%201.svg)

PayPal Chargebacks: Policy, Fees, and Seller Protection

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

PayPal chargebacks are bank-initiated reversals that completely bypass PayPal and hand final decision power to card issuers. Unlike disputes, merchants get limited control, strict deadlines, and unavoidable fees. The ultimate outcome is always controlled by the issuer, not PayPal. PayPal Seller Protection offers only partial coverage and explicitly excludes key issuer claims like “item not received.” Smart merchants win (or minimize losses) by combining strong documentation, robust fraud prevention, and early intervention tools like Chargeflow Prevent.

The current state of PayPal chargebacks is the result of two decades of litigation and regulatory intervention.

In the early 2000s, a wave of payment reversals nearly drowned the young company. The U.S. District Judge Jeremy Fogel ruled that the platform’s “chronically understaffed” system required more efficient procedures for investigating claims. This precedent, combined with the 2009 Weiler Group class-action lawsuit and a $25 million CFPB penalty for mishandling billing disputes, established the foundation for today’s PayPal chargeback framework.

PayPal has since taken steps to address the proliferation of friendly fraud, following a viral $4,000 chargeback fraud case and high-value gallery scam. These pressures triggered a 2023 policy overhaul, which specifically removed “item not received” as a valid reason for certain credit card chargebacks as post-pandemic fraud spiked.

For merchants, navigating this landscape now requires a technical understanding of tiered fees and Seller Protection eligibility. This guide provides the strategic clarity you need to manage PayPal’s modern chargeback protocols efficiently.

What Is a PayPal Chargeback?

A PayPal chargeback is a formal reversal of a completed transaction. The buyer’s credit or debit card issuer, not PayPal, initiates PayPal chargebacks.

A PayPal chargeback differs from a PayPal dispute or claim, which are filed through the Resolution Center. Those keep the process within the platform, enabling PayPal to oversee evidence from both sides. Chargebacks bypass PayPal’s system altogether.

The card issuer makes the final call. PayPal only receives the resulting case and acts as a liaison. This bypass is what makes chargebacks such a powerful instrument in the hands of bad actors.

PayPal Chargebacks vs. PayPal Disputes

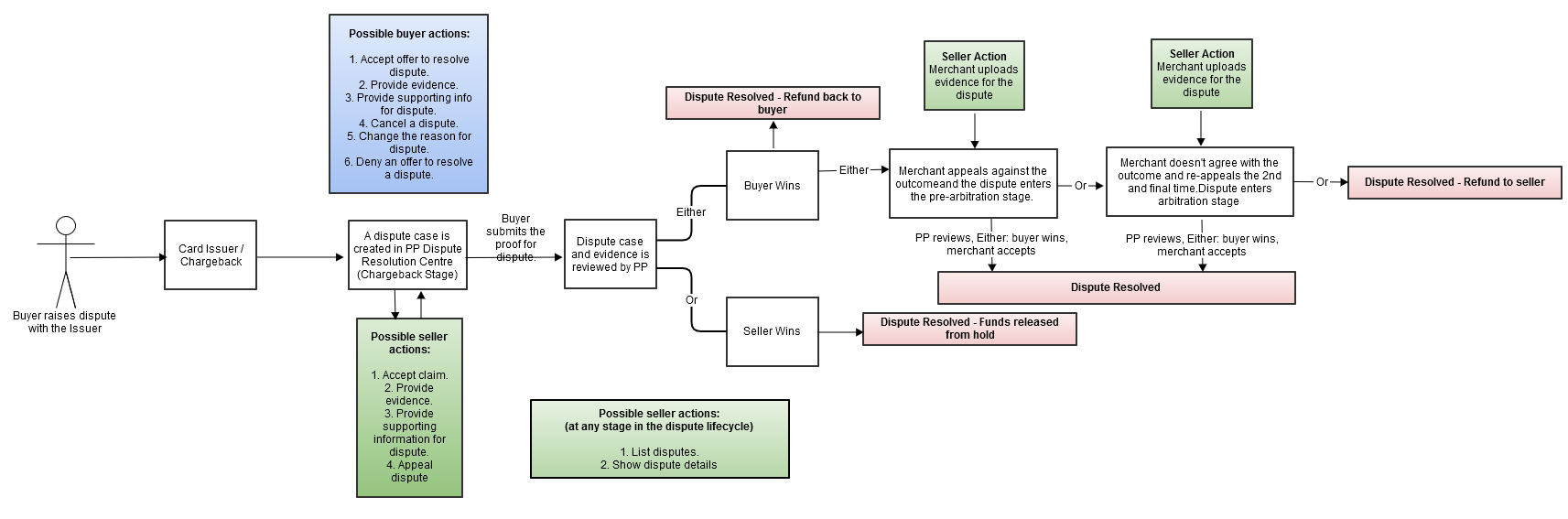

Both chargebacks and disputes stem from the same root causes. But on PayPal, they follow fundamentally different paths and have very different implications for sellers.

A PayPal dispute happens inside the platform, and both parties have 20 days to resolve the issue directly. If unresolved, it escalates to a claim, and PayPal makes a binding decision.

A PayPal chargeback, however, skips PayPal entirely. The buyer goes to their card issuer, which investigates and makes the final call, often within a 120-day window. As indicated earlier, PayPal simply relays information, with zero control over the outcome.

That difference is critical. Disputes, when they haven’t escalated to claims, are a flexible negotiation. They are manageable. Even when disputes escalate into claims, merchants retain some control since PayPal, not an external party, serves as the adjudicator. Chargebacks shift the decision entirely to the card issuer.

In short, disputes give you a chance to resolve. Chargebacks force you to defend.

How to Charge Back a PayPal Transaction (And Why Merchants Need to Understand It)

Once the buyer triggers a chargeback with their bank, the process advances without your input. Money leaves your account before you receive a notification. There is no pause to hear your side, and the burden of proof falls on you. You must respond with documented evidence and meet the issuer’s deadline and formatting standards.

Here’s how cardholders charge back a PayPal transaction:

- The cardholder files a PayPal transaction chargeback through their bank app or other channels.

- Their bank or card issuer reviews the claim under its own rules (mostly within 120 days, though some reason codes allow only 60-90 days, or even 45 days). If it rules in favor of the buyer, it orders a full payment reversal and debits PayPal’s acquiring bank.

- The acquiring bank debits PayPal, which in turn debits your merchant balance and deducts a chargeback fee, typically $20, though this varies by account type and dispute category. A matching case opens automatically in the Resolution Center.

- You receive the alert with a tight deadline (usually 10-20 days) to upload evidence. PayPal compiles and forwards your documents to the issuer, who makes the final determination.

PayPal’s Seller Protection program can reimburse eligible merchants after the fact. But it does not intervene in the issuer’s process.

This structure may not hold indefinitely. In December 2025, PayPal filed a formal application with the FDIC and the Utah Department of Financial Institutions to charter PayPal Bank as an industrial loan company. If approved, PayPal would handle merchant acquiring directly. This collapses the third-party bank operation, giving it meaningful control over the chargeback pipeline for the first time.

PayPal Chargeback Policy and Time Limits

PayPal has always been structurally subordinate to the card issuer in card-network chargebacks. That is a function of hierarchy, not policy choice.

What two decades of litigation and regulatory pressure actually reshaped was the protection aspect around that role. The most recent change was in 2023. PayPal removed “Item Not Received” as a valid basis for Seller Protection on card-funded transactions. If a buyer files a PayPal chargeback on those grounds and the issuer rules in their favor, PayPal will not reimburse the loss. There’s no fallback.

These are the filing windows that govern every chargeback:

Buyer Filing Windows (Issuer Chargebacks)

- Visa, American Express, Discover: Up to 120 days from the transaction date, or from the expected delivery date for “item not received” and not as described claims.

- Mastercard: 90 to 120 days, depending on the chargeback reason code. Certain fraud and authorization codes compress timelines to 45 or 75 days.

📍Note: Internal PayPal disputes operate on a separate 180-day window and are governed by a different set of rules.

Merchant Response Deadlines

Once a chargeback case opens in the Resolution Center:

- Most networks give you 10 days to submit evidence; some cases allow up to 20 days. Your notification will state the exact deadline.

- For Seller Protection eligibility, PayPal may issue follow-up requests after your initial submission. Respond within 10 days, or the case proceeds without your input.

Missed deadlines may result in a loss by default. This is often the case for many merchants because of the short 10-day window between a chargeback filing and your response deadline. It's often too late to start prepping your response by the time the notification arrives.

PayPal Chargeback Fees and Costs

Besides the transaction value that a chargeback reverses, there are costs associated with every chargeback. Banks charge PayPal a service or processing fee for each chargeback. PayPal, in turn, passes this fee over to merchants.

The dispute fee applies when a buyer files a claim through PayPal or a reversal through their bank for transactions made with a PayPal account or PayPal Checkout.

Below is a breakdown of the various fees:

PayPal Dispute Fees (Branded Transactions)

Standard Dispute Fee: $15 (Applied to most merchants by default).

High-Volume Dispute Fee: $30 (Applied if your dispute rate is ≥ 1.5% and you had >100 transactions in the previous 3 months.

High-volume merchants are exempt from a high-volume dispute fee if:

- Inquiries filed in PayPal’s Resolution Center are not escalated to a claim.

- They resolve disputes directly with the buyer, and the case is not escalated to a claim.

- The dispute is reported by the buyer directly to PayPal as an unauthorized transaction.

PayPal Chargeback Fees (Unbranded Transactions)

For "unbranded" transactions (where customers pay directly via credit or debit card without a PayPal account), PayPal applies a chargeback fee when a buyer files a chargeback with their card issuer.

- Fixed Fee: $20.00 USD (or equivalent in the transaction currency).

- Currency Equivalents:

- EUR: €16.00

- GBP: £14.00

- CAD: $20.00

- AUD: $22.00

- Seller Protection: If the transaction is eligible for PayPal Seller Protection, the chargeback fee is waived entirely.

Indirect Costs and Retention Policies

Beyond the specific dispute/chargeback penalties, merchants face several hidden costs during a payment reversal:

- Original Processing Fees: PayPal does not return the original processing fees (e.g., the 2.99% + $0.49 or 3.49% + $0.49) when a refund or chargeback occurs. This means even if you "break even" on the dispute, you lose the initial cost of processing.

- International Surcharge: If the transaction was international, the 1.50% cross-border fee is also retained by PayPal.

- Currency Conversion Spread: Any costs associated with the ~3.00% currency conversion markup are not recovered.

The table below breaks down the various PayPal chargeback fees and costs:

💡Note: PayPal calculates your dispute rate monthly based on the ratio of total claims to your total sales from the previous three months. This can mean even more trouble if your ratio exceeds the acceptable threshold.

Seller Protection and Chargeback Coverage on PayPal

PayPal’s Seller Protection is a reimbursement program with precise eligibility conditions. It’s not a blanket safety net. The gap between what it covers and what merchants assume it covers is where most losses occur.

What PayPal Seller Protection Covers

The program applies in three scenarios:

1) Unauthorized Transactions: The buyer claims they did not authorize or benefit from a payment sent from their PayPal account, and the transaction meets PayPal’s eligibility criteria.

2) Item Not Received: Coverage applies to claims filed through PayPal’s Resolution Center.

3) Unauthorized Chargebacks (limited cases): If a buyer files a chargeback specifically on unauthorized grounds, or a bank reverses a bank-funded payment, Seller Protection may still apply. Yet, that can only happen if the transaction meets all eligibility conditions.

The critical boundary is the routing of the claim, not the reason for it. When a merchant receives an Item Not Received claim as an external card-issuer chargeback, rather than through the Resolution Center, Seller Protection does not cover that claim. The same buyer, same transaction, same reason, but taking different paths results in no coverage for merchants.

Basic Eligibility Requirements of PayPal Seller Protection

All of the following must be satisfied simultaneously. A single unmet condition voids the claim.

Hard requirements:

- Your PayPal account's primary address must be in the United States.

- The item must be a physical, tangible good that can be shipped. Intangible goods are eligible only for Unauthorized Transaction claims, and only when PayPal has marked the transaction as eligible on the Transaction Details page.

- You must ship to the address on the Transaction Details page. Shipping to an address other than the one on the Transaction Details page, or using delivery arrangements that prevent address verification (including certain forwarding or buyer-arranged handling), can void protection. If the item is redirected after dispatch in a way that breaks delivery confirmation, eligibility may be lost.

- You must respond to PayPal's documentation requests within the timeframe specified in their correspondence.

For Unauthorized Transaction claims specifically:

- The payment must be marked "eligible" or "partially eligible" on the Transaction Details page.

- Proof of shipment must show the item was dispatched within two days of the timestamp on PayPal's notification — not two days from when you read it.

For PayPal Checkout integrations:

- You must be running the current version and passing the required session data to PayPal at checkout. An outdated integration or missing session data can disqualify an otherwise eligible transaction. High-risk business models may face additional integration requirements communicated by PayPal in advance.

Shipping timelines: For pre-ordered or made-to-order goods, you must ship within the timeframe stated in your listing. For all other items, PayPal recommends dispatch within seven days of payment. Delays can impact eligibility, depending on the nature of the dispute.

PayPal Seller Protection Proof Standards

For Item Not Received claims, proof of shipment is insufficient. Proof of delivery is required. These include an online, verifiable tracking number showing “delivered” status, a delivery date, and a recipient address that matches the Transaction Details page to at least the city/state or zip code level. Your carrier can determine whether you can meet this standard. Carriers that do not return verified delivery status to an online record will leave you unable to satisfy it, particularly on international shipments.

For intangible goods, the standard is compelling evidence of delivery. These include, but are not limited to: a system of record to show the send date and confirmation that the item was either electronically transmitted to the buyer or accessed by them.

What PayPal Seller Protection Does Not Cover

Below are vital exclusions from PayPal Seller Protection according to the company's policy documents:

Chargeback-related exclusions

- Item Not Received claims filed directly with the card issuer.

- Significantly Not as Described claims, whether filed through PayPal or the card issuer, are entirely excluded.

Payment method exclusions

- Guest Checkout and Standard Credit and Debit Card Payments, where the seller’s account is registered in a defined list of countries, including Singapore, China, Hong Kong, Australia, and most EU member states.

- PayPal Payouts and Mass Pay transactions.

- Payment received through a PayPal business account’s assigned account and routing number.

- Friends and family, and other personal transactions.

Product and transaction exclusions

- Real estate; vehicles (excluding portable recreational items such as bicycles and wheeled hoverboards); industrial machinery; businesses.

- Gold, financial products, and investments.

- NFTs above $10,000; NFTs at or below $10,000 are eligible only for Unauthorized Transaction claims.

- Gift cards, pre-paid cards, and stored value items.

- Gambling and gaming transactions with entry fees and prizes.

- Donations, crowdfunding, and crowdlending receipts.

- Government body and bill payment transactions.

- Travel tickets where an Unauthorized Transaction claim is filed more than 24 hours before the departure date.

- Items shipped after PayPal explicitly advised you not to release them.

The Operative Implication

Seller Protection covers unauthorized transaction disputes and Resolution Center INR claims when properly documented, properly shipped, and processed through a PayPal account. It does not include external chargebacks on Not Received or disputes of product misrepresentation. The card issuer decides in both cases, and the liability remains with the merchant.

How to Protect Yourself From a PayPal Chargeback

Protection against chargebacks operates at four distinct touchpoints in the transaction lifecycle: before the sale, before the high-risk transaction is accepted, before the chargeback is filed, and when a dispute reaches the Resolution Center. Each fabric addresses a different failure mode. None of them substitutes for the other.

Let's examine these critical points of interaction deeper:

Before the Sale

The documentation that wins a chargeback dispute is assembled before the transaction is completed, not after the case opens. This means:

- Shipping exclusively with carriers that return verified delivery status to an online record.

- Keeping customer service correspondence in a retrievable format.

- Maintaining accurate product descriptions that cannot reasonably be characterized as misrepresentation.

- Publishing refund, shipping, and delivery timelines clearly enough that a buyer has zero grounds to claim they were uninformed.

These best practices do not prevent chargebacks. They determine whether you can defend against them once filed, and whether Seller Protection applies when the card issuer makes its ruling.

Before the Transaction is Processed

The most structurally durable protection is upstream, preventing high-risk transactions from completing in the first place. A chargeback cannot be filed on a transaction you never accepted.

Chargeflow Prevent blocks high-risk transactions before they process. Seller Protection explicitly does not cover transactions that are likely to result in 'Significantly Not as Described' claims or first-party fraud. At volume, those gaps compound. Chargeflow Prevent addresses both before a transaction is accepted.

Before the Chargeback is Filed

Most chargebacks do not arrive without warning. But that’s if you’re using the right tools.

When a cardholder initiates a chargeback with their bank, a short window exists before the dispute is formally filed. That’s the space before the case opens, the response clock starts, and any fees are applied. The window between that decision and the formal filing is where early notification has operational value.

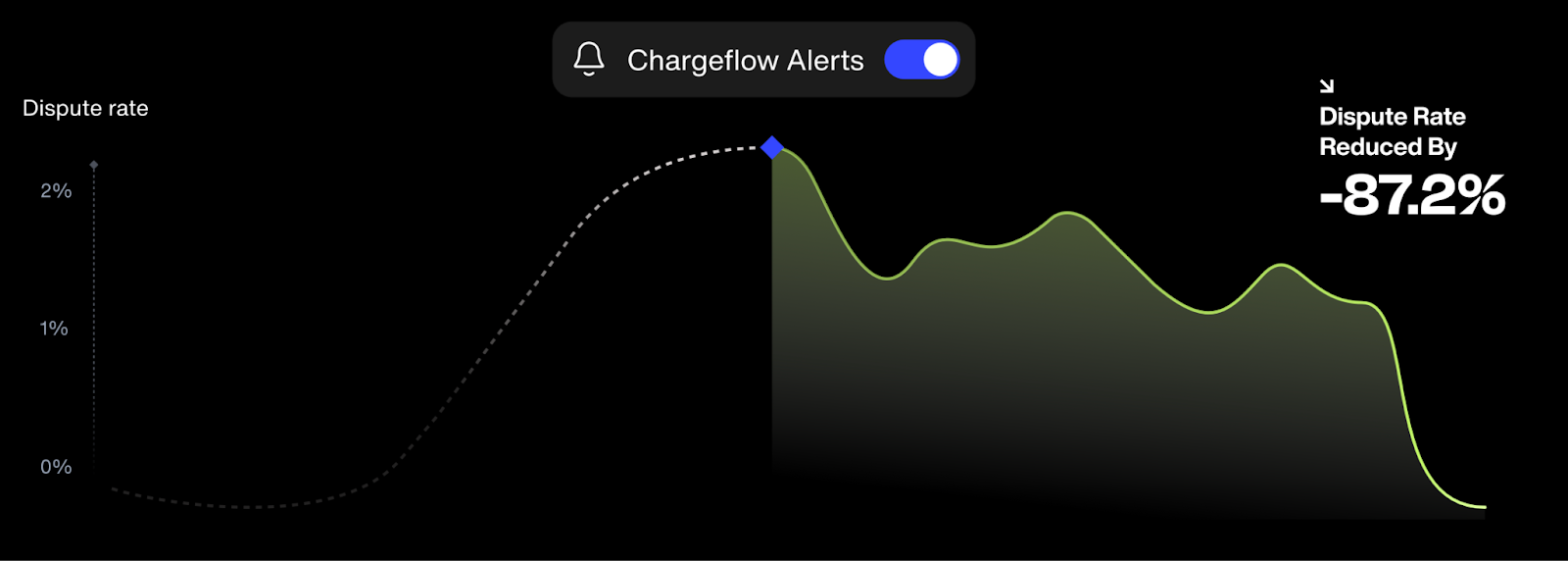

Chargeflow Alerts operate in that window. It notifies merchants of impending chargebacks across all incoming disputes. That lead time allows you to issue a refund or prepare documentation before the case formalises. A chargeback that is never filed carries no fee, no dispute record, and has zero effect on your dispute ratio.

When Chargeback Reaches the Response Center

Early alerting and transaction screening reduce exposure before the chargeback machinery engages. They do not eliminate the disputes that slip through. For those, the question is whether your response process is fast enough, thorough enough, and effectively consistent to meet the card issuer’s evidence standards, regardless of volume.

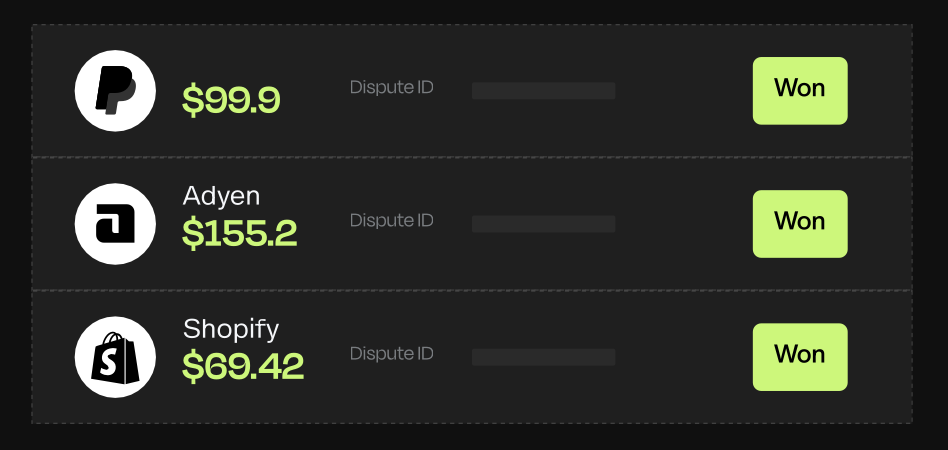

Chargeflow automation handles the dispute lifecycle end-to-end: evidence collection, response construction, and submission across PayPal and other processor accounts. This eliminates staff time, documentation retrieval headaches, and the nightmare of deadline tracking for merchants who manually manage chargeback volume.

PayPal vs. Square Chargeback Policies

For merchants processing payments across both PayPal and Square, or deciding between them, the chargeback mechanics differ in ways that directly affect cost, workload, and exposure. The differences are structural, not cosmetic.

Key Takeaway:

Square removes the per-dispute fee, which lowers the marginal cost of each chargeback. Nevertheless, it compresses the response window to about seven days, which is tighter than PayPal’s standard, and does not support arbitration escalation.

If Square submits your evidence and the issuer rules against you, the decision is final in practice. There is no facilitated path beyond it.

PayPal’s fee structure increases the cost per dispute. And its Seller Protection program carries strict eligibility requirements with meaningful exclusions. What it does offer in return is a longer response window, a formal protection mechanism for qualifying transactions, and participation in the full card network dispute lifecycle. Escalation beyond the initial ruling is at least structurally available.

Conclusion

PayPal is the largest platform for everyday digital payments, with the widest reach, the strongest brand, and the highest market share. That scale places it at the centre of global dispute and chargeback activity.

Its chargeback framework is the result of two decades of litigation, regulatory intervention, and rising fraud pressure. The result is a system built for procedural consistency, not merchant flexibility. The card issuer controls the outcome. Fees apply regardless of resolution. Seller Protection exists, but only within eligibility boundaries that exclude many of the dispute types merchants encounter most often.

The framework does not change. What changes are your position within it: how much of your exposure is screened before a transaction is processed, intercepted before a chargeback is filed, and recovered before a deadline expires.

That is the problem Chargeflow’s PayPal integration was built to solve. It does not change how PayPal works. Instead, it closes every chargeback loophole the process leaves open.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)