%201.svg)

Pre-Arbitration Chargeback: What It Is, How It Works, and How Merchants Can Fight & Win Them

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

A pre-arbitration chargeback is a bank-to-bank escalation filed after you win a representment, and it is the last stop before binding arbitration, where the loser pays fees that reach $600 on Visa. The process differs by network: Visa runs two workflows under VCR where "pre-arbitration" means different things, while Mastercard replaced its old "second chargeback" stage between 2018 and 2020. Once you have put your strongest evidence into the representment, most pre-arbitrations are hard to win unless the issuer's filing raises a new claim you can specifically disprove, so screen cases by evidence first and cost second.

One notable reason many merchants write off chargebacks as the cost of sales is that winning a dispute doesn't always end the chargeback process. If the issuing bank rejects your representment, it can file a pre-arbitration case. This bank-to-bank challenge reopens the dispute and puts the recovered funds back in play. Pre-arbitration chargeback is the last stop before arbitration, where the card network issues a binding ruling and the losing party absorbs fees that can reach $600 under Visa's current schedule.

Chargeback pre-arbitration also works differently on the various card networks. Visa splits disputes into two workflows, where "pre-arb" can mean entirely different things. Mastercard scrapped its old "second chargeback" model in 2020 and rebuilt the stage from scratch. And while the networks advertise 30-day response windows, your acquirer's internal deadlines can cut that to ten.

This guide breaks down both processes, the real timelines and fees, and a simple framework for deciding when to fight a pre-arbitration case. You’ll also learn when accepting it may be the smarter financial call.

What is Pre-Arbitration Chargeback and Why Do They Happen?

A chargeback pre-arbitration, generally called a pre-arbitration chargeback, is a formal challenge filed after the representment dispute stage, when one party, usually the cardholder’s issuing bank, refuses to accept the dispute outcome.

Pre-arbitration in chargebacks is a bank-to-bank action. The issuer files pre-arbitration chargebacks against the acquirer, and the disputed funds are clawed back from the merchant’s account, like in the first chargeback.

Chargeback pre-arbitration usually happens because the merchant won the representment, and the issuer is contesting that win. The reason? Generally because they or the cardholder produced new information. It can equally be that a processing or chargeback reason code error surfaced after the fact. You, the merchant, through your acquirer, then have a fixed window to either accept liability and close the case or push back and risk escalation to the card network stage.

You'll sometimes see pre-arbitration called a "second chargeback." Treat that term with caution. It loosely describes the merchant's experience of the same transaction being pulled back twice. But it's no longer objectively accurate terminology on either network. Visa handles pre-arbitration through two distinct workflows under Visa Claims Resolution, and Mastercard formally eliminated the second chargeback stage in 2020. Both are covered in detail below.

How Pre-Arbitration Chargebacks Work

Before we get into how pre-arbitration in chargebacks works, it’s worth examining the origin of the concept itself, as it lays a clear foundation for the merits and how to navigate the process.

Pre-arbitration only exists because chargebacks exist. And chargebacks are a US consumer protection law: the Fair Credit Billing Act of 1974. The card networks then had to craft operating rules for what happens when banks disagree about who eats the loss.

Chargeback arbitration has long been the card networks’ internal court for bank-initiated disputes. Pre-arbitration emerged as the formalized buffer stage, a designated attempt at bank-to-bank resolution before paying the network to referee. The version merchants navigate today dates only to Visa's 2018 VCR overhaul and Mastercard's 2018–2020 restructuring.

How Pre-Arbs Work on The Card Networks

While the linguistics may have splintered, the underlying mechanics of pre-arbs haven’t. Whether a case arrives as a Visa Collaboration pre-arbitration, a Visa Allocation challenge, or a Mastercard pre-arbitration filing, the case follows the same essential shape. One side formally rejects the current outcome, the money moves, and the other side faces a deadline and a decision.

If you understand this, the network-specific rules in the next two sections become variations on a theme rather than two separate systems to memorize.

Here's the pre-arb lifecycle:

Phase 1: One party files a challenge. In most cases, this is the cardholder's issuing bank rejecting a representment the merchant won, stating why the outcome shouldn't stand, and usually attaching new or supplemental evidence. The notable exception is Visa's Allocation workflow. Here, liability is assigned automatically, and it's the merchant's side that files the pre-arbitration attempt to contest it. Either way, the defining feature holds. Pre-arbitration is initiated between banks, not by the cardholder directly.

Phase 2: Funds move, again. The disputed amount you recovered at representment is withdrawn or provisionally reversed while the case is open. This is the moment that earned pre-arbitration its "second chargeback" nickname. From the merchants’ cash-flow perspective, the same transaction is being clawed back twice, even if the rulebooks no longer use the term.

Phase 3: You are notified through your acquirer and given a response window. Pre-arbitration chargeback response time limits are nominally 30 days on both networks. However, acquirers impose shorter internal deadlines to allow themselves processing time, often leaving merchants ten days or less in practice.

Phase 4: The merchant decides: accept or fight. Accepting liability closes the case. The chargeback stands, and no further fees accrue. Contesting requires a rebuttal that directly addresses the issuer's new claims. Resubmitting the original representment package rarely works. The networks have already seen that evidence, and the issuer has already explained why they think it falls short.

Phase 5: Resolution or escalation. If the filing party isn't satisfied with the response, either side can escalate to arbitration, where the card network itself rules, and the losing party absorbs the fees.

Two Realities That Shape Every Pre-Arbitration Decision:

First, the evidence bar rises at each stage. Anything you held back from is now nearly worthless. The networks expect your strongest case upfront. And in arbitration, Visa explicitly bars members from submitting documentation that wasn't previously shared with the opposing side. Second, the economics shift against fighting: win rates drop under increased scrutiny while potential costs climb. That's why the accept-or-fight decision deserves actual math, not reflex. We'll build that framework in the strategy section.

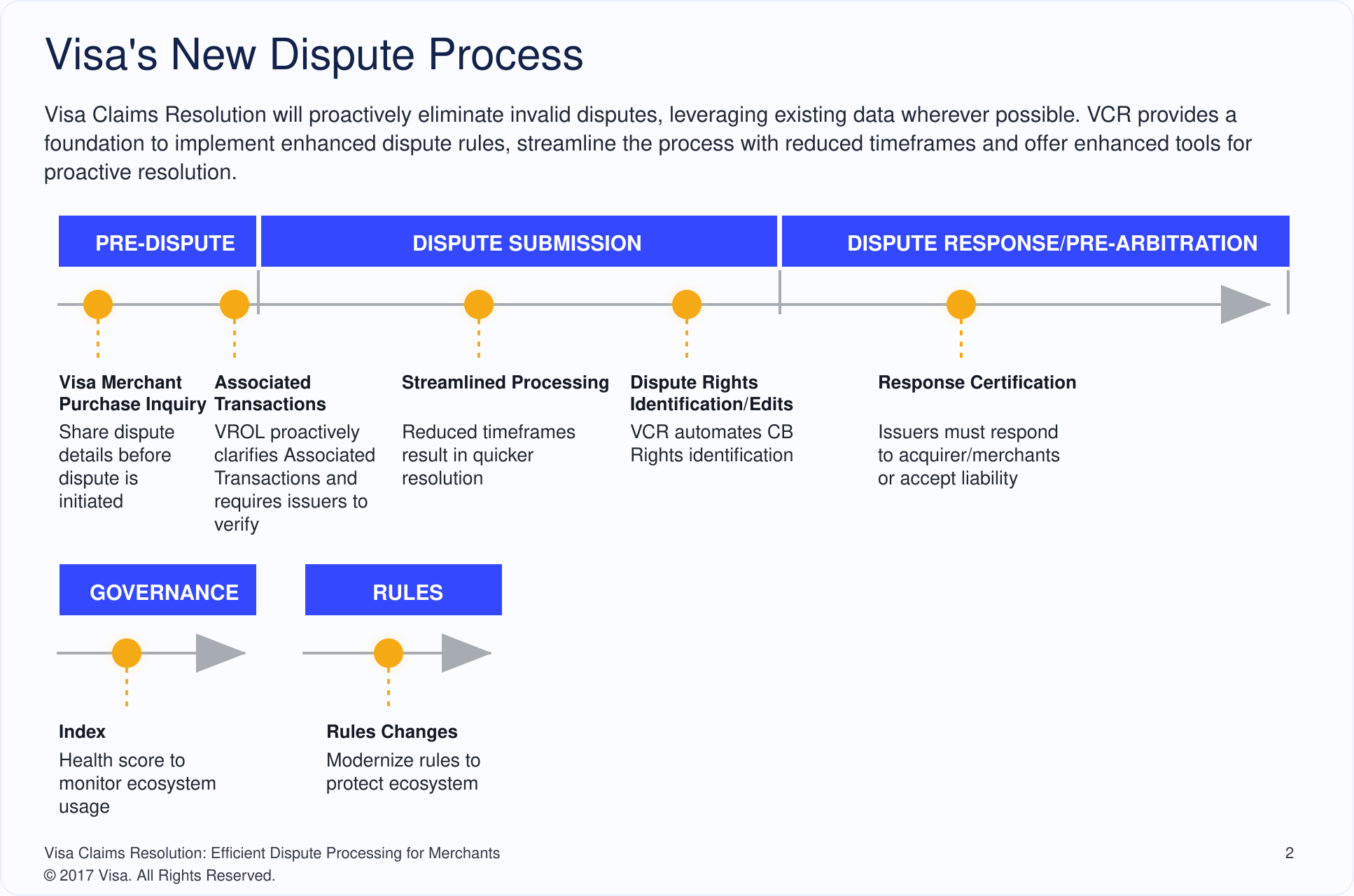

The Visa Pre-Arbitration Process

Everything about Visa pre-arbitration depends on which workflow the dispute entered under Visa Claims Resolution. Visa sorts every dispute into one of two tracks based on its reason code, and “pre-arbitration” works differently in each.

The Allocation Workflow (Fraud and Authorization Disputes, Reason Codes 10.x and 11.x)

The Allocation workflow is automated. Visa systems assign chargeback liability without requiring transaction representment. Here’s how it works in plain sequence:

Step 1: The dispute type determines the track. When a cardholder claims fraud or an authorization error, the dispute enters Allocation. These are considered "clear-cut" chargeback categories where Visa believes its own data can decide who's at fault without a debate.

Step 2: Visa runs gatekeeper checks. Before the dispute proceeds further, Visa's system automatically screens it. Was the transaction 3-D Secure authenticated? Has it already been refunded? Was the dispute filed too late? If any of those is true, Visa blocks the dispute immediately; you don’t get to see it. This filters out invalid disputes.

Step 3: If the dispute survives the checks, Visa assigns a liability rule. No human weighs evidence. The system applies Visa's liability rules to the transaction data and decides who pays, and in surviving fraud disputes, that's usually the merchant. The funds are pulled. Nobody asks you for evidence. In the Collaboration track, you'd now submit a dispute response, and the issuer would consider it. In Allocation, that stage simply doesn't exist.

Step 4: Your only fightback is labeled "pre-arbitration." Because Visa already issued a decision in step 3, the stage where merchants usually argue their case does not exist here. So your opening move is the pre-arbitration response, and it carries late-stage rules: narrow grounds for challenge, filing fees, and arbitration as the only next step.

Step 5: The issuer accepts, or the case escalates. The issuer has 30 days to accept your challenge, which returns the funds, or to let it lapse and stand firm. If they stand firm, your only remaining move is arbitration, with its $600 loser-pays fee.

The Collaboration Workflow (Processing Errors And Consumer Disputes, Reason Codes 12.X And 13.X).

As the name implies, the Visa Collaboration track invites merchants’ participation in dispute resolution. It works the way most merchants picture disputes.

You submit a dispute response within 30 days. If the issuer rejects it, they file a pre-arbitration within 30 days of the designated processing date, typically armed with new cardholder information. You then have 30 days to accept liability or submit a rebuttal.

Visa also imposes additional regional requirements. In Europe, for instance, issuers must certify that they contacted the cardholder to review the evidence before pursuing pre-arbitration.

The time limits are uniform. Each phase gives you 30 days, except escalation to arbitration, which either party must file within just 10 days of the pre-arbitration response. And those are Visa's deadlines. Your acquirer needs time to review and forward your response, so your practical window is often half the official one or less.

The fees escalate with the stakes. Pre-arbitration filing runs $25 to $50, depending on your acquirer. Since April 2025, Visa also charges a $15 fee if you let a pre-arbitration expire rather than formally accepting it, so even walking away from a case requires action.

Check whether your payment provider auto-accepts expiring pre-arbitrations on your behalf or leaves that step to you. This guide gives a detailed overview of the Visa chargeback process.

The Mastercard Pre-Arbitration Process

Mastercard’s current Dispute Resolution Initiative, implemented in phases from October 2018 to July 2020, eliminated the old “second chargeback” cycle and introduced a structured pre-arbitration stage. This is similar to Visa's reformed process.

The workflow runs in four stages, managed through Mastercom, Mastercard's dispute platform:

- Chargeback. The issuer files the dispute, and you have 45 days from the notification date to respond.

- Second presentment. This is your representment and your strongest position in the entire cycle. Every stage after this narrows your odds and raises your costs, so your most complete evidence belongs here, not held in reserve. Note that Mastercard imposes strict size limits on evidence packages (18 pages and 10MB total), so the goal is a focused case, not an exhaustive one.

- Pre-arbitration. If the issuer rejects your second presentment, they have 45 calendar days from its settlement date to file a pre-arbitration case explaining why your evidence falls short. You then have 30 days to accept liability or rebut it. Two caveats: under current rules, pre-arbitration isn't available for authorization and chip liability shift disputes (reason codes 4808, 4870, and 4871), and the issuer isn't obligated to stop here. In some circumstances, they can escalate a dispute directly to arbitration.

- Arbitration. Unresolved cases escalate to Mastercard's Dispute Resolution Management team for a binding ruling. The losing party pays the arbitration fees, and Mastercard can add non-compliance fees for any rule violations its review uncovers. A single arbitration loss can erase the gains from dozens of won disputes.

Two Practical Warnings:

First, the acquirer-buffer problem applies to Mastercard as it does everywhere. The official 30- and 45-day windows compress sharply once your acquirer's internal deadlines are factored in, so plan your evidence gathering as if you have about 10 days. Second, treat your pre-arbitration rebuttal as your last realistic chance to shape the case.

Pre-Arbitration vs. Arbitration: Understanding the Key Differences

The terms are often used interchangeably, but they describe two structurally different proceedings. Pre-arbitration is a negotiation between banks. The filing party makes its case, the responding party decides whether to accept or push back, and the card network watches from the sidelines. Arbitration is a judgment. The network itself reviews the file and issues a binding ruling, with real money attached to losing.

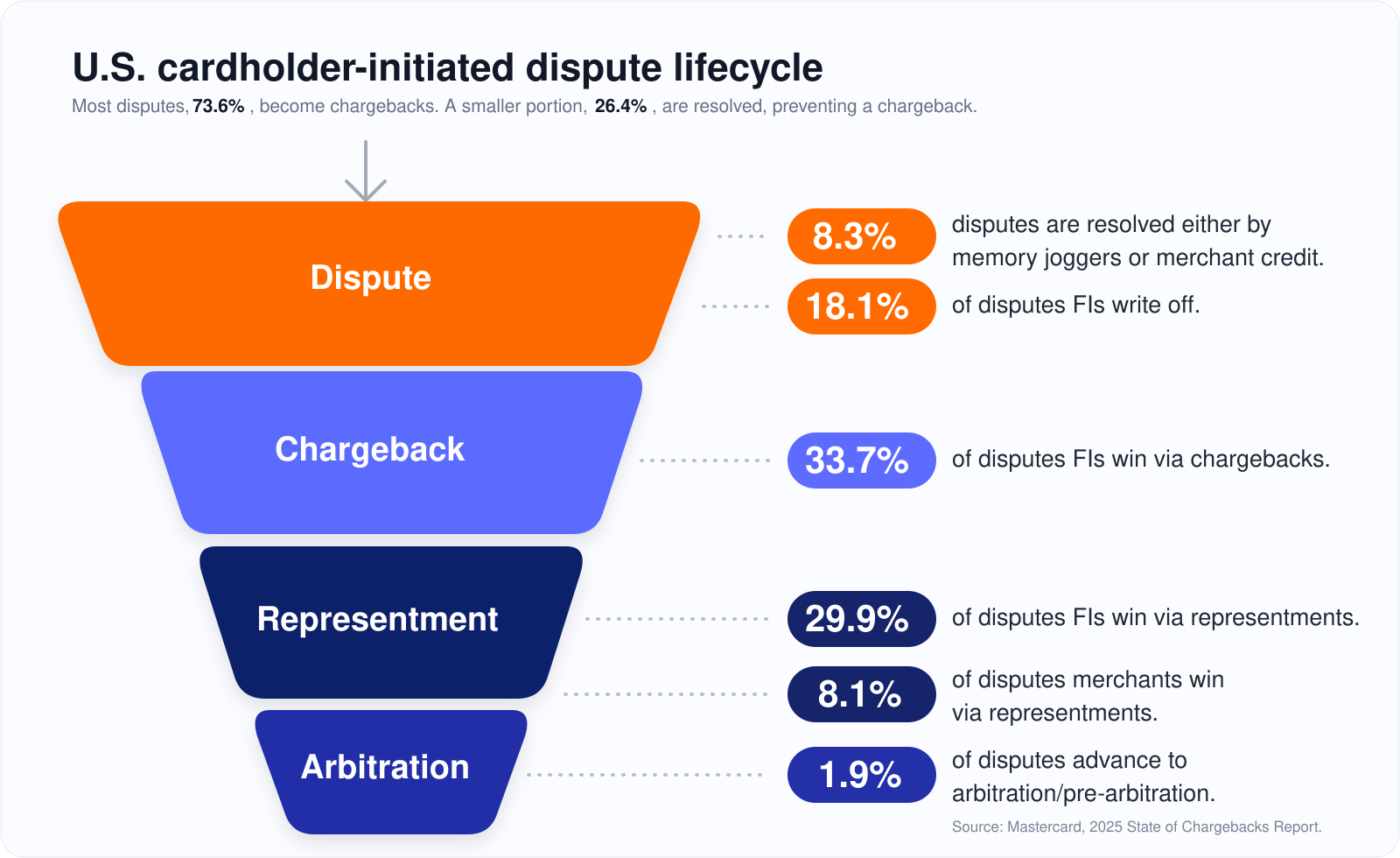

The pattern in that table is the one to internalize: every column shifts against you at arbitration. Costs go from fixed to loser-pays. Evidence goes from open to closed. Your ability to exit cheaply disappears. That’s by design. The networks price arbitration to discourage it, and the pricing works: only an estimated 2% of chargebacks ever reach the arbitration stage, according to industry data.

This is why the pre-arbitration response is the real decision point of the entire dispute. At pre-arb, you still control your downside; accepting liability caps your loss at the disputed amount and fees already paid. The moment you contest, and the case escalates, your downside compounds. You incur the disputed amount, the arbitration fee, and any compliance penalties the network’s review turns up. For a $200 chargeback, fighting into Visa arbitration means risking roughly $800 to recover $200. Such odds only make sense with strong evidence and a high-value transaction.

Another constraint many merchants discover too late is that the choice may not be yours. Some payment service providers, including Stripe, don’t permit their merchants to enter arbitration at all. If the issuer rejects your representment, the case simply ends there. If you process high-ticket transactions, this is worth checking before you need it, not after.

Developing an Effective Pre-Arbitration Chargeback Strategy

Many merchants treat pre-arbitration as a “fold-fast” stage. They believe the correct move is to concede quickly rather than keep spending to fight. But that’s not always the right move. Building a pre-arb strategy enables you to channel your efforts where they actually move the outcome.

Here’s how to actualize that objective.

1. Apply an Evidentiary Test Before a Cost Calculation

If you have already put your strongest evidence into the representment, most pre-arbitrations are difficult to win. Why? First, your strongest evidence belongs in the representment, because arbitration is decided primarily on the existing file. Second, issuers usually file a pre-arbitration claim on one of two grounds:

- New information the cardholder supplied after losing the representment, or

- A claimed processing or technical error in how the dispute was handled.

So before you contest, ask whether the filing gives you something to factually defeat:

- A new cardholder claim you can specifically disprove with evidence you could not legitimately have submitted before, or

- A procedural error you can show did not occur.

If the filing only restates the original dispute reason and you have already submitted your best evidence, you have nothing new to add. Contesting it is paying to lose more slowly.

2. Treat Pre-Arbitration Claims As Evidence That Your Odds Have Dropped

The issuer spent its own resources to reject a representment you had already won. Banks do not generally do that in cases they expect to lose. So the instinct to think “I already won once, so I am likely to win again” is practically backwards at this stage. It makes you lose sight of pertinent details.

3. Use Representment to Make Pre-Arbs Unnecessary

Because the decisive evidence must be in the file early, the highest-leverage work happens before any pre-arbitration arrives. The strongest tool here is Visa’s Compelling Evidence 3.0. But it has real requirements. It uses two prior undisputed transactions, with Visa matching the underlying card number to confirm the cardholder pairing. And it must be configured through your acquirer in advance. Setting this up before disputes occur is worth more than any rebuttal you can write without one.

4. Audit How Your Acquirer and Processor Handle Pre-Arbitration

Your payment provider sits between you and the issuer, and its policies shape outcomes in two ways. The first is handling. Some acquirers assemble and strengthen the representment themselves. Others simply forward whatever you submit without adding to it. So, identical evidence can reach the issuer in a stronger or weaker shape depending on who handles it.

They also set internal deadlines well inside the network's nominal window, which is why your real response time is often around 10 days rather than the published 30. And because non-response counts as acceptance by default, a case can be lost to a missed internal cutoff without anyone deciding to concede it.

The second is escalation. Some providers, Stripe among them, do not permit merchants to enter arbitration at all. This means a rejected representment simply ends the case. If that is your setup, everything above collapses onto getting the representment right. Neither of these is fixed. Before you are mid-dispute, confirm how your provider handles representment and pre-arbitration, what their true internal deadline is, and whether they allow arbitration at all.

That brings us to the last section of this guide.

Preventing Revenue Loss From Pre-Arbitration Chargebacks

A lost chargeback is never just the disputed amount. It arrives as a stack: the refunded or forfeited transaction, the dispute fee, the analyst hours spent responding, and other ancillary costs.

What separates prevention from every stage covered so far is which parts of that stack it can effectively remove. Fighting a pre-arbitration, at best, contains the damage. Acting upstream is the only point at which the fee, wasted hours, escalation risk, and the ratio damage are voided rather than merely recovered or absorbed. The levers below, all measurable and within your control, are where that happens.

Stop High-Risk Orders Before They Ship

A significant number of disputes that eventually escalate are predictable at the point of sale. Screening transactions after authorization but before fulfillment lets you cancel or hold orders most likely to turn into disputes. This is the role Chargeflow Prevent is built for. It analyzes orders post-transaction and pre-fulfillment, flags high-probability disputes including friendly fraud, and lets you hold or cancel them before they ship.

If your worst reason codes cluster around specific products, buyers, or traffic sources, screening at this stage is non-negotiable. It attacks the problem where it starts, rather than after it has become a chargeback.

Deflect Disputes That Do Start. Deflected Dispute Never Reaches Pre-Arb

This is your highest-leverage lever, and the reason is verifiable. Disputes resolved through Rapid Dispute Resolution are excluded from the VAMP ratio entirely. Pre-dispute alerts from Verifi and Ethoca let you refund a transaction in the 24 to 72-hour window before it becomes a formal chargeback. Chargeflow Alerts operates this timeline for you. It pulls real-time notifications from those networks and issues the refund automatically before the chargeback posts, on a model where you pay only for chargebacks actually prevented.

Be honest about the trade. A deflected dispute still costs you the refunded amount. But it saves the chargeback fee, the analyst time, the escalation risk, and the damage to the ratio that ultimately endangers your account. For low-value disputes, where the cost of the count is more than the dollar, that trade is almost always worth taking.

The Cheapest Pre-Arbitration is the One Never Filed

A representment strong enough to satisfy the issuer ends the dispute before pre-arbitration is possible. The infrastructure move is Compelling Evidence 3.0. You can build the evidence packages organically. Or use the more excellent strategy of automated chargeback service to assemble and submit them. The principle is the same regardless. Your strongest, most complete case belongs in the first response, not held in reserve for a stage where new evidence is nearly worthless.

Wrapping Up

Chargeback pre-arbitration is a symptom, not the disease. The disputes that reach it were preventable before fulfillment, deflectable before they posted, winnable at representment, or not worth fighting at all.

A merchant who screens risky orders early, deflects what slips through, represents well, and concedes the rest quickly will face fewer chargeback pre-arbitrations, spend less on the ones that arrive, and protect the ratio that protects the account. The full-funnel logic is the point. Stop what you can at the source, deflect what you cannot, and reserve the fight for cases you can actually win.

If you're managing that funnel by hand, the operational cost adds up faster than the disputes do. Chargeflow is built to run the whole funnel for you. Prevent screens high-risk orders from shipping, Alerts deflects disputes in the window before they post, and the platform's AI assembles and submits representment evidence on the cases worth fighting. You pay only for chargebacks actually prevented, so the model is tied to results rather than activity. Ready to learn more? Talk to our team.

Chargeflow's own blog already ranks organically (position 5) for this exact keyword under a different URL than this chargebacks-101 page — consolidating internal links between the two avoids cannibalization and concentrates authority. No dedicated PAA answer currently dominates this SERP, so a clean, structured stage table is well positioned for AI Overview inclusion. This topic is also closely adjacent to the existing chargeback-arbitration page from batch 1; cross-linking both strengthens topical coverage.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)