%201.svg)

ACH chargebacks: Everything You Need To Know

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

ACH payment is a bank-to-bank computer-based digital payment exclusive to U.S. bank and credit union accounts. ACH transactions attract chargeback too.

TL; DR: ACH payment is a bank-to-bank computer-based digital payment that can reach all U.S. bank and credit union accounts. Although not covered under the Fair Credit Billing Act, ACH transactions are not immune to chargebacks, popularly called ACH returns. The primary sources of ACH returns include administrative returns, authorization revocation, duplicate entries, email phishing scams, and insufficient funds.

ACH chargebacks (or, more accurately, ACH returns) are becoming increasingly prevalent in the financial industry. According to a report by the National Automated Clearing House Association (NACHA), the number of ACH Chargebacks has steadily increased over the past few years, resulting in millions of dollars in business losses. Estimates show that in 2020 alone, there were over 900,000 ACH chargebacks, amounting to $1.2 billion in losses.

Like traditional chargeback issues, ACH chargebacks can have severe consequences on business, not limited to significant financial losses but even legal action.

If you’re hearing about ACH chargebacks for the first time, don’t worry. We’ll dive into all the “whats” and “hows,” including causes, prevention strategies, and the impact of ACH chargebacks on businesses to ensure you’re not disadvantaged.

What is ACH?

Automated Clearing House (ACH for short, or ACH network/ACH scheme) is a network that facilitates money transfers between bank accounts electronically across the U.S.

Nacha (previously NACHA - National Automated Clearing House Association) runs the network, and the system has been around since the 1970s.

On transaction volume, industry records show that ACH moved over $72.6 million worth of financial transactions in 2021 alone. And the network has demonstrated steady growth – with 7.6 billion payments processed at $19.2 trillion in the third quarter of 2022, representing increases of 4.2% and 6%, respectively, from 2021.

With that vital data and the definition of ACH noted, let’s look at ACH payments, what they are, and why they’re becoming fashionable these days.

What is an ACH payment?

An ACH payment is a bank-to-bank computer-based digital payment that can reach all U.S. bank and credit union accounts. These payments, commonly known as ACH transfers or ACH transactions, go through the ACH network instead of card networks like Visa or Mastercard.

The two main branches of ACH payments include Direct Deposit and Direct Payment.

Direct Deposit caters to every deposit payment from companies or governmental agencies to an individual, including payroll (get insights into full payroll guide), employee expense reimbursement, government benefits, tax, and other refunds, annuities, and interest payments.

While Direct Payment deals with electronically transmitting payment instructions between financial institutions through the ACH network.

While both systems use ACH to process electronic transactions, there are critical variances between them, such as the following:

- Purpose: Direct Deposit is primarily for depositing funds into a recipient's bank account, typically for payroll purposes. On the other hand, Direct Payments are for making payments to a recipient's bank account, such as for bills, taxes, etc.

- Authorization: For Direct Deposit ACH, the recipient typically authorizes the transfer of funds to their account, often through an employment agreement with their employer. For Direct Payments ACH, the payer allows the transfer of funds to the recipient's account, often through a contract with a service provider or financial institution.

- Frequency: Direct Deposit ACH is typically ideal for recurring deposits, such as regular paychecks. Direct Payments ACH, on the other hand, is for one-time or recurring payments.

- Information Required: For Direct Deposit, the recipient typically provides their bank account and routing number to the payer. For Direct Payments, the payer needs the recipient's bank account and routing number, payment amount, payment frequency, and payment date.

The main difference between Direct Deposit and Direct Payments is that the former is for depositing funds into an account, while the latter is for making payments from a bank account.

Regarding utility value, ACH payments have some advantages over credit card payments in that they usually have lower processing fees and no expiration date for recurring payments.

Yet, ACH payments are not immune to chargebacks, as we’ll explore below.

What is ACH Chargebacks?

An ACH chargeback (or return) occurs when a receiving bank reverses an ACH transaction. ACH transactions are not under the Fair Credit Billing Act like credit card transactions. However, buyers can still reverse payments made through the ACH network in what constitutes their variation of the chargeback mechanism.

Also, in the case of failed transaction processing, one of the participating financial institutions may receive an ACH return – informing the institution that the bill in question either could not be realized from or remitted into the requisite account.

The Receiving Depository Financial Institution (RDFI) or receiving bank sends the return (or chargeback) notification informing the Originating Depository Financial Institution (ODFI) or originating bank that the ACH Network either couldn’t collect funds or couldn’t deposit funds into the receiver’s account.

Here’s what you need to know about the causes and sources of ACH payment reversals and how to avoid them.

Causes and Sources of ACH Chargebacks

Like traditional card network chargebacks, there are several reasons why a consumer can file an ACH chargeback. Let’s look at the most prominent reasons.

#1: Administrative Return

An administrative return is the most prevalent ACH chargeback, resulting from data entry mistakes. Examples include when the transaction's information is incorrect, an improper transaction code, wrong routing numbers, incorrect account numbers, or credit is unintentionally sent to the receiver during the return process.

In the event of an administrative return, the ACH transaction credits back to the customer's account; the monies are refunded to the bank initiating the transaction. The bank or payment processor often charges the party involved a fee for the administrative return.

To avoid administrative ACH chargeback, ensure all client information is valid and current before processing the transaction. Simple due diligence you can carry out includes:

- Double-checking the transaction codes,

- Reviewing the account and routing information,

- Ascertaining that the consumer has enough money to pay for the transaction.

- Additionally, you can set up automatic notifications for any ACH transaction hiccups with your bank or payment processor to ensure you can identify cases promptly and fix them.

#2: Authorization Revocation

Authorization revocation happens when a consumer withdraws consent for a recurring ACH transaction. Customers do this when they want to end a subscription or membership or contest the charges from a previous purchase. When a buyer revokes authorization, the ACH transaction funds will be credited to the customer's account, and the transaction will be reversed. That also means an imposed fee for the authorization revocation.

Avoid such inconvenience by establishing clear and open policies for canceling recurring transactions and making it simple for customers to revoke their authorization if they so desire. That includes providing clear instructions for canceling subscriptions or memberships.

You can also set up automatic notifications for authorization revocations with your bank or payment processor.

#3: Duplicate Entry

Duplicate entry ACH chargeback occurs when a seller or financial institution processes the same transaction more than once, resulting in multiple identical transactions. That could result from a technical error in the payment processing system or a miscommunication between the business and its bank or payment processor.

As with the previous issues highlighted, duplicate entry ACH chargeback attracts payment reversal and an imposed administrative fee.

Establish adequate checks and balances to avoid repeated entries. You could achieve that by conducting manual inspections to find inaccuracies or using automated tools and systems to detect and prevent duplicate entries. Again, you can set up automatic notifications for duplicate entries with their bank or payment processor.

#4: Email phishing ACH scams

Like legacy phishing scams, email phishing ACH scams are when fraudsters send fraudulent emails that seem to be coming from a reputable financial institution or company. The victim receives a prompt to enter their personal or financial information, which the scammers can use to make unauthorized transactions or steal the victim's identity. Usually, the emails have a link or attachment that, when opened, takes the victim to a false website that imitates the real one.

Once the victim realizes it's a scam, they may initiate a chargeback request to dispute any unauthorized transactions that occurred as a result.

To prevent email phishing from ACH scams:

- Educate your customers on such fraud patterns.

- Never click on links or attachments in unsolicited emails, and always double-check the URL of the website you’re visiting to ensure legitimacy.

- Implement multi-factor authentication and other security measures to prevent unauthorized account access.

#5: Insufficient funds

ACH chargebacks due to insufficient funds occur when the account holder does not have enough funds to cover an ACH transaction, resulting in a return to the originating bank.

As with the above instances, the Receiving Depository Financial Institution (RDFI) or receiving bank must notify the Originating Depository Financial Institution (ODFI) or originating bank within two banking days. The ODFI must then determine if they want to attempt the transaction again or if they want to cancel the transaction.

If the ODFI cancels the transaction, they can request a chargeback from the RDFI to recover the funds. The RDFI will return the funds to the ODFI, and they’ll debit the account holder for the transaction amount plus any applicable fees, which typically range from $2-5 (per issue).

To avoid insufficient funds for ACH chargebacks, ensure the buyer has enough money to pay for the transaction before processing it. And strictly follow all NACHA guidelines.

How Should Sellers Handle ACH Returns?

Unlike credit card chargebacks, vendors have no written rules for disputing ACH returns.

The National Automated Clearing House Association (NACHA), the governing body for the ACH network, still needs to establish standard procedures for handling false ACH chargebacks.

If you face a meritless return, you could try to work things out with the buyer. If the customer is not bent on committing friendly fraud, estimates show that you have a 25% chance of success in resolving the issue.

Further, you can hire an attorney to seek legal remediation of the case. And if all else fails, you could try the good old lawsuit option and have your lawyers fight the case. Industry analysis says merchants who explored this route saw a 31% increase in revenue recovery.

That said, it’s equally vital to note that banks are way more cautious in granting ACH chargebacks than traditional chargebacks. While that’s some good news, it doesn’t mean you’ll have no problems. Every bank transfer that ultimately gets reversed causes significant damages not limited to lost revenue. For ODFIs, too many ACH returns could lead to losing network privileges.

Dishonoring ACH Returns

Suppose that an ACH return needed to be more adequately authorized. The receiving party can request an ACH return reversal or dishonoring in that case.

The party must transmit a dishonored return to the RDFI within five banking days of the settlement date of the return. And they can dishonor an ACH return under the following terms:

- ACH return is untimely (not within the stipulated time frames for return)

- Return request contains wrong information

- The return request was routed to the wrong account

- ACH return is a duplicate of another return already issued

- The return request resulted in an unintended credit to the Receiver related to the reversal process.

That said, let’s look at the return codes.

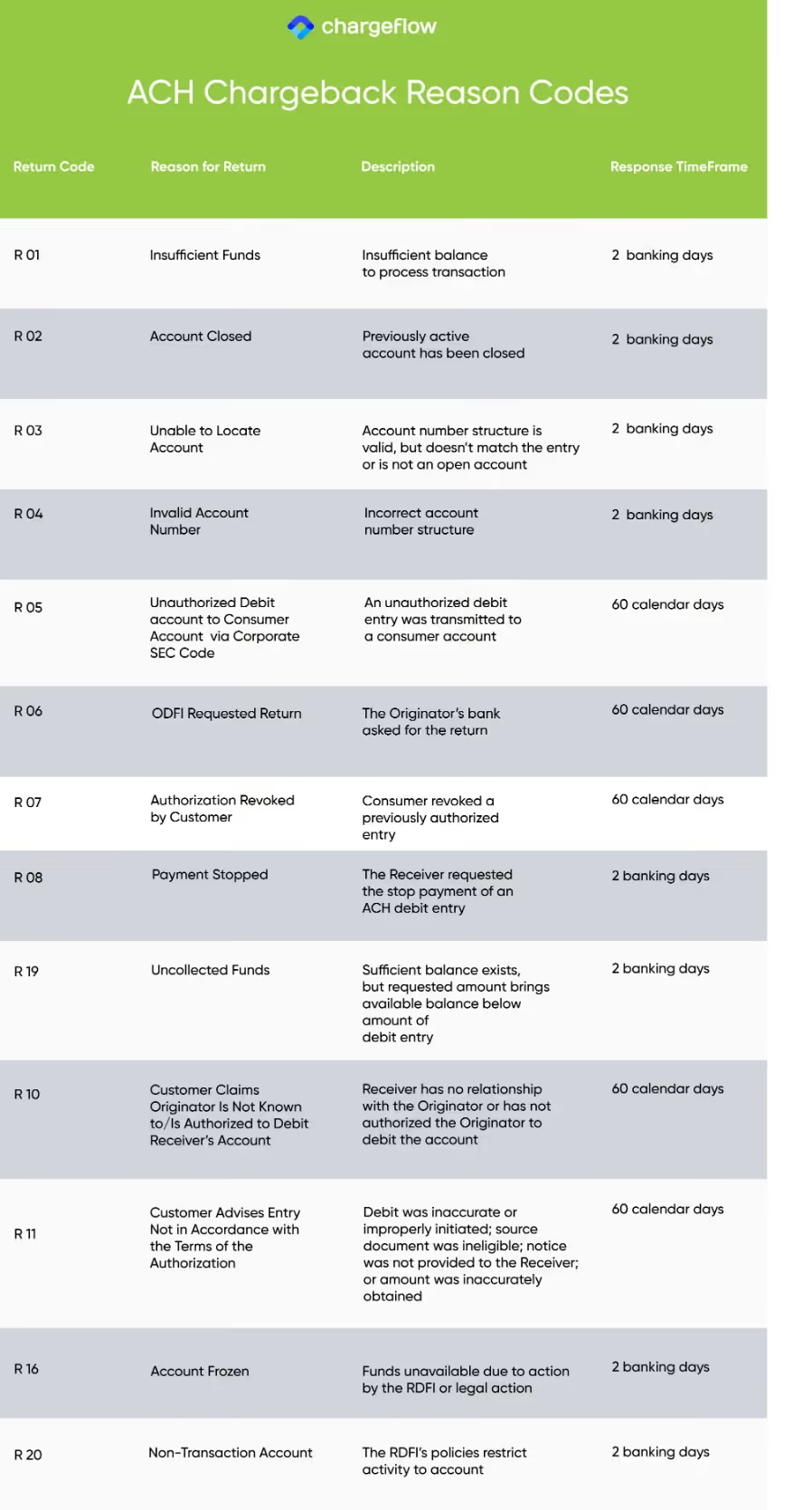

Understanding ACH Return Codes

Like traditional chargeback reason codes, an ACH return code indicates why the RDFI initiated the transaction reversal request. It’s a 3-digit alphanumeric shorthand attached to a returned ACH transaction explaining why an ACH transfer is reversed.

There are over 80 unique return codes, each representing a different return type. Below are the principal ACH return reason codes and the timelines within which one can request an ACH chargeback under each code:

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)

.avif)