%201.svg)

Bank of America Chargebacks: Everything You Should Know on How to Fight Back in 2026

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

Bank of America returns disputed funds to cardholders immediately, forcing merchants to wait 60–90+ days for representment. Visa and Mastercard use different codes and deadlines; fraud-only programs (CE 3.0, First Party Trust) help some cases but exclude many consumer and billing disputes. Prevent chargebacks with precise evidence, fast responses, and purpose-built automation to protect revenue and avoid monitoring penalties.

When a customer files a dispute, Bank of America reverses the funds from your account and credits the cardholder before you even know what’s happening. For debit cardholders, those funds are immediately available for spending. For credit cardholders, the provisional credit restores their available balance. Either way, the money is gone from your merchant account. You must wait 60 to 90 days, sometimes longer, for a representment decision.

Bank of America issues both Visa and Mastercard cards. Each network has different reason codes, dispute deadlines, and monitoring programs. A merchant can be in good standing with one network and flagged by the other simultaneously.

Since 2023, both networks have introduced programs designed to penalize chargeback abuse. Visa’s Compelling Evidence 3.0 and Mastercard's First Party Trust both allow merchants to present proof of cardholder participation. When that proof meets the threshold, the issuer absorbs the chargeback.

But both programs apply only to fraud-coded chargebacks. Consumer disputes, billing errors, and processing issues are not included. That gap is where many merchants’ chargeback losses live.

What you do now, before the next chargeback lands on your dashboard, determines whether you recover that revenue or absorb the loss. This guide tells you exactly how.

Understanding Bank of America Chargeback (and How It Differs from a Refund)

A Bank of America chargeback is a transaction reversal decision made for you when a customer disputes a payment on their card. A refund is a voluntary decision you made directly with the customer, ideally through mutual agreement.

A refund costs you the sale. A chargeback costs you the sale, a fee, and a mark against your merchant account, regardless of whether you win. And a customer can receive your refund and still file a dispute. Bank of America may even issue provisional credit before catching it.

Who Initiates Bank of America Chargebacks?

The customer initiates a Bank of America chargeback. BofA manages the dispute process through the relevant card network.

Chargeback processes move fast due to policy requirements. For example, Regulation E mandates banks to issue provisional credit for debit disputes within 5–10 business days. Network rules govern credit. And so the speed isn’t discretionary, which means slowing it down isn’t an option. Responding correctly is.

How Much Does a Bank of America Chargeback Cost?

Bank of America typically assesses a $25–$50 non‑refundable chargeback fee per dispute. The exact amount is set in your acquirer agreement and varies by industry and risk profile. If a case proceeds to network arbitration, the losing party generally pays an additional arbitration fee that is often in the hundreds of dollars (avg. $500), depending on the card network’s current schedule. The image below shows a quick highlight of the nominal chargeback cost:

Why Bank of America Chargebacks Cost You Money Even When You Did Nothing Wrong

There are three reasons worth highlighting.

First, banks generally apply a no-fault rule to customers during transaction disputes. The burden of proof is yours entirely.

Just as a Judge is not required to act as an investigator, Bank of America is not obligated to determine whether or not the customer is telling a lie. They wait for your evidence to do that. If you submit nothing or submit the wrong documentation, the cardholder keeps the money by default.

Second, winning doesn’t necessarily make you whole. A successful representment recovers the transaction amount. While substantial, the chargeback fee is a non-recoverable loss. The dispute equally counts against your ratio.

The third aspect is that chargeback ratios compound incrementally. Most merchants rarely notice the damage until they receive a monitoring program warning from Visa or Mastercard. At this point, monthly fees begin to apply, and card acceptance becomes even riskier.

Bank of America is one of the largest card issuers in the country. A concentrated spike in BofA disputes can move your ratio faster than you expect.

Why Did I Get a Chargeback? Common Bank of America Dispute Reason Codes Explained

The reason code on your dispute notice is the legal basis for the chargeback, and it determines what evidence you must submit. Responding to a Bank of America chargeback requires precision and deep expertise. Because Visa and Mastercard use different chargeback reason codes and rules, you must stay current on both networks’ policy changes. The same customer dispute maps to different reason codes depending on the card. Your response requirements change with them.

The common Bank of America dispute reason codes are as follows:

Unauthorized Transaction/Fraud (Visa: 10.4 | Mastercard: 4837)

This is the code you get when a cardholder claims they didn’t authorize a transaction. It’s also the code most commonly used to disguise friendly fraud.

Genuine fraud (a stolen card or compromised account) is nearly impossible to win for card-not-present merchants. The liability stays with you unless you can demonstrate that the cardholder participated in the transaction.

That’s where Visa Compelling Evidence 3.0 applies. To use it, you need:

- Two prior undisputed transactions from the same cardholder, processed between 120 and 365 days before the disputed transaction.

- Across all three transactions (the two historical ones and the disputed one), at least two data elements must match, and one of those two must be either the IP address or device ID/fingerprint. The other can be a login ID or a shipping address.

Missing the 120-day floor or failing to produce the right matching elements means CE 3.0 won’t apply.

That window also explains why CE 3.0 benefits subscription and repeat-purchase merchants far more than one-time transaction businesses. If your customer base doesn’t generate a transaction history with your store, you have nothing to draw from.

What helps outside of CE 3.0:

- AVS match, CVV match,

- device fingerprint, IP address tied to the billing address, and

- delivery confirmation.

None of these guarantees a win, but their absence guarantees a loss.

Item Not Received (Visa: 13.1 | Mastercard: 4853)

This Bank of America chargeback category is the most winnable category if you have the right proof of delivery.

Carrier confirmation showing delivered status is the baseline. “In transit” is not enough. For high-value orders, signature confirmation is the difference between winning and losing. For digital goods, you need login records, download timestamps, and IP address information proving the cardholder accessed what they purchased.

One thing merchants consistently get wrong: Bank of America needs proof of delivery as of the dispute date, not proof that the item eventually arrived. Submitting tracking that shows the package is still in transit won’t suffice.

Not as Described or Defective (Visa: 13.3 | Mastercard: 4853)

This dispute category is harder to win because it’s inherently subjective. The cardholder argues that what they received didn’t match what you represented at the product or service listing.

Your defense lives in your product listing. Screenshots of the exact description and images the customer saw at checkout matter here. That does not mean what your website looks like today. But what it showed at the time of purchase. If your return policy is clear and the customer made no attempt to contact you or initiate a return before filing a dispute, document that too.

📍Note: Mastercard uses 4853 for both not received and not as described. The subtype within the dispute notice tells you which claim you’re actually defending against.

Billing Errors: Wrong Amount or Duplicate Charge (Visa: 12.5 (incorrect amount), 12.6 (duplicate) | Mastercard: 4834)

If it’s a genuine error, don’t fight it. Correct it and move on. A merchant who disputes a legitimate billing error and loses pays a fee on top of the refund.

If it’s not an error, you need your authorization records and settlement data showing the amounts and timestamps.

For duplicate charge claims, you need to demonstrate that the two transactions were distinct. Documentation showing different order numbers, different items, or confirmation that the customer authorized both separately is ideal. Two charges of the same amount on the same day for the same customer look like a system error until you prove otherwise.

Credit Not Processed After a Return (Visa: 13.6 | Mastercard: 4853; formerly 4860)

Mastercard retired the standalone reason code 4860 and folded it into 4853. If this code still appears on your dashboard, it’s from a legacy system, but the chargeback is still valid and must be responded to. Treat it like a 4853 Credit Not Processed subtype.

Timing is where some merchants lose this dispute. You may have already processed the refund, but it hadn’t been posted when the dispute was filed.

Your first move should be to check whether the refund was issued before or after the dispute date. If it was issued before and hadn’t been posted, submit the refund confirmation with the processing timestamp. If the customer filed before giving you a reasonable window to act, document your return policy, the return receipt or RMA confirmation, and the refund processing date.

If no refund was due because the item was never returned, say so. And include your policy alongside any communication showing the customer didn’t follow the return process.

How Long Do I Have to Respond to a Bank of America Chargeback?

Merchants must respond and provide evidence within 30 days for Visa transactions and 45 days for Mastercard transactions. Those are the network-set limits. But they are not the limits you should be managing against.

Why? The deadline is measured from the day the chargeback was filed. For Visa, the clock starts the day after the chargeback processing date, which may be several days before the merchant receives notification. By the time a dispute reaches your inbox after it’s been reviewed by your processor, you may have already lost a portion of your window.

Acquirers and processors impose their own internal deadlines on top of network rules. In some instances, merchants have only 5 to 10 days to respond. When an acquirer’s deadline and the network’s deadline conflict, the shorter deadline is always the real time limit.

Treat every chargeback notification as urgent, regardless of when the network deadline technically falls.

What Happens If You Miss the Deadline

Failing to respond to a dispute within the given time limit results in a loss by default. You’ll absorb the transaction loss, the standard chargeback fee, and a non-response penalty on a dispute you might have won.

Missing a deadline is the most avoidable way to lose a chargeback, as the window cannot be reopened. The only time you can choose not to respond is when the dispute isn’t worth fighting.

Retrieval Requests: What They Are and When They Apply

A retrieval request is a pre-chargeback information request that applies to specific card networks, not all of them.

At Bank of America, retrieval requests are also called inquiries. They apply specifically to Discover and American Express transactions. If you don’t reply, don’t reply on time, or don’t supply all the requested information, Discover and American Express will automatically file a chargeback, and your chargeback response rights may be revoked.

The deadline to respond to a retrieval request is typically 10 to 20 days after the original request is sent. If you don’t respond within that window, you will almost always receive a chargeback and will have effectively forfeited your right to fight it.

For Visa and Mastercard transactions through Bank of America, the first official notice you receive will be the chargeback itself. There is no retrieval request stage.

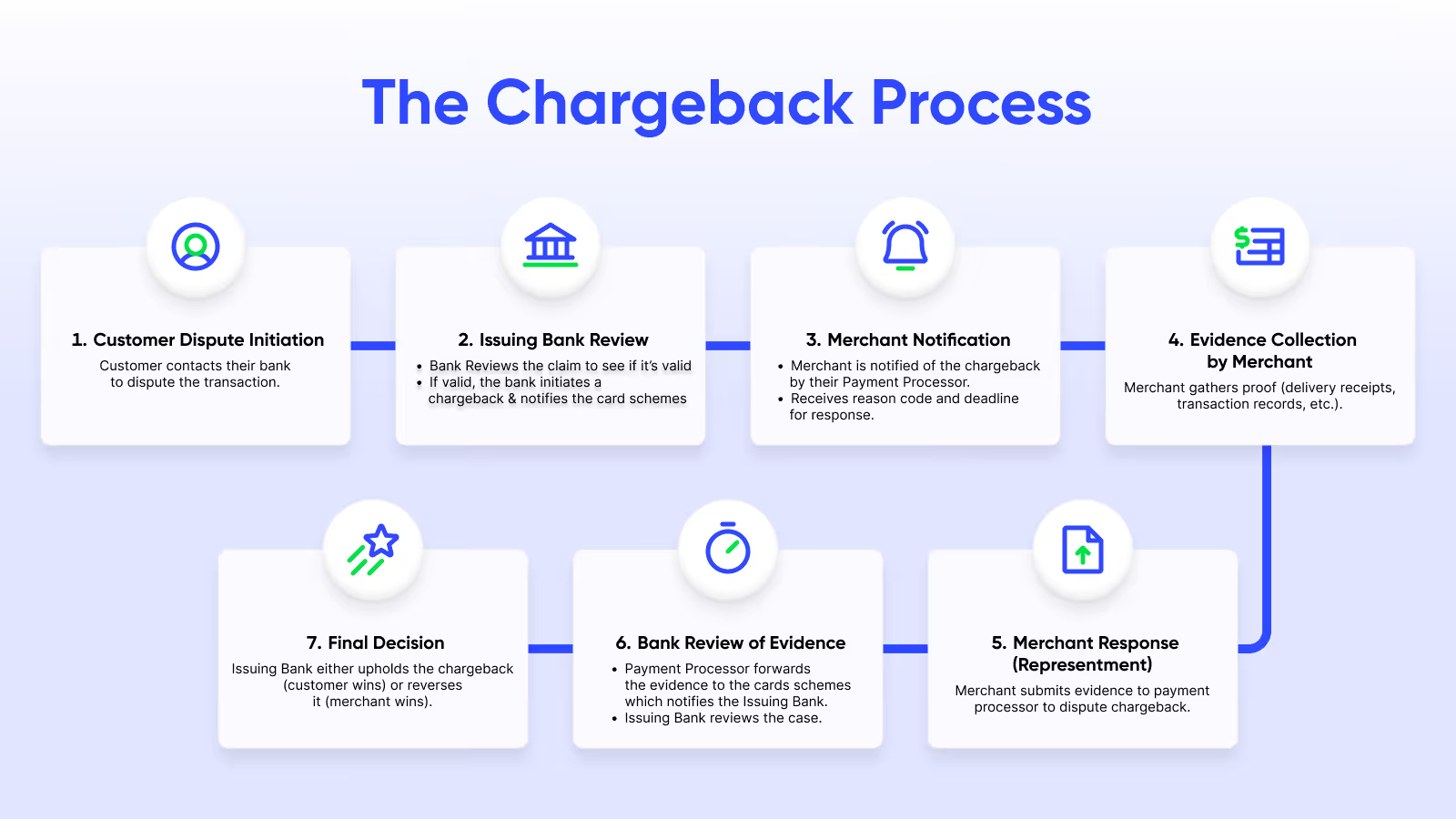

How Do I Fight a Bank of America Chargeback?

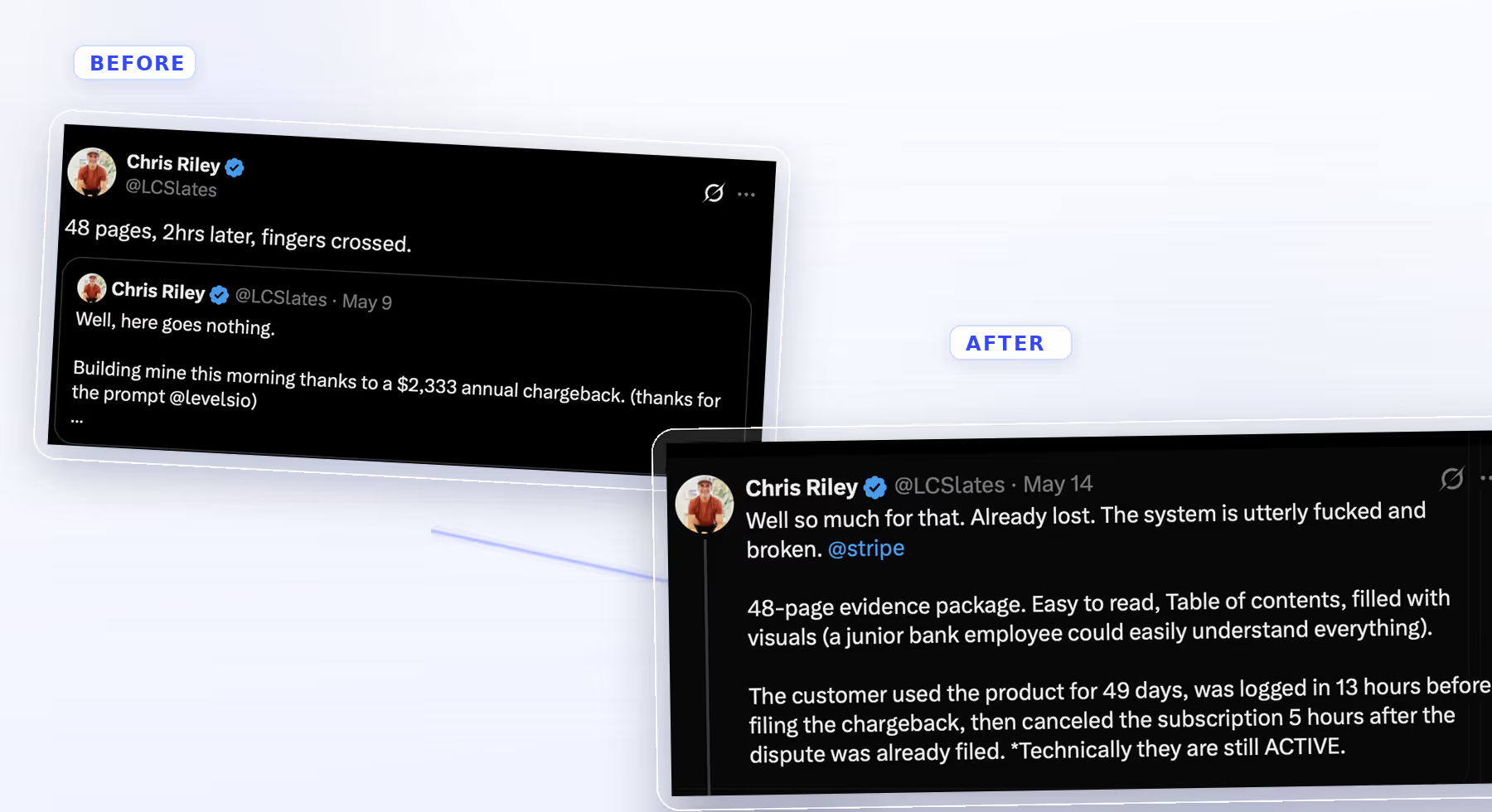

X user Chris Riley spent two hours vibe-coding his case.

Forty-eight pages of evidence generated. Documentation compiled carefully, submitted on time, against a $2,333 chargeback. He did everything his LLM told him a merchant is supposed to do.

He still lost. The screenshot below shows his frustration:

Riley's experience isn't a story about bad luck. It's a precise illustration of how the chargeback system works, and why manual effort on its own, or using outputs from a generic LLM, is not a defense strategy.

The issue was never the volume of his documentation. The chargeback system doesn't reward effort. It rewards technical precision. This means:

- the right evidence,

- matched to the right reason code standard,

- formatted correctly,

- making the right legal argument under the network rules that govern that specific dispute.

Forty-eight pages of the wrong thing, or the right thing, organized the wrong way loses the same as no response at all.

Bank of America’s own research puts it plainly: “Chargebacks, many attributable to fraud, can mean hefty fees, lost merchandise and increased overhead.” Their guidance to merchants goes further: “Many large corporations already use automated response tools matched with customer details, and this kind of automation based on intelligent actioning is where the industry is headed.”

The industry has already moved. The question is whether your business has.

That’s where automated chargeback management platforms like Chargeflow become operationally relevant. Not as a convenience, but as the structural solution to a process that manual effort and generic AI tools consistently fail.

How Chargeback Automation Wins Chargeback Disputes

The gap between losing a dispute like Riley did and winning it consistently is infrastructure. Here’s what that infrastructure does at each stage of the fight:

Reason Code Identification and Evidence Mapping

Every dispute that enters Chargeflow’s system is matched against the network rules governing that specific reason code. That’s purpose-built precision, not a generic evidence checklist. You get the exact evidentiary standard Visa or Mastercard requires for that code.

A 10.4 fraud dispute gets a CE 3.0 eligibility check and prior transaction matching. A 13.3 not-as-described dispute gets product description documentation and return policy evidence. The mapping is automatic. The margin for mismatch is eliminated.

Rebuttal Letters Built to Network Standards, Not Templates

The rebuttal letter is the legal argument. It is structured to address the specific claim under the relevant network rules, not a repurposed template that sounds thorough but argues the wrong thing. This is where most manual and LLM-generated responses fail.

A general-purpose LLM can construct an argument. Chargeflow constructs the argument that the network's own outcome data shows wins. It's trained exclusively on chargeback outcomes, current network rule versions, and the evidence patterns that actually reverse decisions.

Think of it as the difference between a lawyer who studied contract law and one who has tried thousands of cases under the specific clause being contested.

CE 3.0 Data Infrastructure

Winning fraud-coded Visa disputes under CE 3.0 requires distinct transaction documentation, as highlighted earlier. If that data doesn’t exist, CE 3.0 cannot be used retroactively. Chargeflow builds and maintains that data infrastructure continuously. Qualifying evidence exists when a dispute arises rather than after.

Simultaneous Deadline Management Across Every Dispute

Tracking 30-day Visa and 45-day Mastercard windows at volume, individually, is where merchants lose winnable cases. Chargeflow monitors every deadline across every open dispute, removing the single most avoidable failure point in manual chargeback management. A unified dashboard shows every detail. You don’t need to manage disconnected platforms for one store.

Decision Logic on When to Fight and When to Accept

Because of low win rates and the fees involved, it can sometimes make more sense to pick your battles. Automation applies that logic at scale. It evaluates each dispute against win probability, transaction value, and fee exposure before committing resources to a representment. The disputes worth fighting get fought. The ones that aren’t don’t consume time they don’t deserve.

The result? A higher win rate. But also, a chargeback operation that doesn’t depend on someone knowing the difference between Visa 13.1 and Mastercard 4853, or remembering that this week’s deadline is tighter than last week’s. The system handles the precision. You handle the business.

What Is a Chargeback Ratio and Why Does Mine Matter?

Your chargeback ratio is the metric that determines whether card networks treat you as a normal merchant or a problem to be managed.

The calculation is straightforward. For Mastercard, the formula is: chargebacks received in the current month divided by total transactions processed in the previous month, multiplied by 100. Visa calculates it with the same strategy but against current-month transactions.

The one-month lag in Mastercard’s formula means a spike in disputes this month is measured against last month’s sales volume. This can make your ratio look worse than expected during a slow period.

The Acceptable Chargeback Thresholds, And Why the Numbers You’ve Heard May Be Wrong

The figures most commonly cited, Visa’s 0.9% and Mastercard’s 1%, are outdated. Both programs have changed significantly.

In August 2024, Visa announced a new program consolidating its fraud and dispute monitoring programs into a single unified framework called VAMP, which took effect in April 2025. Under VAMP, the ratio now includes TC40 fraud reports plus all non-fraud disputes divided by total transactions. This is a materially broader calculation than the old VDMP, which tracked disputes alone.

The VAMP excessive threshold is currently 2.2% globally, dropped to 1.5% for North America, the EU, and the Asia Pacific from April 1, 2026. Under the old calculation, a merchant with 70 fraud disputes and 10 non-fraud disputes out of 10,000 transactions had a 0.8% ratio, just below the old threshold. Under VAMP, the same merchant calculates at 1.5%, already at the new limit.

On the Mastercard side, the Excessive Chargeback Program no longer identifies merchants at the old 1.0% threshold, which was retired in April 2020. The current ECM designation is triggered when a merchant reaches at least 100 chargebacks in a month and a ratio between 1.5% and 2.99%. HECM or High Excessive Chargeback Merchant is triggered at 300 or more chargebacks and a ratio of 3% or above.

Both conditions, count and ratio, must be met. A low-volume merchant with a high percentage won’t be flagged. A high-volume merchant with a low ratio won’t either. But cross both simultaneously, and the program is automatic.

What Happens When You Cross Bank of America's chargeback threshold

The consequences escalate in stages, and they move faster than most merchants expect.

For Visa under VAMP, fees for excessive merchants run between $5 and $10 per fraudulent or disputed charge. Visa requires a remediation plan within 15 days of program placement, and exiting VAMP requires three consecutive months under the threshold.

Mastercard’s consequences are steeper. ECM merchants face monthly fines that escalate the longer they remain in the program. HECM merchants face monthly fines between $1,000 and $200,000, their Merchant ID is flagged for heightened scrutiny, and acquirers often terminate excessive merchants at that level. HECM status also carries a high likelihood of MATCH list placement, an industry-wide processing ban.

The MATCH list is effectively a death penalty for a business. Once listed, finding a new acquiring bank becomes nearly impossible.

Beyond network fines, acquirers often raise processing fees, demand reserves, or impose stricter contract terms on merchants with excessive chargebacks. This is independent of any network-level action.

How Do I Stop Bank of America Chargebacks Before They Happen?

The most detrimental aspect of chargeback ratio calculations is that win rates from representment do not factor into the ratio at all. The only way to keep a chargeback rate below the threshold is to prevent chargebacks before they happen.

What You Control

Your billing descriptor should match what the customer remembers buying, not your parent company or processor’s name. Your return policy should be easier to find than your bank’s phone number. Delivery confirmation belongs to every order. And any shipping delay, backorder, or subscription renewal should trigger a proactive email. A customer who hears from you first doesn’t always go back and call their bank.

What Technology Controls

When a Bank of America cardholder initiates a dispute, an alert is generated through the card network before the chargeback is formally processed. That window, usually less than 24 hours, is where most chargebacks can be stopped without them registering on your ratio.

Chargeflow Alerts uses Verifi, Ethoca, and the Chargeflow Network to automatically match dispute alerts to transactions and issue refunds before the chargeback stage. With that, you can comfortably deflect up to 90% of incoming chargebacks.

You’re billed only for prevented chargebacks, not alerts received. And duplicate alerts for the same transaction are filtered automatically. If your dispute rate trends toward a card network monitoring program, you also get notified before the fines begin.

For friendly fraud specifically, Chargeflow Prevent identifies abusive customers and repeat dispute filers in real time, before the next order ships.

Every deflected chargeback saves the transaction amount, the fee, and the ratio impact of a dispute that never officially existed.

Conclusion

Bank of America chargebacks don't discriminate between merchants. The process moves fast, the burden is yours, and the costs compound in ways that don't show up on a single invoice.

The merchants who are getting ahead, facing down rising dispute volumes, have built an infrastructure. They have crafted a system that harnesses the right evidence, matched to the right standard, submitted before the right deadline, consistently, across every dispute.

While others are submitting volumes of AI slop, the merchants who win consistently use purpose-built frameworks to automate the precision work and reserve their attention for everything else. They prevent the chargebacks that can be stopped before they register. They fight the ones that can't with technical precision rather than volume. And they track the metrics that matter before a monitoring program letter arrives.

The next chargeback is already in motion somewhere. What you've built to receive it is the only variable you control.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)