%201.svg)

What is Friendly Fraud? Chargeback Fraud Explained for Merchants

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 15,000 merchants.

Friendly fraud is when a real customer disputes a legitimate charge with their bank. It’s a form of chargeback fraud, but it’s driven by cardholder behavior, not stolen cards. In many ecommerce verticals, friendly fraud accounts for most chargebacks. Left unchecked, it raises dispute ratios and can push merchants into monitoring programs for card networks. Reducing it requires better post-purchase design, clearer communication, and structured dispute management, not just fraud tools at checkout.

Chargebacks were built to protect consumers from real fraud.

Today, a large share of them comes from legitimate customers.

Many merchants invest heavily in stopping stolen cards at checkout, only to see disputes climb anyway.

The reason is friendly fraud.

If you’re trying to understand what is friendly fraud chargeback is, how it differs from chargeback fraud, and why it keeps increasing even when fraud tools improve, this is the problem to look at.

Friendly fraud isn’t just a fraud issue. It’s a post-purchase behavior issue. And for many brands, it’s the largest driver of dispute rates.

- What is Friendly Fraud?

Friendly fraud is when a legitimate customer disputes a valid transaction with their bank instead of contacting the merchant for a refund.

The cardholder made the purchase.

The payment was authorized.

The product was delivered, or the service was used.

Then a chargeback hits.

That’s the friendly fraud chargeback definition in simple terms.

When merchants search “what is friendly fraud chargeback,” they’re usually trying to determine whether this is actual fraud or just confusion.

It’s both.

In many ecommerce segments, especially subscription and digital goods, friendly fraud represents the majority of disputes.

Industry research consistently shows that a large share of ecommerce chargebacks come from cardholders disputing legitimate transactions rather than true criminal fraud.

It’s not rare behavior. It’s structural.

- Friendly Fraud vs. Chargeback Fraud: What’s the Difference?

Is chargeback fraud the same as friendly fraud?

No. Friendly fraud is one type of chargeback fraud, but not all chargeback fraud is friendly fraud.

So when comparing friendly fraud vs. chargeback fraud:

- All friendly fraud is chargeback fraud.

- Not all chargeback fraud is friendly fraud.

If a stolen card is used, that’s criminal fraud.

If a real customer buys, receives, and later disputes the transaction, that’s friendly chargeback fraud.

The distinction matters because the prevention strategy is different.

Criminal fraud is solved at authorization.

Friendly fraud is solved after the sale.

- What Causes Friendly Fraud (and Why It’s Growing)

Friendly fraud and chargeback fraud have grown with ecommerce, but scale alone doesn’t explain it.

Three structural drivers matter more.

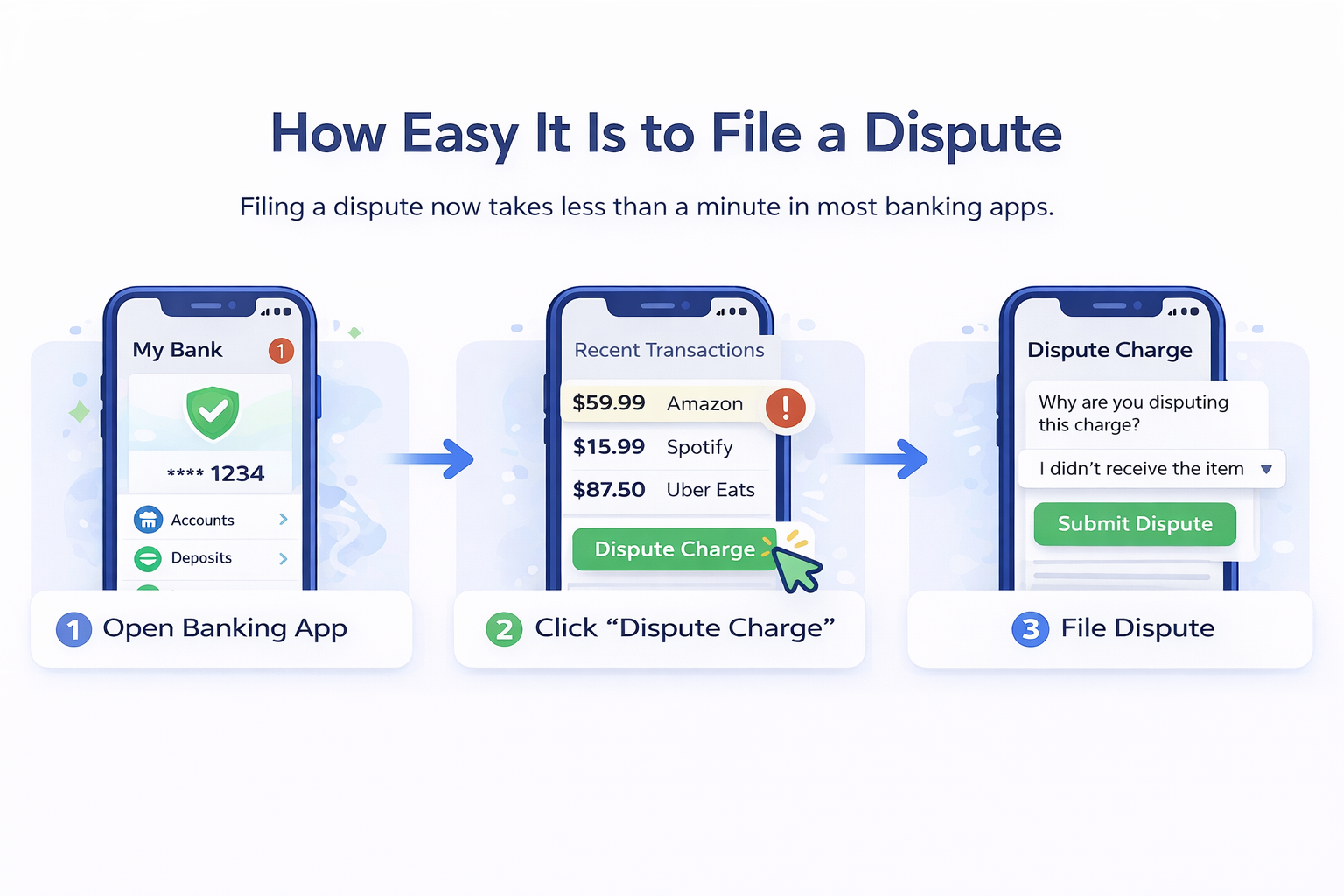

Frictionless disputes

Banking apps now allow cardholders to dispute a charge in seconds. Often, provisional credit is issued immediately.

From the customer’s perspective, it feels fast and low risk.

Refund friction

If your return process is slow, restrictive, or confusing, some customers will bypass it.

A chargeback becomes the shortcut.

Subscription and descriptor confusion

Recurring billing, unclear statement descriptors, and shared household cards create “I don’t recognize this” disputes.

Issuers are built to protect cardholders. Merchants carry the burden of proof.

That incentive structure shapes behavior.

Friendly fraud is not just a customer issue. It’s a system outcome.

- Accidental vs Deliberate Friendly Fraud

Not all friendly fraud is malicious. But the cost to merchants is the same.

Accidental friendly fraud

- A parent disputes a gaming charge made by a child.

- A customer forgets a subscription renewal.

- The billing descriptor is unclear.

Deliberate friendly fraud

- The package shows delivered, but the customer claims it never arrived.

- A user consumes digital content and disputes afterward.

- A shopper misses the return window and files a chargeback instead.

Both result in a friendly fraud chargeback.

For a $20M ecommerce brand sitting at a 0.8% dispute rate, even a small spike in “no authorization” claims can push them toward card network monitoring thresholds around 0.9% to 1%.

Intent doesn’t change the ratio.

- Types of Friendly Fraud

Buyer’s Remorse

Common in apparel and electronics. Instead of returning it, the customer regrets the purchase and disputes it.

Family Fraud

Frequent in gaming and subscription businesses. One household member purchases, another disputes.

Refund Abuse

The customer keeps the product and files a dispute.

Cyber Shoplifting

Common in digital goods. The customer downloads, streams, or accesses the service, then disputes.

In some digital verticals, the majority of fraud-coded disputes are actually post-consumption friendly fraud.

Calling all of it “fraud” hides the behavior driving it.

- Friendly Fraud on the Chargeback Spectrum

Fraud exists on a spectrum.

At one end, stolen cards and organized crime.

At the other, genuine confusion.

Friendly fraud sits in the middle.

It blends convenience, frustration, policy friction, and opportunism.

If disputing is easier than requesting a refund, disputes rise.

Chargeflow’s Psychology of Chargebacks report shows that many consumers who file disputes don’t view their actions as fraud. They often perceive the bank as a neutral problem solver and the dispute button as a faster resolution path. When the issuer interface feels simpler than contacting the merchant, behavior follows convenience.

- How Friendly Fraud Hurts Businesses

A friendly fraud chargeback costs more than the transaction amount.

You lose:

- Revenue

- Cost of goods

- Shipping and fulfillment

- Chargeback fees

- Operational time

Then there’s the ratio impact.

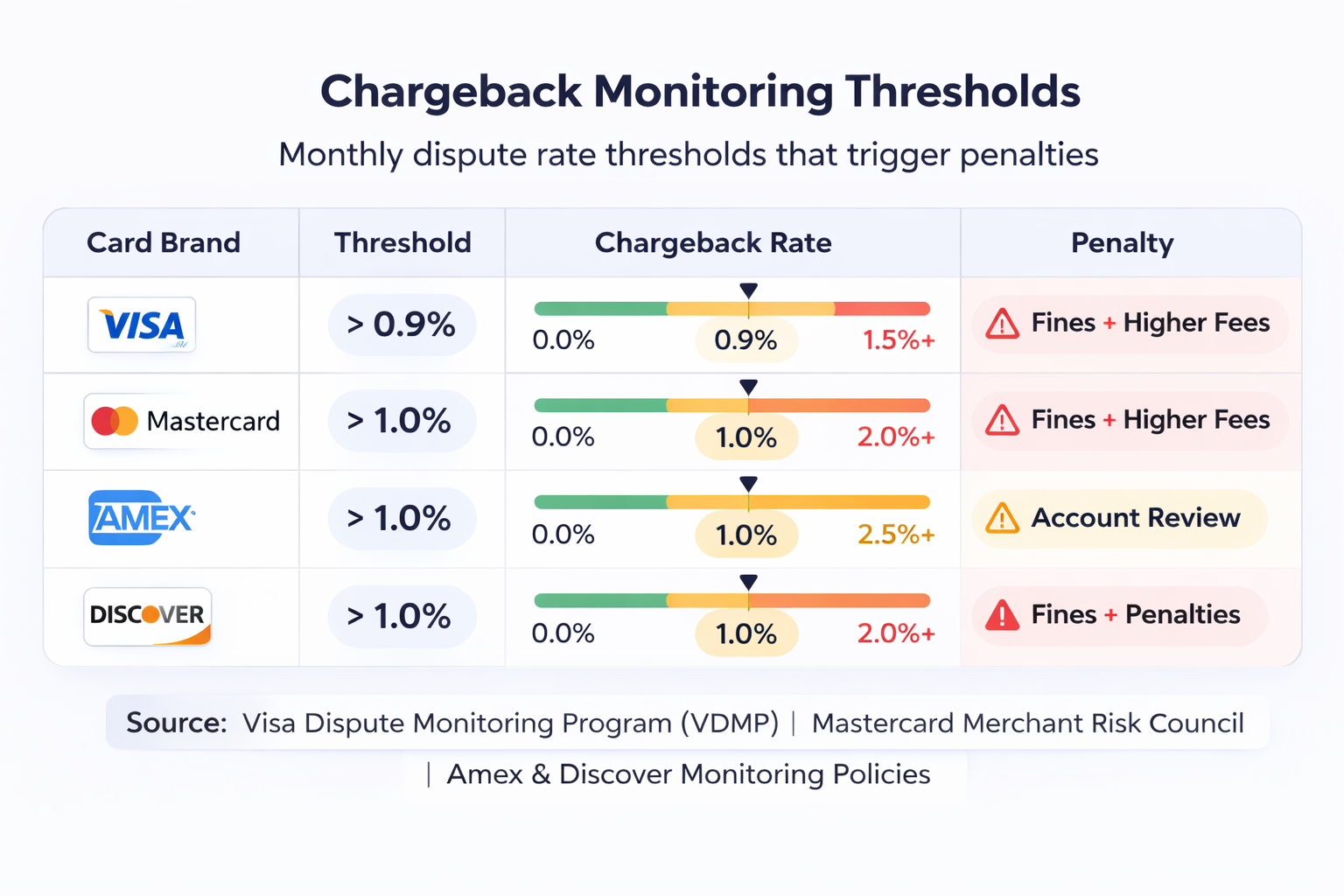

Cross network thresholds, and you enter monitoring programs. That can mean higher processing costs and required remediation plans.

For example, Visa’s Chargeback Monitoring Program and Mastercard’s Excessive Chargeback Program outline specific dispute rate bands that determine when merchants are placed under review or face penalties.

For many growth-stage brands operating near card network thresholds, even a 0.3% to 0.5% increase in dispute rate can materially impact margins.

- Consequences of Friendly Fraud for Consumers

Consumers often treat chargebacks as a refund alternative.

Banks track dispute behavior.

Repeated friendly chargeback fraud can trigger account reviews, reduced dispute privileges, and, in extreme cases, account closure.

Most customers never see this side of the system.

But issuers do.

- How to Prevent Friendly Fraud

Chargeback prevention for friendly fraud begins after checkout.

Most merchants overinvest in stopping stolen cards and underinvest in post-purchase clarity.

If you want to reduce chargeback friendly fraud, remove the friction that pushes customers toward their bank.

Make your billing descriptor recognizable

The name on the statement should clearly match your storefront brand.

Send renewal reminders before billing

Send reminders 5 to 7 days before subscription renewals. Include the date, amount, and a direct cancellation link.

Remove friction from cancellations

If cancellation requires multiple steps or hidden portals, some customers escalate to their bank instead.

Strengthen delivery documentation

Use signature confirmation for high-ticket items and store carrier timestamps.

Track repeat dispute behavior

Flag repeat cases of friendly fraud and adjust risk controls accordingly.

Make support visible everywhere

Order confirmations, receipts, and shipping emails should clearly show how to contact you.

Prevention is an operational discipline. The fewer surprises customers experience after checkout, the fewer disputes you’ll see.

- How to Respond to Friendly Fraud (and Fight It Successfully)

When prevention fails, evidence determines outcomes.

Winning a friendly fraud chargeback requires the following:

- Proof of authorization

- Delivery confirmation

- IP and device data for digital goods

- Clear refund and cancellation policy records

- Customer communication logs

The goal is to demonstrate that the transaction was valid and fulfilled under disclosed terms.

Structured representment turns disputes into a controllable process instead of recurring loss.

- The Bottom Line on Friendly Fraud

Friendly fraud is not a niche issue.

For many ecommerce brands, it is the dominant source of chargebacks.

You can reduce authorization fraud and still lose margin to friendly fraud chargebacks.

Merchants who treat friendly fraud as a behavioral and operational problem protect their dispute ratio, recover revenue others write off, and avoid unnecessary network scrutiny.

Chargebacks are often framed as a cost of doing business.

Friendly fraud shows they are a design problem.

And design problems can be fixed.

Want to understand why customers dispute legitimate transactions?

Read The Psychology of Chargebacks to understand why customers dispute legitimate transactions and how better post-purchase design reduces preventable chargebacks.

If you’re ready to move from insight to execution, see how Chargeflow automates dispute management end-to-end.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 15,000 merchants.

.png)

Questions?

we’ve got answers.

Chargeflow collects data from dozens of third party signals, automatically. This allows for much more coverage and much better win rates because the evidence submitted is much more comprehensive and compelling.

Chargeflow collects data like order info, customer messages, and payment details. It builds a full dispute case for you, so you don’t have to lift a finger.

Yes! Chargeflow works with 50+ payment processors. That means one tool for all your chargebacks, no matter how you process payments.

You only pay a percentage of the revenue we help you recover. No upfront fees, no subscriptions — just success-based pricing.

Yes. Chargeflow is SOC 2 Type 2, GDPR, and ISO certified. We use top security standards to keep your data safe.

need more help?

Have a question? We’re here to help. Just hit the chat button to initiate a conversation with support.