%201.svg)

Klarna Chargeback Guide: Process, Fees and Defense Best Practices

Estornos?

Não são mais problema seu.

Recupere 4 vezes mais estornos e evite até 90% dos estornos recebidos, com o apoio da IA e de uma rede global de 20.000 comerciantes.

Os estornos da Klarna seguem as regras da própria Klarna, e não as da Visa ou da Mastercard. No entanto, uma única transação paga com cartão pode seguir os dois caminhos simultaneamente, sem garantia de que a resolução de um encerre o outro. A Proteção ao Comerciante oferece ampla cobertura para “Mercadorias não recebidas” apenas quando o envio é feito para o endereço aprovado, acompanhado de um comprovante de entrega válido. Ela oferece proteção limitada para disputas relacionadas à qualidade, “Não conforme a descrição” e devoluções. Espere taxas de disputa de cerca de US$ 15 (que dobram se sua taxa exceder cerca de 1,5%). O sucesso exige disciplina rigorosa no atendimento, respostas rápidas e evidências organizadas. Categorias de alto risco enfrentam um escrutínio mais rigoroso. Quando bem feita, a Klarna impulsiona o crescimento; quando mal feita, ela corrói as margens por meio de disputas e taxas.

A Klarna processou cerca de 127,9 bilhões em 2025, tornando-se uma opção de pagamento global essencial para os comerciantes.

Mas, à medida que a Klarna crescia, o número de estornos também aumentava. Os clientes apresentam essas contestações diretamente à Klarna, e elas são tratadas fora das redes de cartões. A Klarna atua tanto como credora quanto como árbitra nas contestações.

Se um comprador alegar falta de entrega, problemas com o produto ou uso não autorizado, você, o comerciante, corre o risco de perder o valor total do pedido e de incorrer em uma taxa de contestação de cerca de US$ 15 por caso. Caso o volume de contestações exceda os limites estabelecidos pela Klarna, você poderá ter que arcar com taxas ainda mais elevadas. Os riscos geralmente variam de acordo com o produto, com as opções de curto prazo “Pague em 4” apresentando maior vulnerabilidade à fraude de estorno em comparação com o financiamento de longo prazo, onde a Klarna assume mais risco de crédito.

O Programa de Proteção ao Comerciante da Klarna pode cobrir disputas elegíveis que apresentem provas sólidas de entrega. No entanto, os requisitos rigorosos e as exclusões por categoria, especialmente em setores de maior risco, fazem com que muitos comerciantes ainda tenham de arcar com as perdas. Este guia apresenta o manual de estratégias para estornos da Klarna. Você aprenderá como funcionam os estornos da Klarna, quais provas são determinantes e como estruturar suas operações para que a Klarna se torne um canal de crescimento lucrativo, e não um passivo oculto.

O que é um estorno da Klarna e em que ele difere dos estornos tradicionais de cartão?

Um estorno da Klarna é uma reversão formal de pagamento iniciada quando um cliente contesta uma transação financiada pela Klarna. Ao contrário dos estornos tradicionais de cartão, as contestações da Klarna seguem os próprios códigos de motivo, prazos e regras internas da Klarna, em vez dos procedimentos da Visa ou da Mastercard.

A Klarna gerencia esses litígios por meio de seu próprio ciclo de vida: após o envio das provas, a Klarna analisa a documentação e emite uma decisão preliminar. É possível recorrer da decisão, mas, uma vez que a equipe de arbitragem encerre o caso, a decisão é definitiva. Não há revisões externas nem canais de escalonamento.

Se a decisão for favorável ao cliente, a Klarna estorna a transação por meio do PSP (Stripe, Adyen etc.) e debita o valor contestado e quaisquer taxas aplicáveis. As taxas de estorno da Klarna são cobradas independentemente do resultado da contestação.

Pode haver uma contestação específica para transações pagas com cartão, e o procedimento difere das disputas habituais da Klarna.

Estornos de cartão na Klarna

A Klarna aceita Visa e Mastercard como formas de pagamento para os planos “Pague em 4”, “Pague em 30” e “Cartão Único”. Quando um cliente efetua uma compra dessa forma, ele mantém os direitos previstos pela rede do cartão. A política de proteção ao comprador da Klarna afirma explicitamente que não limita quaisquer direitos que o titular do cartão possa ter, nos termos da legislação aplicável ou das regras da rede, de contestar uma transação junto ao emissor do cartão.

Na integração padrão, qualquer estorno da rede de cartões é registrado contra a Klarna como comerciante registrado, e não diretamente contra o próprio MID do comerciante ou contra a adquirente. De forma semelhante à metodologia de estorno da Affirm, a Klarna analisa o caso e decide se absorve o prejuízo ou se o repassa ao comerciante (resultado mais provável). Se uma contestação da Klarna já estiver em andamento, a Klarna normalmente a cancela ao receber o estorno do cartão, mas isso não protege necessariamente o comerciante de um débito subsequente.

Na prática, a mesma transação pode gerar exposição em várias vertentes, sujeitas a regras, prazos de resposta e tomadores de decisão diferentes.

Como funciona o processo de contestação e estorno da Klarna

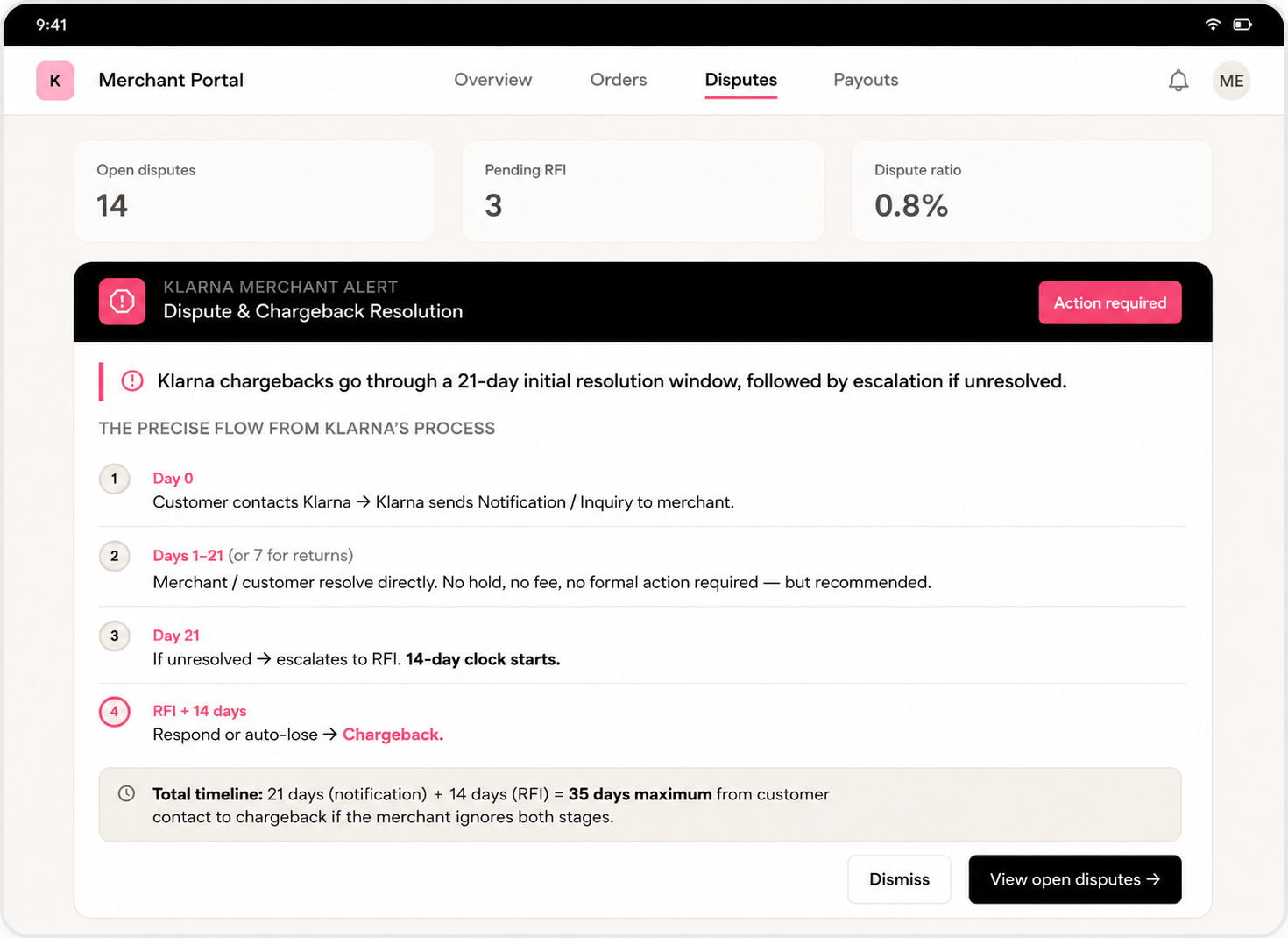

Quando um cliente apresenta uma reclamação sobre uma transação financiada pela Klarna, ela passa por um processo estruturado de escalonamento. Geralmente, as disputas começam com um prazo inicial de 21 dias para resolução (muitas vezes mais curto no caso de devoluções). Se não forem resolvidas, elas são encaminhadas para o próximo nível.

Os prazos variam de acordo com o código de motivo e com o seu contrato de comerciante específico. Verifique sempre o Portal do Parceiro ou a documentação de integração para saber os prazos exatos.

O caminho de escalada em três etapas

Etapa 1: Consulta (Notificação de contestação)

Este é um primeiro passo informal. A Klarna te avisa e te dá a oportunidade de resolver a situação diretamente. Respostas rápidas geralmente evitam que o caso seja encaminhado para instâncias superiores. A falta de resposta é considerada como aceitação, o que leva ao encaminhamento automático do caso.

Etapa 2: Solicitação de Informações (RFI)

Se a questão não for resolvida, a Klarna encaminha o caso para uma instância superior e investiga ativamente. É necessário apresentar provas documentais. Os comerciantes têm normalmente de 7 a 14 dias (dependendo do código de motivo; por exemplo, geralmente 7 dias para compras não autorizadas). O não cumprimento do prazo geralmente resulta em uma decisão automática a favor do cliente.

Etapa 3: Estorno

Este é o ponto de reversão formal. A Klarna debita o valor contestado (ou retém-no na liquidação). Os prazos para contestação variam normalmente entre 7 e 21 dias, dependendo do motivo e da jurisdição. Em geral, não são aceitas provas apresentadas fora do prazo.

🔥Conclusão principal: Durante o mecanismo de 21 dias, o silêncio do comerciante é considerado uma renúncia. A ausência de resposta a uma RFI geralmente resulta em uma decisão automática contra você ao completar 21 dias. Respostas parciais ou incompletas ainda podem resultar em prejuízo se a Klarna não conseguir validar sua posição. O prazo de 21 dias começa a contar a partir da data em que a RFI é formalmente emitida, e não a partir da data em que o comerciante abre a notificação.

Motivos de contestação da Klarna e o que a Klarna espera dos comerciantes

A Klarna utiliza códigos padronizados de motivos de estorno para reclamações de clientes em seus produtos “Compre Agora, Pague Depois” e de pagamento. Uma defesa bem-sucedida depende do envio de provas claras, específicas e bem organizadas por meio do Portal do Comerciante da Klarna, do aplicativo Disputes ou da API. A tabela abaixo explica em detalhes:

Motivos de contestação da Klarna e requisitos de defesa

| Código | Reclamação do comprador | Principais argumentos de defesa do comerciante e provas necessárias |

|---|---|---|

| mercadorias_não_recebidas | Os produtos ou serviços nunca chegaram (total ou parcialmente). |

Obrigatório: Comprovante de entrega (POD) válido que atenda aos padrões do Programa de Proteção ao Comerciante — incluindo o número de rastreamento, a data de entrega, o nome do destinatário e o endereço de entrega, que deve corresponder ao endereço aprovado pela Klarna.

Os links de rastreamento, por si só, geralmente não são suficientes. Adicione a nota fiscal, a confirmação de peso ou o relatório da transportadora, sempre que possível. |

| produtos com defeito | Artigos com defeito, danificados ou que não correspondem à descrição. |

Avaliação detalhada (reclamação válida/inválida) acompanhada de provas: fotos do produto, capturas de tela com descrições precisas, histórico de comunicação com o cliente e comprovante de qualquer solução oferecida (reembolso, substituição ou reparo).

O comprovante de entrega (POD) por si só raramente é suficiente. |

| devolução_reembolso_não_recebido | Reembolso não processado ou atrasado após a devolução. |

Comprovante da emissão do reembolso (data, valor, forma de pagamento) ou motivo claro da recusa, acompanhado de documentação comprovativa (por exemplo, fotos da inspeção mostrando a caixa vazia, o item danificado ou a violação da política).

Inclua comprovante do envio de devolução. |

| compra não autorizada | Compra realizada sem autorização (fraude). |

A evidência mais sólida prevalece: POD, juntamente com o histórico de contato com o cliente, registros de IP/e-mail/acesso, dados de autenticação 3DS e registros de prevenção de fraudes.

Esses casos têm os prazos de resposta mais curtos. |

| já_pago / fatura_incorreta | Cobrança duplicada ou valor incorreto. | Fatura precisa, detalhamento dos preços, confirmação do pedido e comprovante de quaisquer ajustes ou cancelamentos. |

As reclamações relacionadas a “produtos não recebidos” e a devoluções/reembolsos são predominantes em lojas de grande volume. Esses são os casos mais difíceis de resolver sem uma documentação rigorosa e oportuna. A abordagem da Klarna, que prioriza o comprador, exige que os comerciantes sejam proativos e altamente organizados.

Padrões de evidência e melhores práticas para estornos da Klarna

Requisitos gerais (aplicáveis a todos os litígios):

- As provas devem estar diretamente relacionadas à transação/pedido da Klarna em questão.

- Envie apenas em formato PDF (legível, completo; aplicam-se limites máximos de tamanho).

- Inclua uma explicação clara que aborde especificamente a reclamação do comprador.

- Forneça um cronograma conciso (pedido → envio → entrega/reembolso/devolução).

- Nomeie os arquivos de forma clara (por exemplo, POD_Pedido12345.pdf, Fotos_da_Inspeção.pdf).

- Destaque ou anote seções importantes em capturas de tela ou documentos.

Detalhes do POD (para mercadorias não recebidas): É necessário cumprir integralmente a Seção 1.1 ou 1.3 do MPP. Inclui detalhes da confirmação de entrega; provas adicionais (guia de remessa, peso, etc.) reforçam o caso. Dados de GPS ou fotos da transportadora servem apenas como apoio. Os comerciantes que automatizam a coleta de provas obtêm resultados significativos devido aos padrões de prova específicos da Klarna

Dicas para responder:

- Utilize os modelos de resposta oficiais da Klarna, quando disponíveis.

- Responda à reclamação específica: o envio de um POD para uma disputa relacionada a produtos com defeito, por exemplo, será rejeitado.

- Cumpra todos os prazos (as compras não autorizadas geralmente exigem uma resposta imediata).

Para criar pacotes de evidências convincentes, é necessário elaborar pacotes em PDF bem estruturados que contem uma história completa. Automatize sempre que possível: integre-se ao seu sistema OMS/Shopify/armazém para extrair instantaneamente números de rastreamento, registros, transcrições de chat e fotos.

Custo do estorno da Klarna: quando e quanto dinheiro você realmente perde

Com a Klarna, um “estorno” não significa apenas que o valor do pedido é descontado do seu pagamento. Você perde a receita, arca com os custos e, além disso, a Klarna ainda cobra uma taxa de contestação.

1. O custo visível: as taxas de contestação da Klarna

A Klarna cobra uma taxa fixa por contestação, e em muitos mercados há dois níveis: uma taxa padrão e uma taxa mais elevada para “contestações excessivas”, caso sua taxa de contestação se torne muito alta.

Os níveis típicos de taxas nos documentos da Klarna e dos PSP são os seguintes (os valores exatos podem variar de acordo com o contrato/PSP, mas esta é uma estimativa aproximada):

| Região | Taxa padrão (aproximada) | Taxa excessiva (aprox.) |

|---|---|---|

| UE | 15 EUR | 30 EUR |

| Reino Unido | 10 GBP | 20 GBP |

| EUA | 15 USD | 30 USD |

| Países Nórdicos (SEK/NOK/DKK) | 150 | 300 |

A Klarna utiliza um limite de taxa de contestação para determinar quando você passa da categoria padrão para a de contestação excessiva: por exemplo, mais de 1,5% de pedidos contestados durante 3 meses consecutivos e pelo menos 100 pedidos nesse MID podem acionar a faixa de taxa mais elevada.

Pontos importantes para os comerciantes:

- A taxa é cobrada por caso de contestação, e não por linha do pedido.

- A taxa não é reembolsável caso você perca.

- Esse valor é deduzido do seu pagamento juntamente com quaisquer valores de pedidos reembolsados.

2. Quando você realmente paga (e quando não paga)

Você não paga uma taxa à Klarna por cada reclamação de cliente. No entanto, assim que a Klarna transformar uma reclamação em uma contestação formal, será cobrada uma taxa fixa e não reembolsável por caso, mesmo que você vença.

Na prática:

- Se não houver contestação, não haverá cobrança de taxa. Se você resolver a questão diretamente com o cliente antes que a Klarna inicie um processo formal de contestação, não será cobrada nenhuma taxa de contestação.

- Contestação iniciada (você ganha). A Klarna retém o valor da transação e cobra uma taxa de contestação não reembolsável por caso. Se você ganhar, o valor contestado será devolvido a você, mas a taxa não será reembolsada.

- Contestação iniciada (você perde ou não responde). A Klarna reembolsa o cliente com o valor retido, e você já pagou a taxa de contestação além disso. Você perdeu efetivamente o valor do pedido, seus custos (produtos, frete, operações) e a taxa fixa.

Os agregadores e os PSPs geralmente repassam essa cobrança. Quando você perde, eles deduzem o valor da transação mais a taxa de contestação da Klarna do seu pagamento; quando você ganha, eles devolvem o valor da transação, mas a taxa continua sendo cobrada.

3. O nível da “disputa excessiva”: o assassino silencioso da margem

A taxa padrão já é pesada, mas o nível excessivo de contestação é o que, silenciosamente, destrói sua lucratividade se você deixar que as taxas de contestação subam.

Como funciona na prática:

- A Klarna monitora sua taxa de contestação (pedidos contestados / total de pedidos) por ID de comerciante.

- Se a sua taxa de contestação ficar acima de aproximadamente 1,5% por três meses consecutivos e você tiver pelo menos 100 pedidos, a Klarna poderá aplicar a faixa de taxa de contestação mais alta, considerada “excessiva”.

- Isso normalmente dobra a sua taxa por caso (por exemplo, de 15 para 30 euros), aumentando imediatamente o seu prejuízo em cada litígio futuro.

A lição: mesmo uma variação percentual “pequena” na taxa de contestação pode alterar significativamente o custo por pedido da Klarna assim que você ultrapassar o limite.

Programa de Proteção ao Comerciante da Klarna: O que ele cobre (e o que não cobre)

O Programa de Proteção ao Comerciante da Klarna foi criado para transferir a responsabilidade de volta para a Klarna em certos litígios, desde que você cumpra integralmente suas rigorosas condições. Ele é eficaz principalmente em casos de “produto não recebido” e em casos específicos de fraude, não constituindo uma proteção geral contra todos os litígios.

Requisitos básicos de elegibilidade

A Política de Proteção ao Comerciante da Klarna e os modelos de reclamação destacam especificamente que a proteção para “produtos ou serviços não recebidos” depende de critérios rigorosos de comprovação de entrega (POD).

A seguir, apresentamos alguns critérios específicos de elegibilidade exigidos por eles:

- A remessa deve ser processada de acordo com a política de envio e as regras do programa da Klarna (ou seja, utilizando uma transportadora reconhecida, garantindo um rastreamento adequado, etc.).

- Seu POD deve incluir, no mínimo:

- Nome da transportadora/empresa de entregas

- Número de rastreamento ou número da remessa

- Data de entrega confirmada

- Endereço de entrega indicado no comprovante de entrega

- Um documento comprovativo de entrega (confirmação da transportadora, recibo assinado, etc.).

- O endereço de entrega indicado no comprovante de entrega (POD) deve corresponder ao endereço de entrega aprovado pela Klarna no momento da finalização da compra ou da solicitação; as políticas de fraude e de envio da Klarna exigem explicitamente o uso do endereço aprovado pela Klarna.

- No caso de produtos intangíveis, a Klarna espera receber provas de prestação do serviço, como comprovantes de acesso, registros de data e hora, endereço de e-mail ou IP de destino e registros de uso, em vez de um comprovante físico de entrega.

O que está claramente excluído ou é de alto risco

A Klarna também fornece uma lista de tipos de negócios proibidos e restritos, incluindo certos setores de alto risco (conteúdo adulto, jogos de azar, alguns produtos de CBD, downloads digitais, dropshipping, certos produtos médicos/de saúde, etc.). As empresas que atuam nesses segmentos não podem usar a Klarna de forma alguma (proibido) ou só podem fazê-lo sob condições especiais (restrito).

Resumindo, se você estiver proibido, não poderá usar o Klarna de forma alguma, portanto, a Proteção ao Comerciante não se aplica. Se você estiver restrito, poderá usar o Klarna, mas sob um controle mais rigoroso de risco e conformidade. Se você for um comerciante comum autorizado a vender produtos físicos, a Proteção ao Comerciante e o procedimento de contestação descritos nos modelos do Klarna são as configurações padrão que você deve adotar.

É importante ressaltar que a Proteção ao Comerciante está intimamente ligada à forma como você envia e comprova o pedido, e não apenas ao fato de a Klarna ter aprovado inicialmente a transação.

Na prática, isso significa:

- O comércio eletrônico de produtos físicos não perecíveis que opera fora de segmentos restritos ou proibidos é o cenário que mais se alinha à Proteção ao Comerciante.

- Produtos digitais, bens de consumo de alto risco, conteúdo adulto e outras categorias restritas podem estar sujeitos a mais disputas, maior escrutínio e resultados negativos mais frequentes, mesmo que sejam entregues conforme prometido, pois a própria natureza dessas categorias altera a forma como a Klarna aplica suas regras de risco e conformidade.

Limites do Programa de Proteção ao Comerciante da Klarna

O Programa de Proteção ao Comerciante da Klarna cobre principalmente litígios tratados por meio do próprio sistema da Klarna. Mesmo quando você se qualifica para a proteção:

- A Proteção ao Comerciante não elimina todos os riscos a jusante no ecossistema de pagamentos.

- As disputaspor “Item não recebido” (mercadoria não recebida) são decididas principalmente com base na Comprovação de Entrega (POD) em comparação com a reclamação do cliente. Se você enviar a mercadoria para o endereço aprovado pela Klarna e sua Comprovação de Entrega (POD) atender aos requisitos da Klarna, a Proteção ao Comerciante foi criada para impedir que a Klarna debite o valor de sua conta.

- Disputas relacionadas a produtos que não correspondem à descrição, produtos com defeito, qualidade ou serviço: a proteção é muito mais limitada neste caso. A simples comprovação de entrega geralmente não é suficiente. A Klarna exige provas concretas, como descrições precisas do produto, fotos, histórico de comunicação com o cliente e comprovação de tentativas de resolução. Os comerciantes podem ter cumprido perfeitamente com o combinado e ainda assim perder essas disputas se a Klarna determinar que o produto não correspondia à descrição do anúncio ou apresentava defeito.

No que diz respeito aos pagamentos com cartão: os estornos de cartão passam primeiro pela Klarna. A Proteção ao Comerciante determina se a Klarna absorve o prejuízo ou o repassa a você.

🔥Em resumo, a Proteção ao Comerciante não se sobrepõe ao direito da Klarna de reter fundos por motivos de risco ou conformidade, nem de restringir contas em setores proibidos ou restritos.

Estratégias proativas para reduzir drasticamente as disputas com a Klarna

A Klarna espera que os comerciantes mantenham sua taxa de contestação abaixo de 1,5% dos pedidos registrados; portanto, a prevenção é tão importante quanto vencer os casos. Os melhores resultados são obtidos quando se começa por aperfeiçoar as operações e, em seguida, se recorre à tecnologia para lidar com os casos que ainda escapam.

Principais estratégias de prevenção

- Cuidados com os produtos e o processo de finalização da compra: use títulos precisos, descrições detalhadas e fotos de alta qualidade. Defina expectativas claras sobre prazos de entrega, custos de envio e devoluções na página de finalização da compra. Deixe bem claro que o cliente está comprando de você e pagando via Klarna.

- Regras de atendimento de pedidos: Envie sempre para o endereço aprovado pela Klarna. Utilize transportadoras com rastreamento que forneçam comprovantes de entrega confiáveis. E armazene todos os comprovantes de entrega, guias de remessa e registros de comunicação em um sistema de fácil acesso.

- O atendimento ao cliente como primeira linha de defesa: responda rapidamente às dúvidas dos clientes antes que elas sejam encaminhadas à Klarna. Ofereça soluções justas (reembolsos, substituições, crédito na loja) quando for o caso. E documente todas as interações.

- Controles contra fraudes e riscos: Implemente regras adicionais para pedidos de alto risco (primeiros pedidos de grande valor, endereços incomuns etc.). Considere o uso de ferramentas como o Chargeflow Prevent para sinalizar ou bloquear pedidos suspeitos da Klarna e fraudes cometidas por clientes de boa-fé. Você também pode usar alertas de estorno para evitar casos iminentes antes que cheguem ao fim do processo.

Dica operacional: integre seu OMS (por exemplo, o Shopify) com a Klarna para que os números de rastreamento, as notas de pedido e as mensagens dos clientes sejam importados automaticamente para as respostas a contestações. Pacotes de provas em PDF bem organizados e enviados dentro do prazo aumentam significativamente as taxas de sucesso.

Conclusão

A economia do BNPL veio para ficar. Por isso, a Klarna é uma das opções de checkout mais poderosas disponíveis atualmente. No entanto, ela recompensa os comerciantes bem preparados e, discretamente, penaliza aqueles que não compreendem os requisitos específicos relativos a estornos.

Portanto, trate cada pedido da Klarna com o mesmo rigor operacional que você aplicaria a transações de alto risco. Envie apenas para endereços aprovados, mantenha registros impecáveis, responda rapidamente às consultas e elabore pacotes de evidências claros como procedimento operacional padrão. Os comerciantes que automatizam a coleta de evidências e aplicam políticas rigorosas de atendimento mantêm, de forma consistente, relações mais saudáveis com a Klarna.

Quando bem utilizada, a Klarna se torna um poderoso motor de crescimento, sem atritos. Quando mal utilizada, ela corrói silenciosamente seus lucros por meio de contestações e taxas.

Comece analisando seu processo atual de processamento de pedidos da Klarna em relação aos requisitos de Proteção ao Comerciante descritos neste guia. Pequenas melhorias na qualidade das evidências e na rapidez de resposta costumam resultar em reduções significativas nas perdas. Em seguida, utilize o gerenciamento automatizado de estornos para identificar os casos que passam despercebidos.

Se você colocar em prática pelo menos metade das estratégias descritas aqui, estará à frente da maioria dos comerciantes que utilizam o Klarna atualmente. Desejo-lhe tudo de bom!

Estornos?

Não são mais problema seu.

Recupere 4 vezes mais estornos e evite até 90% dos estornos recebidos, com o apoio da IA e de uma rede global de 20.000 comerciantes.

.png)