%201.svg)

How Does a Chargeback Work? A Step-by-Step Guide

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 15,000 merchants.

A chargeback is a forced transaction reversal. Your bank pulls the funds back before you get a say. Unlike a refund, you don't agree to it. A cardholder disputes a transaction with their issuer, and the money leaves your account immediately, along with a non-refundable fee. Win the dispute, and you get it back. Lose, or ignore it, and the cost compounds fast. The rules have become stricter, the windows are shorter, and the merchants who understand how this works are the ones who keep their money.

Ask any eCommerce merchant about recent noteworthy shifts in payments. You’ll likely hear the same answers. New regulations (like the GENIUS Act), faster settlement rails, and the steady rise of digital wallets.

What many merchants underestimate, however, is a quieter but far more consequential change: how card networks now enforce risk at scale.

Programs like the updated Visa’s Acquirer Monitoring Program (VAMP) don’t just track individual merchants. They pressure entire acquirer portfolios. Understanding how chargebacks work is no longer a back-office admin chore. It’s now a critical part of how merchants protect their revenue.

Chargeback volumes are surging at record levels. The rules governing them are equally unforgiving. Businesses that wish to avoid processor wrath must play by a complicated set of rules created by banks and card networks.

That’s why we put this guide together. Whether you’re launching your first store or just want a clearer picture of how a chargeback works in 2026, we’ll break everything down step by step. By the end, you’ll gain expert insights to confidently navigate card disputes and avoid unnecessary losses.

What is a Chargeback and How Does a Chargeback Work?

At its core, a chargeback is a consumer protection mechanism. It allows a cardholder to dispute a transaction directly with their bank when fraud, non-receipt, or unresolved issues occur. They can bypass the merchant and go directly to their bank to demand a funds reversal. Unfortunately, that system has evolved into a multi-billion-dollar challenge for the entire eCommerce ecosystem.

How does a chargeback work on a credit card? Unlike a standard refund, which is a voluntary agreement between a buyer and seller, a chargeback is a forced transaction reversal. The funds are immediately withdrawn from the merchant’s account, often accompanied by a penalty fee, before the merchant even has a chance to tell their side of the story.

Key Players Involved in a Chargeback

The chargeback ecosystem is a "four-party model" in addition to modern intermediaries:

- The Cardholder: The dispute instigator.

- The Issuing Bank: The cardholder's bank (e.g., Chase, Barclays) that judges the initial validity of the claim.

- The Merchant: You, the party defending hard-earned revenue.

- The Acquiring Bank/Processor: The merchant's partner (e.g., Stripe, Adyen) that facilitates funds movement.

- The Card Network: Visa or Mastercard, acting as the ultimate "Supreme Court" if the dispute escalates to arbitration.

Below is a full breakdown of the chargeback process and how these parties interact:

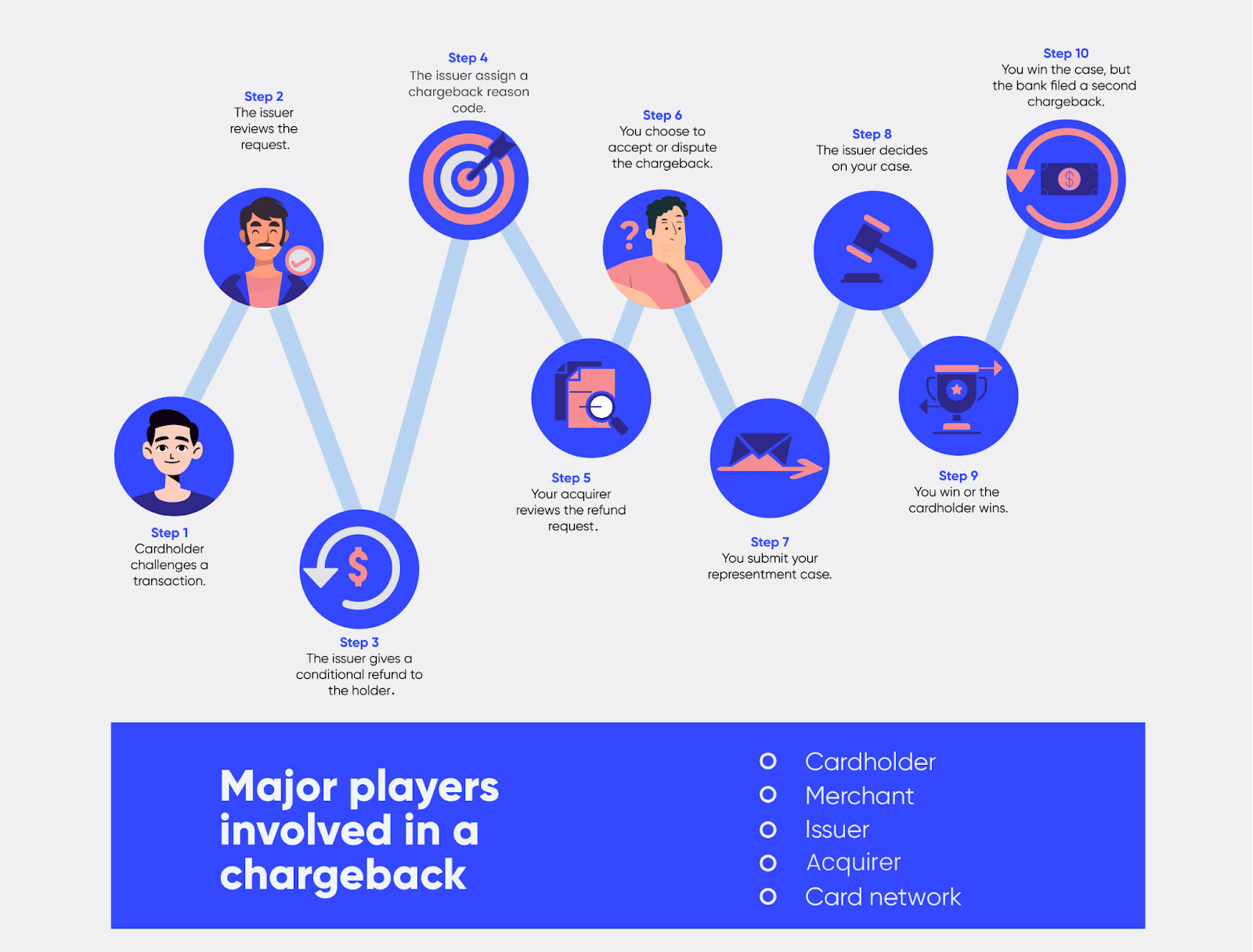

How Does a Chargeback Work? Step-by-Step Process

- Cardholder Initiates a Dispute: The process begins when a customer contacts their bank. Whether through a mobile app or phone call, they trigger the dispute under specific "reason codes." In 2026, the standard window is generally up to 120 days, though this can vary by reason code. Some disputes can extend much longer under certain conditions.

- The Issuing Bank Reviews and Investigates: The bank performs a "triage." If the claim seems plausible, they grant the customer a provisional credit. How does a bank chargeback work at this stage? The bank essentially "borrows" the money back from the merchant’s processor to satisfy its customer.

- The Merchant Is Notified, and Funds Are Pulled: Notification is mostly instantaneous. Your payment gateway will flag the dispute, and the transaction amount, plus a non-refundable chargeback fee ($15–$100), is debited from your merchant balance.

- The Merchant Responds With Representment Evidence: This is where the battle is won or lost. The merchant submits a chargeback representment package. The evidence must be surgical.

- Pre-Arbitration or Second Chargebacks: If you, the merchant, win the first round, the bank may "push back" with a second dispute (pre-arbitration). This signals that the cardholder has provided new information or is doubling down on the claim.

- Arbitration and Card Network Ruling: If neither side concedes, the case goes to arbitration. This is the final stage. Be aware: Arbitration attracts up to $1350 if a Visa card is involved; see full details in our Visa chargebacks guide.

With all that said, let’s examine how you can win false credit card chargebacks today without hurting your conversion rates.

How Merchants Dispute and Win Chargebacks

The way merchants dispute and win chargebacks has changed.

The anatomy of winning chargeback disputes shows that treating these claims like "customer service disputes" is so 1996. Why? Because the best story doesn’t win anymore.

Today, banks won't read narratives. They scan for technical data consistency.

Disputes have shifted from a "legal argument" to a binary data match. To win chargebacks today, you don't write a “letter.” You provide a golden record of evidence.

The 3 Core Pillars of a Winning Dispute Strategy

1. Liability Shift Through CE 3.0

One of the most effective ways to win a dispute is to prevent it from counting against you entirely. Under Compelling Evidence 3.0 (CE 3.0) rules, if you can provide a historical footprint of two prior undisputed transactions (between 120–365 days old) that match the current dispute’s IP Address or Device ID, Visa shifts the fraud liability back to the bank.

2. Speed as a Metric, Not a Goal

Response windows have tightened to as little as 7–9 days for many processors. In the "binary" world of 2026 adjudication, a late response is a 100% loss. Top-tier merchants use Real-Time Dispute Ingestion to submit evidence packages within minutes, not days.

3. Precision "Data Nuggets" Over Document Volume

As highlighted earlier, card issuers now use automated scanners to review representment packages. To succeed, you must deliver irrefutable nuggets that trigger an auto-win:

- Matching Device ID + browser fingerprinting.

- GPS-stamped delivery photos and carrier API pings.

- Timestamped server logs showing the customer viewed the Return Policy and spent time on the checkout page before clicking "Pay."

- User session/engagement metadata

All these must tightly align with the reason code and issuer expectations. That’s why eCommerce veterans are moving from manual defense to automated intelligence.

What Happens When You Accept a Chargeback?

Accepting a dispute can be the correct decision when the claim is legitimate or when the transaction value does not justify the effort. Not every chargeback should be contested.

However, treating chargebacks as a cost of doing business hides their true financial impact. It turns one “easy” resolution into a painful impact on your bottom line.

Here’s what happens when you accept a false chargeback (and why that’s an expensive mistake for merchants):

- Lost Revenue: You refund the transaction amount, even if the product was delivered. Scammers use chargeback fraud to get freebies, retaining the product and the transaction amount.

- Chargeback Fees: The $15 to $100 fees eat into your margins. According to Mastercard, an average dispute costs merchants at least $74.

- Operational Cost: Time and resources dedicated to gathering evidence and responding to disputes divert resources from growth prospects.

- Strained Customer Relationship: Disputes, false and legitimate, often erode consumer trust. This makes repeat business impossible.

- Long-Term Damages: Brands with excessive chargebacks enter fraud monitoring programs, incur high processing fees, and even face account termination by card processors.

Put this in a better perspective. A $70 chargeback with a $25 fee and two 1.5 hours of staff time (at $20/hour) could cost you $125. This is far more than the original transaction amount. Now do the math for multiple cases, and you’ll see why chargeback costs sting!

What Are the Best Ways to Prevent Chargebacks?

Under programs like VAMP, chargeback prevention is a necessary risk-mitigation layer. It directly determines merchant viability. High-performing merchants treat prevention as infrastructure, not support. The best ways to prevent chargebacks include:

1. Risk-Based Authentication

3D Secure 2 helps neutralize fraud disputes by shifting liability to the issuer. It transmits rich contextual data while enabling frictionless authentication for low-risk transactions.

The 2026 best practice is to trigger 3DS2 only when risk signals warrant it (e.g., first-time buyers, high-value orders, or device or geolocation mismatches). That way, you preserve conversion while eliminating unauthorized-transaction exposure.

2. Issuer Context Injection

Most chargebacks begin as issuer inquiries, not accusations of fraud. When issuers lack context, they escalate by default.

Leading merchants proactively inject transaction clarity into issuer-facing systems:

- Recognizable merchant identity and item-level details

- Subscription status, renewal timing, and cancellation visibility

- Clear customer support paths for shoppers to contact you before their bank

Why it matters: Transactions that explain themselves are far less likely to become disputes, reducing friendly fraud before TC15 is ever generated.

3. Pre-Dispute Deflection

Prevention now includes intercepting disputes after the cardholder contacts their bank, but before the chargeback posts.

Tools like Chargeflow Alert and Chargeflow Prevent enable merchants to instantly refund low-value or high-risk disputes.

VAMP Advantage: Disputes resolved at this stage are typically excluded from VAMP calculations, protecting merchant standing.

4. Advanced Billing Transparency

A significant share of “friendly fraud” disputes stems from confusion, not malicious intent.

High-impact controls include:

- Enhanced billing descriptors aligned with the customer-facing brand

- Digital receipt delivery and in-bank purchase confirmations

Clarity at the point of recognition prevents disputes from forming.

5. Data Enrichment

While Compelling Evidence 3.0 is a recovery framework, prevention starts at data capture.

Merchants must consistently collect:

- Device identifiers (UUID)

- IP address and geolocation

- Shipping or accessing data

Chargeback prevention is no longer about stopping bad customers. Without this foundation, both prevention and recovery fail.

Final Thoughts on How Chargebacks Work

Chargebacks have evolved from isolated disputes into a systemic risk shaped by issuer automation, network policies, and portfolio-level enforcement. Acquirers are now pressured to keep their entire portfolio under 0.5%. Every dispute affects not only a single merchant but also the broader ecosystem.

Merchants who treat chargebacks as exceptions risk revenue, processing privileges, and brand trust. Those who treat them as infrastructure stay compliant, protect margins, and grow with confidence. That’s how chargebacks work today

Early, precise, and systematic engagement is the current standard. Category‑leading merchants meet that objective with platforms like Chargeflow.

FAQs:

How does a credit card chargeback work?

A credit card chargeback is a consumer protection process that allows a cardholder to request payment reversal from their bank due to fraud, non-receipt of goods, or service dissatisfaction. If the card issuer finds the cardholder’s request to be legitimate after their investigation, they’ll reverse the funds from the merchant with a non-negotiable chargeback fee. The merchant can then dispute the chargeback by presenting compelling evidence.

How does a bank chargeback work?

A bank chargeback is a transaction reversal filed by the financial institution that provided the customer’s card when a technical error occurs during transaction processing. Bank chargebacks often happen without the cardholder or merchant being aware of it. In addition to cardholder-initiated chargebacks, banks can also initiate them, but the dispute cycle is usually the same.

How does a chargeback work with PayPal?

PayPal has three processes through which cardholders can seek remediation for transaction disputes: dispute, claim, and chargeback. The distinction is that unresolved disputes can be escalated to a claim, and PayPal decides the outcome of the case through its internal "Resolution Center." The card issuer handles chargebacks. When a customer disputes a transaction processed through PayPal to their bank, PayPal acts as a liaison between the merchant and the customer’s bank. Their fraud specialists will communicate with the issuer on your behalf throughout the chargeback process. Again, if the user filed the dispute through their credit card issuer instead of PayPal, the card issuer’s rules take precedence, and PayPal’s "Seller Protection" only applies if specific shipping and tracking criteria are met.

What happens during a chargeback dispute?

During a dispute, funds are held in escrow. Both parties provide evidence, such as receipts, logs, communications, etc. The issuing bank then decides to either return the funds to the merchant or make the reversal permanent.

How long does a chargeback take to resolve?

A typical dispute takes 4 to 12 weeks. However, if it reaches the arbitration stage, it can take up to 6 months to reach a final, binding verdict. That’s why chargeback automation has the most economic upside, as it ensures you can dispute the case with a maximal recoverability guarantee without lifting a finger.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 15,000 merchants.

.png)

.jpg)

Questions?

we’ve got answers.

Chargeflow collects data from dozens of third party signals, automatically. This allows for much more coverage and much better win rates because the evidence submitted is much more comprehensive and compelling.

Chargeflow collects data like order info, customer messages, and payment details. It builds a full dispute case for you, so you don’t have to lift a finger.

Yes! Chargeflow works with 50+ payment processors. That means one tool for all your chargebacks, no matter how you process payments.

You only pay a percentage of the revenue we help you recover. No upfront fees, no subscriptions — just success-based pricing.

Yes. Chargeflow is SOC 2 Type 2, GDPR, and ISO certified. We use top security standards to keep your data safe.

need more help?

Have a question? We’re here to help. Just hit the chat button to initiate a conversation with support.