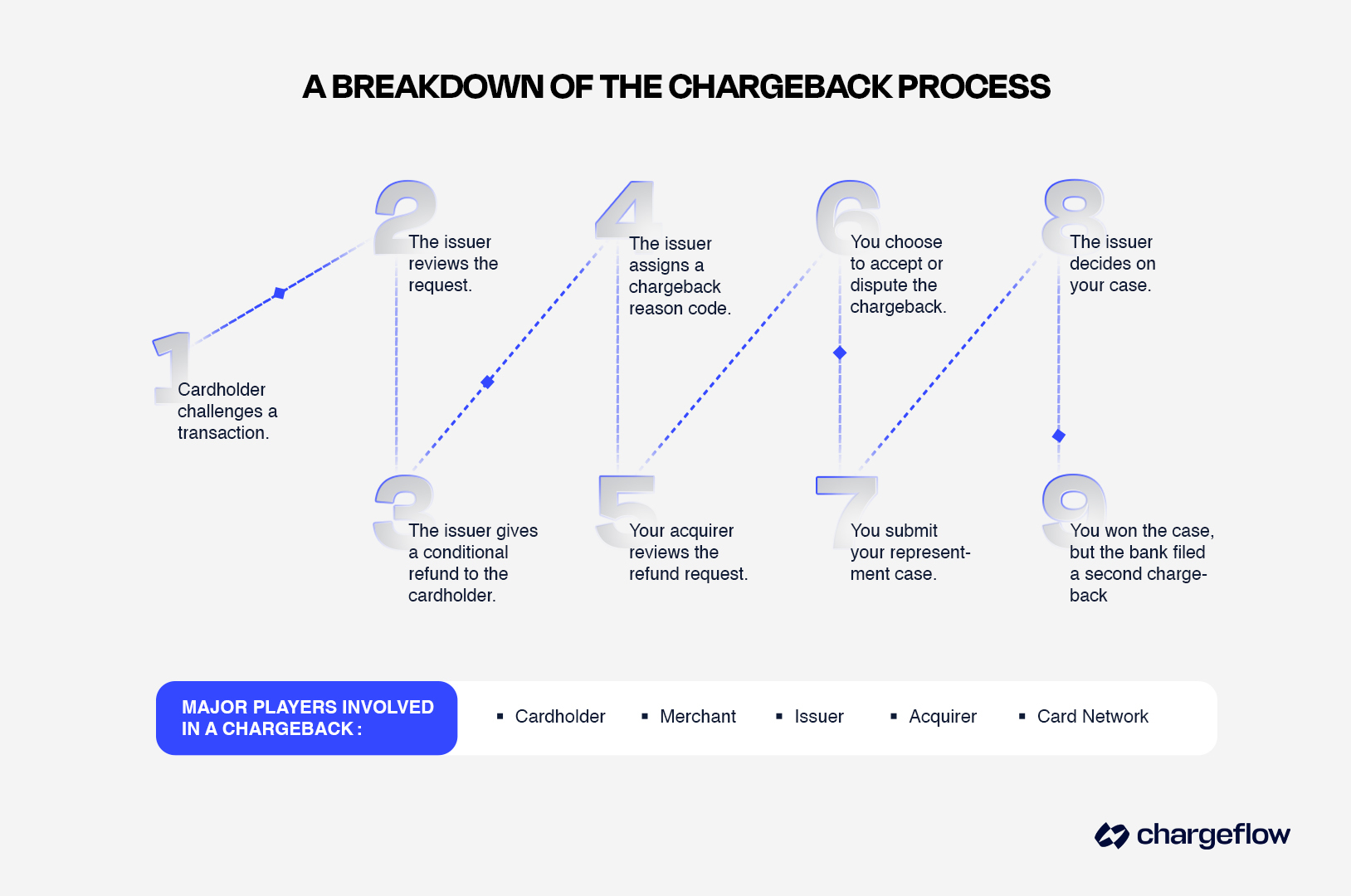

Understanding the Chargeback Representment Cycle

Chargeback representment is a strict, systematic procedure for fighting invalid chargebacks. Understanding the crucial steps you need to take for each stage of the long-winding representment cycle is essential. It helps you recover transaction revenue and optimize your systems effectively.

Here’s how the chargeback representment process works in three steps:

- Step 1: Chargeback Notification Reception

After you’ve received the chargeback notification from the customer’s credit card provider or bank, you have one of two choices:

- Accept the chargeback. You may choose to respond that you accept the dispute, which closes the loop. Not responding will equally mean accepting the dispute by default.

- Represent, disputing the customer’s claim. You must provide requisite documentation to counter the cardholder’s claim.

- Step 2: Merchant Dispute Response

A net positive chargeback response requires adhering to stringent rules on evidence submission, meeting card network response deadlines, following chargeback dispute procedures, and presenting case-specific proof to the card issuer while understanding how to challenge the case further if the outcome is unsatisfactory.

- Step 3: Card Issuer Chargeback Decision

Based on your compelling evidence, the credit card provider or bank will make a final decision on the dispute, and either reverse the transaction to the customer or keep the charge intact.

So there are three possible outcomes at this point:

- You won. The bank will reverse the chargeback and mark the case closed.

- The cardholder won. They will retain the transaction fund.

- You won but the cardholder or their bank presented new evidence.

Available records show that banks reject over two-thirds of chargeback cases, resulting in a second chargeback, called a “pre-arbitration” or “pre-arb” chargeback.

Merchants rarely win arbitration chargebacks, where banks, bound by rigid card network rules, typically make a judgment call to close the case. Pursuing debt collection through the legal system often becomes the last viable option when high-value transactions are involved. Fortunately, you can save yourself that dilemma with automated chargeback management.

"The chargeback-to-transaction ratio increased by 19% year-over-year in 2024, indicating more disputes per transaction, even as the average chargeback value grew from $165 in 2023 to $169 in 2024." – Industry data.

Payment Dispute vs Chargeback: What is the Difference Between a Chargeback and Dispute?

A chargeback happens when a cardholder goes over a merchant's head and asks their bank or card issuer to reverse a completed transaction. As indicated earlier, this pulls the funds back from the merchant to the cardholder.

Chargebacks are a consumer protection tool designed to correct unjust, fraudulent, or erroneous charges. Think of it as a financial rewind button triggered by the financial institution.

Conversely, a payment dispute marks the beginning of the process that can result in a chargeback. In legal terms, payment disputes are buyers' formal objections to specific charges on their payment cards. They signal trouble that could eventually grow into losses, penalties, and excessive processing fees.

Thus, the sharp distinction between chargebacks and disputes lies in how they're handled. Businesses can remediate customer disputes directly with the cardholder. Chargeback remediation involves third parties: banks, the card network, etc. It’s a tangled fight.

Besides that, chargebacks attract fees. They can also lead to complex issues like loss of payment processing rights, while disputes carry no such financial or operational penalties.

⛔Note: Banks place chargeback fees to cover their administrative cost of processing the dispute. Chargeback fees can vary depending on the cardholder's bank or the card network (more on that later).

Chargeback vs Refund: Is a Chargeback the Same as a Refund?

A chargeback is NOT the same as a refund, although both mechanisms return transaction funds to the customer.

In refunds, merchants voluntarily reverse a completed transaction and send money back to the customer's original payment method, usually to resolve a complaint. It's a friendly and direct process.

A chargeback, however, is a forced payment reversal. As indicated earlier, customers initiate chargebacks through their banks by disputing a completed transaction, often citing fraud, billing errors, or product/service dissatisfaction unresolved by the merchant.

Whereas refunds carry zero extra costs to sellers, chargebacks slap merchants with non-negotiable fees, penalties, and reputational damage. In that sense, refunds are mere handshake agreements while chargebacks are comparable to full-blown legal battles with banks and card brands wearing the black robe and wielding the gravel that determines your fate.

Another distinction you should keep in mind is timing. It differs between refunds and chargebacks. We covered that in this piece on payment reversal best practices. That said, let’s examine the differentiation between a dispute and chargeback.

Chargeback:

- Involves multiple parties including cardholder, merchant, issuer, Acquirer, and Card Network.

- Card networks set specific limits, after which additional fees/conditions apply.

- The merchant pays a non-negotiable chargeback fee.

- Could result in loss of processing rights.

- It takes at least 45 days to resolve.

Refund:

- Involves only the cardholder and merchant.

- There are no conditional limits applied.

- The merchant pays no additional fees.

- Merchant account privileges intact.

- Can be resolved immediately.

Chargeback vs Refund vs Reversal: Comparing the Mechanisms, Costs, and Outcomes of Payment Disputes

The main difference among chargebacks, refunds, and reversals lies in:

- Who initiated the action,

- The procedure involved, and

- The timing relative to the transaction.

These mechanisms, chargeback, refund, and authorization reversal, serve distinct purposes in resolving payment disputes. They have distinct implications for customers and merchants.

Chargeback:

- Mechanism: Initiated by customers and executed by banks and card issuers forcibly.

- Cost: $20-$100 fee per case, and also attracts additional penalties or higher processing rates for frequent disputes.

- Outcome: Customer receives money back; merchant loses sale the disputed amount, marketing cost, and ancillary expenses.

Refund:

- Mechanism: Initiated by the merchant on their own accord due to product return, order cancellation, or a goodwill gesture to address customer complaints.

- Cost: May involve a negligible processing fee – albeit much lower than chargeback fees – as the refund is treated as a new transaction.

- Outcome: Customer receives their money back; merchant incurs a loss of sale but voids additional penalties.

Authorization Reversal:

- Mechanism: Initiated by merchants or payment processors to cancel a transaction before it is processed or settled, preventing funds from leaving the payor's account. Typical reversal causes include errors or customer requests.

- Cost: marginal costs, often limited to standard processing fees, since the transaction is incomplete.

- Outcome: Money does not change hands; the transaction is voided.

How Can Merchants Prevent Disputes From Becoming Chargebacks?

Preventing disputes from becoming full-blown chargebacks is now a significant business sustainability strategy. Here’s what the latest data reveal:

- According to Chargeflow's State of Chargebacks 2024 report, friendly fraud accounted for approximately 80% of all chargeback losses for merchants, up from 70% in earlier years.

- First-party fraud costs the industry over $132 billion a year, according to Mastercard.

Want to limit disputes from turning into chargebacks? Start with your customer data. But not the usual way. Don’t waste time digging through mangled CRM like folks used to. Instead, uncover the psychology of chargebacks with specialized data analytics and friendly fraud solutions like Chargeflow Insights and Chargeflow Alerts.

To do that:

- Tract high-risk customers: Chargeflow Insights is a free add-on product when you install Chargeflow. It helps you analyze customer behavior, look for fraud patterns, and pinpoint potential issues.

- Understand the psychological triggers of chargeback: Uncovering why customers might file a chargeback is key to limiting loopholes.

- Predict and prevent: You can pre-emptively resolve chargebacks by tracking at-risk transactions and contacting customers. Or you can sit back and gather evidence way before the notification hits your inbox.

These data analytics tools help you intuit customer behaviors at every turn. So instead of responding blindly to strings the cardholder and their bank pulled, you can confidently resolve chargebacks on your terms.

“Card-not-present fraud is driving sustained demand for chargeback and fraud prevention tools. Consumers increasingly prefer chargebacks over direct merchant refunds, with 84% finding chargebacks simpler to process.” – Ariel Chen, Chargeflow co-founder and CEO.

How to Improve Your Odds of Winning a Chargeback Dispute

Every good material on eCommerce dispute management has mostly the same laundry list of best practices:

- Gather and submit every piece of evidence that supports your case.

- Don’t run out of time before you send your response and rebuttal.

- Provide clear and concise facts to the issuer for a better understanding of the situation.

- Be prepared to provide additional evidence or documentation if requested.

- Track all chargeback disputes and their outcomes.

- Stay updated on the latest chargeback policies and regulations, as they may change frequently.

This is a valuable checklist, assuming you have the time, specialized knowledge, and resources to fight each customer dispute profitably. But they’re not enough. Not even close.

Look at these facts:

- Chargeback reason codes are rarely a reliable indicator of chargeback cause.

- Card brands prioritize the cardholder, making it much easier for them to commit friendly fraud intentionally.

- Merchants are often pre-judged guilty of the crime before you send your rebuttal letter.

- About eight out of ten chargeback cases are friendly fraud cases.

- Friendly fraud takes away an estimated 28% of all eCommerce revenue today.

- 40% of customers who commit friendly fraud repeat the act in 60 days.

How can you possibly rely on that rubric when fighting false chargebacks? It's a losing game. You can’t get commensurate value for money.

That is why savvy merchants are using Chargeflow’s automated systems to confirm order details with customers, monitor customers' accounts for irregularities, and track down and resolve disputes without lifting a finger.

How Chargeflow Automates Chargeback Management

Chargeflow automates chargeback management by monitoring customer activity in real-time and automatically disputing cases with proven net positive outcomes.

Using big data and direct integrations, our proprietary tools, ChargeScore and ChargeResponse, generate custom-tailored, AI-driven evidence to combat friendly fraud and recover revenue. With over $130,000,000 chargeback revenue recovered, Chargeflow has boosted the industry-standard 12% recovery rate to 75% or higher. Some clients even achieve up to 85% win rates.

Our success-based pricing, no hidden fees, and 4x ROI guarantee ensure risk-free commitment. Minimize your workload, prevent 90% of chargebacks, and let your team focus on growth. Chargeflow is trusted by over 20,000 merchants, delivering financial resilience and real-time insights.

FAQs About Chargebacks, Disputes, Refunds, and Representment

Who loses money in a chargeback?

The merchant does. When a bank sides with the cardholder, it reverses the payment out of the merchant’s account and adds a chargeback fee on top, typically $20 to $100 per case. The cardholder keeps the funds and, in most cases, the product or service as well.

What are valid reasons for a chargeback?

Valid reasons include unauthorized or fraudulent transactions, billing errors like duplicate charges, and merchandise or services that were never delivered as promised. A chargeback filed over buyer’s remorse or after using a product as intended is not a valid reason, and falls under friendly fraud instead.

What are the downsides of chargebacks for merchants?

Beyond losing the sale, merchants pay a non-negotiable chargeback fee, can face higher processing rates as their chargeback ratio climbs, and risk losing payment processing rights at high volumes. Resolution also takes significantly longer than a refund, often 45 days or more.

Are chargebacks usually successful for cardholders?

Yes, in most cases. Banks reject roughly two-thirds of merchant representment attempts on the first try, which means the cardholder keeps the funds by default unless the merchant successfully disputes it. That imbalance is part of why friendly fraud makes up such a large share of total chargeback volume.

What does it mean when a chargeback is represented?

It means the merchant has formally disputed the chargeback by submitting evidence, such as delivery confirmation or proof of authorization, to the card issuer to argue the charge was legitimate. The issuer then reviews that evidence and either reverses the chargeback or upholds it.

What are the three types of chargebacks?

Chargebacks generally fall into three categories: true fraud, an unauthorized transaction on a stolen or compromised card; merchant error, such as billing mistakes or undelivered goods; and friendly fraud, where a legitimate customer disputes a valid charge, often over buyer’s remorse.

Why do merchants dislike chargebacks?

Chargebacks cost more than the disputed amount: merchants also lose the product, shipping costs, and marketing spend, then get hit with a fee on top. Unlike a refund, the process also runs through the bank and card network, taking weeks longer to resolve.

Summing Up

Meeting card network demands, and truly understanding chargeback dispute requirements, is crucial for safeguarding your business interests. Mastering chargeback is a strategic advantage.

We've explored these concepts thoroughly. We’ve shared essential insights and strategies for effective dispute management in this article. By understanding chargebacks, disputes, refunds, and representment, you can protect your revenue in these periods of economic downturn.

For merchants seeking to enhance their approach to these issues, exploring solutions like Chargeflow can make a real difference. Interested in elevating your chargeback management and safeguarding your business's financial health? Discover more about how Chargeflow can empower your operations.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)

.webp)

.webp)

.webp)