%201.svg)

Chargeback Fraud Management Explained: Purpose and Benefits

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

Chargeback fraud management is the systematic process of preventing, tracking, and resolving forced payment reversals. Effective management requires two approaches: prevention (fraud detection, customer communication, clear policies) and dispute resolution (evidence gathering, timely responses, strategic fighting). Modern solutions like Chargeflow use AI automation to handle evidence compilation and submission, achieving 60-70% win rates versus manual processes. Without proper management, chargebacks trigger processor penalties, account termination, and revenue loss exceeding the original transaction value.

A recent scientific discovery has revealed why chargeback fraud continues to rise, as Mastercard expects global chargeback volume to reach 324 million in 2028. Stay with me as I explain. This phenomenal discovery will astound you!

The anterior mid-cingulate cortex (aMCC) is a vital hub in the human brain's network. A breakthrough study published in the National Library of Medicine demonstrates that aMCC is the engine room for cost/benefit analysis of decision-making.

The study found that when people do things they don’t want to do, their anterior mid-cingulate cortex grows. This brain change creates a neurological feedback loop that induces the desire to repeat the act.

This explosive scientific discovery is in parallel with industry records on chargeback trends. Research shows that many chargeback fraudsters are indeed customers experiencing buyer’s remorse. Filing chargebacks, therefore, becomes their recourse to undo legitimate transactions. Guess what? 40% of these buyers who successfully chargeback a transaction will likely submit another dispute within 90 days.

Incidentally, you, the merchant, bear the full cost.

This comprehensive guide will take you on a transformative journey through every aspect of chargeback fraud management. By the end, you’ll gain unquestionable expertise in navigating the intricacies of payment fraud. Let’s dig in!

What Are Chargebacks (and Why Do They Matter)?

Chargebacks are forced payment reversals that trigger a self-reinforcing crisis. Not just refunds with extra steps. Each one trains customers that disputing charges is faster than calling customer support. That’s the neurological feedback loop in action. And it’s bankrupting merchants who treat chargebacks as isolated incidents instead of the systematic threat they are.

But that’s not all. Every dispute nudges your chargeback ratio to the card network threshold, where processors terminate accounts. Meanwhile, the customer who caused this is coaching others on TikTok.

This is why chargeback fraud management isn’t optional. It’s a skillful approach to break the cycle and stop the spiral.

What Is Chargeback Fraud Management?

Chargeback fraud management is the systematic measures a business puts in place to prevent, track, examine, and resolve chargeback requests from a buyer’s card issuer or financial institution.

Effective chargeback fraud management covers two critical dimensions:

- Prevention: Implementing strategic measures to reduce the likelihood of chargebacks occurring in the first place. This includes friendly fraud detection and deflection, clear communication, quality customer service, and transparent billing practices.

- Remediation: Proactively investigating and responding to chargebacks that do occur, gathering compelling evidence, and submitting well-crafted rebuttals to win disputes.

Chargeback procedures are intricate. They involve several parties, strict timelines, and ever-changing industry restrictions. Understanding these complexities helps you minimize losses in the gruesome chargeback fraud management process.

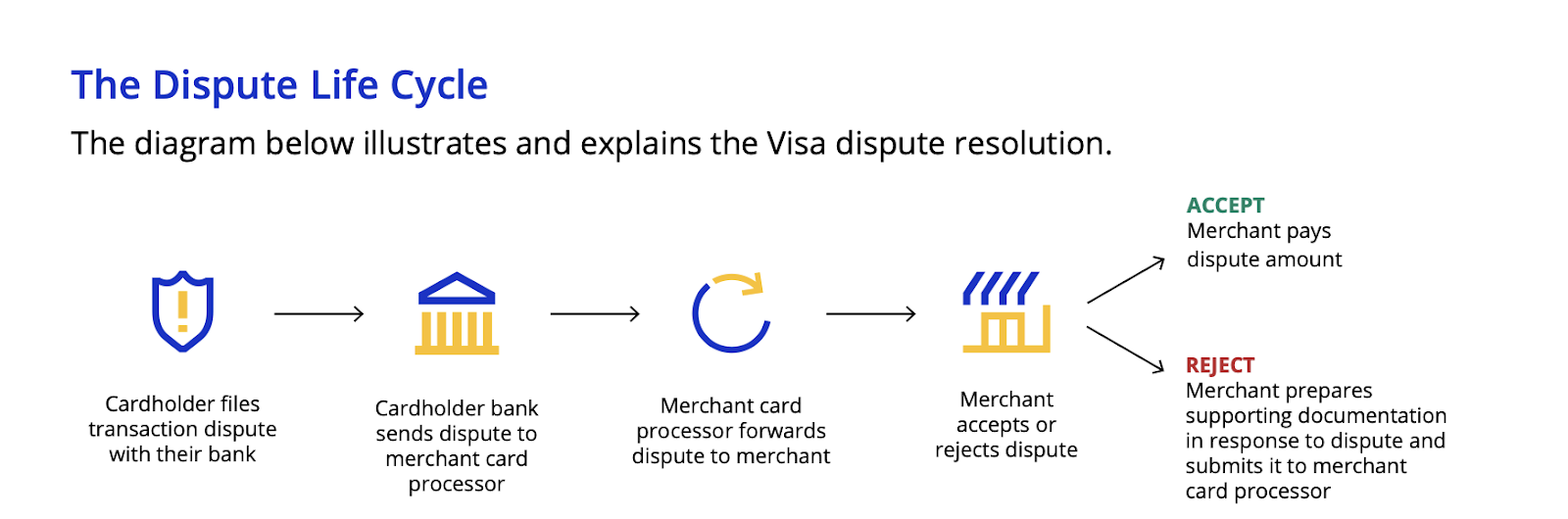

How the Chargeback Process Works

Understanding the chargeback process is essential for informed dispute management. Here’s the step-by-step breakdown:

- Customer disputes a charge: The customer contacts their bank to dispute a specific transaction. Cardholders usually have 45-180 days to dispute charges.

- Issuer reviews the claim: After receiving the claim, the card issuer reviews its validity. This typically takes about six weeks, or 30 days for Visa cards.

- Conditional reversal: If they see merit in the case, the bank initiates a chargeback on behalf of the customers, awarding them a temporary funds reversal from the merchant’s account.

- Merchant response: You’re required to investigate the dispute, gather relevant documentation as evidence of transaction legitimacy, and present an air-tight case to the payment processor or acquiring bank to challenge the chargeback.

- Resolution: If your case is compelling enough, the card issuer or financial institution will overturn the claim and return the charge to your account. But if not, the cardholder retains the provisional credit issued.

The chargeback process often takes up to 90 days. It can extend further if the case goes to arbitration. Each step has specific deadlines that vary by card network.

Why Businesses Need Chargeback Fraud Management Systems

According to Chargeflow chargeback statistics and trends, chargebacks increase as digital transactions grow. The need for tools, processes, and best practices to combat the rising chargeback threat has become even more pronounced today.

Here’s why you need a well-defined chargeback fraud management system:

1) Closing Fraud Loopholes Before Transactions

De-risking transactions is a crucial aspect of chargeback fraud management. This involves pre-transaction measures, such as tracking and verifying customers’ identities before they purchase, to prevent fraud.

For example, augmenting customer authentication and pre-transaction holds with Chargeflow Prevent stops fraudsters from making transactions that will ultimately lead to chargebacks.

2) Minimizing Errors and Confusion After Billing

Having a policy for how you plan to prevent and contest disputes ensures you’re not flushing hard-earned revenue down the pipe. This may include quality-assuring transaction records to eliminate merchant errors, such as double-billing and clerical mistakes.

Aside from limiting internal errors, having a well-defined chargeback policy enables customers to track bills, especially for subscription payments. For example, ensuring digital bank channels and issuer back-office teams have pertinent merchant information, such as name, logo, and receipt, helps minimize friendly fraud.

3) Efficient Chargeback Accounting and Reporting

This is one of the most essential benefits of well-thought-out chargeback fraud management. Accounting for chargebacks will no longer be a nightmare. Instead of adding chargeback losses into the cost of sales, you can better account for these distinct costs and make your books make sense. Furthermore, having a streamlined chargeback fraud management approach is fundamental for KPI monitoring and reporting. You can track issue areas and close loopholes by analyzing chargeback data.

4) Optimizing Net Win Rate With Automated Chargeback Fraud Management

The primary reason for most retailers’ disappointingly low chargeback win rate is the communication gap between issuers, merchants, and consumers. Chargeback processes, terminologies, and rules are not uniform among all the stakeholders. Understanding the timeframe for each stage alone is a nightmare.

But imagine a tool that helps you stop chargebacks before they become chargebacks. Chargeback automation minimizes chargebacks with data-driven measures. It challenges false disputes at a superior win rate and keeps your chargeback ratio in check.

"Nothing has decreased in payment risk. Businesses still have major risks and always will, especially in online transactions. If anything, it is getting worse. Agentic commerce will create way more friction." -- Ariel Chen, CEO and Co-Founder, Chargeflow

Chargeback Fraud Management Strategy: Roles, Risk, and Responsibility

Traditionally, creating a chargeback fraud management strategy requires clearly defined roles, understanding your risk profile, and establishing accountability across your organisation.

That means establishing a procedure that determines who handles what, which disputes to fight, and how to prevent the next wave of cases.

Key Roles in Conventional Chargeback Fraud Management

- Chargeback Specialist: Handles day-to-day dispute responses, evidence gathering, rebuttal submission, and follow-up (if applicable).

- Fraud Analyst: Monitor transactions for suspicious patterns and implement prevention measures to limit dispute exposure.

- Customer Service Team: Serves as the first line of defense by resolving customer issues before they escalate to costly chargebacks.

- Finance/Accounting: Track chargeback costs, monitor dispute ratios, and ensure proper chargeback accounting.

- Chargeback Manager: Oversees the entire program, analyzes trends, optimizes processes, and coordinates between departments.

Understanding Your Risk Profile

Banks assess merchant risk through four main categories: your company's financial history and credit, your industry vertical, your billing model, and your transaction volume. Different business models face different chargeback risks. High-risk industries include:

- Travel and hospitality (long fulfillment windows, cancellations)

- Digital goods and SaaS (intangible products, subscription fatigue)

- eCommerce (card-not-present fraud, delivery disputes)

- Nutraceuticals and supplements (aggressive marketing, buyer's remorse)

- High-ticket items (luxury goods, electronics)

Fighting chargebacks without knowing your risk profile is like treating symptoms without diagnosing the disease. Your risk profile should inform your prevention strategies, evidence collection protocols, and resource allocation.

Establishing Clear Responsibilities

Whether you’re a solo founder fighting disputes between customer calls or running a dedicated fraud team, the challenge is practically the same. Someone needs to track deadlines, gather evidence, understand reason codes, monitor card network rule changes (such as Visa VAMP), and submit responses: all within 7-21-day windows.

This sounds great on paper. But the cost rarely makes sense with manual processes. Small teams burn hours they can’t afford. Large teams burn salaries on work that algorithms handle better. Both approaches cost more than the chargebacks themselves when you factor in opportunity cost and sub-optimal win rates.

That’s why teams are shifting chargeback fraud management responsibility to automated systems. Automated systems don’t replace your judgment. They replace administrative burden and minimize false representment. You still decide strategy, while AI handles execution.

Chargeback Fraud Management and Dispute Management

Managing chargebacks effectively requires excelling at two distinct, but related, principles: fraud management and dispute management.

Let’s examine these principles further.

1) Chargeback Fraud Management

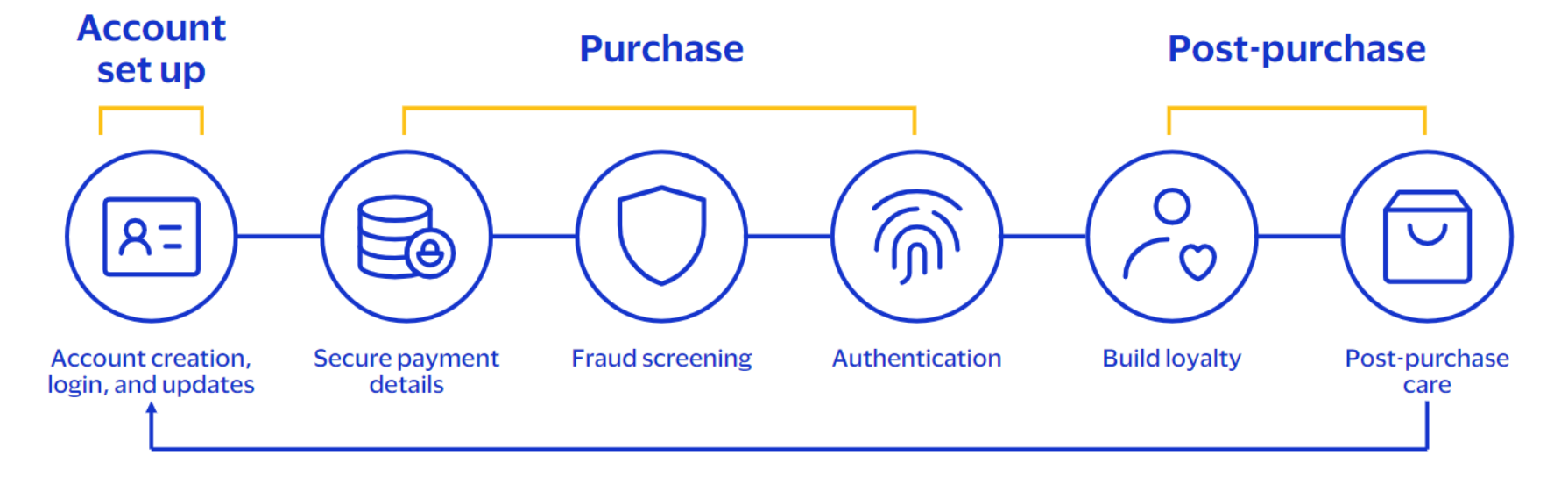

This pre-transaction mechanism excels at preventing illegitimate chargebacks before they occur. Your goal here is to de-risk transactions before processing. The two aspects of chargeback fraud are as follows:

- True fraud: These are cases that result from unauthorised use of payment credentials by criminals. Prevention includes deploying Prevent, AVS/CVV checks, 3D Secure authentication, device fingerprinting, and velocity checks.

- First-party fraud: First-party fraud (friendly fraud): Customers dispute valid purchases, intentionally or by mistake, to reverse charges. Chargeback alerts prevent this by notifying you before disputes are filed.

2) Dispute Management

When prevention fails, for whatever reason, and a chargeback occurs, well-thought-out dispute management becomes critical. The goal is to maximize net recoverability of false claims through:

- Rapid response: Acting within tight deadlines to gather and submit evidence.

- Evidence compilation: Gathering transaction details, shipping confirmations, customer communications, IP addresses, device data, and any other relevant documentation.

- Reason code analysis: Understanding the specific reason code to provide the most relevant evidence that sways the bank’s decision.

- Compelling rebuttal: Crafting clear, concise responses that address the customer's claim with irrefutable evidence.

- Strategic decision-making: Determining which disputes to fight based on win/lose probability, transaction value, and resource costs.

Modern chargeback solutions handle the entire process, from evidence gathering across the customer journey to reason-code-optimized response generation and submission.

The thing is, there are several tools nowadays, and not all chargeback fraud management solutions deliver the same results.

Chargeback Fraud Management Solutions: Tools, Software, and Systems

In today’s dispute-prone eCommerce landscape, chargeback fraud management has evolved into a specialized industry addressing a $41.69 billion problem. The solutions span from basic alert systems to comprehensive AI-powered platforms, each designed to tackle different aspects of the chargeback lifecycle.

Types of Chargeback Fraud Management Frameworks

- Chargeback alerts: Services like Chargeflow Alerts use network data (Ethoca and Verifi RDR) as well as proprietary frameworks to notify you of disputes before they turn into chargebacks. This heads up gives you a window to choose the most profitable course of action.

- Fraud prevention tools: Anti-fraud solutions like SEON, Sift, or Kount screen transactions in real-time using machine learning, behavioral analytics, and preset filters to block fraudulent purchases.

- Dispute management software: These are solutions that help teams handle evidence gathering, response generation, and, in some cases, submission to payment processors. Options include self-managed SaaS subscriptions or managed "dispute-as-a-service" with consultancy.

- Analytics and reporting tools: These are not standalone products, but an intelligence layer within platforms. While performance differs across platforms, they track ratios, win rates, reason codes, and trends for insights that inform both dispute prevention and response.

- All-in-one platforms: AI-native platforms like Chargeflow offer comprehensive coverage through alerts, friendly fraud prevention, representment, and analytics.

But how does this magic work? Let’s expand into that.

How Chargeback Fraud Management Software Works: Focus on Chargeflow

Advanced chargeback fraud management platforms like Chargeflow use machine learning to analyze win patterns, optimize evidence selection and submission, and predict dispute outcomes. They get smarter with every case while eliminating manual work.

How Chargeflow Works:

1. Integration: Connect your payment processors (Shopify, Stripe, PayPal, 100+ platforms) and enrichment tools (Gmail, Gorgias, Zendesk, Recharge, Chargebee). Chargeflow syncs historical and new dispute data immediately, monitoring chargebacks in near real-time.

2. Automation configuration: Choose how aggressively to fight disputes based on your risk tolerance, customize evidence with your branding assets (logo, policies, terms), and decide whether Chargeflow submits automatically or queues cases for your approval.

3. Hands-off operation: The system queues existing disputes, processes new ones as they arrive, and handles evidence gathering across all connected platforms. You focus on growing your business while Chargeflow fights disputes 24/7.

Benefits of Automated Chargeback Fraud Management

Automation has transformed the chargeback workflow. The process has transitioned from a manual, reactive process into a proactive, data-driven operation. Prominent benefits of automated chargeback fraud management include:

- Net positive chargeback processing: Automated systems run as long as your systems are active. They yield the best results in terms of win rates, even as chargeback prevention and disputes are set on autopilot.

- Scalability: Handle hundreds or thousands of disputes without proportionally increasing staff.

- Consistency: Every response follows best practices and includes all relevant evidence, eliminating human error and oversight.

- Speed: Instead of working to beat the clock, responses are generated and submitted in minutes without you lifting a finger.

- Data-driven optimization: Continuous analysis of dispute outcomes to refine strategies and improve win rates.

- Resource efficiency: Free your team to focus on high-value activities, such as fraud prevention strategy and customer experience improvement.

Additional incentives include a centralized dashboard to monitor all disputes, review automated responses before submission (if desired), and access real-time analytics from anywhere with an internet connection.

Can You Handle Chargeback Fraud Management Internally?

The short answer is yes, you can. Nevertheless, handling chargeback fraud management manually isn’t as feasible as it sounds. Even a low volume of 20 disputes monthly can be challenging. You will have to track deadlines across multiple processes, learn various card network reason code nuances, compile evidence from various systems, and craft compliant rebuttals.

That’s exactly what Chargeflow customer Fanatics learned the hard way. In their words:

Besides the “I can do it myself” aspect, some teams handle chargeback fraud management internally because they’re protective. They want control over their process, customer data, user experience, existing workflow, etc. Adding new software means granting system access, risking integration headaches, and trusting automation not to send embarrassing responses to banks or disrupt how things currently work.

That caution makes sense. But modern chargeback solutions don’t replace your systems. They plug into them. They serve as your operating system for all things chargebacks.

Thus, the debate of in-house vs outsourced chargeback fraud management really boils down to how much control you maintain over daily decisions versus strategic oversight. And you can achieve this control through hybrid or fully managed options.

Hybrid vs. Fully Managed SaaS Chargeback Solutions

Hybrid SaaS Chargeback Fraud Management Solutions

What they provide: A combination of software and selective outsourcing where merchants choose which transactions and chargebacks to dispute while relying on a service provider for actual dispute handling. Dispute Ninja and Chargebacks911 are among companies offering the hybrid model.

Best for: Teams with some internal chargeback knowledge but need expert backup for complex or high-value disputes. Practical for small businesses and growing teams that want to reduce costs by choosing specific cases to pursue while maintaining greater oversight and leveraging external expertise for specialized tasks.

Key advantage: You maintain oversight and control, potentially reducing costs by choosing which cases to fight internally versus outsourcing, while still accessing technical expertise when needed. You can also get flexibility to scale your approach as you grow; you can start with more hands-on involvement, and gradually delegate more as volumes increase.

Limitation: Managing and coordinating multiple tools or agencies can be difficult. Some providers use offshore, semi-skilled labor, which compromises efficiency and turnaround time, but negatively impacts win rates. You still need to hire a chargeback analyst for internal decision-making and expertise on which disputes are worth your time versus the provider’s.

Fully Managed Solutions

What they provide: Proprietary, end-to-end tools, machine learning, and human forensics to manage the entire dispute lifecycle, disputing chargebacks on your behalf so you can focus on day-to-day operations.

Best for: Merchants who want chargebacks completely off their plate, high-volume businesses drowning in disputes, or companies lacking internal chargeback expertise.

Key advantage: Win-rate guarantees (Chargeflow offers a 4x ROI guarantee, far higher than what merchants achieve handling their own) with zero internal resources required. The combination of patented technologies, machine learning, and human forensics enables long-term, sustainable ROI that one-size-fits-all DIY strategies can't match. You get dedicated account managers, not support queues.

Limitation: Performance-based pricing means you pay a percentage of recovered funds, which may not appeal to everyone, but it’s aligned with results. Less hands-on control over individual dispute decisions; you set parameters, and the provider executes.

| Factor | Hybrid SaaS Solutions | Fully Managed SaaS Solutions |

|---|---|---|

| What they provide | A mix of software and selective outsourcing. Merchants decide which disputes to pursue while the provider assists with dispute handling. | End-to-end chargeback management using proprietary tools, machine learning, and dispute specialists who handle the full dispute lifecycle. |

| Example providers | Dispute Ninja, Chargebacks911 | Chargeflow, Kount, Riskified |

| Best for | Teams with some internal chargeback expertise that want flexibility and selective outsourcing for complex or high-value disputes. | High-volume merchants or businesses that want chargebacks handled entirely by external specialists. |

| Key advantage | Greater oversight and cost control. Merchants can decide which cases to fight internally versus outsourcing. | Minimal operational burden. Providers manage the entire dispute process with automation and dedicated expertise. |

| Operational effort | Moderate. Requires internal review, coordination with vendors, and decisions on which disputes to pursue. | Low. Most operational work is handled externally, with merchants reviewing only key outcomes. |

| Limitations | Managing multiple tools or agencies can create complexity. Internal expertise is still required to determine dispute strategy. | Performance-based pricing and less direct control over individual dispute decisions, depending on the platform you choose. |

Key Chargeback Metrics, Fees, and Timeframes to Track

Excellent chargeback fraud management requires tracking the right metrics. Here are the critical KPIs every business should track:

Critical Chargeback Fraud Management Metrics

- Chargeback ratio: Total chargebacks divided by total transactions. Most payment processors flag accounts at 0.5-07% due to card network oversight.

- Win rate: Percentage of disputed chargebacks that you successfully overturn. Industry average is 20-40%; many Chargeflow clients achieve 60-70%.

- Net dollar recovery: The most important metric, which is actual dollars recovered minus the cost of fighting disputes.

- Reason code distribution: This identifies (mostly in theory) the cardholder’s intent for filing disputes and where to focus rebuttal and prevention efforts.

- Chargeback rate by product/service: An indicator to identify which offerings generate the most disputes.

- Average response time: How quickly you respond to disputes. Faster responses often correlate with better win rates.

Fees to Track

- Chargeback fees: $20-$100 per chargeback, regardless of chargeback representment outcome.

- High-risk processing fees: Increased processing rates if your chargeback ratio exceeds card network thresholds.

- Alert fees: Costs for chargeback deflection alerts (typically $20-40 per alert, but cheaper than full chargebacks).

- Software/service fees: Monthly platform fees or per-dispute costs for chargeback fraud management tools.

- Internal labor costs: Staff time spent on chargeback fraud management.

Critical Chargeback Timeframes

- Response deadline: Typically 7-21 days, depending on the payment processor and card network.

- Dispute window for customers: 45-180 days, depending on the card network and dispute reason.

- Resolution time: 60-90 days for initial decision; arbitration can extend to 120+ days.

- Fraud analysis window: Real-time to 24 hours for preventing fraudulent transactions before they become chargebacks.

How to Choose the Right Chargeback Fraud Management Tools

Selecting a chargeback fraud management solution is a critical revenue decision. I say that because it’s not simply about buying software. You’re determining your processor standing and whether you're recovering enough to justify the fight or just burning money on losing battles. Furthermore, the wrong choice equally exposes you to risks.

Essential Chargeback Solution Evaluation Criteria

- Integration capabilities: Seamless data flow is non-negotiable. So the platform must connect effortlessly with your payment processor, eCommerce platform, shipping carriers, and customer service tools.

- Automation level: Look for solutions that handle evidence gathering, response generation, and submission automatically. If they promise automation but leave you with manual labor, is it worth it?

- Evidence intelligence: Can the system pull from multiple data points and customize evidence based on reason codes? Generic responses are a thing of the past.

- Prevention features: Does it offer chargeback alerts, fraud screening for chargeback deflection, and prevention analytics? Fighting chargebacks is important, but preventing them is better.

- Analytics and reporting: Real-time dashboards, reason code analysis, win rate tracking, and ROI metrics should be standard.

- Proven results: What win rates do they achieve? Ask for case studies from businesses similar to yours.

- Pricing model: Is it subscription-based, per-dispute, performance-based (you only pay for recovered funds), or a hybrid? Align pricing with your volume and scalability goals.

- Scalability: Can it grow with your unique business model? Switching providers can be painful.

- Support and expertise: Human support is still relevant even in today’s AI world. Evaluate the team's experience. For SaaS tools, assess customer support quality and response times.

- Compliance and security: Ensure PCI compliance and robust data security practices.

Standard Red Flags to Avoid

- Promises of a hundred percent win rates regardless of chargeback type (unrealistic, as chargebacks where you’re wrong are unwinnable)

- Poor integration options (manual data entry defeats the purpose)

- Lack of transparency about pricing or results signals dishonesty

- A one-size-fits-all approach without customization means a headache for your team

- Slow or unresponsive support during evaluation can signal poor customer service

Final Thoughts on Chargeback Fraud Management

Chargeback fraud management is about preventing financial losses, stopping fraud in its tracks, and having your buyers talk to you before talking to their bank. It is also about complying with industry regulations that could impact your payment processing privileges. And when disputes slip through the cracks, you know how to fight back and resolve them.

Having systematic measures and tools for limiting dispute exposure, excavating, and making sense of chargeback data for maximum net win rate is a competitive advantage. Instead of the “whack-a-mole” game many merchants play when disputing cases, you are intentionally enhancing customer experience while keeping chargeback fraudsters at bay.

Learn more about Chargeflow’s chargeback automation.

Manage Chargeback Fraud End to End

You can set the parameters and let automation handle every fraud dispute, instead of reviewing each case by hand. Chargeflow automates fraud management end to end, backed by a 4X ROI guarantee.

Start for FreeChargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)