%201.svg)

What Is the Chargeback Process? A Complete Merchant Guide

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

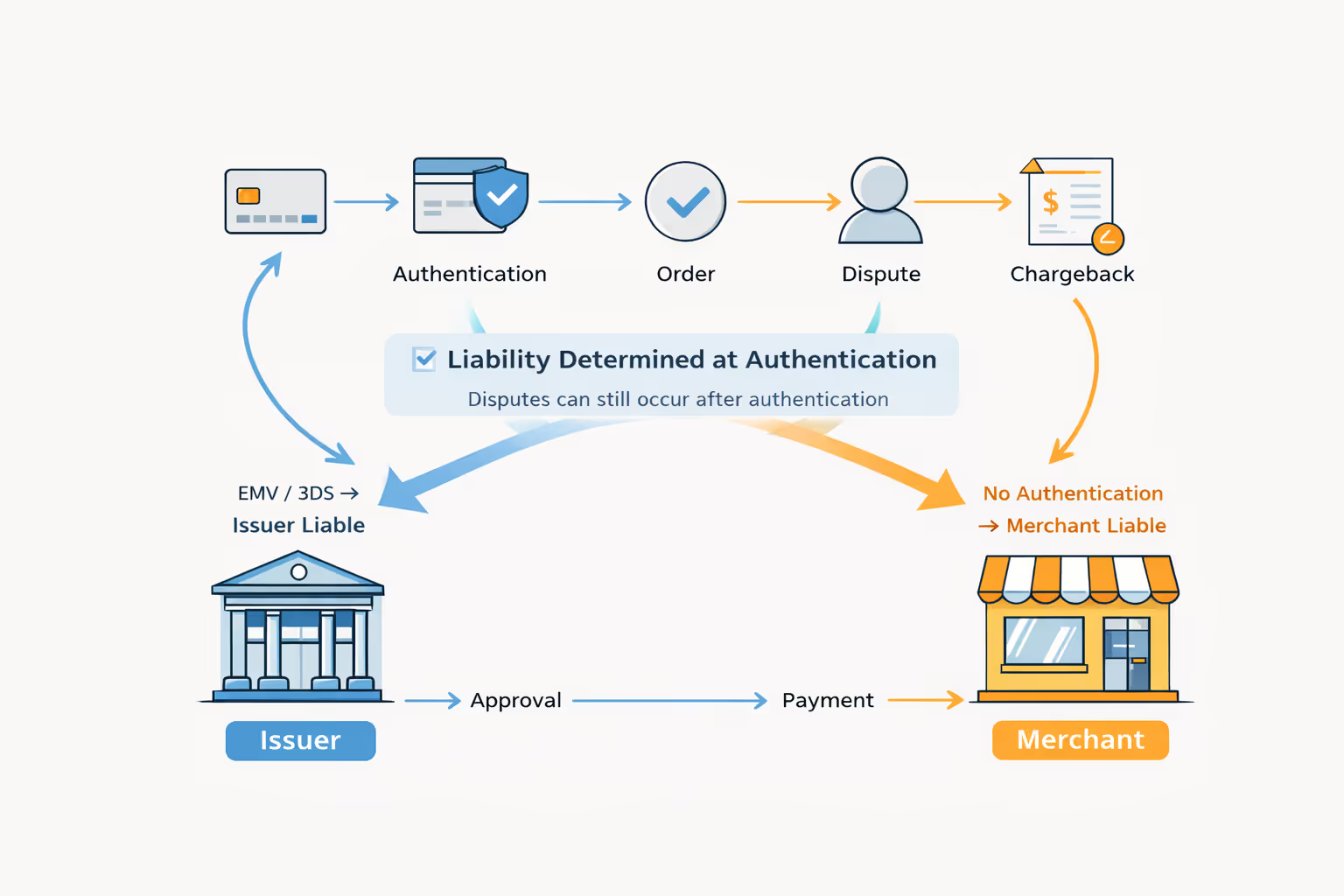

The chargeback process starts when a customer disputes a card transaction with their bank. Funds are pulled from the merchant, evidence is reviewed under card network rules, and the case is either won, lost, or escalated. Merchants feel the impact immediately, long before a decision is made.

Many merchants search for “what is chargeback process” when trying to understand what actually happens after a card dispute is filed. The chargeback process occurs when a customer disputes a card transaction with their bank. Control shifts from the merchant as funds are withdrawn and the dispute is reviewed through a bank-led, rules-driven process. For merchants, the cost is evident early on in revenue, dispute ratios, and operational strain.

Once a dispute enters this system, it follows a fixed path. Timelines, evidence, and outcomes are set by banks and card networks, not by the merchant.

Understanding the Chargeback Process

Chargebacks were created to protect cardholders when something goes wrong with a purchase. Over time, they’ve become the default path for resolving everything from real fraud to simple misunderstandings.

For merchants, that means operating inside a bank-controlled system with fixed timelines, strict evidence standards, and very little context. Once a dispute starts, you’re reacting, not negotiating.

Key Participants in the Chargeback Ecosystem

Every chargeback follows the same chain, even if merchants only interact with part of it.

- Cardholder: files the dispute

- Issuing bank: reviews the claim and opens the chargeback

- Card network: enforces timelines, reason codes, and outcomes

- Acquiring bank/processor: delivers the case to the merchant

- Merchant: accepts or disputes the chargeback

Outcomes are dictated by chargeback rules, not intent or customer history.

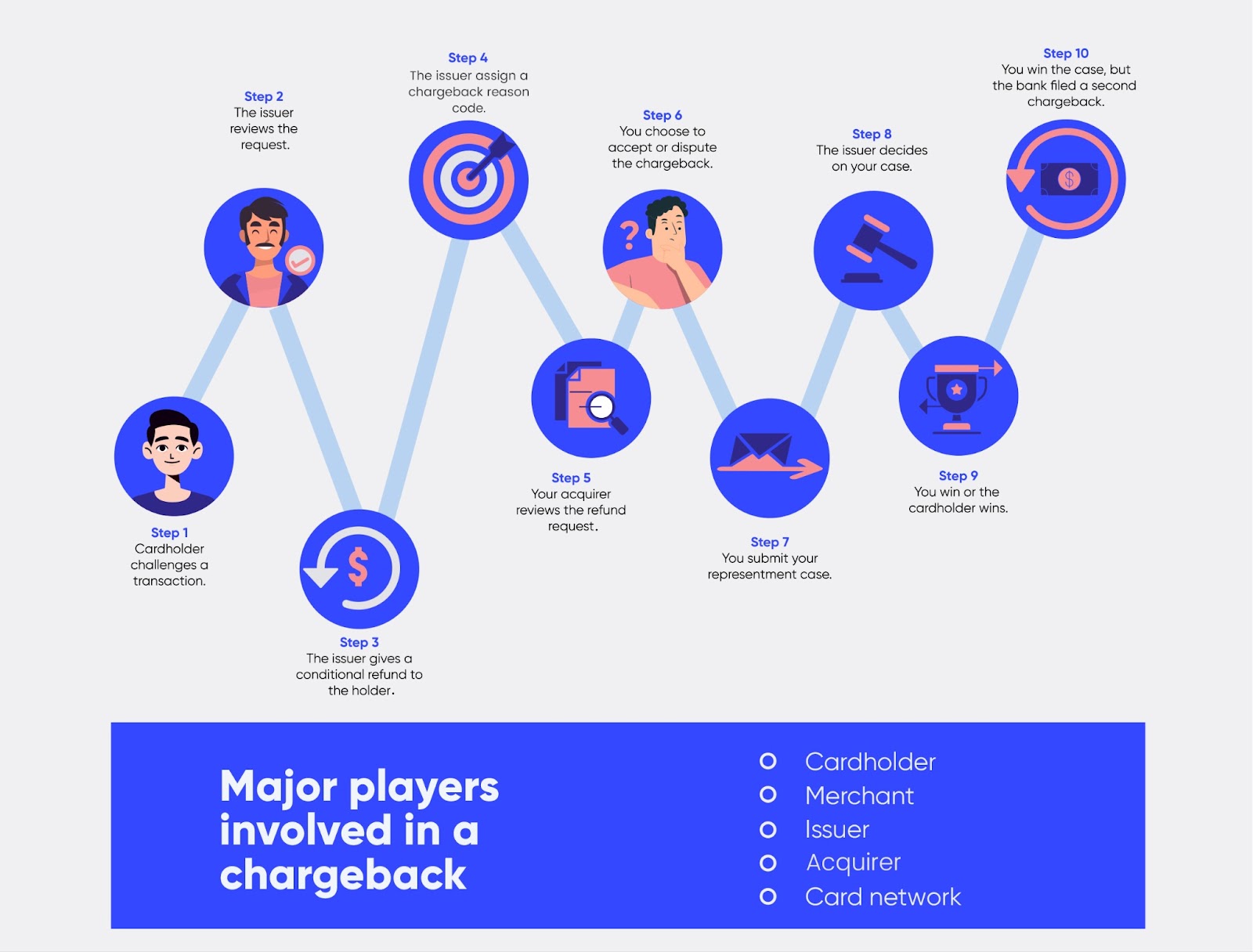

The Chargeback Process Step-by-Step

This is the credit card chargeback process as it actually plays out for merchants. Details vary by network and reason code, but the structure stays the same.

Step 1: A customer completes a transaction

A card payment has been approved, and the order has been fulfilled. At this stage, merchants generate the data that later determines whether a dispute can be won:

- Order confirmation and timestamps

- Billing and shipping details

- IP, device, and session data

- Delivery confirmation or access logs

None of this matters until it suddenly does. A faster route to chargeback recovery is to let automation handle the filings.

Step 2: The customer disputes the charge with their bank

Instead of contacting the merchant, the customer reaches out to their issuing bank and selects a dispute reason, such as fraud, not received, or not as described.

From this point on, the dispute is framed entirely through the bank’s categories. The customer’s version becomes the starting assumption.

For a deeper breakdown of how banks handle this stage, read How Does a Chargeback Work in detail.

Step 3: The issuing bank files the chargeback and removes the funds

The bank issues the chargeback through the card network. For the merchant, this usually means:

- The transaction amount is withdrawn

- A chargeback fee is applied

- A reason code and response deadline are assigned

The money moves before any review happens.

Step 4: The chargeback reaches the merchant

The acquiring bank or processor posts the chargeback to the merchant’s dashboard or sends a notification. Often this comes with limited detail and little time.

This is where chargeback processing breaks down for many teams. The clock is running, and the case file is thin.

Step 5: The merchant decides to accept or fight

This is the first real decision point. Many merchants lean on real-time chargeback alerts to intercept disputes early.

Accepting the chargeback

The merchant bears the loss, and the case is closed. This is common when the amount is small, the dispute is valid, or documentation is missing.

Fighting the chargeback

The merchant responds through chargeback representment, submitting evidence that directly addresses the reason code.

Learn how this works in detail in chargeback representment.

Step 6: Evidence is submitted and reviewed

Issuers don’t look for context. They look for proof that matches the reason code.

Effective evidence can include:

- Proof of delivery with address match

- Digital access or usage logs

- AVS and CVV results

- Clear refund and cancellation policies

- Customer communication records

In the retail chargeback process, delivery confirmation, return tracking, and clearly disclosed refund policies often determine whether a dispute is recoverable.

Generic or mismatched evidence usually fails, even if the merchant is right.

Step 7: The issuer makes a decision

After reviewing the submission, the issuer rules in favor of either the merchant or the cardholder.

- Merchant wins: funds are returned, fees often remain

- Merchant loss: funds stay reversed, dispute counts toward ratio

Even wins carry operational cost. Treating chargeback management as a system, not a fire drill, pays off.

Step 8: The dispute can escalate

Some cases don’t end after representment.

- Pre-arbitration: the issuer challenges the outcome

- Second chargeback: funds are reversed again

- Arbitration: the card network issues a final ruling, with high fees

These stages are strictly governed by chargeback rules, which is why most merchants stop before arbitration.

Step 9: Long-term impact shows up later

Once the case closes, the effects linger:

- Chargeback fees

- Increased dispute ratios

- Higher monitoring risk

- More customers are choosing disputes over support

The damage often compounds quietly.

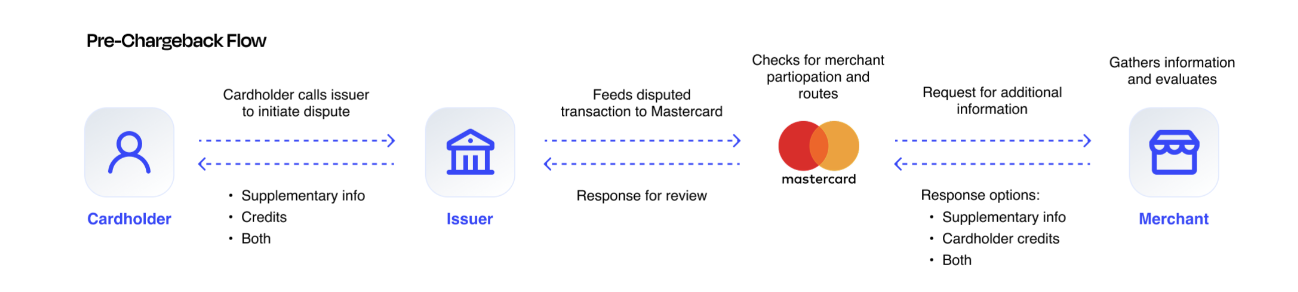

Chargeback Process Flow and Diagram Overview

If you mapped this as a chargeback process flow diagram, it would illustrate two things happening simultaneously.

Not every dispute immediately becomes a chargeback. In some cases, issuing banks first request additional information through card-network systems before deciding whether to escalate the dispute.

Funds are returned quickly from the merchant to the cardholder as soon as the chargeback is issued. Evidence moves slowly in the opposite direction, passing through the acquirer, network, and issuer before a decision is made.

That mismatch explains why merchants feel behind the moment a chargeback appears. Stopping the bleeding means learning to prevent chargebacks at the source.

What Happens After a Chargeback Is Filed

Once filed, a chargeback becomes part of your dispute history. Even low-value cases contribute to risk thresholds, and repeated disputes can trigger monitoring programs or processing restrictions.

This is why chargebacks aren’t just a support issue. They’re a risk signal.

How Merchants Can Dispute and Manage Chargebacks

The chargeback process is reactive by design. It assumes disputes will happen and focuses on reversing transactions after the fact.

For merchants, the real cost isn’t just the disputed amount. It’s the time, fees, ratios, and customer behavior that compound with every case.

That’s why teams that understand the process stop trying to “win” every dispute and start reducing how often they enter it in the first place, using early signals like chargeback alerts to intervene before a dispute becomes official.

What It Means to Accept a Chargeback

Accepting a chargeback means you don’t contest it. The funds stay reversed, the case closes, and the dispute still counts against your chargeback ratio.

There are plenty of situations where acceptance is the practical choice:

- The transaction value is low, and the time cost isn’t worth it

- The dispute is clearly valid (true fraud, real fulfillment failure)

- You don’t have the documentation needed to support the claim

- The deadline is too tight to gather evidence responsibly

The mistake is treating acceptance as “doing nothing.” It’s still a decision with consequences. High acceptance rates can train customers to skip support and go straight to their bank, especially if they get an easy win once. It also makes chargebacks feel routine internally, which leads to weaker tracking and slower response habits. A large share of disputes are really friendly fraud in disguise.

A clean rule of thumb: accept when the case is unwinnable or uneconomical, not because the workflow is annoying.

Pre-Arbitration, Second Chargebacks, and Arbitration Explained

Winning representment doesn’t always end the dispute. Some cases escalate, and each stage becomes more rules-heavy and expensive.

Pre-arbitration is when the issuing bank pushes back after representment, usually claiming the evidence didn’t address the reason code or introducing new information from the cardholder. For merchants, it often feels like the goalposts have moved, but this is a defined part of the process.

A second chargeback (often tied to pre-arb) is when the funds are reversed again after the issuer challenges the outcome. At this point, merchants have to decide whether the case is worth continuing.

Arbitration is the final step. The card network becomes the decision-maker and issues a binding ruling. The catch is cost: arbitration can involve significant fees, and the risk isn’t just losing the disputed amount. It’s paying additional penalties on top.

Most merchants avoid arbitration unless:

- The transaction value is high

- The evidence is unusually strong

- The reason code and timeline are clean

- There’s a repeat-abuse pattern worth drawing a line against

This is also where chargeback rules matter most. Deadlines get tighter, documentation standards get stricter, and process errors become automatic losses.

Simplify the Entire Chargeback Process

You can respond to every stage of the chargeback lifecycle automatically instead of managing it manually. Chargeflow automates the process end to end, backed by a 4X ROI guarantee.

Start for FreeChargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)