%201.svg)

Stripe Chargebacks: Fees, Protection, and Policy Explained

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

Stripe chargebacks follow card network rules, not Stripe's rulebook, and the full cycle runs 2-3 months from filing to resolution. Merchants get a 7-21-day window to respond, and missing it means an automatic loss. Stripe monitors chargeback ratios closely and can suspend or terminate accounts before merchants ever breach card network thresholds. Since June 2025, Stripe's two-tier fee structure means a lost dispute costs $30 in fees alone. Stripe's built-in Smart Disputes automates evidence submission but lacks CRM integration, offers limited transparency, and only contests disputes it deems winnable, unlike in-built apps like Chargeflow.

Stripe chargebacks are a (card-network-enforced) consumer protection mechanism. They exist because fraud, merchant mistakes, and cardholder disputes are unavoidable realities within the payment ecosystem. Yet, chargebacks represent a real cost of accepting cards…one that merchants must actively manage to stay in good standing with the payment provider.

Stripe is highly protective of its acquiring relationships and platform-wide dispute ratios. They monitor merchant chargeback activity closely and enforce thresholds defined in the Services Agreement. A modest spike or upward trend in dispute can prompt a warning email, often while your rate remains well below the industry’s 0.75% benchmark.

Every fraud and dispute signal contributes to your monitoring ratios. This includes won, lost, withdrawn, partial disputes, and Early Fraud Warnings (EFWs). Visa, in particular, counts the same transaction twice if it triggers EFW and later becomes a formal dispute.

Stripe’s risk intelligence systems continuously analyze patterns and can flag deteriorating trends months in advance. If metrics continue to worsen, the Services Agreement authorizes a range of correction measures, including reserves, payout delays, suspension, termination, and blacklist.

In this guide, we’ll break down how Stripe evaluates and handles chargebacks, the mechanics that drive your account health, and practical steps you can take to keep Stripe chargebacks under control.

What Is a Stripe Chargeback?

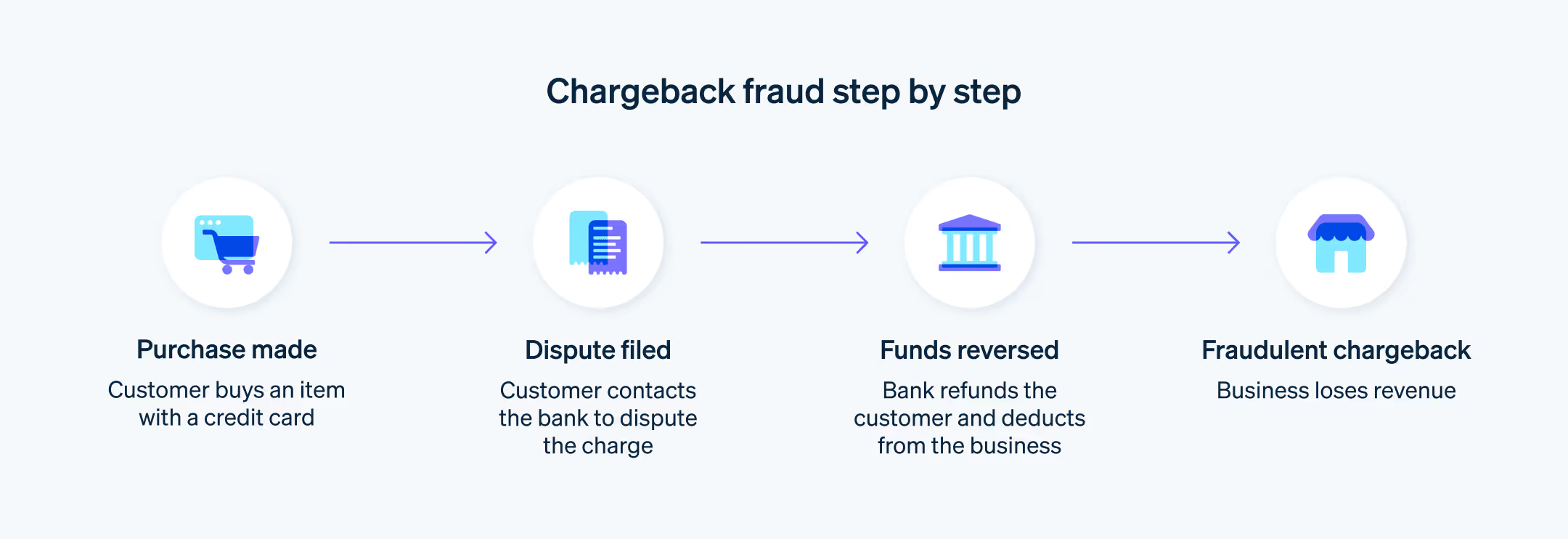

A Stripe chargeback is a payment reversal initiated when the cardholder disputes a transaction to their card issuer. It’s a type of consumer protection enforced by card brands.

Stripe chargebacks give cardholders recourse if they’re charged incorrectly or don’t receive products or services they paid for. Unlike refunds, which you control and issue voluntarily, chargebacks insert the issuing bank in the driver’s seat. You can fight it, but the initial payment reversal and incidental dispute fee happen automatically, irrespective of whether the claim is legitimate fraud, chargeback fraud, or buyer’s remorse.

How the Stripe Chargeback Process Works

Similar to all payment disputes, Stripe chargebacks follow a standardized lifecycle that is largely engineered by the card network and initiated by the cardholder’s issuing bank. Stripe is a neutral facilitator.

The full cycle spans 2-3 months (in many cases) from filing to final resolution, though your active involvement can shorten the chargeback timeline:

Stage 1: Cardholder Dispute Initiation (Pre-dispute or Direct dispute)

The cardholder contacts their bank to contest a charge. Reasons for cardholder disputes range from legitimate fraud to product delivery issues. But friendly fraud drives most cases, as our research has uncovered.

- The case may start as an inquiry or Early Fraud Warning (EFW/TC40). This soft signal often escalates if ignored.

- If unresolved (e.g., no response), the issuer escalates to a formal dispute.

Step 2: Issuer Files the Dispute

Once the card issuer creates a formal dispute on the card network, an instant payment reversal takes place.

- The network immediately deducts the full disputed amount and applicable fees from Stripe.

- Stripe then instantly debits your connected balance for the disputed amount and Stripe’s Dispute Received Fee, as highlighted above.

- If your balance is insufficient, a negative balance is created (which may trigger holds or recovery attempts).

This process happens in real time with zero merchant input needed.

Step 3: Stripe Notification and Merchant Window Opens

Stripe will notify you immediately through:

- Dashboard (Disputes tab)

- Webhooks (charge.dispute.created)

- API events

You get: the dispute reason code, cardholder claim details, and evidence due date.

The response window for most cases is 7 days (we’ll discuss timelines further in the subsequent section. However, the exact deadline will be stamped in your Dashboard, and missing that equals automatic loss. The issuer wins by default.

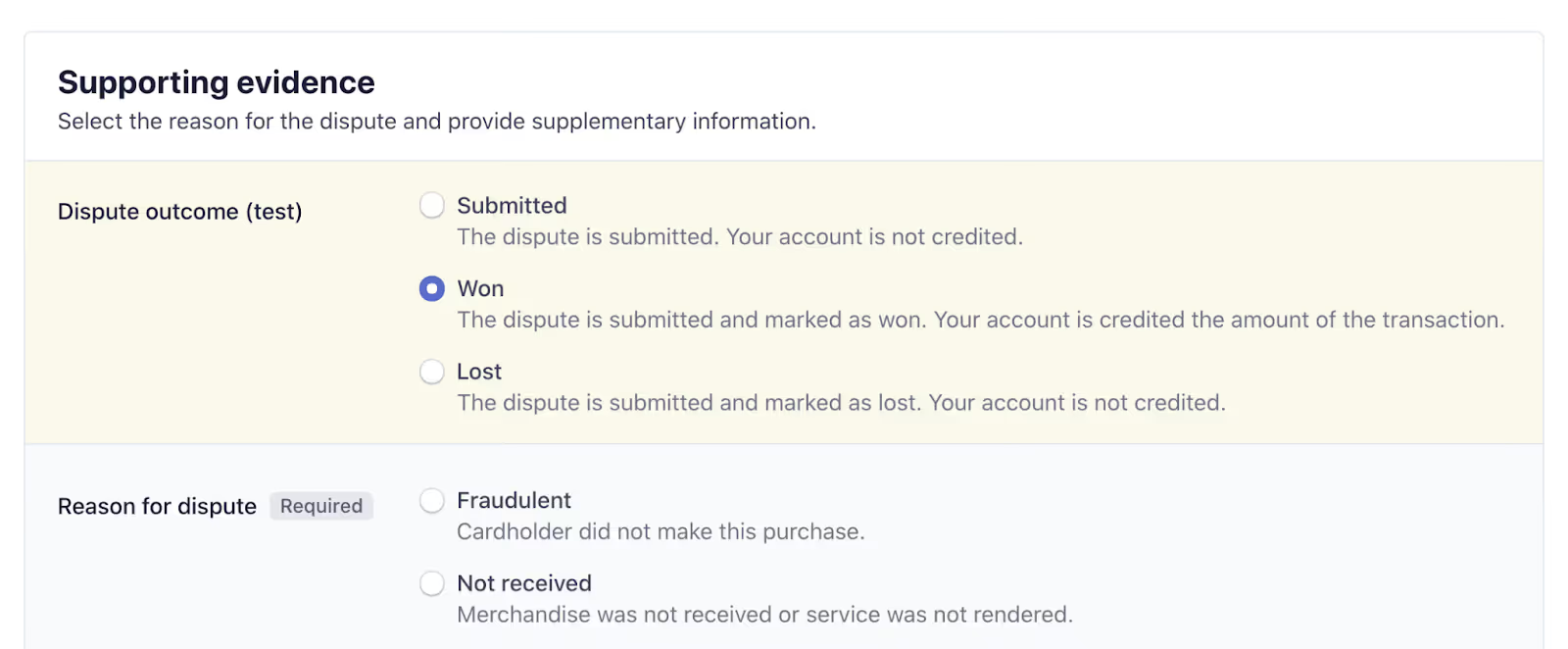

Stage 4: Merchant Response Phase

This is the only stage you can control. You decide whether to:

- Accept the dispute by doing nothing or explicitly accepting, which makes the reversal permanent and closes the case.

- Counter (challenge) the dispute by submitting evidence through the Dashboard or API.

Your evidence is one-shot. There are no rooms for editing your documentation after submission.

Stage 5: Issuer Review and Decision

At this black box phase, Stripe forwards your evidence to the issuer through the network. General outcomes after issuer review are:

- You won: Disputed amount and countered fee (if applicable) returned to your balance.

- You lost: Funds and fees stay gone; the decision remains final if you do not appeal.

In some cases, the issuer can file a second chargeback after you’ve won, prolonging the process. You can always find the status update through charge.dispute.closed webhook and your Dashboard.

Stripe Chargeback Time Limits and Deadlines

Stripe does not set arbitrary chargeback time limits. The dispute deadlines pass through the card networks’ rules. Historically, merchants are given a short response window to ensure timely submission.

Here’s the breakdown of key Stripe dispute time limits:

1) Cardholder Filing Window

Card networks allow cardholders to initiate a dispute within 120 days of the original transaction date, or the expected delivery date for physical goods (whichever is later).

In some cases, especially subscription chargebacks involving goods or services not received or provided far in the future, Visa allows cardholders to file disputes up to 120 days after the expected delivery or performance date. That is only possible if the total time from the original transaction date does not exceed 540 calendar days.

2) Merchant Response Window

You generally have 7-21 days to respond to Stripe chargebacks once notified.

The precise due date depends on the card network involved and will be shown in the Dashboard, in emails, and in API/webhook events (evidence_due_by).

Networks’ underlying rules are longer (Visa ~30 days, Mastercard ~45 days, AmEx ~20 days from issuer notification). Stripe (and most payment processors) compress this to 7-21 days to account for their processing time and to avoid network penalties.

🔥Pro Tip: Certain payment methods and processor integrations impose significantly shorter time limits, particularly for fraud disputes. The clearest example is Klarna processed through Stripe. Standard Klarna disputes allow 12 calendar days to submit evidence. Fraud disputes compress that to 5 days, with no second round of submission permitted.

3) Issuer Review and Decision Period

The card issuer generally has 60-75 days to deliver a ruling, depending on the card network involved. As indicated earlier, escalations to pre-arbitration or arbitration proceedings can extend the case.

Stripe Chargeback Fees and Costs

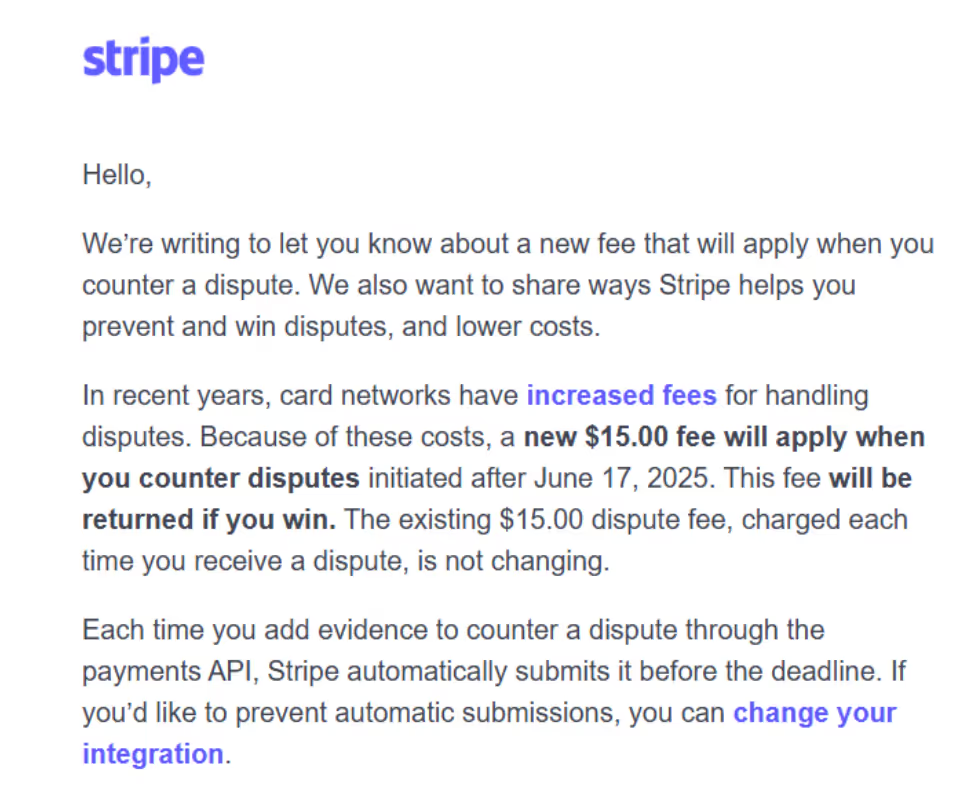

Stripe maintains one of the lowest direct chargeback fees in the industry, charging a flat $15 in the US. That’s until June 2025, when the company shifted gears in how the economics of fighting chargebacks work.

Here’s the precise Stripe dispute fee model as of writing, including the policy change that caught many merchants off guard:

The Two-Tier Dispute Fee Structure

Following the June 2025 dispute fee policy change, every Stripe chargeback now triggers two potential dispute fees:

1. Dispute Received Fee (always charged)

- US: $15

- Other countries: Local equivalent, e.g., £20 GBP, €20 EUR, AUD 25, etc. (The full table from Stripe’s June update can be found here).

- This fee is deducted instantly from your balance the moment the issuer files the dispute.

- It’s non-refundable in almost every case (the only exception is Mexico, where it may be returned on a win or withdrawal).

- It applies whether you fight or accept the dispute.

2. Dispute Countered Fee (new since the big policy shift)

- US: Additional $15

- Same local equivalents as above.

- Applies only if you manually submit evidence to counter the dispute.

- Refunded in full if you win.

- Not refunded on a loss or partial win.

- Does not apply in Japan, Mexico, or Thailand.

Net result for manual dispute counters:

- Win means you lose only the original $15 dispute received fee; the counter fee is refunded.

- Lose, and you pay a total of $30 (US) chargeback fee.

This change makes Stripe chargebacks one of the most expensive in the world for lost cases. Stripe said it introduced it to offset the rising card-network costs across the full dispute lifecycle.

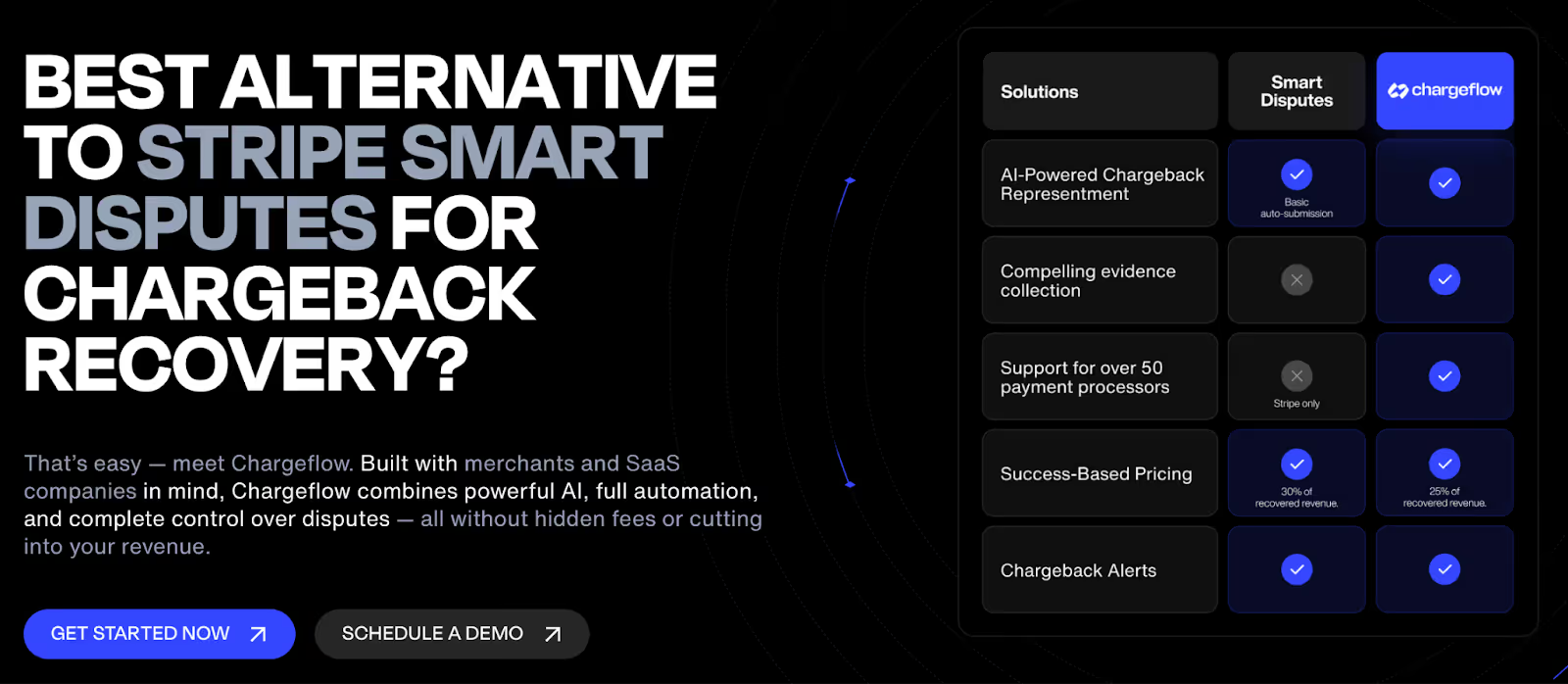

Does Smart Disputes Change the Dispute Math?

Stripe launched Smart Disputes alongside the new “dispute countered fee” policy as the intended step forward. Smart Disputes uses AI to auto-build and submit evidence for eligible disputes. It promises an automated path to resolution.

The impact on your dispute fee:

- If you lose the dispute, you pay only the $15 receipt fee.

- If you win, you pay 30% of the recovered amount as a success fee instead of a flat fee.

Key Benefits of Smart Disputes

- Reduces manual labor by automating dispute resolution.

- Increases win rates by optimizing evidence submission with AI.

- Reduces dispute expenses and waives the new dispute counter fee.

- Helps businesses scale dispute resolution without increasing their workload.

Important Downsides of Stripe Smart Disputes

- Limited data integration: No connection to communication tools or CRMs from third parties.

- Lack of control over evidence: Merchants have less control over the evidence that is submitted, reducing flexibility.

- Selective dispute handling: Only contests disputes Stripe’s AI deems winnable.

- Unclear success metrics: Stripe has not provided detailed data on win rates compared to third-party solutions.

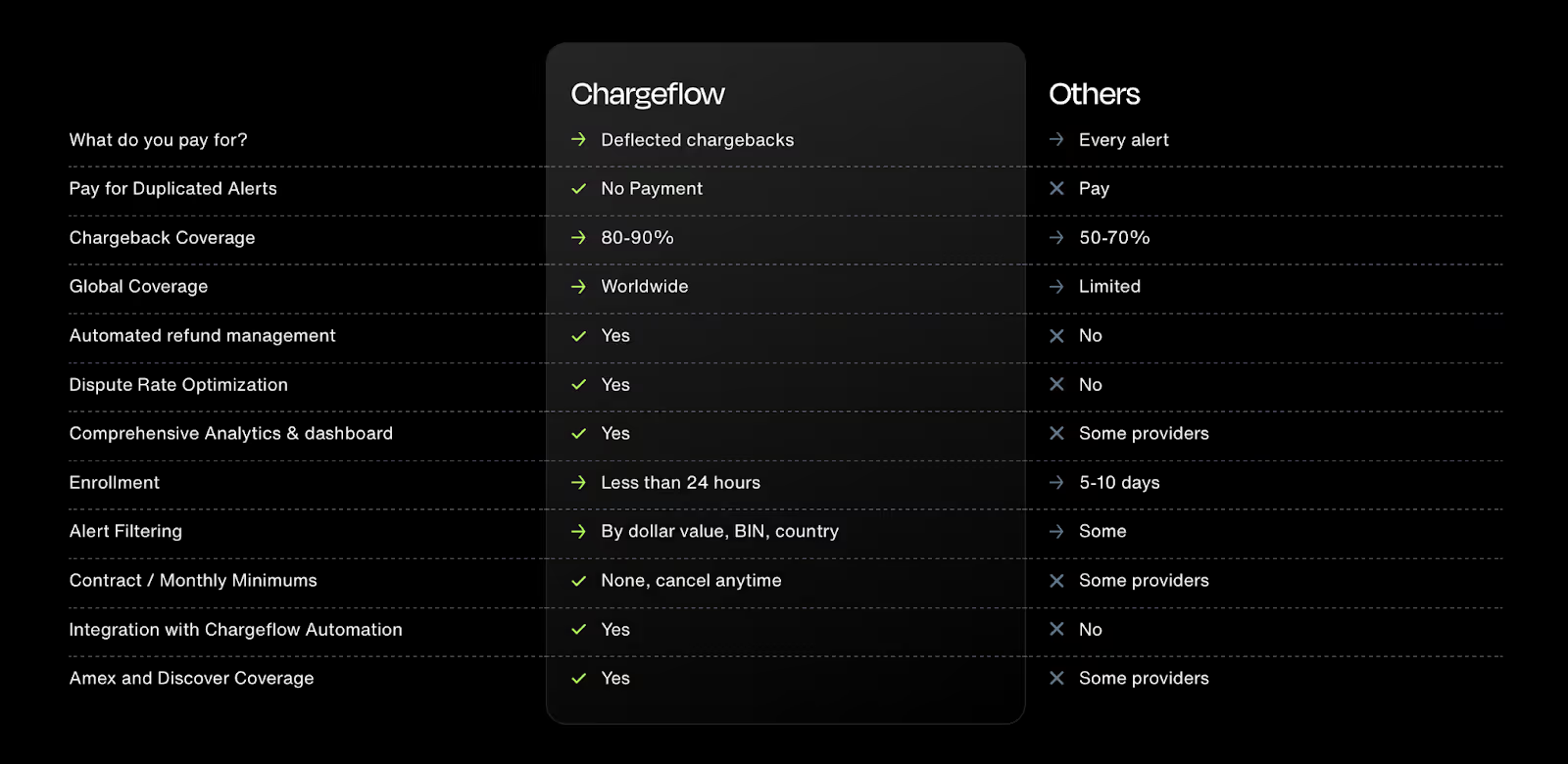

Why Chargeflow is the Smarter Alternative to Stripe Smart Disputes

Stripe’s Smart Disputes prioritizes speed and convenience. That’s not bad. But for high-value or complex disputes, an end-to-end solution like Chargeflow offers better control, deeper integrations, and higher success rates.

Stripe’s system may not counter every dispute. It also lacks access to external data like CRM records or customer communications, which Chargeflow uses to enrich evidence quality and increase win rates.

Key Takeaways:

Chargeflow helps merchants change the dispute fee math with:

- Full automation with zero manual work.

- Superior evidence collection from CRMs, emails, and customer interactions.

- Higher win rates through AI-optimized strategies and multiple processor integration.

- Custom solutions for subscription, SaaS, eCommerce, and high-ticket merchants.

- Real-time transparency, reporting, and pre-dispute alerts.

- Ideal for high-value disputes and high-risk industries, where success directly impacts profitability and prevention is prioritised.

With all that said, let’s examine Stripe chargeback prevention requirements.

Stripe Chargeback Prevention Best Practices

Stripe requires all merchants to maintain the lowest possible chargeback ratios. Your goal is clear: implement robust prevention mechanisms to keep ratios low and avoid triggering Stripe’s proactive outreach or enforcement. Prevention is, therefore, an operational necessity.

Here’s how seasoned merchants stay ahead:

Transaction Risk Control

The strongest defense against Stripe chargebacks begins at the authorization stage. Once a fraudulent or high-risk transaction is approved, the probability of a future dispute increases dramatically.

Stripe Radar serves as the core authorization-time safeguard. It assesses every payment in real-time using a combination of network signals, device fingerprinting, behavioral patterns, and historical fraud indicators.

Experienced merchants rarely depend on Radar’s default configuration. Instead, they:

- Craft custom rules to block or challenge suspicious patterns unique to their business (e.g., rapid same-card attempts, proxy usage, or geo-velocity anomalies).

- Dynamically tune thresholds and rules using Radar’s analytics and backtesting.

That said, it’s also worth noting that while Radar performs exceptionally well against third-party fraud, it may not prevent friendly fraud. At the authorization point, a customer planning to dispute later appears indistinguishable from a genuine buyer. They both have identical cards, devices, and initial intent.

This creates a critical gap that requires post-approval rework.

Post-approval/Pre-fulfillment Risk Mitigation

Solutions like Chargeflow Prevent address this by operating the post-purchase, pre-fulfillment window:

- It applies additional risk scoring using signals available after approval (order behavior, identity verification consistency, and anomalies not visible at checkout).

- Drawing from a shared cross-merchant network, Prevent flags actors with histories of dispute abuse, even if their initial transaction looked clean.

That’s the proven strategy for keeping dispute ratios below 0.5%. Prevent is a net after checkout to catch disputes Radar cannot see.

Pre-Dispute Interception

Even with powerful authorization-time control like Radar and a post-purchase scoring tool like Prevent, chargebacks can still occur. Why? Some cases originate from merchant mistakes, such as clerical errors or buyer confusion.

Some of these disputes do not begin as formal chargebacks. They start as issuer inquirers or early fraud signals. Card network services, such as Ethoca Consumer Clarity, Verification Order Insight, and Mastercard Collaboration alerts, allow issuers to query merchants before escalating a complaint into a formal dispute.

Leveraging this 24-48 hour window, merchants who implement chargeback alerts can resolve customer confusion or trigger refunds before the chargeback is filed. Because the case never becomes a formal dispute, it generally does not contribute to the merchant’s chargeback ratio.

Customer recognition Failures

Our research indicates that a considerable percentage of chargebacks are not fraud in the traditional sense. Rather, they are recognition failures. The cardholder simply doesn’t recognize the charge.

That’s why you must reduce ambiguity at every step of the customer journey:

- Billing descriptors must clearly match the brand customers remember.

- Product description and images must align with the delivered goods.

- Shipping timelines should meet customer expectations.

- Post-purchase communications, such as order confirmation, receipts, and tracking updates, must be leveraged to preempt buyer’s remorse.

When customers understand what they purchased and who billed them, the likelihood of a dispute drops significantly.

The objective reality is that Stripe chargeback prevention is a system. Not a feature.

Stripe Chargeback Coverage, Insurance, and Risk Exposure

Stripe chargeback protection is an optional add-on that reimburses merchants for specific fraud disputes. These include card-not-present unauthorized use, where the cardholder claims they did not authorize the transaction.

What It Covers: Eligible one-time transactions processed through Stripe Checkout, where the customer enters card details manually. Stripe handles the dispute, reimburses the disputed amount, waives dispute fees, and covers related network fines. No evidence submission is required from merchants.

What Is Not Covered: Friendly fraud, recurring billing charges, manually approved or overridden transactions, post-3DS fraud, and non-fraud reason codes. In practice, this excludes the majority of disputes that most merchants actually face.

Costs and Limits

Pricing: 0.4% per protected transaction, added on top of standard fees. The fee only applies to protected transactions.

Annual cap: $25,000 per merchant account (€20,000 in Europe, £20,000 GBP, with equivalent limits varying by settlement currency). The cap covers reimbursed amounts and waived fees combined. Stripe can adjust limits at its discretion after notice.

Eligibility: Available primarily in the US and Europe; typically requires 6+ months of processing history, use of Stripe Checkout, no selective routing of high-risk charges, and ongoing compliance with program terms.

Risk Exposure Reality Check

This program shifts some financial risk for true third-party fraud. But it leaves the bulk of real-world chargeback exposure uncovered:

- Most chargebacks stem from friendly fraud or merchant-related issues, which are not covered.

- The $25,000 annual cap can be exhausted quickly for mid-to-high-volume merchants in a bad month.

- The 0.4% fee applies to every protected transaction regardless of whether a dispute occurs, making it somewhat of a fixed cost rather than insurance against rare events.

- Even protected disputes still count against your ratios, as protection does not reduce your chargeback rate, and card networks track dispute volume regardless of reimbursement status.

The key takeaway for this section is that Stripe chargeback protection can be a targeted hedge against one slice of fraud risk. It does not provide comprehensive coverage.

Stripe Chargeback Policy and Account Limits

Stripe chargeback policy and account limit are tethered to card network thresholds. To that effect, Stripe tracks disputes as a percentage of successful payments within the same period, calculated on a dispute-date basis. Stripe monitors for accounts approaching the card network dispute threshold, not just exceeding it.

Card Network Monitoring Programs

The margin of error in chargeback management is becoming slimmer as card networks continually tighten policies.

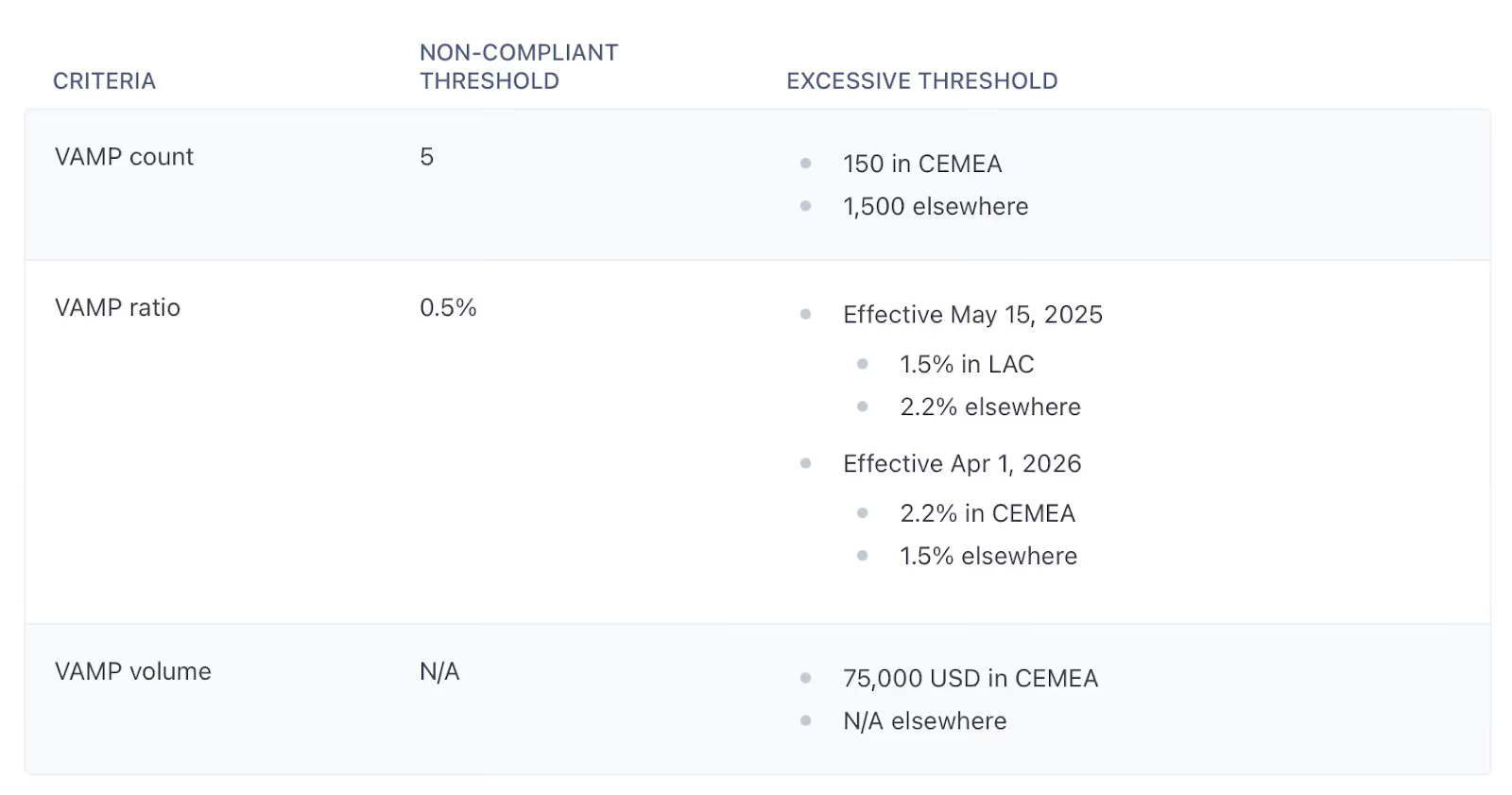

- Visa Acquirer Monitoring Program (VAMP) has consolidated fraud signals (TC40/EFWs) and formal disputes (TC15) into a single ratio. The excessive merchant threshold dropped from 2.2% across all regions except CEMEA.

- Mastercard ECM is triggered at 100-299 chargebacks with a ratio at or above 1.5%, while Mastercard HECM triggers at 300 or more chargebacks with a ratio at or above 3%. Monthly fines run from $1,000 to $200,000, with a MATCH listing a near-certainty at the HECM level.

Stripe may act on a reasonable belief that your account is likely to incur excessive disputes or presents an unacceptable risk.

Stripe’s Escalation Sequence

Stripe’s enforcement priority is platform stability and broader ecosystem relationships. This is why intervention is early, and the escalation sequence moves fast.

The escalation sequence generally moves through:

- Proactive outreach: Warning emails and Radar recommendations when activity trends north.

- Reserves: Holdback of 10-25% of volume to cover potential losses.

- Payout delays: Altered schedules to reduce exposure.

- Suspension: Temporary processing halt.

- Termination: Full account closure, with reporting to MATCH?VMSS for up to five years, making re-onboarding across processors extremely challenging.

The safe zone is to stay clear of outreach and network entry through proactive dispute mitigation. Stripe can (and does) terminate for “likely to incur excessive disputes” before you ever reach network thresholds.

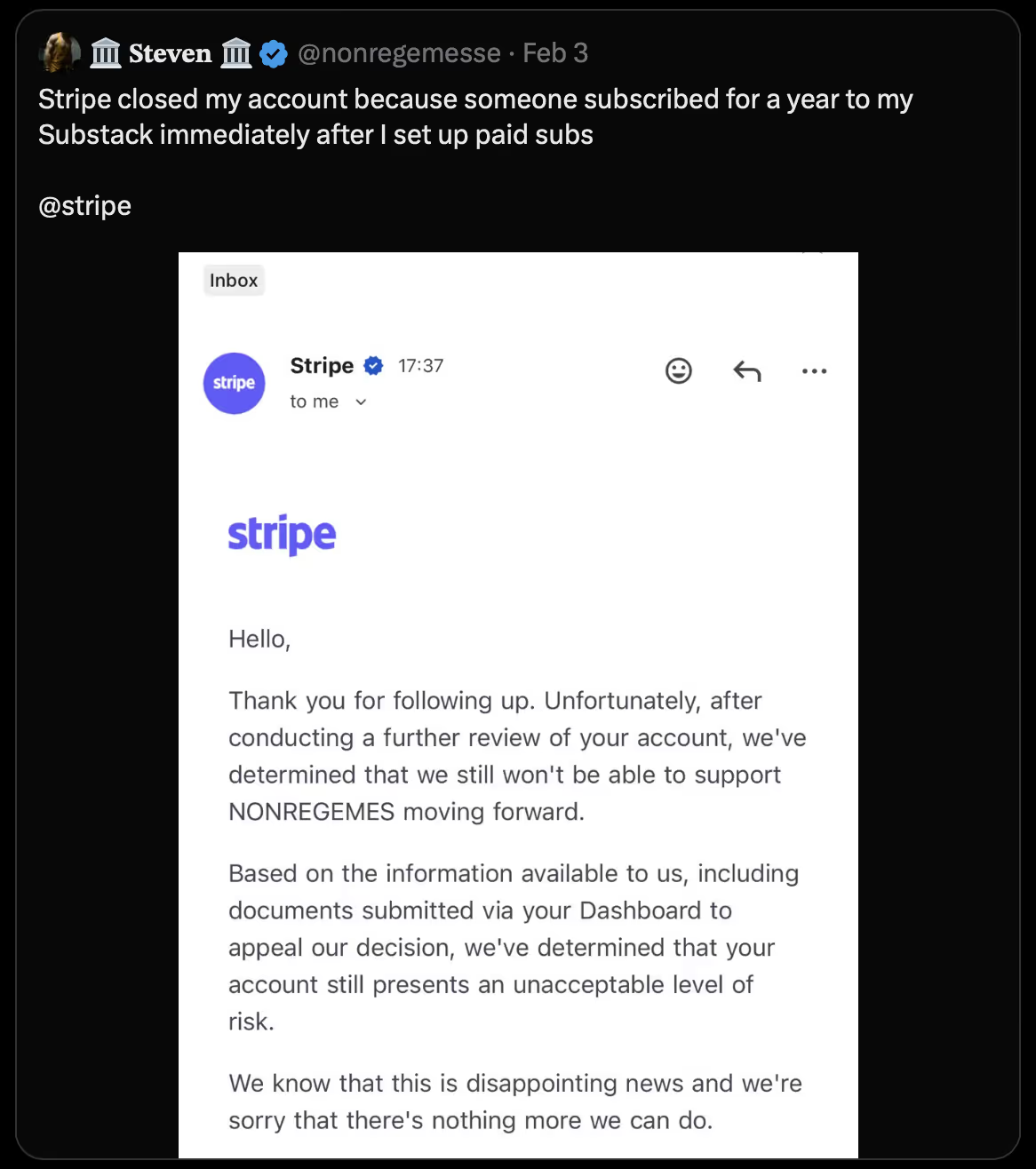

“This is what people misunderstand about 'risk.' It’s not about fraud already happening; it’s about sudden behavior that looks anomalous to a model. One event, wrong timing, wrong pattern, and the system overcorrects. It’s brutal, but predictable.” – Avia Chen, Co-founder of Chargeflow

How to Fight Stripe Chargebacks

Fighting a Stripe chargeback means challenging it through chargeback representment. This entails submitting compelling evidence to the issuing bank through Stripe to reverse the chargeback and recoup funds.

Since this is a one-shot process where success isn’t guaranteed, you might as well skip the manual representment lottery. To quote Mastercard’s 2025 State of Chargebacks Report, “the chargeback process is costly and time-consuming. So, it should not be surprising that Financial Institutions are steering away from manual human review toward analysis supported by automation or AI-based models.”

If banks and issuers are leaning hard into AI to handle disputes faster and cheaper, you have every incentive to do the same.

How to Automate Stripe Chargebacks with Chargeflow in 3 Steps

Step 1. Integration: Download Chargeflow from the Stripe Apps marketplace and connect data enrichment tools (Gmail, Gorgias, Zendesk, Recharge, Chargebee). Chargeflow syncs historical and new dispute data immediately, monitoring chargebacks in near real-time.

Step 2. Automation configuration: Choose how aggressively to fight disputes based on your risk tolerance, customize evidence with your branding assets (logo, policies, terms), and decide whether Chargeflow submits automatically or queues cases for your approval.

Step 3. Hands-off operation: The system queues existing disputes, processes new ones as they arrive, and handles evidence gathering across all connected platforms. You focus on growing your business while Chargeflow fights disputes 24/7.

🔥 Read Stripe’s case featuring Chargeflow’s excellence in chargeback automation.

Final Thoughts on Stripe Chargebacks

The fact remains that every card payment you accept carries an embedded right of reversal. That’s not a Stripe policy, but rather a card network guarantee that predates Stripe by decades. No amount of prevention will eliminate chargebacks.

Fraud, merchant errors, and delivery failure are permanent features of commerce at scale. The chargeback mechanism exists precisely for that reason.

What is solvable, though, is your exposure to Stripe chargebacks. The merchants who stay in good standing are the ones who’ve built a system that keeps ratios predictable. They equally craft responses of high enough quality that Stripe's risk systems never have cause to look closely at their account.

That system has four components:

- Radar to filter bad transactions at authorization.

- Chargeflow Prevent to catch friendly fraud in the post-approval window that Radar can’t see.

- Alerts to intercept disputes before they land on the Dashboard.

- Chargeflow Automation to submit evidence that’s truly built to win, enriched with CRM data, customer communications, and reason-code-specific arguments.

Each fabric addresses a different point of failure. Running all four means disputes that do reach you are the minimum, not a symptom of a preventable operational gap.

That, my friend, is the difference between chargebacks as a manageable cost and chargebacks as an existential risk.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)