%201.svg)

Why Do Customers File Disputes After a Refund?

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

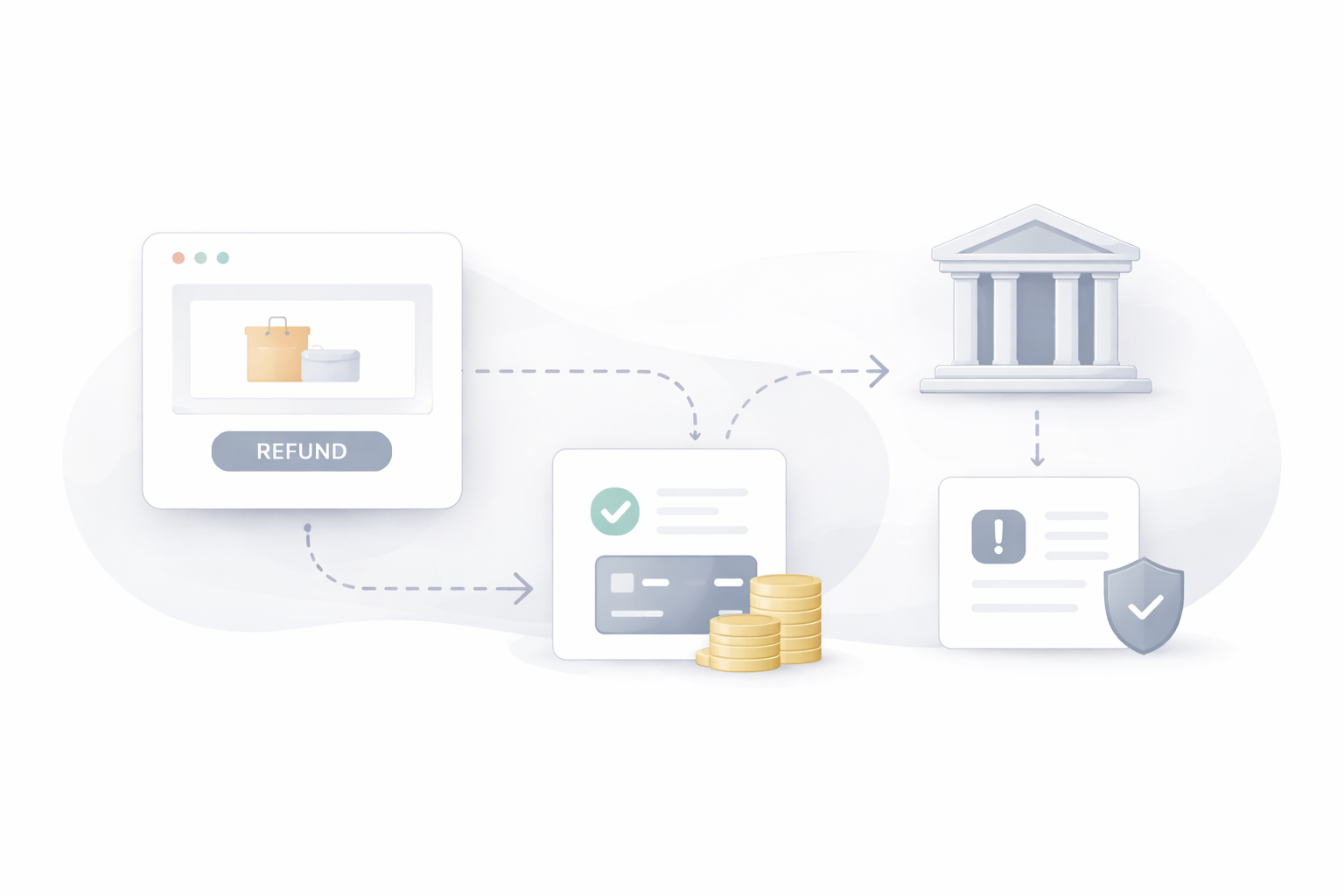

Customers dispute after a refund when they think it failed, took too long, or was only partial. A refund does not prevent a chargeback, but clear timing and visible proof of refund usually stop it, or win it.

Short Answer

Customers file disputes after a refund when they think the refund failed, took too long, or was only partial. Many do not understand how card refunds work, so they go to their bank before the refund finishes processing. Banks then open a dispute even though the merchant already issued the refund.

Can a customer file a chargeback after being refunded?

Yes. A refund does not prevent a chargeback. A customer can still dispute a charge with their bank even after you issue a refund, because the two systems do not talk to each other in real time. The good news: if you can show the refund was issued before the dispute date, issuers will typically reverse the chargeback so you are not debited twice. Merchants who already refunded win these representments often — as long as they submit the refund receipt, date, and transaction ID.

How long do refunds take to settle?

Steps to Solve the Problem

- Set refund timing expectations clearly

Tell customers exactly how long refunds take on cards. “5–10 business days” should be visible in the confirmation and follow-up email. - Send proof that the refund was issued

Always send a refund confirmation with the amount, date, and last four digits of the card. This reduces panic-driven disputes. - Watch for partial refunds

Shipping, taxes, or restocking fees often cause confusion. Make partial refunds obvious before the customer agrees. - Refund fast on high-risk cases

If a customer is upset or already threatening a dispute, speed matters more than policy enforcement. - Track repeat refund disputes

If the same customers or products keep triggering post-refund disputes, fix the process upstream. Chargeflow Insights helps surface these patterns. - Respond cleanly when disputes still happen

When a dispute is filed after a refund, submit proof of refund immediately. Chargeflow Automation helps ensure the evidence is complete and on time.

Platform or Use Case Variations

Stripe: Refunds may show as “pending” for days, which drives disputes if not explained, the Stripe integration keeps refund and dispute data in sync.

PayPal: Customers often dispute even after seeing a refund marked as completed.

Subscriptions: Customers dispute when refunds overlap with renewals or billing cycles.

Evidence Needed

Banks typically expect:

• Refund receipt or confirmation

• Refund date and amount

• Transaction ID linking the refund to the original charge

• Proof the refund was processed before the dispute date

• Communication showing the customer was informed

For context on how these representments are judged, see how issuers evaluate chargeback disputes and this primer on the credit card chargeback process.

Why This Happens

Refunds are slow, banks are fast, and customers do not trust timelines they cannot see. When anxiety spikes, the bank becomes the shortcut.

Disputes after refunds usually stop when refund timing is clear, proof is visible, and Chargeflow helps merchants track and respond before banks escalate the issue.

Frequently Asked Questions

Can a customer file a chargeback after being refunded?

Yes. A refund does not prevent a chargeback because refunds and disputes run on separate rails. If you can prove the refund was issued before the dispute, the issuer will usually reverse the chargeback.

Why do customers dispute after getting a refund?

Usually because the refund had not settled yet, was only partial, or was not clearly communicated. Anxious customers go to their bank instead of waiting for the card refund to appear.

How long do card refunds take?

Most card refunds settle in 5–10 business days. PayPal balance refunds are near-instant, while PayPal-to-card and bank transfers take 3–5 business days.

What evidence wins a post-refund chargeback?

The refund receipt, refund date and amount, the transaction ID linking it to the original charge, proof it processed before the dispute, and communication showing the customer was informed.

How do I stop disputes after refunds?

State refund timing up front, send a refund confirmation with amount and card last four, make partial refunds obvious, and use Chargeflow to track repeat patterns and respond fast.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)

More articles.

How Do I Track Dispute Performance Across Multiple Accounts?

To track dispute performance across multiple accounts, consolidate chargeback data from every processor, store, and merchant account into one dashboard, then compare the same core metrics, dispute rate, win rate, recovery rate, and reason-code trends at both account and portfolio level. Centralized reporting surfaces rising-risk accounts before they trip card-network thresholds like Visa’s VAMP.

How Do I Standardize Evidence Across Dispute Types?

Standardize chargeback evidence by building one core evidence package for every order, transaction, fulfillment, customer, and policy records, then layering in dispute-specific proof mapped to the reason code. A single repeatable framework beats managing evidence reason code by reason code: it closes gaps, speeds responses, and lifts win rates.

How Do I Align Customer Support and Payments to Reduce Disputes?

Many chargebacks start as unresolved support issues, not payment problems. When customer support and payments share one dispute-prevention queue, escalation rules, and pre-chargeback alert data, you resolve refund, delivery, and billing complaints before they reach the issuing bank.

Questions?

we’ve got answers.

Chargeflow collects data from dozens of third party signals, not just transaction data like Stripe Dispute does. This allows for much more coverage and much better win rates because the evidence submitted is much more comprehensive and compelling..

Chargeflow collects data like order info, customer messages, and payment details. It builds a full dispute case for you, so you don’t have to lift a finger.

Yes! Chargeflow works with many processors — not just Stripe. That means one tool for all your chargebacks, no matter how you process payments.

You only pay a percentage of the revenue we help you recover. No upfront fees, no subscriptions — just success-based pricing.

Yes. Chargeflow is SOC 2, GDPR, and ISO certified. We use top security standards to keep your data safe.

need more help?

Have a question? We’re here to help. Just hit the chat button to initiate a conversation with support.