%201.svg)

Chargeback Alerts: What They Are and How to Implement Them [2026]

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

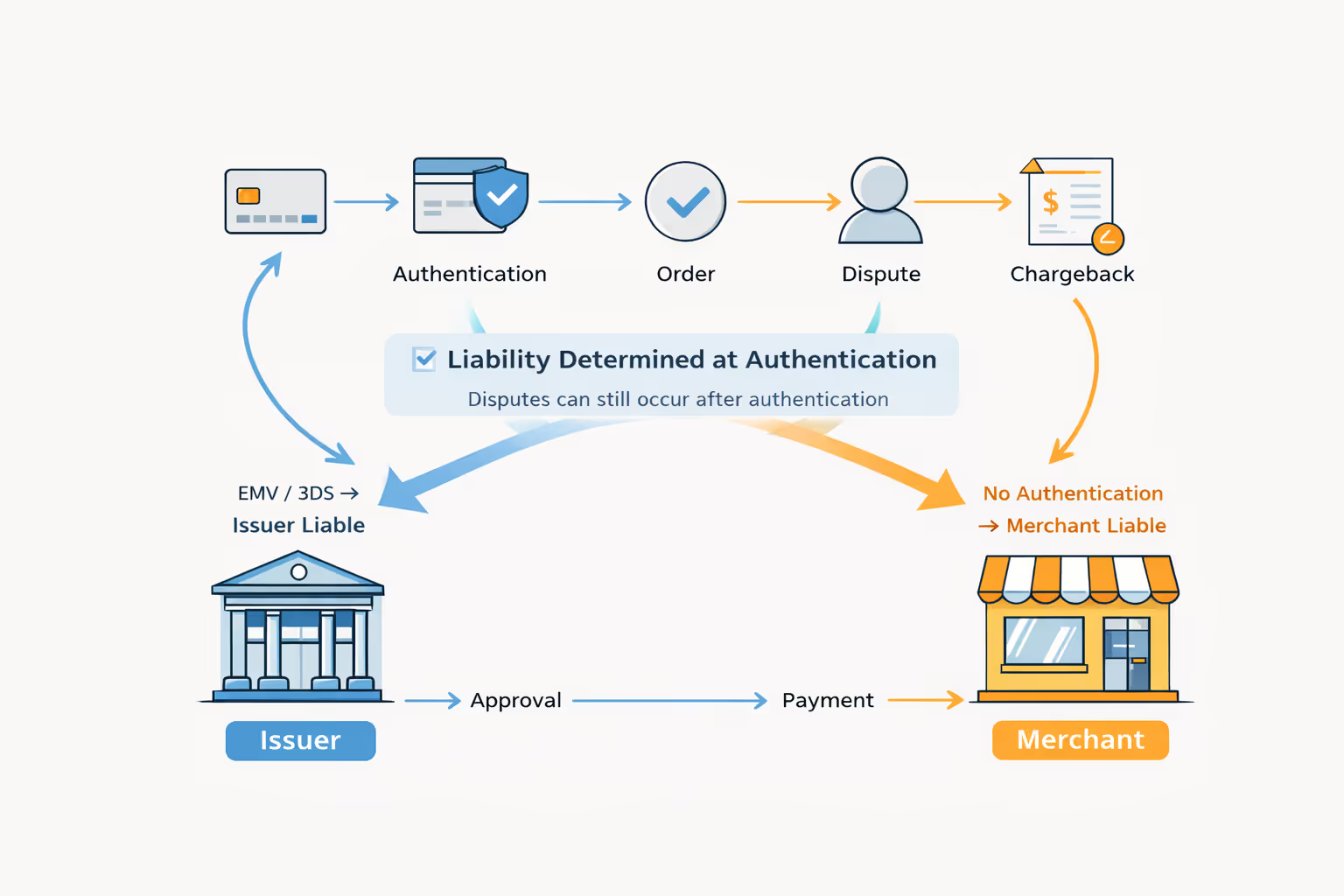

Chargeback alerts provide merchants with early warning when a customer disputes a transaction, providing a short window to resolve the issue before it becomes a formal chargeback. This early intervention can prevent dispute fees, protect ratios, and reduce operational costs. Alerts, including Chargeflow Alerts, are delivered through card network platforms like Verifi and Ethoca. These systems promptly inform merchants as soon as issuers receive a dispute request, enabling faster response and resolution.

Imagine you received advance notice of a serious issue about to affect your portfolio. You’d act immediately to reduce risk. Right? That’s exactly what chargeback alerts do for merchants. They provide an early chargeback warning that helps limit exposure before damage occurs.

Chargebacks are a persistent revenue killer. Global estimates suggest that by 2028, there could be 324 million chargeback cases, with card-not-present (CNP) fraud losses reaching 28.1 billion this year alone. These losses are driven in part by rising friendly fraud and third-party disputes. When you factor in the downstream costs, the total chargeback-related costs to merchants could reach $42 billion by 2028.

That’s why early dispute alerts are crucial. They give you the proactive edge to prevent disputes from escalating into costly chargebacks. Because in today’s dispute-prone eCommerce environment, it’s not a matter of if chargebacks will happen. It’s whether you can stay ahead of scammers when they try to steal from you with false claims.

What Are Chargeback Alerts?

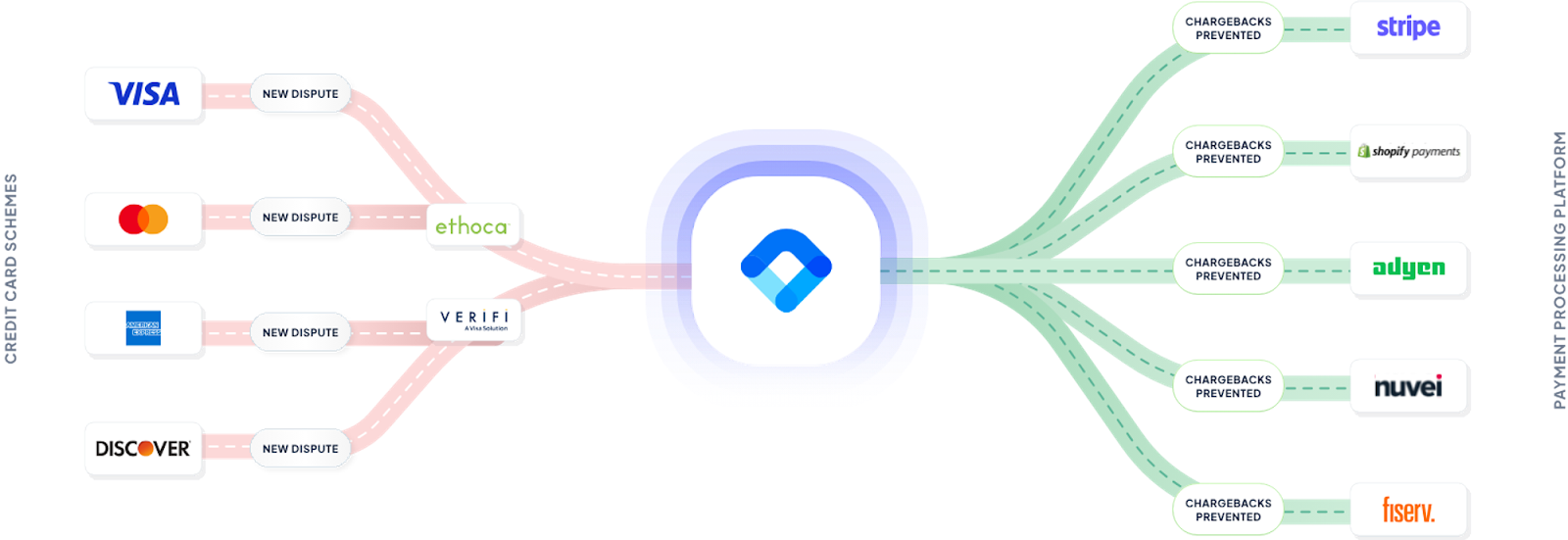

Chargeback prevention alerts are pre-dispute notifications from issuing banks to help merchants know when cardholders initiate disputes. They are routed through networks such as Verifi (a Visa subsidiary with strong U.S. coverage) and Ethoca (a Mastercard subsidiary with stronger coverage in Canada, Europe, and Asia).

When a merchant signs up for a chargeback prevention alert, the service provides them a 24-72-hour window to resolve a dispute and halt it from escalating into a chargeback.

Insights into How a Chargeback Alert Works: Focus on Chargeflow Alerts

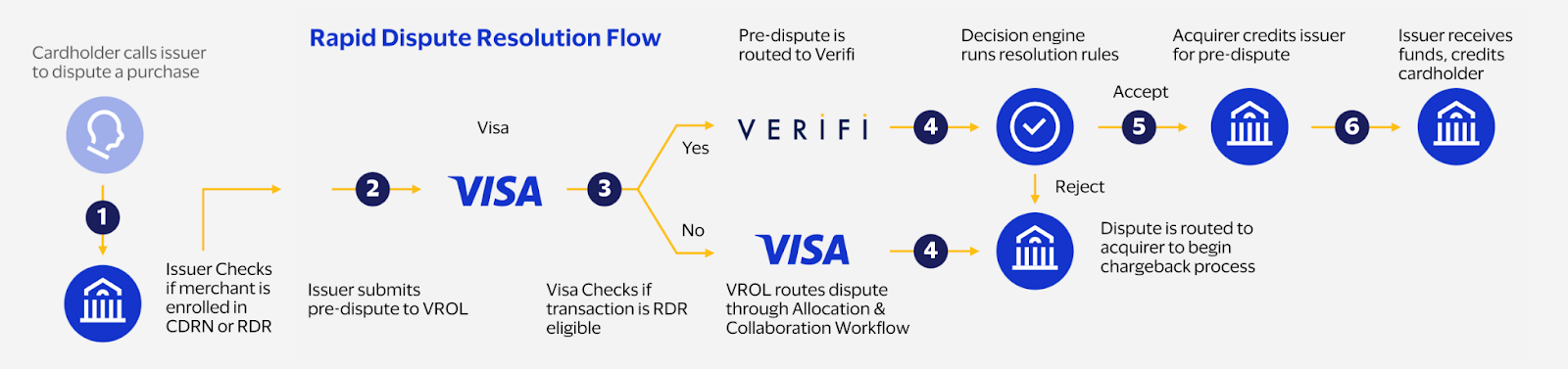

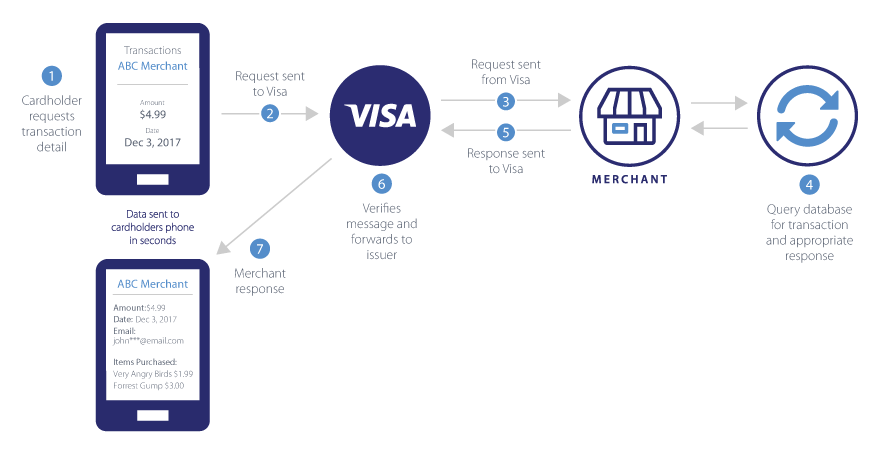

Chargeback alerts use card network data to help you intercept an impending chargeback and decide how best to handle the case. Chargeflow Alerts are connected directly to the card schemes. The system is notified immediately when a dispute is initiated.

Here’s how it works:

- A cardholder contacts their card issuer through an app, phone, chat, or a dedicated portal to dispute a transaction.

- Issuer evaluates and routes the case. If potentially resolvable, the issuer forwards to Verifi CDRN/RDR or Ethoca Alerts.

- Leveraging its proprietary fraud scanning technology and deep integration with Verifi and Ethoca, Chargeflow receives real-time notification of the disputed transaction.

- Chargeflow sends real-time notification through email, API, or dashboard, including transaction details, reason code, and cardholder information (privacy-compliant).

- Your system can then flag the transaction for human review or auto-refund it, depending on your specific rules when integrating Chargeflow Alert.

- The chargeback is avoided and does not count towards your dispute ratio.

💡 Chargeflow Alerts charge for prevented chargebacks, not for alerts. This means Chargeflow handles locating transactions and issuing refunds on your behalf, and you won’t receive duplicate alerts from different providers.

The Impact of Chargebacks and Why Alerts Matter

According to Visa literature, “chargebacks can be time-consuming and resource-intensive. And, for merchants, the process of responding to disputes, gathering evidence, and waiting for resolution can pull focus from day-to-day operations.”

We’ve done several research experiments on the chargeback multiplier effect. Every $100 chargeback costs 3-4.6x

The 4.6x multiplier for every $1 chargeback is not arbitrary. It’s the true cost merchants face when cardholders initiate fraudulent chargebacks, according to LexisNexis. A single spike amplifies this cost exponentially. It drives merchants towards network monitoring programs and severe penalties. We’ll examine this further in a subsequent section.

Why Chargeback Alerts Matter

To help you see why chargeback alerts make such a big difference, here’s a real-world case study.

Dizzy Path runs a small subscription box business. Things had been going pretty well. Until one morning. She woke up to the most frustrating chargeback situation ever.

A customer signed for the subscription, paid for two months, and received both boxes. She had tracking information and proof that the customer opened her emails. Still, they filed two “unauthorized transaction” chargebacks. She submitted full evidence, but the banks sided with the customer both times.

Your guess is as good as mine: this is a classic case of friendly fraud. Small businesses rarely win.

But the story could have been very different. If Dizzy Path had chargeback alerts, she could have acted immediately by refunding the transaction. She could have avoided losses equivalent to 4.6 times the transaction value.

What Happens When Your Chargebacks Spike?

When disputes surge, whether from seasonal fraud waves, policy abuse, or scaling issues, the fallout is rapid and multifaceted:

- Immediate financial impact: Each chargeback wipes out operating cash flow while incurring fees and reversal costs. As we highlighted earlier, true losses multiply rapidly. A $100 sale can cost at least $360 overall.

- Ratio escalation and network enforcement: Visa’s VAMP program tracks a count-based ratio. Exceeding the tightened new limits triggers:

- Fines.

- Rolling reserves or payout holds.

- Higher processing rates.

- Account restrictions or outright termination.

- Processor and acquirer pressure: Acquirers, under VAMP scrutiny, watch merchants like hawks. They often impose stricter merchant thresholds to stay compliant. This leads to frequent warnings, restricted volumes, or forced downgrades.

- Reputational and growth damage: Repeated issues signal poor user experience, hurting customer trust, acquisition, and retention. High-risk flags limit expansion into new markets or payment methods.

- Operational overload: Your wonderful CX team will keep drowning in pointless manual reviews, evidence submission, and firefighting, instead of focusing on core business.

- Spikes often snowball: One unresolved pattern encourages repeat offenders. It creates a vicious abuse cycle. Chargeback prevention alerts interrupt this early.

When you do the math on the cost of chargeback alerts, you’ll realize the service practically pays for itself.

“By sharing fraud and dispute data from issuers in near-real-time, chargeback alerts enable merchants to quickly respond to potential chargebacks by stopping order fulfillment, refunding the purchase, and effectively stopping the need for chargebacks altogether. For merchants and issuers alike, this speeds up the dispute process and not only gives customers a better experience but also reduces the operational costs associated with chargeback management.” -- Mastercard.

How Much Do Chargeback Alerts Cost?

Chargeback alerts are typically priced per alert. Costs vary depending on the provider, transaction volume, and the card network involved.

- Direct networks: ~$40 per alert (Ethoca often lower than Verifi), with volume tiers and minimums for direct signup.

- Platforms (Chargeflow): Pay-per-success ($29 billed only on deflected chargebacks).

- Other resellers may charge per dispute alert issued.

Overall, Chargeflow Alert pricing is the most flexible model that makes alerts accessible, offering you Verifi and Ethoca for broader coverage without dual integrations.

What Percentage of Chargebacks Can Alerts Prevent?

Many providers say they can realistically guarantee a 30-40% overall chargeback reduction. Conversely, the case study of Chargeflow merchants shows ~90% chargeback deflection, even as dispute win rate doubled within the review period.

So here are the facts:

- Standard implementation: 30-40% overall reduction.

- Platform enhanced: Up to 90% in AI-automated setups (Chargeflow Alerts through Verifi + Ethoca + proprietary matching, deduplication, and auto-refunds targeting friendly fraud and subscriptions).

Again, do the math. The ROI reality is that at a $29 pay-per-success instance, Chargeflow Alerts deliver fast breakeven. Near VAMP thresholds, they avert fines far exceeding costs, making them high-ROI infrastructure rather than optional add-ons.

How to Know If Your Business Needs Chargeback Alerts

If you’re wondering whether your business needs chargeback prevention alerts, there are certain telltale signs to look out for. Certain patterns and risk signals make chargeback alerts most essential. Use the following indicators to determine whether alerts could save you time, money, and dispute remediation headaches.

Strong Indicators:

- Ratio nearing or exceeding 0.5% or flagged Above Standard/Excessive.

- Friendly fraud makes up most of your disputes (common with subscription, digital goods, and high-ticket merchants).

- Recent spikes, processor warnings, or VAMP warnings.

- Volume where alert fees are lower than the prevented losses (e.g., 100+ monthly disputes).

There may be exceptional cases not covered in the checklist. Feel free to consult with our experts for an informed decision, especially if you’re beginning to scale.

Can You Self-Manage Chargeback Alerts?

Sure, you can. Just like you can do your own accounting with spreadsheets.

Here’s what salesmen never tell you about self-managing alerts: You’re not just “checking a dashboard.” You’re logging into Ethoca’s portal, then Verifi’s, then your processor’s RDR interface. Each alert requires you to play detective and everything in between. You must locate the transaction, retrieve order details, verify if it has shipped, check if there’s a refund already in process, determine your best response, execute it, and document everything.

For five alerts, this is annoying but manageable. But for fifty? You’ve spent your entire Tuesday on data entry instead of building your business.

The real cost isn’t the hours, though. It’s what you’re missing. Without aggregated data, you can’t see that the same customer disputes every third order from every store. Or that a specific product line generates 10x more alerts, or that your fraud rate spiked after that TikTok campaign. You’re flying blind, paying $30 per alert for the privilege.

Is it worth it when you have a more excellent alternative? Your guess is as good as mine!

How Network Inquiries Strengthen Chargeback Prevention

Card disputes generally happen in two stages:

- Inquiry

- Chargeback.

Network inquiries precede alerts. Through programs like Visa’s Order Insight and Mastercard’s Consumer Clarity, inquiries enable you to stop disputes at that discovery stage.

Here’s how network inquiries work to strengthen chargeback prevention (following the chargeback process highlighted earlier):

- A cardholder questions a charge with their bank.

- Instead of filing an outright chargeback, the issuer does some due diligence. They check the inquiry network for transaction details. That includes your company name, purchase description, delivery confirmation, and customer contact information.

- In some cases, they’ll contact you for supporting documentation. If the cardholder sees “Nike Running Shoes, Delivered Jan 15” instead of a cryptic merchant descriptor, genuine buyers often recognize the transaction and drop the dispute.

In a nutshell, network inquiries help merchants resolve disputes before the issuer initiates the chargeback. Hence, an accurate and timely response is crucial. That requires real-time integration between inquiry networks and your order management system.

Chargeback Alerts and Prevention Tools Platforms

The chargeback prevention ecosystem is a fragmented network of inquiry systems, alert providers, dispute resolution programs, and your own transaction data scattered across payment processors, order management systems, and fulfillment platforms.

Running these separately creates operational chaos. An inquiry comes in. But your generic merchant descriptor doesn’t help recognize purchases. An alert notifies of an impending dispute. But you’re manually romaging through systems to find the order. The process goes on.

Some merchants solve this by choosing a prevention platform. But not all platforms are built the same. Here’s a quick overview:

- Alert-Only Providers give you alert access but leave reconciliation, management, and analytics to you. You’re logging into multiple dashboards and manually matching alerts to orders.

- Gateway-Integrated Solutions (Stripe Radar, Chargebee) offer convenience if you’re already on their platform. But they lock you into their ecosystem. Switching processors means rebuilding your entire prevention infrastructure.

- Full-Stack Prevention Platforms (Chargeflow, Kount, Signifyd) consolidate alerts, inquiries, and dispute management with automated data enrichment and cross-system reconciliation.

The difference, though, is the level of automation, AI sophistication, and whether they handle representment or just prevention.

What Separates The Best Chargeback Platforms

- True automation: Do they just aggregate data, or actually take action with net-positive ROI? Auto-refunding valid alerts, enriching inquiries without manual input, and routing decisions based on win probability matter more than dashboards.

- Intelligence, not just data: Pattern recognition that flags repeat offenders, product-level risk scoring, and predictive dispute likelihood turn raw alerts into strategic advantage.

- Full lifecycle coverage: Platforms handling only prevention leave you scrambling when disputes slip through. Integrated representment with evidence generation means one system, one strategy, complete protection.

- Transparent economics: Some platforms charge per alert plus percentage fees. Chargeflow takes a transparent success-based fee on recovered disputes. Understanding the total cost at your volume matters.

The strategy should be simple. Analytics help you stop cases at source, alerts catch the rest, and representment comes in for leftovers. A full-stack chargeback coverage maximizes coverage and VAMP exemptions.

Fully Managed vs. Self-Managed Chargeback Alerts

The choice between managing alerts yourself or outsourcing to a fully managed platform isn’t about capability. It’s about economics and scale. Let’s examine the pros and cons of each strategy:

| Factor | Self-Managed | Fully Managed |

|---|---|---|

| Daily Work | Log into multiple portals (Ethoca, Verifi, RDR). Locate the transaction, verify order and shipping status, and manually issue refunds. Typically 10, 20 minutes per alert. | Alerts are processed automatically using AI and preset rules. Merchants review only exceptions. Typically 2, 3 minutes per flagged case. |

| Speed | Response depends on when dashboards are checked. Nights or weekends may cause delays, and some alerts expire within 24 hours. | Automated responses occur within ~15, 30 minutes, 24/7, regardless of time or day. |

| Accuracy | Higher risk of duplicate refunds across networks, missed alerts during busy periods, and manual matching errors. | Automatic deduplication prevents double refunds and maintains consistent accuracy even at high volumes. |

| Real Costs | Network fees ($20, 40 per alert) plus labor (~15 minutes per alert). Missed alerts result in full chargeback costs. Example: 100 alerts at $30/hr ≈ $750 monthly labor plus network fees. | Success-based pricing with platforms like Chargeflow. Captures more alerts and prevents additional chargebacks. |

| Volume Scaling | 50 alerts ≈ 12 hours/month. 500 alerts ≈ 120 hours/month, eventually requiring dedicated staff. | Operational effort remains nearly constant regardless of alert volume; only exception reviews increase slightly. |

| Insights | Manual spreadsheet tracking. Difficult to identify patterns, repeat offenders, or problematic products. | Automated analytics provide prevention rates by network, repeat offender detection, product-level trends, and ROI tracking. |

| VAMP Compliance | Dispute ratios calculated manually and tracked retroactively. | Real-time monitoring of dispute ratios with automated exemption applications and early warnings when thresholds approach. |

| Best For | <1,000 transactions/month, fewer than 20 alerts/month, simple product lines, and merchants comfortably below dispute limits. | 2,000+ transactions/month, 50+ alerts/month, lean teams, multiple products, or merchants approaching the 0.50% dispute threshold. |

| Break-Even Point | Labor remains cost-effective under roughly 20, 40 alerts per month (assuming $25, 40/hr labor). | ROI typically becomes positive above ~50, 75 alerts/month due to labor savings and higher capture rates. |

For scaling merchants, especially those approaching or exceeding the card network limit, fully managed alerts are a non-negotiable risk management instrument.

Getting Started with Chargeback Prevention Alerts

Activating Chargeflow Alerts is straightforward. Follow the steps below for a quick and successful setup.

If You’re Already Using Chargeflow, Do This:

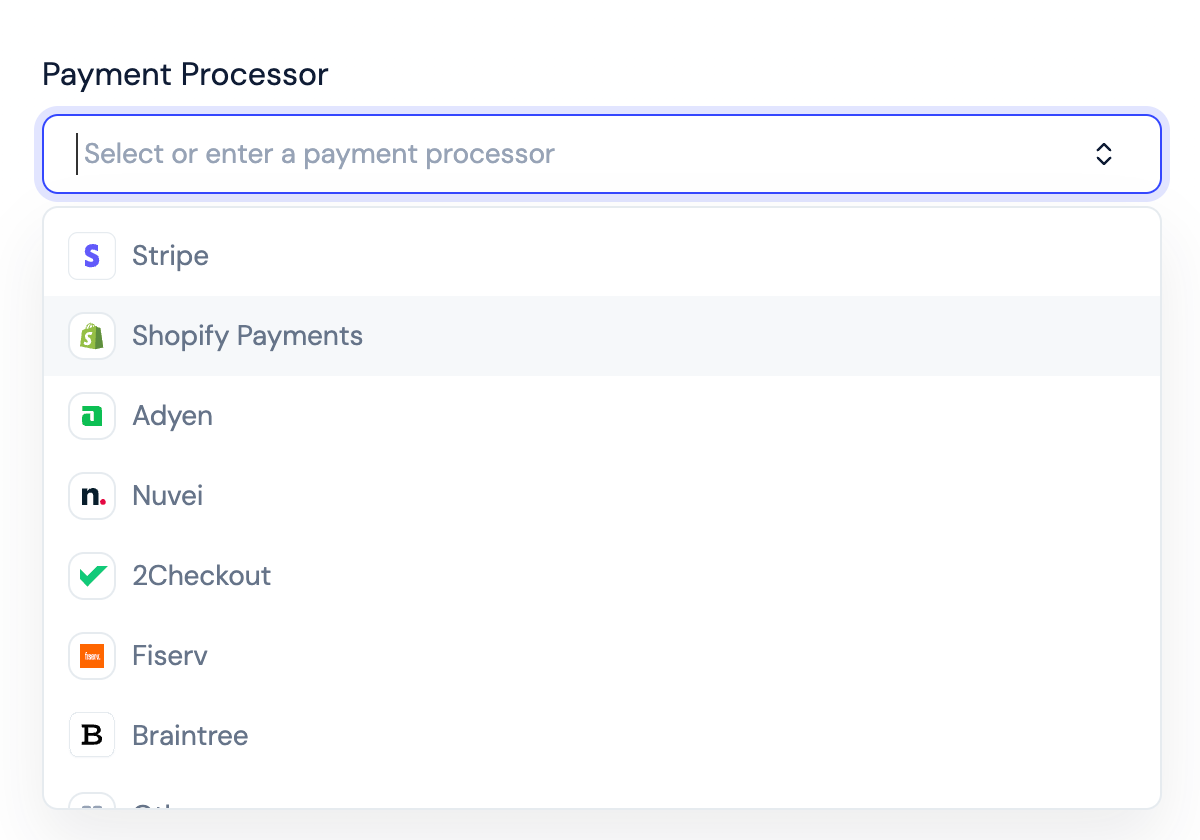

1. Go to the Alerts tab and click “Activate Now.”

2. Select your relevant payment processor(s).

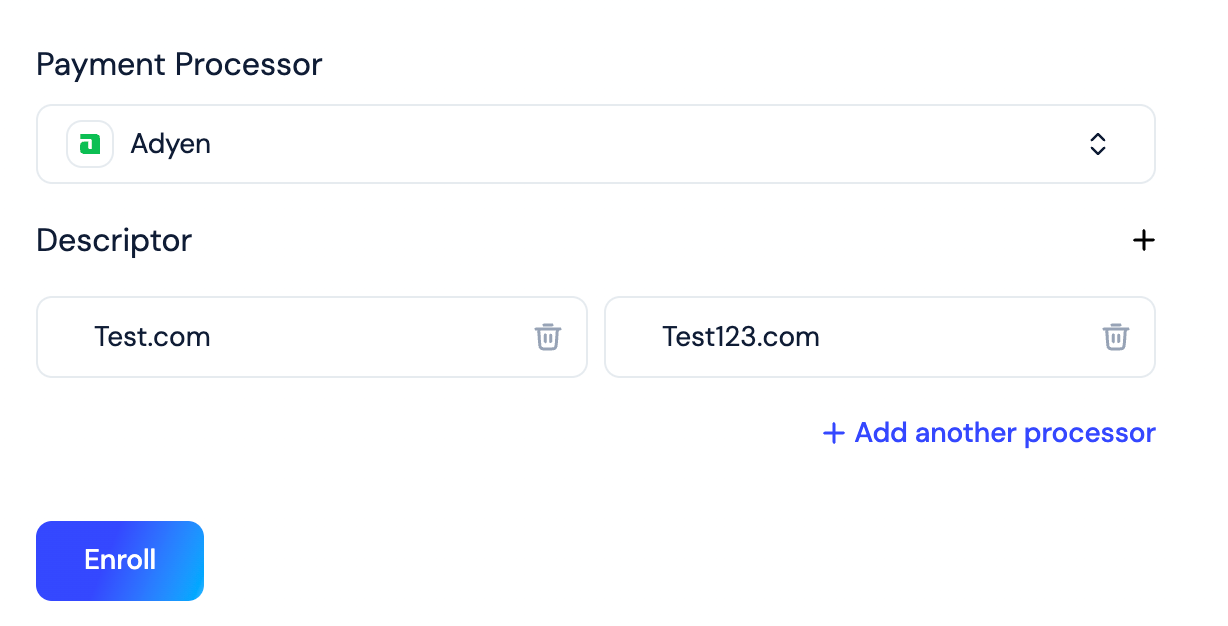

3. Add your statement descriptor, exactly as it appears in your processor or gateway dashboard (including correct capitalization). You can usually find this under Transaction, Payment, or Statement Descriptor settings.

💡 Need help? Read: How to find your payment descriptor.

4. Add a payment method if you haven’t already.

💡 Chargeflow places a temporary $100 hold for 7 days to verify eligibility. The funds are fully refunded afterward.

5. Watch for emails from the Chargeflow team requesting refund access to your payment processor. This step is mandatory; alerts will not go live until access is granted.

🚨 Complete this step promptly to avoid onboarding delays.

If You’re New to Chargeflow, Do This:

- Install Chargeflow from Stripe, Shopify, or WooCommerce.

- Take the steps above.

Once complete, you will start receiving alerts within 24 hours. While the complete Alerts Enrollment process can take up to 14 days due to varying enrollment times of different providers, you’ll begin getting alerts from some providers almost immediately.

Final Thoughts on Chargeback Alerts

When there’s early visibility into a risk, the smart move is to act before it turns into a loss. That’s the role chargeback alerts play in modern payments: early intervention, controlled outcomes, and predictable costs in an otherwise reactive system.

We’ve covered how the system works. Cardholders dispute, providers like Chargeflow route through Verifi, Ethoca, and proprietary infrastructure, and you respond before it escalates. We’ve also examined why self-managed options break down at scale, how automated setup involves a seamless plug-and-play process, and how network inquiries add pre-alert protection.

In today’s landscape, alerts aren’t optional for high-growth merchants. With VAMP tightening and fraud spiking, proactive interception puts you in the driver's seat. Again, if ratios are creeping or chargeback spikes loom, implementing chargeback prevention alerts now is a smart move. The cost of inaction is lost revenue.

Schedule a call with our sales team for onboarding support, or click here to get started right away.

Get Chargeback Alerts That Actually Stop Disputes

You can catch a dispute before it becomes a chargeback instead of finding out after the funds are already gone. Chargeflow automates prevention and dispute response end to end, backed by a 4X ROI guarantee.

Start for FreeChargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)