What Is Chargeback Representment? Definition and Process

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 15,000 merchants.

Chargeback representment is the process where a merchant disputes a chargeback by submitting evidence to the issuing bank. The chargeback representment process follows strict timelines, depends on the reason code, and ends with either a win, a loss, or escalation to arbitration. By the time representment begins, the merchant has already lost the money.

Chargeback representment begins after a chargeback is filed and funds are already removed from the merchant. At that point, the only way to recover the transaction is to respond within the allowed window, using evidence that directly matches the reason code.

Understanding how chargeback representment works, and when it’s worth pursuing, determines whether disputes turn into recoverable revenue or permanent losses.

What is Chargeback Representment?

Chargeback representment is the formal process of contesting a chargeback by submitting evidence to the issuing bank through the card network.

The chargeback representment process typically includes notification, evidence collection, rebuttal submission, issuer review, and either reversal, loss, or escalation.

In simple terms, representment means the merchant is saying:

“This chargeback is invalid, and here’s the proof.”

A chargeback representment definition always includes three core elements:

- A disputed transaction

- A reason code that defines why the chargeback was filed

- A rebuttal package that addresses that reason code directly

Representment is not negotiation. It’s a rule-based review where issuers evaluate whether the evidence meets network requirements. Context, intent, or customer history rarely matters unless it is explicitly relevant to the reason code.

When Can You Initiate the Representment Process? Timeline and Deadlines

The chargeback representment timeline starts the moment the chargeback is officially issued.

Once the issuing bank files the chargeback:

- Funds are withdrawn from the merchant

- A response deadline is assigned

- The representment window opens

Deadlines vary by card network and reason code, but most merchants have 7 to 30 days to respond. Missing that window automatically forfeits the case.

This is why speed matters. Chargeback representment isn’t about writing the perfect response. It’s about submitting compliant evidence before the deadline expires.

The Chargeback Representment Process: Step-by-Step Timeline

This is how the chargeback representment process actually unfolds for merchants.

3.1 Receive the Chargeback Notification

The chargeback notification is delivered through the acquiring bank or payment processor. At this stage, merchants typically receive:

- The transaction details

- The reason code

- The representment deadline

- Limited information about the cardholder’s claim

The case clock starts immediately.

3.2 Review the Reason Code and Evidence Requirements

Every representment chargeback lives or dies by the reason code.

Reason codes determine:

- What evidence is required

- What arguments are valid

- What timelines apply

Submitting evidence that doesn’t match the reason code almost always leads to a loss, even if the merchant is technically right.

3.3 Collect Compelling Representment Evidence

Representment evidence must directly refute the cardholder’s claim.

Depending on the reason code, this can include:

- Proof of delivery with address match

- Digital access or usage logs

- IP, device, and session data

- Clear refund, cancellation, or terms of service acceptance

- Customer communication records

Issuers do not weigh evidence equally. Each document must clearly connect the cardholder to the transaction or prove that the merchant fulfilled their obligations under the terms of sale. Evidence that does not directly contradict the reason code is typically ignored.

More evidence is not better. Relevant evidence is.

3.4 Prepare and Format the Rebuttal Document

The rebuttal document explains why the evidence proves the chargeback is invalid.

Issuers are not reading for narrative. They’re checking whether:

- The evidence matches the reason code

- The documentation is complete

- The response is formatted correctly

A strong rebuttal is concise, factual, and structured around the issuer's criteria, not the merchant's frustration.

Many merchants rely on a chargeback representment template to ensure rebuttal documents follow issuer formatting requirements and include only evidence that directly supports the assigned reason code.

Poorly formatted rebuttals, even with strong evidence, are often rejected due to issuer processing rules rather than merit.

3.5 Submit the Representment Packet

Once compiled, the representment packet is submitted through the processor or platform.

After submission:

- Merchants cannot modify evidence

- Late additions are ignored

- The case moves back to the issuing bank

At this point, the decision is entirely in the issuer’s hands.

3.6 Await Issuer Review or Escalation

The issuing bank reviews the chargeback representment and makes a decision:

- Merchant wins: funds are returned (fees often remain)

- Merchant loss; funds stay reversed

- Escalation: the dispute moves to pre-arbitration

Issuer review timelines vary, but most decisions arrive within 30-75 days.

Before Representment: Pre-Dispute and Retrieval Requests Timeline

Not all disputes start with a chargeback.

In some cases, issuers initiate:

- Retrieval requests

- Information requests

- Pre-dispute inquiries

These requests ask the merchant for transaction details before a chargeback is filed. Responding successfully can prevent representment entirely by stopping the chargeback from being issued.

Ignoring these early signals increases representment volume later.

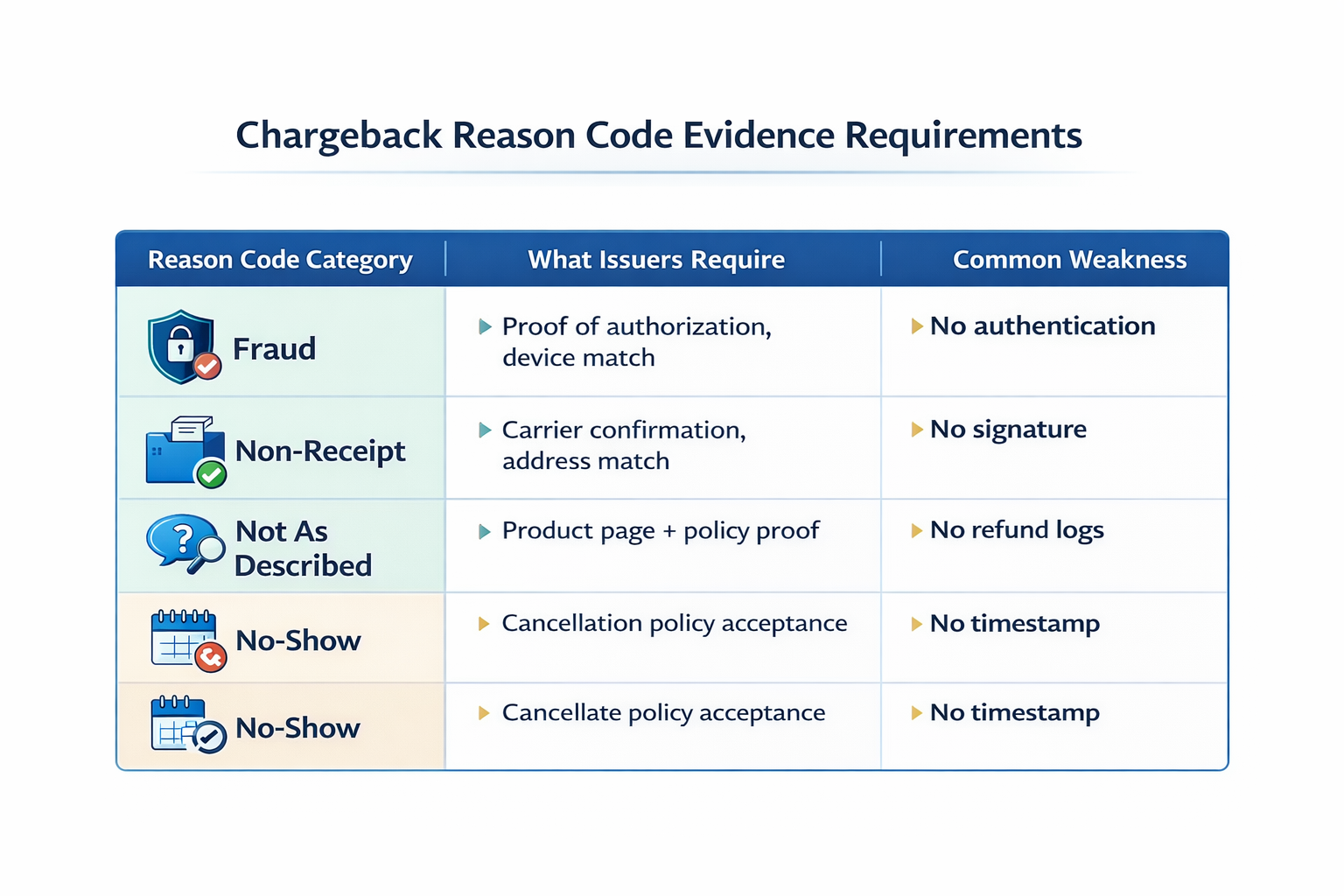

Chargeback Reason Codes and Their Impact on Representment Strategy

Reason codes dictate representment strategy. They define why the chargeback was filed and what evidence issuers will accept when reviewing a representment chargeback.

Each card network assigns reason codes that fall into broader categories, such as fraud, authorization issues, non-receipt, or not-as-described claims. While the numbering and wording vary by network, the impact on the chargeback representment process is consistent: evidence must directly address the reason code, or the case will fail.

For example:

- Fraud reason codes require proof that the cardholder authorized or participated in the transaction. This can include authentication data, IP and device matching, account activity logs, or evidence of prior successful transactions. Without proof tying the cardholder to the purchase, fraud-related representment is rarely successful.

- Non-receipt disputes rely almost entirely on fulfillment evidence. Issuers look for delivery confirmation, address matching, carrier timestamps, and, in some cases, signature confirmation. If delivery cannot be verified at the cardholder’s address, representment outcomes are weak.

- “Not as described” or defective merchandise claims depend on documentation that shows the customer received what was advertised. Product descriptions, screenshots, order confirmations, refund policies, and customer communications are often required to counter these disputes.

- No-show, canceled recurring, or subscription-related disputes require proof that the customer agreed to the billing terms. This includes cancellation policies, timestamps showing acceptance, billing descriptors, and evidence that cancellation rules were enforced correctly.

What matters most is not how persuasive the merchant’s explanation is, but whether the submitted evidence meets the issuer’s criteria for that specific reason code. Submitting generic documents or unrelated proof almost always results in a loss, even if the merchant is technically correct.

This is why successful chargeback representment is strategy-driven, not reactive. Merchants who tailor their representment evidence to each reason code consistently outperform those who submit the same documentation for every dispute.

Understanding reason codes also helps merchants decide when representment is worth pursuing. Some reason codes have historically low win rates regardless of effort, while others are highly defensible with proper documentation. Aligning representment strategy with reason code viability reduces wasted effort and improves overall recovery rates, and helps merchants avoid fighting cases they are unlikely to win.

When Representment Is Not Worth Pursuing

Representment is not always the right move.

It is rarely worth pursuing when documentation is incomplete, delivery confirmation is missing, authentication evidence is weak, or historical win rates for that specific reason code are low.

Fighting unwinnable disputes increases operational cost without improving recovery rates. Effective chargeback representment strategy includes knowing when to accept a loss and preserve resources for defensible cases.

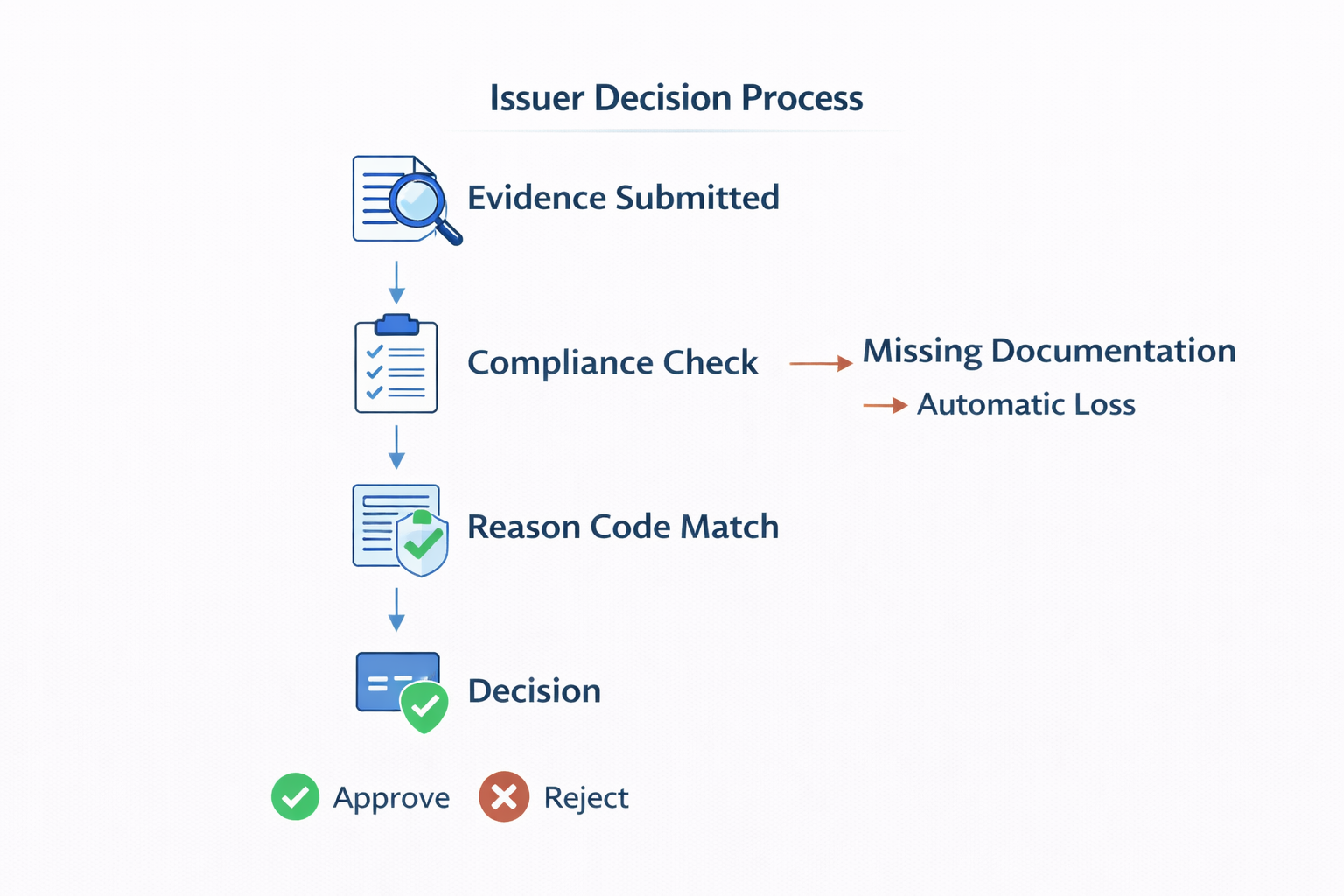

Representment Evidence, Issuer Decision Criteria, and Outcome Timelines

Issuers evaluate representment based on compliance, not context.

They check whether required documents are present, whether those documents directly match the reason code, and whether submission rules were followed exactly. Evidence that arrives late, is mislabeled, or does not map clearly to the claim is often dismissed without deeper review.

This explains why merchants can lose chargebacks even when they believe the facts are on their side. Representment outcomes are driven by process adherence, not fairness.

Outcome timelines typically follow this pattern:

- Issuer review begins after submission

- Decisions arrive within 30 to 75 days

- Escalated cases extend timelines significantly

When to Escalate to Arbitration After Representment

Arbitration is the final stage of the chargeback process.

After representment, a case may escalate to:

- Pre-arbitration

- Second chargeback

- Network arbitration

Arbitration involves high fees, strict documentation requirements, and binding outcomes. For most merchants, it is only worth pursuing when transaction value is high, evidence strength is exceptional, and abuse patterns justify the cost.

This is why many merchants stop at representment.

Best Practices for Automated Chargeback Representment

Manual representment does not scale. As dispute volume grows, inconsistency becomes the primary driver of avoidable losses.

Automated chargeback representment systems standardize evidence collection, reason-code matching, formatting, and submission timing. This reduces human error and ensures deadlines are never missed.

Best practices include:

- Reason-code specific evidence mapping

- Automated deadline tracking

- Consistent rebuttal formatting

- Performance reporting by reason code

Automated chargeback representment systems help merchants meet deadlines, standardize evidence, and reduce avoidable losses. But the real advantage comes from knowing which disputes are worth fighting and which are not.

When representment is treated as a repeatable process, guided by reason codes and evidence standards, chargebacks become more predictable and less disruptive. The outcome isn’t zero disputes. It’s fewer wasted efforts and better recovery when disputes do happen.

Chargeback Representment Is a Process, Not a One-Off Fix

Chargeback representment is not about winning every dispute. It’s about understanding when recovery is possible, when effort is wasted, and how issuer rules shape outcomes long before evidence is reviewed.

Merchants who treat representment as an isolated task often lose disputes they could have won. Those who approach it as a structured process, guided by reason codes, timelines, and evidence standards, recover more revenue with less operational strain.

Effective representment strategies rely on three elements:

- Clear decision-making about which disputes to fight

- Evidence tailored precisely to reason code requirements

- Consistent execution that meets issuer and network rules every time

When representment is managed this way, chargebacks stop being unpredictable interruptions and become a measurable, controllable part of post-purchase operations.

Understanding chargeback representment is not just about disputing transactions. It’s about knowing how the system works, where leverage exists, and how to respond within it efficiently.

Chargeback representment works best when it’s structured, not reactive.

If your team is managing disputes manually or struggling to meet issuer evidence requirements, explore how automated representment systems standardize documentation, enforce reason-code matching, and improve recovery rates

Want to see how automated chargeback representment works in practice?

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 15,000 merchants.

.png)

Questions?

we’ve got answers.

Chargeflow collects data from dozens of third party signals, automatically. This allows for much more coverage and much better win rates because the evidence submitted is much more comprehensive and compelling.

Chargeflow collects data like order info, customer messages, and payment details. It builds a full dispute case for you, so you don’t have to lift a finger.

Yes! Chargeflow works with 50+ payment processors. That means one tool for all your chargebacks, no matter how you process payments.

You only pay a percentage of the revenue we help you recover. No upfront fees, no subscriptions — just success-based pricing.

Yes. Chargeflow is SOC 2 Type 2, GDPR, and ISO certified. We use top security standards to keep your data safe.

need more help?

Have a question? We’re here to help. Just hit the chat button to initiate a conversation with support.