%201.svg)

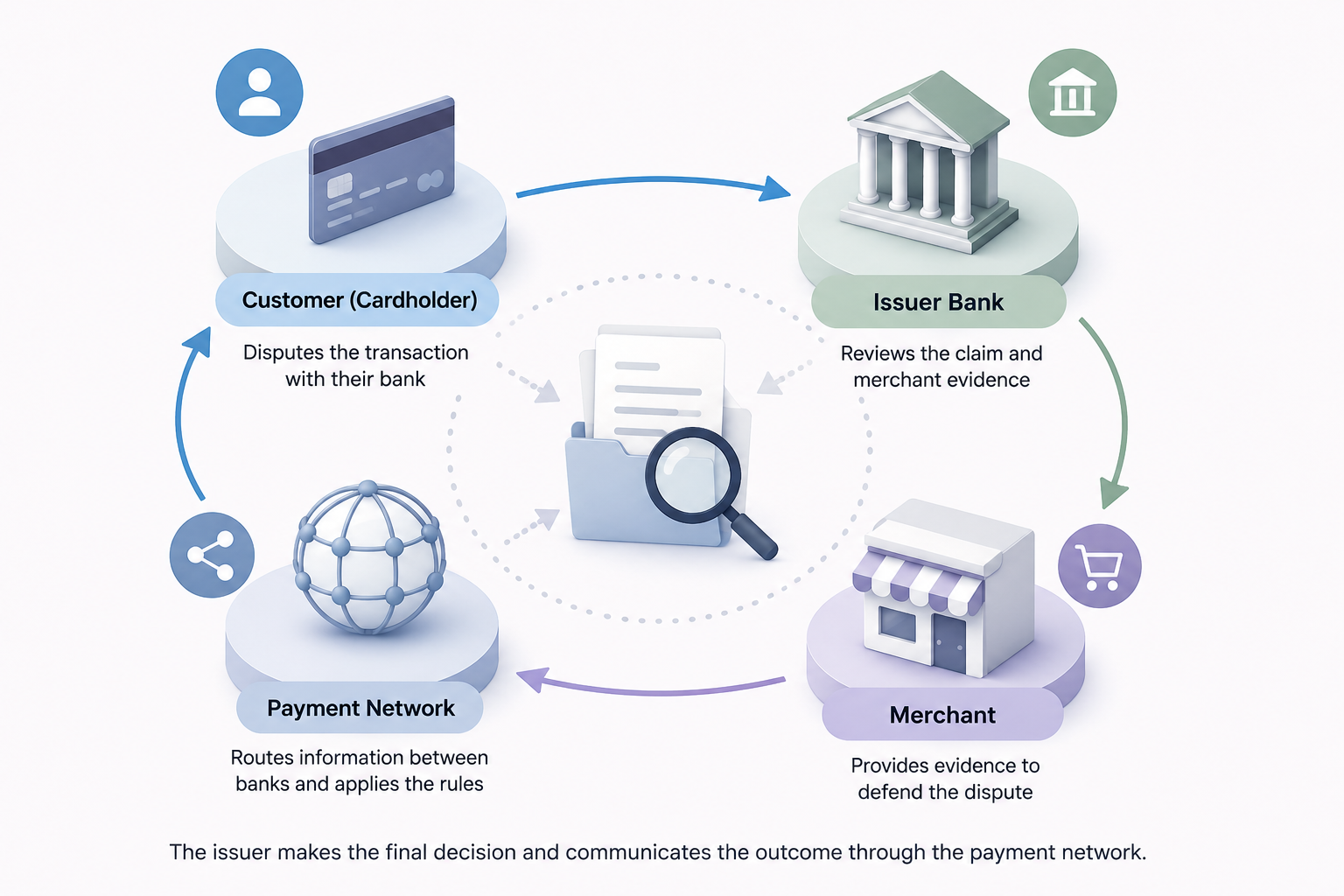

How Do Issuers Evaluate Chargeback Disputes?

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

Issuers weigh the cardholder's claim against your evidence, the transaction record, and the card network rules for that specific reason code. Consistent proof that directly answers the reason code wins far more often than long explanations. Visa caps issuer review at 30 days.

Short Answer

When a customer files a chargeback, the issuing bank reviews the transaction details, the cardholder's explanation, and any evidence the merchant submits. The issuer checks whether you followed card network rules, delivered what was promised, and responded with evidence that directly addresses the dispute reason code.

Issuers are looking for consistency. If the transaction timeline, customer activity, and fulfillment records all line up, your win odds rise sharply. Most disputes are decided in four to six weeks, and Visa limits the issuer to 30 days to review representment evidence, so speed and clarity matter.

What do issuers look for in chargeback evidence?

1. Evidence matched to the reason code

Issuers do not evaluate disputes generically. They review them against the specific reason code attached to the claim. Visa 10.4 (fraud, card-absent) demands very different proof than Visa 13.1 (merchandise not received).

For example:

- Unauthorized transaction disputes (Visa 10.4) require login data, device information, AVS/CVV results, or 3DS authentication.

- Item not received disputes (Visa 13.1) require valid tracking and delivery confirmation.

- Subscription disputes (Visa 13.2) require renewal disclosures and cancellation records.

2. Transaction consistency

Issuers compare:

- Billing and shipping details

- Customer communication history

- Device or IP data

- Purchase history

- Delivery timing

Any mismatch weakens the case quickly. If your evidence is solid but keeps getting turned down, see why evidence is rejected by issuers.

3. Evidence submitted before the deadline

Late submissions are often ignored automatically by processors and card networks.

Chargeflow Automation can help merchants collect and submit evidence before issuer deadlines expire.

4. Simple, organized proof

Issuers review large volumes of disputes daily. Long explanations usually hurt more than help. Use clear timelines, short summaries, organized screenshots, and relevant receipts and tracking.

5. Repeat friendly-fraud patterns

Issuers increasingly monitor repeat dispute behavior from cardholders. Chargeflow Insights can help merchants identify repeat abusers, high-risk order patterns, and recurring dispute triggers.

What evidence do issuers expect by reason code?

How do card network rules and arbitration affect the outcome?

Each network sets its own framework. Visa routes most disputes through Visa Claims Resolution (VCR), which standardizes timelines and pushes liability automatically when rules are not met. Mastercard uses its own dispute resolution process with comparable reason-code requirements.

If the issuer rejects your representment, the case can move to pre-arbitration and then arbitration, where the network makes the final ruling and the losing side pays additional fees. Because arbitration is costly, only fight disputes where the evidence is strong and clearly mapped to the reason code. When a bank comes back for more, see what to do when a bank requests more evidence.

How does evaluation differ by platform?

Stripe

Stripe disputes rely heavily on structured evidence fields. Missing required fields can weaken a case even when the merchant has valid proof. See the Stripe integration for how evidence is assembled automatically.

PayPal

PayPal places strong weight on tracking confirmation, delivery status, and documented customer communication.

Digital Goods

Issuers usually expect login timestamps, usage records, download confirmations, and device consistency. Digital goods disputes are harder to win without behavioral evidence.

What evidence should you always have ready?

Issuers commonly expect:

- Order confirmation

- Payment authorization details

- AVS/CVV match results

- Proof of delivery or service

- Customer communication logs

- Refund or cancellation records

- Device/IP data

- Subscription acceptance records

- Tracking information

The strongest evidence directly disproves the customer's claim.

Why issuers decide the way they do

Issuers are determining whether the transaction followed card network rules and whether the cardholder's claim is valid. Most disputes are evaluated quickly, so weak or incomplete evidence often leads to automatic losses.

The merchants who win more disputes are usually the ones submitting cleaner evidence faster, not longer explanations, and Chargeflow helps automate that process at scale.

FAQ

How long does an issuer take to review a chargeback dispute?

Most disputes are decided within four to six weeks. Under Visa rules, the issuer has up to 30 days to review the merchant's representment evidence before issuing a decision.

What counts as compelling evidence?

Compelling evidence directly contradicts the cardholder's claim and matches the reason code, such as AVS/CVV and 3DS results for fraud, or signature-confirmed delivery for an item-not-received dispute.

Do issuers automatically side with the cardholder?

Issuers grant the cardholder provisional credit when a dispute is filed, but they will reverse it if the merchant's evidence is consistent, on time, and clearly tied to the reason code.

What happens if the issuer rejects my evidence?

The dispute can move to pre-arbitration and then arbitration, where the card network makes the final ruling and the losing party pays additional fees.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)

More articles.

How Do I Track Dispute Performance Across Multiple Accounts?

To track dispute performance across multiple accounts, consolidate chargeback data from every processor, store, and merchant account into one dashboard, then compare the same core metrics, dispute rate, win rate, recovery rate, and reason-code trends at both account and portfolio level. Centralized reporting surfaces rising-risk accounts before they trip card-network thresholds like Visa’s VAMP.

How Do I Standardize Evidence Across Dispute Types?

Standardize chargeback evidence by building one core evidence package for every order, transaction, fulfillment, customer, and policy records, then layering in dispute-specific proof mapped to the reason code. A single repeatable framework beats managing evidence reason code by reason code: it closes gaps, speeds responses, and lifts win rates.

How Do I Align Customer Support and Payments to Reduce Disputes?

Many chargebacks start as unresolved support issues, not payment problems. When customer support and payments share one dispute-prevention queue, escalation rules, and pre-chargeback alert data, you resolve refund, delivery, and billing complaints before they reach the issuing bank.

Questions?

we’ve got answers.

Chargeflow collects data from dozens of third party signals, not just transaction data like Stripe Dispute does. This allows for much more coverage and much better win rates because the evidence submitted is much more comprehensive and compelling..

Chargeflow collects data like order info, customer messages, and payment details. It builds a full dispute case for you, so you don’t have to lift a finger.

Yes! Chargeflow works with many processors — not just Stripe. That means one tool for all your chargebacks, no matter how you process payments.

You only pay a percentage of the revenue we help you recover. No upfront fees, no subscriptions — just success-based pricing.

Yes. Chargeflow is SOC 2, GDPR, and ISO certified. We use top security standards to keep your data safe.

need more help?

Have a question? We’re here to help. Just hit the chat button to initiate a conversation with support.