%201.svg)

Liability Shift: A 2026 Guide to Fraud Responsibility in Card Payments

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

The liability shift changed who pays for fraudulent transactions. Instead of issuers absorbing most losses, merchants became responsible when they fail to use secure payment methods like EMV chips or 3D Secure. While it reduced counterfeit fraud in physical stores, it pushed more fraud into online transactions. For merchants, a successful liability shift doesn’t eliminate risk. It changes where that risk shows up.

Fraud didn’t disappear after EMV. It moved, making card-present fraud harder and card-not-present fraud easier. The liability shift didn’t reduce fraud. It changed where it shows up and who pays for it. For merchants, that shift changed more than fraud patterns. It changed who absorbs the loss.

What Is the EMV Liability Shift?

The EMV liability rule determines which party is financially responsible when a transaction turns out to be fraudulent.

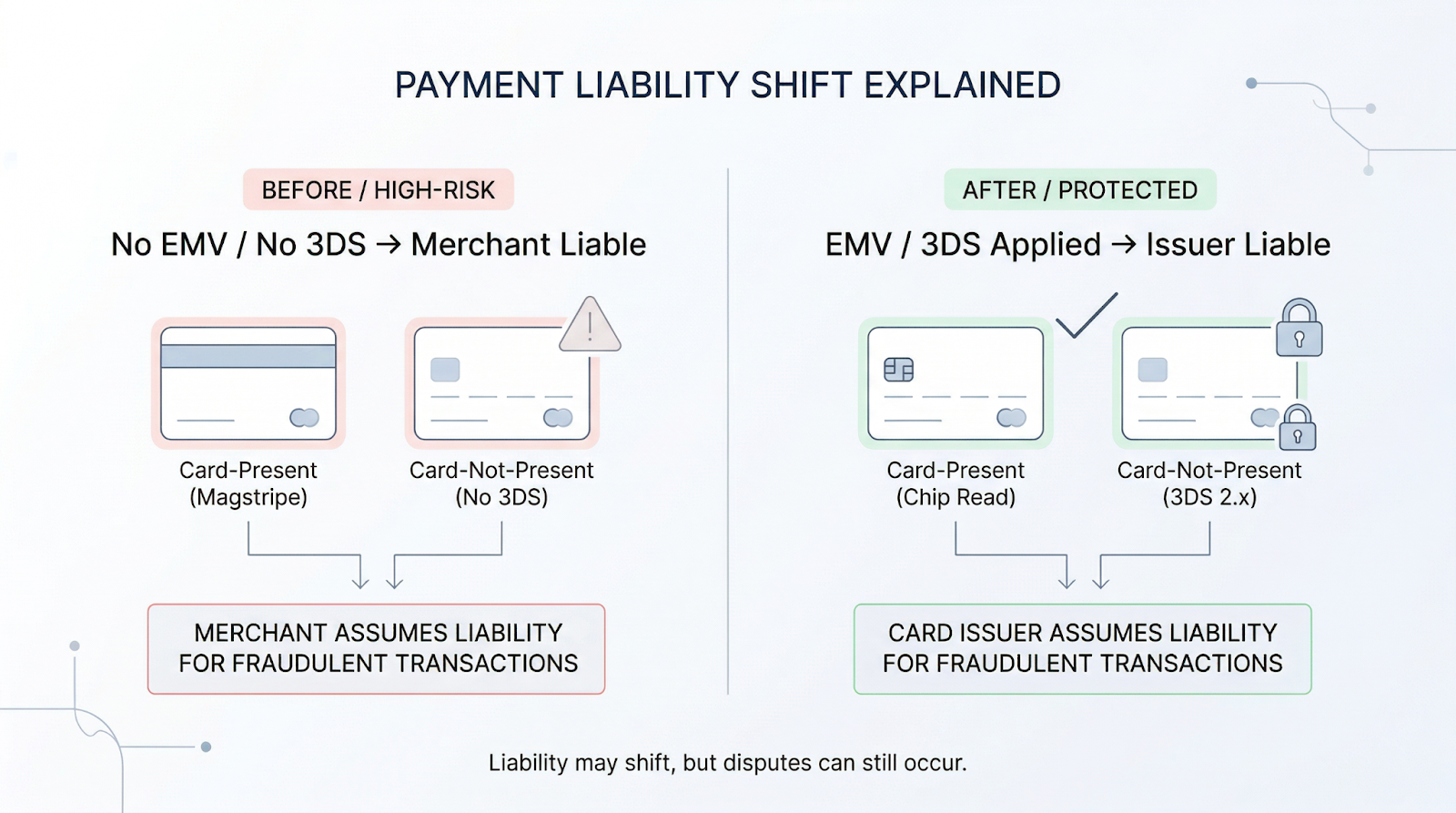

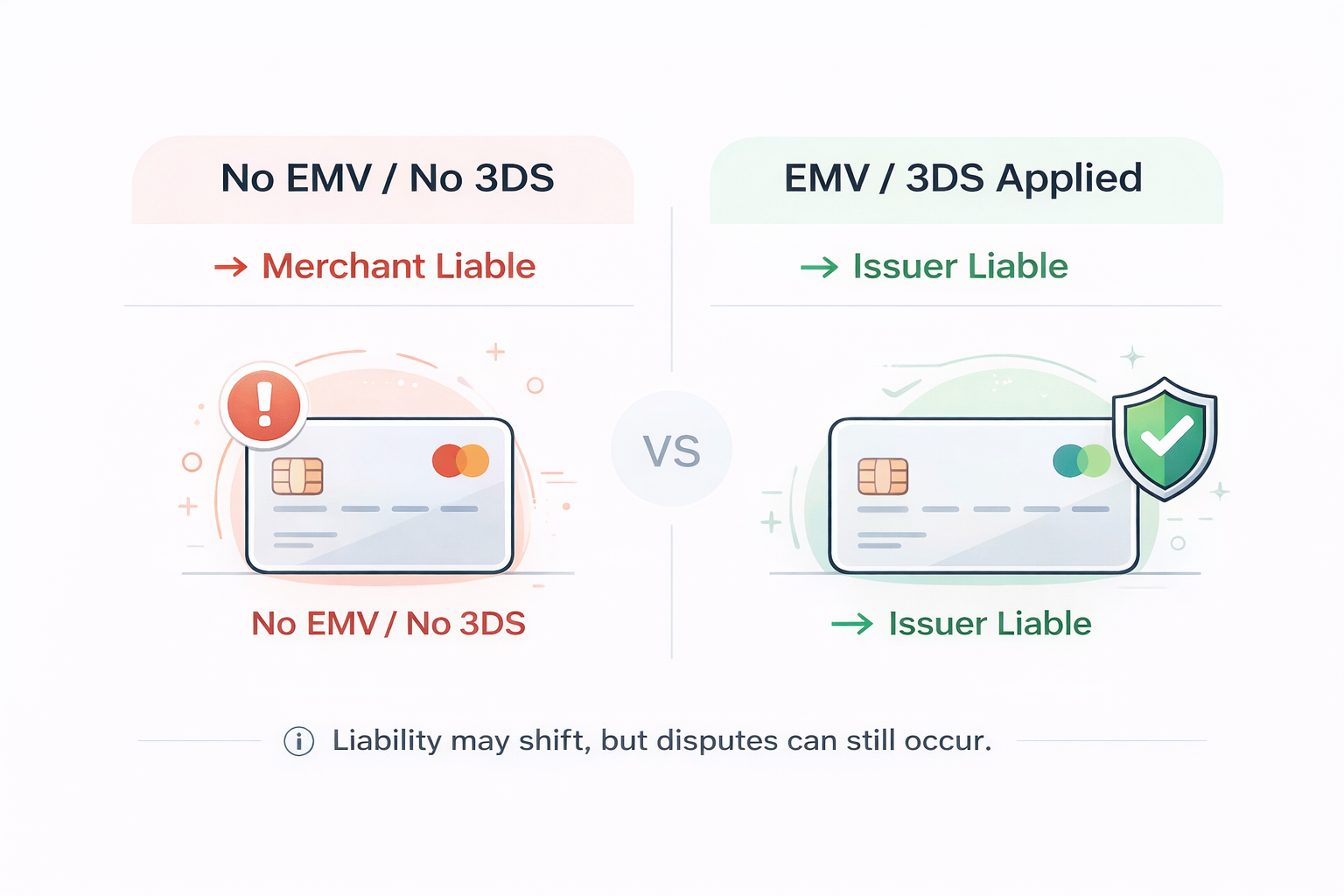

This is often referred to as a fraud liability shift, where responsibility moves based on how the transaction is authenticated. In practice, it determines which party is financially responsible when a transaction turns out to be fraudulent.

Before the adoption of EMV, issuers typically absorbed fraud losses. After the shift, liability moved to the party using less secure technology.

In practice:

- If a merchant does not support EMV chip transactions, merchant is liable

- If both sides support EMV, issuer is typically liable

This is what people mean by a credit card liability shift, card payment liability shift, or payment liability shift.

The goal was simple: force the adoption of more secure payment methods.

So what does a successful liability shift mean? It means the transaction was authenticated using the required method, and the issuer, not the merchant, is responsible for fraud-related losses.

How the Liability Shift Changed Payment Fraud Responsibility

The liability shift didn’t just change who pays for fraud. It changed how risk is distributed across the transaction lifecycle.

Before the shift, issuers often absorbed fraud losses, and transactions could be approved without the merchant carrying the full risk.

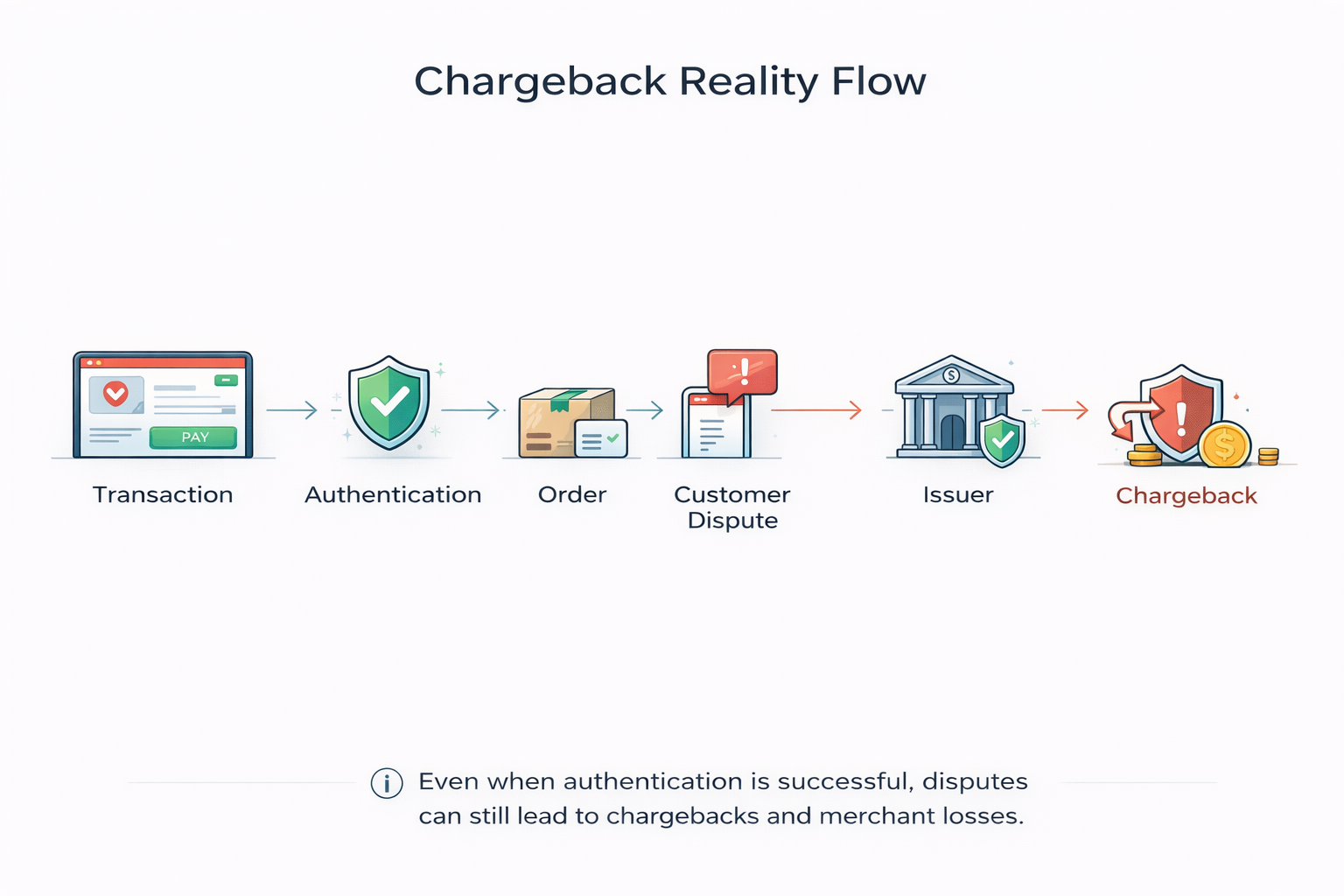

After the shift, that changed: if a transaction isn’t authenticated using the expected method, the loss moves downstream to the merchant, even if the payment was approved. That creates a gap between system approval and dispute reality.

From the system’s perspective, the transaction is valid and authorized. From the issuer’s perspective, the situation is simpler: the cardholder denies the charge. Liability is determined by how clearly the merchant can connect the customer to the transaction, not whether the payment was approved.

In practice, the liability shift determines which party is financially responsible for a fraudulent transaction when proper authentication isn’t used, shifting responsibility to the party with weaker security controls.

Card-present fraud declined after EMV adoption, while online fraud increased as attackers moved to environments without chip-based verification. Today, card-not-present fraud accounts for the majority of payment fraud losses, even though it represents a smaller share of total transactions.

The shift didn’t make fraud easier or harder. It made merchants accountable for what happens after approval, which is why many losses show up later, when a completed transaction turns into a dispute.

Card-Present vs. Card-Not-Present Fraud After the Liability Shift

Liability shifts based on how a transaction is authenticated, not whether it is approved.

The biggest impact of the EMV liability shift was where fraud happens. In physical stores, chip cards reduced counterfeit fraud and made skimming less effective, while shifting liability to merchants still using outdated systems. As a result, card-present fraud declined.

Online, the opposite happened. Transactions don’t benefit from chip verification and rely on weaker authentication signals, which made them easier to exploit and increased fraud rates.

This is where most liability gaps exist today. Online transactions carry more exposure, which is why unauthorized transaction disputes remain common even when payments are successfully approved.

Liability Shift in Online Payments (3D Secure)

In online transactions, liability shift works differently. Instead of EMV, it depends on authentication methods like 3D Secure (3DS). When applied correctly, the cardholder is verified during checkout, and liability can shift from the merchant to the issuer. But this only applies under specific conditions.

Liability shift typically applies when authentication is successful and fully completed. If the transaction bypasses 3DS, fails authentication, or isn’t triggered when required, the merchant may still be liable.

Even when liability shifts, gaps remain. The transaction can still be disputed, and the outcome depends on the issuer’s evaluation. 3D Secure reduces risk. It doesn’t remove it. Like EMV, it protects the transaction at a specific moment. It does not address what happens after authentication, including account takeover or post-purchase disputes.

How the Liability Shift Affects Merchants and Payment Processors

For merchants, the liability shift is not just about compliance. It’s about exposure. Even when transactions look legitimate, the account may be compromised, the payment method may be valid, and the authorization may pass. But if the cardholder disputes the charge, the merchant may still be liable

This is where chargeback liability shift expectations break down. Authorization does not equal protection, because approval only confirms the transaction, not the customer behind it.

Processors handle the transaction. They facilitate authentication and routing, but they don’t determine liability in a dispute. That decision rests with the issuer, based on how the transaction was authenticated. Issuers evaluate the dispute, and merchants absorb the loss if the proof is insufficient. Liability shift changes who pays for fraud. It doesn’t prevent the dispute from happening.

How EMV Technology Helps Prevent Fraudulent Transactions

EMV technology reduces fraud by making transactions harder to replicate. It uses dynamic authentication codes and chip-based verification and reduces reliance on static card data.

This measure makes counterfeit fraud significantly harder in physical environments. But EMV has limits. It does not protect online transactions or prevent account takeover and friendly fraud. It secures the card, not the account.

When Liability Shift Fails

Liability shift only applies under the right conditions. In practice, it often fails. Common reasons include fallback to magnetic stripe transactions, missing or skipped authentication, incomplete transaction data, and issuer-side decisions during dispute review.

When the transaction is completed, liability moves back to the merchant. This situation is where many losses occur, not because the transaction was obviously fraudulent, but because the required conditions for liability shift weren’t met.

Best Practices for Merchants After the Liability Shift

The liability shift changed responsibility. It didn’t eliminate risk.

Most fraud today doesn’t fail at authentication. It fails after access is granted. That’s why merchants need to focus beyond payment approval and control what happens across the full transaction lifecycle.

Don’t rely on authorization alone. Approved transactions can still become disputes, especially in account takeover and friendly fraud scenarios where the payment itself looks legitimate.

Use authentication selectively. Apply EMV and 3D Secure where risk justifies it. Overusing authentication adds friction, while underusing it increases exposure without actually reducing disputes.

Strengthen post-login monitoring. Most fraud now happens after the customer is authenticated, when the session is trusted and actions inherit that trust.

Track behavior, not just transactions. Fraud rarely appears as a single event. It shows up as a sequence, where actions connect over time.

Prepare for disputes, not just fraud prevention. Even when liability shifts, disputes still happen. What matters is whether you can connect the customer to the transaction in a way the issuer accepts.

The goal isn’t to stop every risky transaction. It’s to reduce the number of valid transactions that turn into disputes later.

The Bottom Line

The liability shift didn’t remove fraud. It changed where risk sits and how losses surface. For in-store payments, EMV reduced counterfeit fraud. For online transactions, risk increased and shifted toward merchants.

A successful liability shift depends on using the right authentication at the right time. But most losses today don’t come from failed authentication. They come from trusted sessions that lead to disputes later. Understanding where liability sits matters. Controlling what happens before the chargeback is what actually reduces loss.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)