%201.svg)

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 15,000 merchants.

Chargeback protection at its core is about control. It’s the mix of tools, services, and structured workflows that help merchants prevent chargebacks, reduce dispute ratios, and protect long-term payment stability. Merchant chargeback protection can include fraud screening, chargeback alerts, guarantees, and end-to-end dispute automation. The best chargeback protection strategies focus first on prevention, second on early intervention, and only then on recovery. Chargeback protection is not about winning more disputes. It is about controlling risk before it compounds.

Chargebacks are no longer isolated operational issues. They directly affect revenue, dispute ratios, monitoring program exposure, and long-term processing access.

Beyond lost sales, chargebacks create:

- Non-refundable dispute fees

- Operational strain

- Card network scrutiny

- Increased processing costs

- Potential account termination

A $120 chargeback can quickly reach a true cost of $200–$250 once fees, internal labor, and ratio impact are factored in. To put this in perspective, even a smaller $70 chargeback, combined with a $25 fee and 3 hours of staff time, instantly becomes a $125 loss. Multiply that by 40 or 50 disputes per month, and chargebacks become a structural risk, not a transactional inconvenience.

This is where many merchants miscalculate. They evaluate chargebacks individually. Card networks evaluate them cumulatively.

Chargeback protection exists to reduce that risk. For ecommerce businesses, understanding what chargeback protection is and how it works is essential to maintaining payment stability as dispute volumes rise.

This guide explains:

- What is chargeback protection

- How chargeback protection for merchants works

- The difference between merchant chargeback protection and fraud protection

- What qualifies under chargeback protection

- How to evaluate the best chargeback protection options

What is Chargeback Protection?

Chargeback protection is a combination of tools and processes designed to help merchants prevent, manage, or reduce the impact of chargebacks.

At its core, chargeback protection focuses on reducing disputes before they occur, minimizing losses when disputes happen, and protecting merchants from excessive chargeback rates.

Chargeback protection may include:

- Chargeback fraud protection and transaction screening

- Chargeback alerts and early dispute notifications

- Automated refund and dispute reconciliation

- Chargeback guarantees or reimbursement programs

- End-to-end dispute lifecycle automation, including representment

Not all chargeback protection solutions work the same way. Some focus only on fraud prevention at checkout, while others are designed to manage the full chargeback lifecycle after a transaction is completed.

The difference is critical. A fraud-only solution protects transactions. A true chargeback protection system protects your ratios.

Understanding this distinction is critical when evaluating chargeback protection ecommerce solutions.

Chargeback Protection for Merchants: Why It Matters

Chargeback protection for merchants matters because chargebacks impact far more than individual transactions.

Each chargeback can result in:

- Lost revenue from the original sale

- Non-refundable chargeback fees

- Increased chargeback ratios

- Placement into monitoring programs

- Higher processing costs or account termination

Merchant chargeback protection helps businesses:

- Reduce dispute volume

- Protect payment processing privileges

- Lower operational burden

- Maintain long-term revenue stability

Merchants can win individual disputes and still face penalties if overall chargeback volume remains high.

Winning disputes feels productive. Controlling ratios is what keeps accounts alive.

How Chargeback Protection Works for Ecommerce and Credit Cards

Chargeback protection for ecommerce and credit card transactions works across multiple stages of the customer journey.

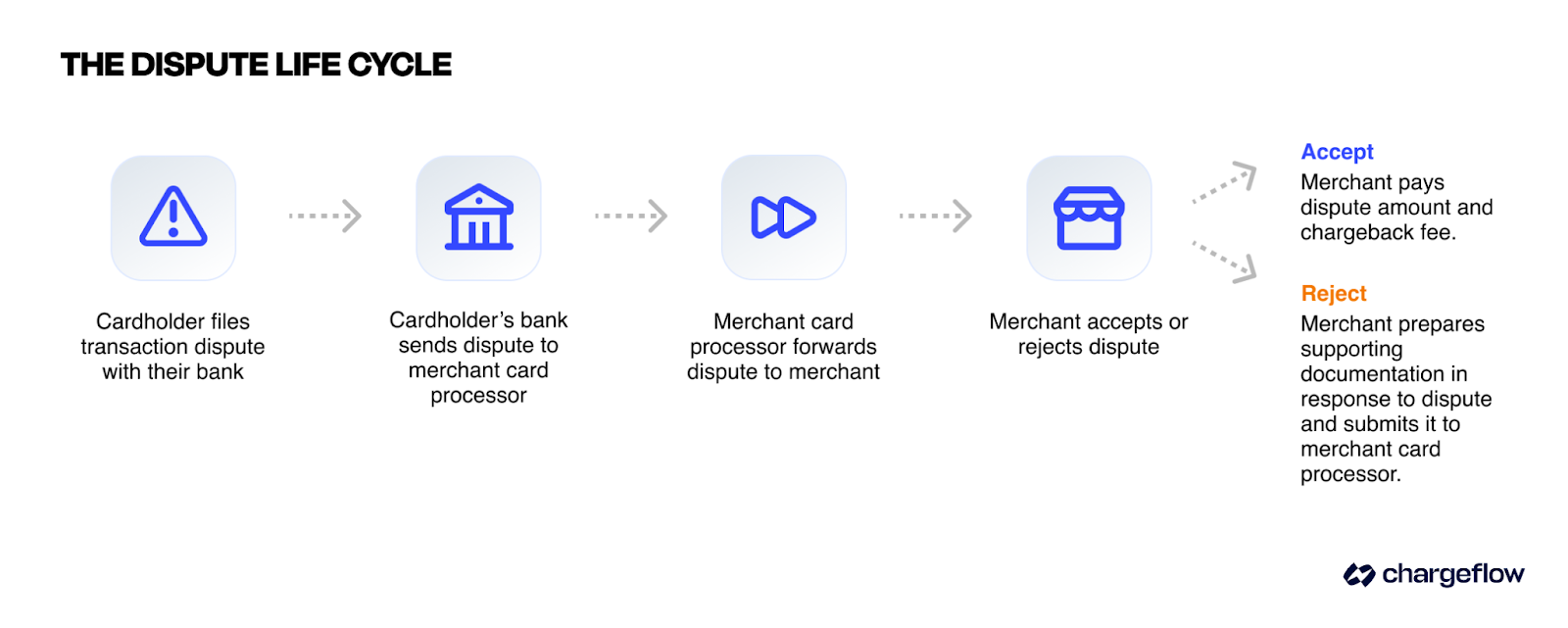

The Chargeback Process: From Dispute to Resolution

Before Checkout

Fraud detection systems evaluate transaction risk to prevent stolen card usage and high-risk orders.

After Purchase

Chargeback protection may include:

- Alerts when a dispute is about to be filed

- Refund intervention to prevent chargebacks

- Automated dispute intake and workflow management

- Representment and evidence submission

Credit card chargeback protection must align with Visa and Mastercard rules, including:

- Reason codes

- Response timelines

- Evidence standards

If a protection system does not align with issuer compliance rules, it fails at the most expensive stage: recovery.

Merchant Chargeback Protection vs. Fraud Protection: Key Differences

Fraud protection and chargeback protection are related but not the same.

Fraud protection focuses on stopping unauthorized or high–risk transactions before checkout. Chargeback protection focuses on managing disputes after a transaction has already occurred.

Key differences:

Many merchants believe fraud tools are enough. They are not. Fraud tools reduce unauthorized transactions. They do not control dispute ratios driven by refunds, delivery issues, or subscription complaints.

Eligible vs. Ineligible Chargebacks Under Chargeback Protection

Not all chargebacks are covered by chargeback protection programs.

Eligibility depends on:

- The chargeback reason code

- The type of protection in place (fraud-only vs. end-to-end)

- Whether required data and policies were present at the time of purchase

- Compliance with the provider’s operational and documentation requirements

Commonly eligibility:

- Certain fraud reason codes

- Transactions that met predefined risk criteria

Commonly ineligibility:

Chargebacks are often excluded from protection when they involve:

- Non-receipt disputes without delivery confirmation

- “Not as described” or product dissatisfaction disputes

- Duplicate charges, no-shows, or subscription cancellations

- Transactions missing required documentation or policy disclosures

This is one of the most misunderstood areas of merchant protection. Coverage is conditional. It is not universal.

What Information Merchants Must Provide for Chargeback Protection

Chargeback protection is conditional. Coverage depends on the merchant’s ability to provide accurate, verifiable data that meets issuer and provider requirements.

Most chargeback protection programs require merchants to maintain:

- Accurate billing descriptors that clearly identify the business

- Clear refund and cancellation policies are displayed before checkout

- Proof of delivery or access, where applicable

- Customer communication records, including confirmations and support interactions

- Authentication and transaction data, such as IP, device, or login details

Failure to provide required information can invalidate protection coverage, even when the underlying dispute is defensible. In many cases, protection is denied not because a merchant was wrong, but because required data was missing, incomplete, or unavailable at the time of review.

Chargeback Protection Insurance and Coverage Models

Some chargeback protection solutions operate as insurance-style coverage models.

These models typically:

- Approve or decline transactions at checkout

- Guarantee reimbursement for approved orders

- Charge fees based on transaction volume, approval rate, or risk profile

While chargeback protection insurance can reduce financial exposure, it does not necessarily reduce:

- Chargeback volume

- Operational workload

- Monitoring program risk

Merchants should understand whether a protection solution:

- Prevents disputes from occurring

- Reimburse losses after disputes happen

- Manages the full chargeback process end-to-end

Insurance protects revenue. It does not automatically protect ratios.

Merchants should evaluate whether a solution:

- Prevents disputes

- Reimburses losses

- Manages chargebacks end-to-end

Best Chargeback Protection Options for Ecommerce Businesses

The best chargeback protection options depend on dispute drivers, risk tolerance, and operational capacity.

Protection Models Compared:

Fraud Prevention Platforms with Guarantees

Best for merchants facing primarily fraud-driven chargebacks. These reduce unauthorized transactions but do not address service disputes or friendly fraud.

Chargeback alerts and network tools

Best for early intervention. Alerts create a refund window before disputes finalize. Coverage depends on issuer participation.

End-to-end ecommerce chargeback protection platforms

Best for merchants facing high dispute volume across fraud, friendly fraud, and service claims.

These combine:

- Fraud screening

- Alerts

- Refund reconciliation

- Representment automation

- Performance analytics

The best chargeback protection is not defined by reimbursement alone. It is defined by how effectively it controls dispute volume and protects long-term processing stability.

What “best chargeback protection” really means

The best chargeback protection is not defined by a single feature. It is defined by how well a solution:

- It reduces dispute volume

- It protects your dispute ratio

- It limits financial exposure

- It scales operationally

Merchants under 0.3% dispute rate may survive on fraud plus alerts.

Merchants near monitoring thresholds require ratio-first protection, not reimbursement-first models.

Point solutions can help reduce specific risks.

Comprehensive systems protect long-term payment stability.

Chargeback Fraud Protection and Risk Reduction

Chargeback fraud protection focuses on reducing disputes caused by:

- Stolen card usage

- Account takeovers

- Friendly fraud

Effective chargeback fraud protection includes:

- Identity and device verification

- Behavioral analysis

- Transaction monitoring

- Post-purchase usage and fulfillment validation

Fraud prevention reduces one major category of disputes, but it must be paired with post-purchase protection to fully control chargeback risk.

Main Causes of Chargebacks and How Protection Helps

Most chargebacks fall into a small number of recurring categories. Understanding these causes helps merchants choose the right chargeback protection approach.

Common causes of chargebacks include:

- Fraud-related disputes from stolen cards or account takeovers

- Friendly fraud, where cardholders do not recognize or remember a purchase

- Non-receipt claims caused by delivery issues or delays

- Product or service dispute, such as “not as described” or dissatisfaction

- Subscription and billing disputes related to unclear terms or cancellations

Chargeback protection helps by addressing these causes at different stages of the transaction lifecycle.

How chargeback protection reduces risk:

- Fraud protection reduces unauthorized transactions before checkout

- Chargeback alerts allow early intervention before disputes escalate

- Refund automation resolves issues before banks become involved

- Dispute management tools ensure valid disputes are defended correctly

No single tool eliminates all challenges. Protection works best when it targets the specific drivers behind a merchant’s disputes.

The Impact of High Chargeback Rates on Merchants

High chargeback rates affect far more than short-term revenue.

When chargeback thresholds are exceeded, merchants may face:

- Placement into Visa or Mastercard monitoring programs

- Higher processing fees and rolling reserves

- Increased scrutiny from acquiring banks

- Limits on payment method availability

- Termination of merchant accounts in severe cases

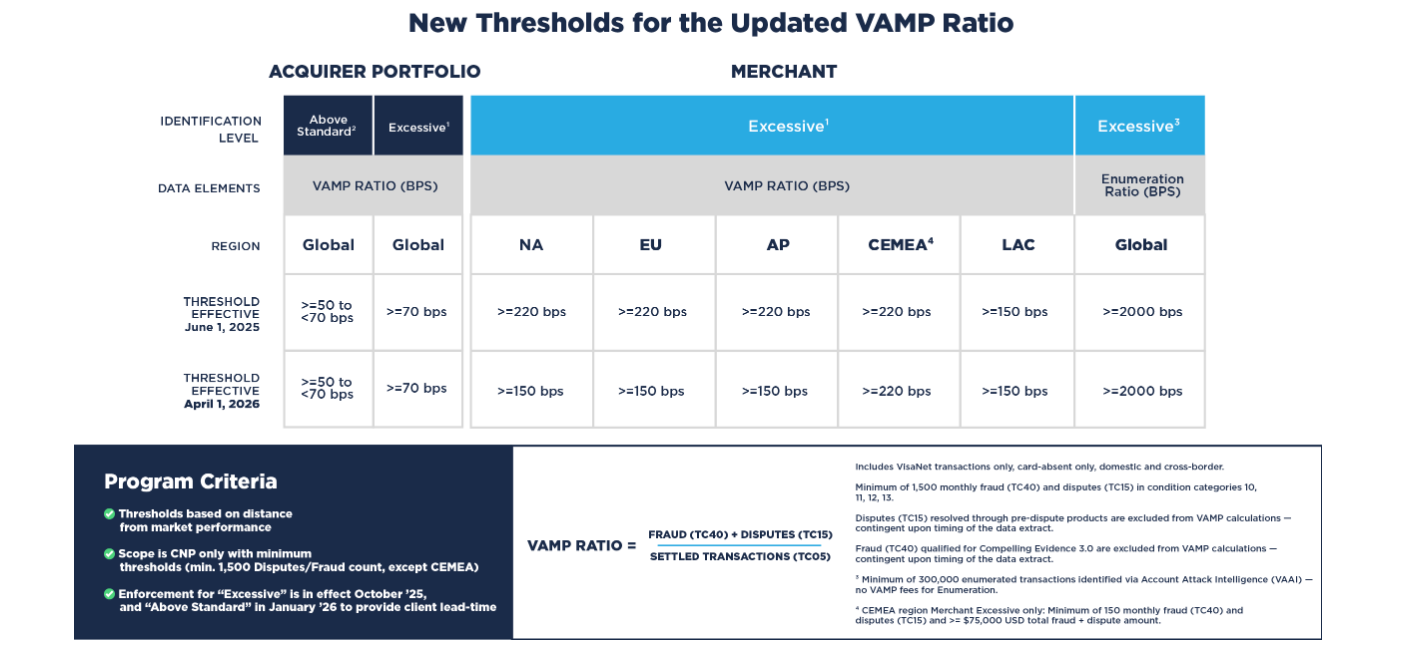

Visa’s updated VAMP thresholds for 2025–2026 significantly tighten acceptable dispute ratios.

Networks evaluate merchants mechanically. Deadlines and ratios are system-driven, not negotiable.

Below is a breakdown of Visa’s updated VAMP thresholds for 2025-2026, illustrating how dispute ratios are now evaluated globally.

Even merchants that win individual disputes can suffer penalties if overall chargeback volume remains high.

This is why chargeback protection is not only about recovery. It is about controlling ratios, maintaining compliance, and protecting long-term payment access.

For ecommerce merchants, sustained high chargeback rates are one of the fastest paths to processing instability.

Key Aspects of an Effective Chargeback Protection Strategy

An effective chargeback protection strategy is layered and intentional. It does not rely on a single tool or promise.

Strong strategies include:

- Pre-purchase fraud screening

- Clear refund and cancellation policies

- Chargeback alerts

- Automated refund reconciliation

- Structured representment

- Performance tracking

Prevention should always be prioritized over recovery. Every avoided chargeback protects ratios, processor trust, and future revenue.

Chargebacks cannot be eliminated. But they can be controlled.

Chargeback Protection Is About Control, Not Just Coverage

Chargeback protection is often misunderstood as insurance or reimbursement.

In reality, the most valuable protection gives merchants control.

Control over:

- Which transactions are accepted

- How disputes are handled

- Chargeback ratios and compliance risk

- Long-term payment stability

Merchants that rely solely on reimbursement may recover revenue but still lose processing access.

The best chargeback protection for ecommerce businesses combines fraud screening, early alerts, automated dispute workflows, and performance visibility into a single operational system.

Understanding what chargeback protection is, and what it is not, allows merchants to choose solutions that protect revenue today and processing access tomorrow.

Take Control of Your Chargeback Risk

Chargeback protection is not about reacting faster. It is about building a system that prevents avoidable disputes, controls ratios, and protects long-term processing stability.

If your dispute rate is rising, if monitoring thresholds are tightening, or if internal teams are overwhelmed by manual workflows, it may be time to evaluate whether your current protection model truly protects your ratios.

Schedule a demo to see how automated chargeback protection can reduce dispute volume, protect compliance thresholds, and recover revenue at scale.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 15,000 merchants.

.png)

Questions?

we’ve got answers.

Chargeflow collects data from dozens of third party signals, automatically. This allows for much more coverage and much better win rates because the evidence submitted is much more comprehensive and compelling.

Chargeflow collects data like order info, customer messages, and payment details. It builds a full dispute case for you, so you don’t have to lift a finger.

Yes! Chargeflow works with 50+ payment processors. That means one tool for all your chargebacks, no matter how you process payments.

You only pay a percentage of the revenue we help you recover. No upfront fees, no subscriptions — just success-based pricing.

Yes. Chargeflow is SOC 2 Type 2, GDPR, and ISO certified. We use top security standards to keep your data safe.

need more help?

Have a question? We’re here to help. Just hit the chat button to initiate a conversation with support.